Gold World News Flash |

- Gold’s Key Level $1,278 Needs To Hold

- Ellen Brown: Banks Will Take Deposits in the Coming Financial Meltdown, LIBOR Rate Rigging and More

- Japan Proves That Central Banks Cannot Produce Growth With QE

- Collapse Of Western Ponzi Scheme To Send Gold Skyrocketing

- A game-changer the ‘peons’ could control

- Safe Deposit Boxes Are Not Safe for Silver & Gold Buyers

- Chinese gangs implicated in India gold smuggling

- HSBC China PMI Indicates 4th Month Of Contraction As Yuan Weakens To Fresh 16 Months Lows

- US Navy Makes Gas from Seawater

- The Gold Price Lost $7.40 Today and Closed on the Comex at $1,280.60

- The Gold Price Lost $7.40 Today and Closed on the Comex at $1,280.60

- Guest Post: Piketty's Gold?

- Silver About To Move Higher and S&P Lower

- “Axis Of Power” As Countries Move To Link Currencies To Gold

- Dubai Global Gold Centre On Continuing Bullion Demand

- A Simple Strategy for Investing in the US Energy Boom

- Gold Daily and Silver Weekly Charts - Hotel California

- Gold Daily and Silver Weekly Charts - Hotel California

- Gold, Banks, & Interest Rates

- Dr.Copper Looking Grim

- Dr.Copper Looking Grim

- U.S. Dollar Crash In a Matter of Months?

- Silver Up, Stocks S&P Down

- Imagine if we had free prices!

- How gold was manipulated today in light trading

- Gold Prices Slip Back to 3-Week Lows as Stocks Rise, Oil Falls Despite Fresh Ukraine Tensions

- Tuesday Morning Links

- Time to Buy Silver, Again

- Time to Buy Silver, Again

- A Crisis vs. the REAL Crisis: Keep Your Eye on the Debt Ball

- America’s Pipe Dreams: Hollywood vs. Buffett

- Jim Rickards on the Death of Money, China, and Financial Warfare

| Gold’s Key Level $1,278 Needs To Hold Posted: 22 Apr 2014 11:30 PM PDT from KitcoNews: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ellen Brown: Banks Will Take Deposits in the Coming Financial Meltdown, LIBOR Rate Rigging and More Posted: 22 Apr 2014 10:02 PM PDT Can bank bail-ins come to America? Ellen Brown of the Web-of-Debt blog says, "It could, and I think it will." Brown, who has written two books on the advantages of public banking, contends, "They don't have any alternative if they are going to keep these banks alive. This is the solution: They just... [[ This is a content summary only. Visit http://www.GoldSilverNewsBlog.com or http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Japan Proves That Central Banks Cannot Produce Growth With QE Posted: 22 Apr 2014 10:00 PM PDT by Graham Summers, Gold Seek:

Their "way" involves rampant debt monetization, also called Quantitative Easing or QE. Indeed, the primary argument from the Keynesians as to why QE has thus far failed to generate a rip-roaring recovery is that none of the QE programs in place were large enough. Japan is where the Keynesian economic model rubber hit the road. In April 2013, the Bank of Japan announced a staggering $1.4 trillion QE program. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Collapse Of Western Ponzi Scheme To Send Gold Skyrocketing Posted: 22 Apr 2014 09:57 PM PDT  Today one of the most highly respected fund managers in Singapore told King World News that the collapse of the Western Ponzi scheme will send the price of gold skyrocketing. Grant Williams, who is portfolio manager of the Vulpes Precious Metals Fund, also discussed the coming implosion of the Western scheme as well as how the Russians and the Chinese positioning themselves ahead of this collapse. Today one of the most highly respected fund managers in Singapore told King World News that the collapse of the Western Ponzi scheme will send the price of gold skyrocketing. Grant Williams, who is portfolio manager of the Vulpes Precious Metals Fund, also discussed the coming implosion of the Western scheme as well as how the Russians and the Chinese positioning themselves ahead of this collapse.This posting includes an audio/video/photo media file: Download Now | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A game-changer the ‘peons’ could control Posted: 22 Apr 2014 07:40 PM PDT by Bill Rice, Jr., Silver Seek:

Why, one asks, would China suddenly reverse course and change a policy that it has now been aggressively pursuing for years? Such a scenario would not/does not make sense. No, any fair-minded observer has to assume that China has been acquiring and stockpiling gold for reasons it considers very important (and these reasons presumably have not, nor will not disappear). | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Safe Deposit Boxes Are Not Safe for Silver & Gold Buyers Posted: 22 Apr 2014 07:38 PM PDT Goldsilver | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Chinese gangs implicated in India gold smuggling Posted: 22 Apr 2014 07:20 PM PDT by Shivom Seth, MineWeb.com

Over the last few months, customs officials at the Rajiv Gandhi international Airport in Hyderabad, have detained more than 50 passengers and recovered approximately 80 kilograms of gold. On April 1, about 7.70 kilogram of gold was seized from two passengers by the Directorate of revenue intelliegence sleuths, which was the first instance to alert the investigating team about the role of the neighbouring nation. “Though it sounds incredulous, investigators have come across enough evidence to indicate that Chinese gangs are hiring operators in other countries and smuggling gold into Hyderabad, Kerala and other Indian cities,” said Kalyan Revella, Assistant Commissioner, Customs and Central Excise, at Hyderabad. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| HSBC China PMI Indicates 4th Month Of Contraction As Yuan Weakens To Fresh 16 Months Lows Posted: 22 Apr 2014 06:52 PM PDT HSBC's (Flash) China Manufacturing PMI for April met expectations at 48.3 - holding at its 2nd lowest in 20 months. This is the 4 month of contraction and 4th month without a beat of expectations. April's flash (preliminary) print rose modestly over March's 48.0 but all sub-indices remain weak though some 2nd derivatives are shifting. Employment is worsening at a faster pace and new export orders contracted. While the world waits open-mouthed for the next Chinese stimulus (which they have now explained will be limited and targeted and not 2009-style) and bloviators expound on last night's RRR cut for rural banks (remember, they do not have a liquidity issue, banks are hording PBOC cash and not lending - due to credit risk concerns), it seems no matter what the PMI (weak, weaker, or weakest) the reforms are being stuck to, CNY is being allowed to weaken, and no new avalanche of credit creation (commodity-backed or not) is coming anytime soon.

Most market participants believe HSBC's survey is more weighted towards small and medium-sized businesses than the official government data (which is likely more biased to SOEs and larger enterprises) and Markit's stratification description suggests a more accurate representation of the overall economy - therefore HSBC better reflects the tightening liquidity conditions than China's official data.

Overall the sub-indices are weak with some hope for the ever optimistic that the pace of collapse is slowing

CNY has dropped to fresh 14-month lows against the USD... At 6.2423, USDCNY is back to pre-QE4EVA levels in Dec 2012 - 6.40 next target

Charts: Bloomberg and Markit Economics | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| US Navy Makes Gas from Seawater Posted: 22 Apr 2014 05:14 PM PDT Follow ZeroHedge in Real-Time on FinancialJuice

Age-old myths and fantasies about turning stuff that was worthless into gold. Alchemists leaning over their cauldrons of bubbling brew in the dark recesses of the dungeon of some mythical castle somewhere unknown to mankind. Well, perhaps not so unknown and not so fantastical. Today, the US Navy has succeeded in transforming sea water into gasoline. No point in having sea water these days either for all the eco-warriors that will worry about the fauna and flora. My, oh my! Since when did people actually care what might happen to the fish in the sea or the plants? We have been shown for many a year now that it's the economy that counts; fuel and energy are the key-words of the 20th century and they are even more so in the 21st. Holy Cow! Damn the sea water, fill the barrels and turn it into gas! How can they do it? Simple: Seawater contains carbon dioxide and hydrogen. Separating them in H2O would mean being able to create hydrocarbons. Oil is just one form of hydrocarbon, that's all. The gasses are transformed into a fuel by using a process of gas-to-liquid using catalytic converters. Easy-peasy. Even the US Navy can do it! We wanted renewable energy, didn't we? Haven't we been harping on about the ethics of preserving our mode of consumption and at the same time not wasting our resources for years now? It's taken the US Navy decades, but now they have managed to power a small model plane. All that there's left for them to do is to produce it in industrial quantities. The proof-of-concept test was carried out in September 2013 atBlossom Point, Maryland on a model P-51 Mustang 2-stroke engine. It was made public just a few days ago. The US Navy relies on oil-based fuel for 289 vessels. There 72 submarines rely on nuclear power. Moving into a new era of producing enough gas to power those vessels would mean that there would be incredible savings to be made and thus less reliance on the Middle East or other countries for the source of energy. The idea would be that the vessels would be transformed into floating refineries that would transform seawater into their own energy source, thus doing away with the need to refuel with tankers in tow. The Navy has called it a "game-changer" and a "huge milestone". Strangely, it can power ships, it will power aircraft too on the aircraft-carriers, but the Navy says that after a decade of research they can't make cars run on it yet. Oh! Really? Does that mean the common and mortal American will have to continue digging in his pocket at the pump to get the tank filled with gas before he speeds off to the factory to produce…(what do we produce still in the USA?)? Right! So we'll have to bleed the planet dry, use it all up, spend all the money and then maybe then, just maybe, they will have come up with the miraculous solution that they will announce to us in a few decades. Nice! The predicted cost for the US Navy to fuel a jet has been estimated to work out to roughly $3-$6 per gallon. The US Navy has suggested that the project would come to commercial fruition within the next 7 to 10 years and that would mean that there would be removal of dependence on gas from other countries. But, what they fail to realize is that the object of a fight is not the important thing it's the reason why the punches get pulled. If we aren't fighting over gas in the future, then we'll be fighting over sea-water. There's lots of it on the planet, and everyone could get to it. But, whatever it is, if it's coveted, then it's a reason to go to war, invade, pillage, burn and plunder. If that new object is going to be seawater, so be it. Just as well they decided to use the seawater. Apparently, the seas and oceans are rising in level due to the melting of the ice caps. Hey, you know, the Americans will end up being the saviors of the planet, ecologically-speaking! There's 96% of the world's water in the oceans today. Water covers 70% of the planet. The US Navy has 332, 519, 000 cubic miles of water to turn into fuel now. Who cares about the fish? Having trouble working out how many gallons that works out to be? It's simple: 352, 670, 000, 000, 000, 000, 000. That's going to take a hell of a long time at the gas pump, isn't it? Originally posted: US Navy Makes Gas from Seawater Day Trading Data Sheets Futures and Forex

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Gold Price Lost $7.40 Today and Closed on the Comex at $1,280.60 Posted: 22 Apr 2014 05:10 PM PDT

Since I took off during Holy Week and Easter Monday, I'll give y'all a report today for the last week, which may set our minds straight for the rest of the week. The GOLD PRICE lost $7.40 today and closed Comex at $1,280.60. Silver gained -- get ready -- one cent to close at 1935.1 cents. Silver and gold price momentum is down, clearly, but without a lot of conviction. That is, they are running out of downward steam. A ratio today at 66.177 shows that the SILVER PRICE has played the weak sister. I expect the GOLD PRICE might hit $1,270 before it turns and silver 1900c. Dow below silver must not drop below 1890c nor gold below $1,260. Clear rally confirmations occur when gold betters $1,331.40 and silver 2050c. Think of silver and gold (and stocks) as a huge bus turning -- it's a slow, tedious business. Unless prices gainsay it, my operating interpretation remains that the June - December lows constituted a double bottom, and silver and gold won't again drop below those prices. Before I start on markets, I've got to hack up a bone. This morning I was driving from my home (The Shoe) to the office torturing myself by listening to National Pompous Radio, a.k.a., National Proletarian Radio. As I listened to their advertisement ( it couldn't properly be called a newscast) for extending early childhood education, a.k.a., pre-pre-pre-kindergarten, I realized that every single clause was a propaganda lie. Yes, it was all outright lies, presented as if it were truth. They claimed that institutionalizing little children at an earlier age would somehow pay "benefits." (Remember how much you liked going to school as an intimidated six year old? Imagine how much more fun that would be as a 4 year old.) They called these expenditures of tax funds extorted at gunpoint from citizens "investing." They called all this "free" when clearly somebody must pay for it. Every claim was manifestly untrue as a matter of fact. All this is presented without every asking, indeed, to avoid enabling anyone to ask, the threshold question, Is any of this necessary? Is public education (really "state-run child indoctrination force-paid by taxpayers") really necessary? Why is it a crime for private people to kidnap children and indoctrinate them, but not for the state? Then to pour salt in my bleeding intellectual wounds, they call this "democracy." But then again, maybe that's the ONLY true thing they said. Hack, hack! Okay, that bone's out of my throat, let's move to markets. Stepping back form the charts a little, the silver and gold rally that began the year has cycled downward and stocks that were falling have turned up. Play this out against the backdrop of a probable double bottom (June 2013 - Dec 2013) closing the long correction in silver and gold, and a 300 year cyclical top coming in stocks probably in May. In monetary terms the Fed since 2008 has roughly quadrupled the US money supply, but has managed to (1) make the banks balance sheets whole, the true aim of Quantitative Easing and (2) quarantine most of the inflation out of consumer prices and into asset prices (stocks) and bank reserves. By manipulating stocks higher by inflation, the Fed has set the stage for a worse crash to come, and enormously higher silver and gold prices. Currency markets are drifting sideways in broad ranges, which probably reflects the terror of the Nice Government Men and central bank criminals. Above all things, they want stability. But the trump card in the reasoning process that tries to make sense of all this is, WHAT HAS CHANGED? WHAT IS ABOUT TO CHANGE? What voice of reason is calling for economic, government-budget, monetary, or financial market reform? Where is that Solon who will straighten this out? He ain't in the US congress, and he ain't in the European parliament, and if he's anywhere he's sure enough well camouflaged. As long as a cause continues, it begets the same outcome. The causes have not changed, so the outcome will not change. That puts the world's strongest powers -- governments and central banks -- squarely on the side of silver and gold investors, because they have proven through crisis after crisis that they will inflate until they die, and inflation drives silver and gold higher. Now in the shorter term . . . After a brutal correction stocks are approaching again their last highs. May could see them exceed those old highs, but the end of stocks draweth nigh, and 'twill be bloody. In the last week the Dow rose 1.5%, the S&P500 2%. Dow today rose 65.12 (0.4%) to 16,514.37. S&P500 climbed 7.66 (0.41% to 1,879.55. The last week's stock strength and metals weakness has played hob with the Dow in Gold and Dow in silver. Thanks to lagging silver the Dow in Silver has risen nearly to its high for the move seen at December's end, 853.15 oz. Today it closed at 851.70 oz (s$1,101.19 silver dollars). It appears to be in the last leg of its rise, and could easily rise to a new high for this move, say, 870 oz (S$1,124.85). Dow in Gold chart offers a different pattern. From December to the March low, the Dow in gold fell from 13.8 oz to 11.62, then recovered by 1 April to 12.92, about 2/3 of the fall before. It fell again, to 12.16 oz in mid-April, and now has rallied today to 12.87 oz (G$266.05 gold dollars). I expect it will rise a bit further, but not to a new high. In the last 12 days the US dollar index has fallen nearly to the last low, then recovered. Right now it's stymied at the confluence of the 20 and 50 day moving averages (80.07 and 80.06), staring at 'em like a calf staring at a new gate. After rising six trading days, the dollar fell back today 5 basis points to 79.99. Basically the buck has been range-trading since August, but in the last two months the range has narrowed and weakened. The manic-depressive euro has been Range-trading, too, but hasn't been able to make good its upside escape. Today at $1.3805 it's above its 20 and 50 DMAs, but within a downtrend of lower highs and lower lows. Nothing to cheer about there. Yen has been perfectly range bound, 99.24 - 96.05, in a slightly declining channel since 1 February. Presently it is crumpling yet again. Recall that all the central banks' and the US government's grand plans hang upon one slender hook: suppressed interest rates. 10 days ago it looked as if the 10 year treasury note yield would break down, but it caught and scrabbled its way out of danger. Today it closed 2.726%, up 0.18%. Last June it broke out to the upside, and although it lapsed into a consolidating range the rest of the year, the longer trend points up. Higher interest rates will tear all those grand plans off the hook and shred them. Aurum et argentum comparenda sunt -- -- Gold and silver must be bought. - Franklin Sanders, The Moneychanger The-MoneyChanger.com © 2014, The Moneychanger. May not be republished in any form, including electronically, without our express permission. To avoid confusion, please remember that the comments above have a very short time horizon. Always invest with the primary trend. Gold's primary trend is up, targeting at least $3,130.00; silver's primary is up targeting 16:1 gold/silver ratio or $195.66; stocks' primary trend is down, targeting Dow under 2,900 and worth only one ounce of gold or 18 ounces of silver. or 18 ounces of silver. US $ and US$-denominated assets, primary trend down; real estate bubble has burst, primary trend down. WARNING AND DISCLAIMER. Be advised and warned: Do NOT use these commentaries to trade futures contracts. I don't intend them for that or write them with that short term trading outlook. I write them for long-term investors in physical metals. Take them as entertainment, but not as a timing service for futures. NOR do I recommend investing in gold or silver Exchange Trade Funds (ETFs). Those are NOT physical metal and I fear one day one or another may go up in smoke. Unless you can breathe smoke, stay away. Call me paranoid, but the surviving rabbit is wary of traps. NOR do I recommend trading futures options or other leveraged paper gold and silver products. These are not for the inexperienced. NOR do I recommend buying gold and silver on margin or with debt. What DO I recommend? Physical gold and silver coins and bars in your own hands. One final warning: NEVER insert a 747 Jumbo Jet up your nose. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Gold Price Lost $7.40 Today and Closed on the Comex at $1,280.60 Posted: 22 Apr 2014 05:10 PM PDT

Since I took off during Holy Week and Easter Monday, I'll give y'all a report today for the last week, which may set our minds straight for the rest of the week. The GOLD PRICE lost $7.40 today and closed Comex at $1,280.60. Silver gained -- get ready -- one cent to close at 1935.1 cents. Silver and gold price momentum is down, clearly, but without a lot of conviction. That is, they are running out of downward steam. A ratio today at 66.177 shows that the SILVER PRICE has played the weak sister. I expect the GOLD PRICE might hit $1,270 before it turns and silver 1900c. Dow below silver must not drop below 1890c nor gold below $1,260. Clear rally confirmations occur when gold betters $1,331.40 and silver 2050c. Think of silver and gold (and stocks) as a huge bus turning -- it's a slow, tedious business. Unless prices gainsay it, my operating interpretation remains that the June - December lows constituted a double bottom, and silver and gold won't again drop below those prices. Before I start on markets, I've got to hack up a bone. This morning I was driving from my home (The Shoe) to the office torturing myself by listening to National Pompous Radio, a.k.a., National Proletarian Radio. As I listened to their advertisement ( it couldn't properly be called a newscast) for extending early childhood education, a.k.a., pre-pre-pre-kindergarten, I realized that every single clause was a propaganda lie. Yes, it was all outright lies, presented as if it were truth. They claimed that institutionalizing little children at an earlier age would somehow pay "benefits." (Remember how much you liked going to school as an intimidated six year old? Imagine how much more fun that would be as a 4 year old.) They called these expenditures of tax funds extorted at gunpoint from citizens "investing." They called all this "free" when clearly somebody must pay for it. Every claim was manifestly untrue as a matter of fact. All this is presented without every asking, indeed, to avoid enabling anyone to ask, the threshold question, Is any of this necessary? Is public education (really "state-run child indoctrination force-paid by taxpayers") really necessary? Why is it a crime for private people to kidnap children and indoctrinate them, but not for the state? Then to pour salt in my bleeding intellectual wounds, they call this "democracy." But then again, maybe that's the ONLY true thing they said. Hack, hack! Okay, that bone's out of my throat, let's move to markets. Stepping back form the charts a little, the silver and gold rally that began the year has cycled downward and stocks that were falling have turned up. Play this out against the backdrop of a probable double bottom (June 2013 - Dec 2013) closing the long correction in silver and gold, and a 300 year cyclical top coming in stocks probably in May. In monetary terms the Fed since 2008 has roughly quadrupled the US money supply, but has managed to (1) make the banks balance sheets whole, the true aim of Quantitative Easing and (2) quarantine most of the inflation out of consumer prices and into asset prices (stocks) and bank reserves. By manipulating stocks higher by inflation, the Fed has set the stage for a worse crash to come, and enormously higher silver and gold prices. Currency markets are drifting sideways in broad ranges, which probably reflects the terror of the Nice Government Men and central bank criminals. Above all things, they want stability. But the trump card in the reasoning process that tries to make sense of all this is, WHAT HAS CHANGED? WHAT IS ABOUT TO CHANGE? What voice of reason is calling for economic, government-budget, monetary, or financial market reform? Where is that Solon who will straighten this out? He ain't in the US congress, and he ain't in the European parliament, and if he's anywhere he's sure enough well camouflaged. As long as a cause continues, it begets the same outcome. The causes have not changed, so the outcome will not change. That puts the world's strongest powers -- governments and central banks -- squarely on the side of silver and gold investors, because they have proven through crisis after crisis that they will inflate until they die, and inflation drives silver and gold higher. Now in the shorter term . . . After a brutal correction stocks are approaching again their last highs. May could see them exceed those old highs, but the end of stocks draweth nigh, and 'twill be bloody. In the last week the Dow rose 1.5%, the S&P500 2%. Dow today rose 65.12 (0.4%) to 16,514.37. S&P500 climbed 7.66 (0.41% to 1,879.55. The last week's stock strength and metals weakness has played hob with the Dow in Gold and Dow in silver. Thanks to lagging silver the Dow in Silver has risen nearly to its high for the move seen at December's end, 853.15 oz. Today it closed at 851.70 oz (s$1,101.19 silver dollars). It appears to be in the last leg of its rise, and could easily rise to a new high for this move, say, 870 oz (S$1,124.85). Dow in Gold chart offers a different pattern. From December to the March low, the Dow in gold fell from 13.8 oz to 11.62, then recovered by 1 April to 12.92, about 2/3 of the fall before. It fell again, to 12.16 oz in mid-April, and now has rallied today to 12.87 oz (G$266.05 gold dollars). I expect it will rise a bit further, but not to a new high. In the last 12 days the US dollar index has fallen nearly to the last low, then recovered. Right now it's stymied at the confluence of the 20 and 50 day moving averages (80.07 and 80.06), staring at 'em like a calf staring at a new gate. After rising six trading days, the dollar fell back today 5 basis points to 79.99. Basically the buck has been range-trading since August, but in the last two months the range has narrowed and weakened. The manic-depressive euro has been Range-trading, too, but hasn't been able to make good its upside escape. Today at $1.3805 it's above its 20 and 50 DMAs, but within a downtrend of lower highs and lower lows. Nothing to cheer about there. Yen has been perfectly range bound, 99.24 - 96.05, in a slightly declining channel since 1 February. Presently it is crumpling yet again. Recall that all the central banks' and the US government's grand plans hang upon one slender hook: suppressed interest rates. 10 days ago it looked as if the 10 year treasury note yield would break down, but it caught and scrabbled its way out of danger. Today it closed 2.726%, up 0.18%. Last June it broke out to the upside, and although it lapsed into a consolidating range the rest of the year, the longer trend points up. Higher interest rates will tear all those grand plans off the hook and shred them. Aurum et argentum comparenda sunt -- -- Gold and silver must be bought. - Franklin Sanders, The Moneychanger The-MoneyChanger.com © 2014, The Moneychanger. May not be republished in any form, including electronically, without our express permission. To avoid confusion, please remember that the comments above have a very short time horizon. Always invest with the primary trend. Gold's primary trend is up, targeting at least $3,130.00; silver's primary is up targeting 16:1 gold/silver ratio or $195.66; stocks' primary trend is down, targeting Dow under 2,900 and worth only one ounce of gold or 18 ounces of silver. or 18 ounces of silver. US $ and US$-denominated assets, primary trend down; real estate bubble has burst, primary trend down. WARNING AND DISCLAIMER. Be advised and warned: Do NOT use these commentaries to trade futures contracts. I don't intend them for that or write them with that short term trading outlook. I write them for long-term investors in physical metals. Take them as entertainment, but not as a timing service for futures. NOR do I recommend investing in gold or silver Exchange Trade Funds (ETFs). Those are NOT physical metal and I fear one day one or another may go up in smoke. Unless you can breathe smoke, stay away. Call me paranoid, but the surviving rabbit is wary of traps. NOR do I recommend trading futures options or other leveraged paper gold and silver products. These are not for the inexperienced. NOR do I recommend buying gold and silver on margin or with debt. What DO I recommend? Physical gold and silver coins and bars in your own hands. One final warning: NEVER insert a 747 Jumbo Jet up your nose. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 22 Apr 2014 05:03 PM PDT Originally posted at The New York Sun, With all that has been written in respect to Thomas Piketty's new book, “Capital,” you would think that someone — Paul Krugman, say, or Jonathan Chait or David Brooks or Hendrik Hertzberg; we’re not worried about who it might be so much as someone among the liberal intelligentsia — would have remarked on an odd coincidence of timing. We’re speaking here of the timing of the rapid rise of the blasted inequality over which Professor Piketty is so upset. After all, this inequality has become the cause celebre of the season for President Obama and his entire political party. It’s the issue of the hour. Yet when it comes to the timing at which this phenomenon presented itself, nada. Omerta. Well, feature the chart that Professor Piketty publishes showing inequality in America. This appears in the book at figure 9.8; a similar version, shown alongside here, is offered on his Web site. It’s an illuminating chart. It shows the share of national income of the top decile of the population. It started the century at a bit above 40% and edged above 45% in the Roaring Twenties. It plunged during the Great Depression and edged down in World War II, and then steadied out, until we get to the 1970s. Something happened then that caused income inequality to start soaring. The top decile's share of income went from something like 33% in 1971 to above 47% by 2010.

Hmmm. What could account for that? Could it be the last broadcast of the “Lawrence Welk Show?” Or the blast off of the Apollo 14 mission to the Moon? Or could it have something to do with the mysterious D.B. Cooper, who bailed out of the plane he hijacked, never to be seen again? A timeline of 1971 offers so many possibilities. But, say, what about the possibility that it was in the middle of 1971, in August, that America closed the gold window at which it was supposed to redeem in specie dollars presented by foreign central banks. That was the default that ended the era of the Bretton Woods monetary system. That’s the default that opened the age of fiat money. Or the era that President Nixon supposedly summed up in with Milton Friedman’s immortal words, “We’re all Keynesians now.” This is an age that has seen a sharp change in unemployment patterns. Before this date, unemployment was, by today’s standards, low. This was a pattern that held in Europe (these columns wrote about it in “George Soros’ Two Cents”) and in America (“Yellen’s Missing Jobs”). From 1947 to 1971, unemployment in America ran at the average rate of 4.7%; since 1971 the average unemployment rate has averaged 6.4%. Could this have been a factor in the soaring income inequality that also emerged in the age of fiat money? This is the question the liberals don’t want to discuss, even acknowledge. They are never going to get it out of their heads that the gold standard is a barbarous relic. They have spent so much of their capital ridiculing the idea of honest money that they daren’t open up the question. It doesn’t take a Ph.D. from MIT or Princeton, however, to imagine that in an age of fiat money, the top decile would have an easier time making hay than would the denizens of the other nine deciles, who aren’t trained in the art of swaps and derivatives. We don’t belittle the skills of the top decile. We tend to view them the way we view great baseball players or violinists — heroic figures. Neither do we make a totem out of economic equality; in inequality, after all, are found incentives. In terms of public policy, though, we favor honest money. It works out better for more people. And there is a moral dimension to the question of honest money. This was a matter that was understood — and keenly felt — by the Founders of America, who almost to a man (Benjamin Franklin, a printer of paper notes, was a holdout), cringed with humiliation at the thought of fiat paper money. They’d tried it in the revolution, and it had been the one embarrassment of the struggle. They eventually gave us a Constitution that they hoped would bar us from ever making the same mistake. There is an irony here for Monsieur Piketty. It was France who gave us Jacques Rueff, the economist who had the clearest comprehension of the importance of sound money based on gold specie. He was, among other things, an adviser of Charles De Gaulle. It was De Gaulle who in 1965, called a thousand newspapermen together and spoke of the importance of gold as the central element of an international monetary system that would put large and small, rich and poor nations on the same plane. We ran the complete text of Professor Piketty’s book “Capital” through the Sun’s own “Electrically-operated Savvy Sifter” and were unable to find, even once, the name of Rueff. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

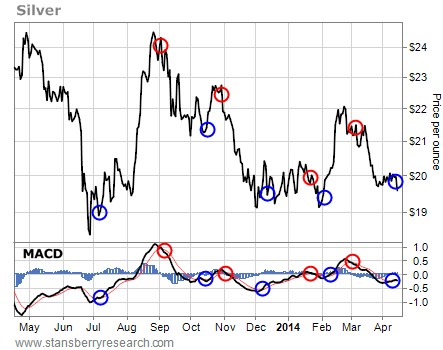

| Silver About To Move Higher and S&P Lower Posted: 22 Apr 2014 02:55 PM PDT Silver has had three bad years while the S&P has had five good years. It is time for both markets to reverse. Examine the following graph of Silver versus the Silver to S&P ratio. It tells me the ratio has returned to levels seen in 2008 and that the ratio follows the price of silver. This is interesting but not that helpful.

Now examine the second graph in which the same ratio is plotted against the 14 month Relative Strength Index of the ratio. The RSI is a timing indicator that ranges between 0 – 100 and indicates buy zones when the indicator is low and sell zones when the RSI is high. Currently the RSI of the index is about 23 – quite low and indicating that the silver to S&P ratio should increase from here. Either the silver price should go up or the S&P should come down, or more likely, both will occur.

Note the RSI of the ratio was about 16 at the end of December 2013 when silver hit its double-bottom lows. That RSI reading was the lowest in 25 years. The December low in silver should have been an important bottom in the silver market and an important bottom in the silver to S&P ratio. So What Does This Prove?In a world of High-Frequency-Trading, managed and manipulated markets, gold leasing, politics, and Quantitative Easing, it might mean very little. In the short term, markets can be moved rather easily by large traders and influential forces such as central banks. But, in a longer perspective, the ratio of silver to the S&P is at a low, the actual S&P 500 Index is near an all-time high, and the RSI timing indicator for the ratio was at a 25 year low in December. The next major move is much more likely to be a rise in silver prices and a fall in the S&P. That major move might be many weeks away, but it seems both inevitable and imminent. Consider this 20 year chart of the S&P. Does the S&P look safe and healthy?

Consider this 20 year chart of silver. Does silver look like it has bounced off an intermediate bottom in a long-term bull market?

Conclusions

An intriguing article from Bill Holter that addresses silver, an interesting interpretation, and a possible answer to questions about silver supply is My Back And Forth Yesterday with John Embry. I encourage you to read it.

GE Christenson | aka Deviant Investor | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| “Axis Of Power” As Countries Move To Link Currencies To Gold Posted: 22 Apr 2014 02:36 PM PDT  On the heels of continued uncertainty around the globe, today an acclaimed money manager spoke with King World News about a new "axis of power," as Russia and China move to link their currencies with gold, and both countries continue to form an alliance with Germany. Below is what Stephen Leeb had to say. On the heels of continued uncertainty around the globe, today an acclaimed money manager spoke with King World News about a new "axis of power," as Russia and China move to link their currencies with gold, and both countries continue to form an alliance with Germany. Below is what Stephen Leeb had to say.This posting includes an audio/video/photo media file: Download Now | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dubai Global Gold Centre On Continuing Bullion Demand Posted: 22 Apr 2014 02:15 PM PDT Even though the price of gold has fallen below the psychological level of $1330 an ounce, and while the mainstream media continues with its consistently negative coverage, demand for physical gold remains extremely robust in certain regions. One of these regions is the Middle East and the one centre that always fascinates me is Dubai. And, I am not surprised that business in Dubai has increased substantially. From what I see and hear, people in this region have no interest in what analysts at the major banks have to say about gold nor do they pay any attention to what Western main stream media has to report on gold. They are also not interested in the fact that Hedge funds in the West have trimmed their net long positions in gold. What is important to them is ownership of physical gold. From my personal observation of the activities in the main gold souks, things are very busy and when it comes to the global gold market, and according to Ahmed bin Sulayem, Executive Chairman of Dubai Multi Commodities Centre (DMCC), Dubai has become a major global gold and precious metal trading hub. “Dubai has quickly emerged as the leading global hub for the precious metals trade. As a result of DMCC’s continuous efforts to realise the vision of His Highness Shaikh Mohammed bin Rashid Al Maktoum, Vice-President and Prime Minister of the UAE and Ruler of Dubai, the emirate has risen as the destination for global precious metals trading,” Sulayem said in his keynote address at the Third Dubai Precious Metals Conference. In 2013, almost 40% of the world’s physical gold trade came through Dubai and the value of total gold traded through Dubai grew to $75 billion, compared to $6 billion in 2003, and $70 billion in 2012. This is truly incredible considering Dubai does not produce the yellow metal. Dubai also saw an annual trade volume increase of 73% accounting for 2,250 tons of gold, Sulayem said. “This market has proven to be resilient under all conditions; even on a year where total global demand fell by 15%. Dubai gained from near-record consumption demand growth. These figures represent a significant shift in the balance of global demand flows with Dubai positioned as one of the global market leaders,” the DMCC chief said at the conference. Meanwhile, the Dubai Gold and Commodities Exchange (DGCX) plans to introduce a spot gold contract this June as part of its growth as a top trading centre for the precious metal, its' chief executive Gary Anderson said. “The DGCX is in the final stages of finalising contract specifications,” a spokesman quoted Anderson at the conference. The contract is expected to be for one kilogramme (32 troy ounces) of 0.995 purity gold, the spokesman added. The DGCX already trades gold futures. The latest trading figures disclosed by the DMCC also highlighted Dubai’s growing reputation as the global bullion centre, ideally located between the producing and consuming nations. In Japan, demand for physical gold soared in recent weeks, as the government pumped up their sales tax. Japanese gold bars and coins investment demand rose sharply by five-fold ahead of nation’s consumption tax hike that went into effect this month. According to Forbes Asia, the China Gold Association showed that China’s gold consumption increased by 41% over 2012 to 1,176 tons in 2013. (China does not publish official numbers so discrepancies range in the hundreds of tons) Adding these imports to China’s domestic production of 428 tons indicates that China accumulated at least 1,604 tons last year. Furthermore, combining China’s aggregate domestic production and apparent imports indicates that China has more than 3,514 tons, making it the world’s second largest national owner after the United States, if one can believe that the US still owns any gold. In a report from Reuters, published on April 21, China has begun allowing gold imports through its capital Beijing. Beijing is 3rd mainland gold import point, after Shenzhen & Shanghai and the opening of a third import point after Shenzhen and Shanghai could threaten Hong Kong’s pole position in China’s gold trade, as the mainland can get more of the metal it wants directly rather than through a route that discloses how much it is buying. The People’s Bank of China (PBOC) is believed to be adding to its gold reserves, according to the World Gold Council (WGC), as it looks to diversify from U.S. Treasuries. The central bank rarely reveals the numbers. Gold has traditionally been imported from Hong Kong into Shenzhen, where nearly 70 percent of the Chinese gold jewellery business is located. Shanghai was opened up as a second port last year. Only banks are allowed to import gold into China. Industrial and Commercial Bank of China Ltd, Agricultural Bank of China Ltd, ANZ and HSBC are among the 12 banks that can import gold. In addition to China and India, Indonesia, Saudi Arabia and Thailand increased their gold holdings in 2013. As gold is a widely recognized representation of wealth, this represents a massive transfer of ‘real’ wealth from West to East. And, while the official figure shows that India’s imports were 978 tons last year, the figure does not take into account the massive quantities that were smuggled into the country. As I have mentioned countless times, one of the reasons for owning gold is to protect your wealth against the depreciating value of fiat currencies. One example is the Ukrainian Hryvnia. It has been in free fall in 2014 and is the world's worst performing currency this year. The Hryvnia was relatively stable until 2014, when the currency collapsed from 0.12 to 0.08 since the start of this year. At the same time, the price of gold in Hryvnia went from 10,000 to 17,444 last week. One could easily observe that this is an example of runaway inflation, even hyperinflation. In such a situation, gold is known to hold its value. It proves that people do not hold gold to have more value in terms of a currency. Rather, one holds gold as monetary insurance to preserve its purchasing power when things turn out bad. Gold chart

The upward momentum in gold prices seen recently has failed to gain any traction and have hit resistance at around $1320/oz. Prices seem to building some support at around $1280/oz. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

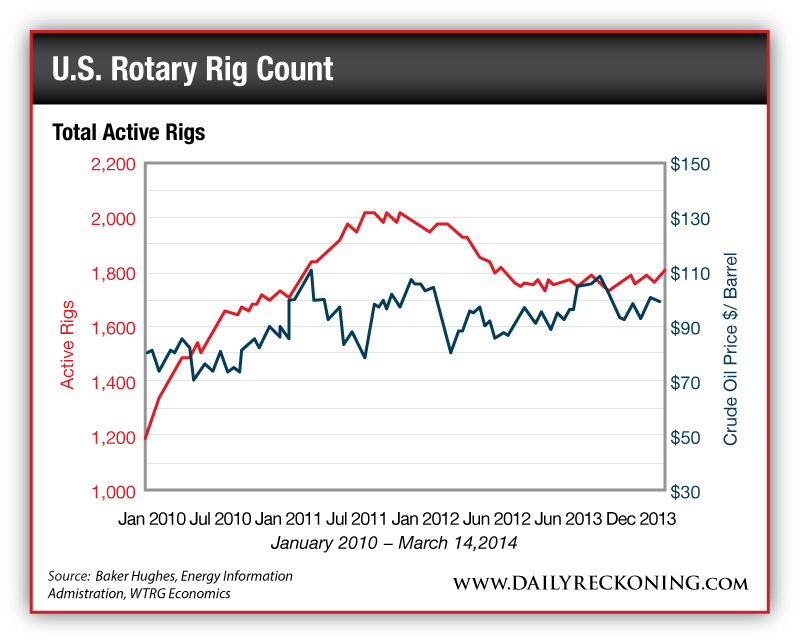

| A Simple Strategy for Investing in the US Energy Boom Posted: 22 Apr 2014 02:10 PM PDT "There are no dry holes," the man said. "Every well produces good oil and pays for itself." That's what I learned during a talk with an oil company executive not long ago. The man's operations are mostly in the Eagle Ford play of south Texas. He told me that just a few years ago, his first well cost nearly $30 million to drill and complete, over almost 60 days. Now, with multiwell drill pads and reusing everything from rig roads to fracking water, his average cost per well is under $6 million; and drilling takes about seven days, with another seven days for completion. Savings go straight to the bottom line and dramatically improve the economics of every well. So how does this affect your investing outlook? Let's dig in. Now, because everything is connected to everything else, developments in one sector affect investments in another. For example, not long ago, a chart graphing out the number of active rotary drilling rigs in the U.S. over the past four years caught my eye. Here we see the number of rigs compared to average oil prices over the same time (the finer line):

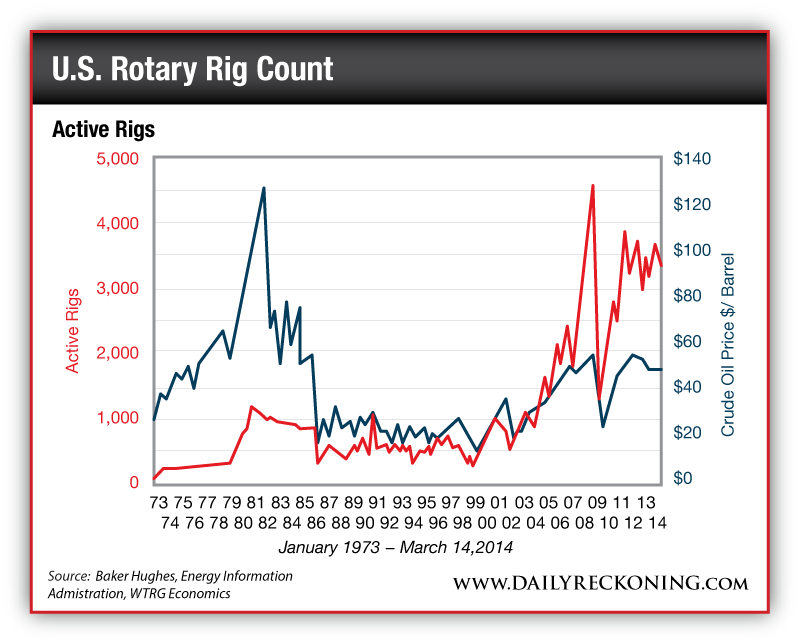

As you can see, the number of active rigs rose fast starting in late 2009, during the post-crash oil patch recovery. Generally, the pace of U.S. drilling increased along with a rise in oil prices, from the $70-80 per barrel range to the current $100 per barrel zone. As the chart shows, in 2012, the number of active rigs peaked and then declined to the current plateau (just under 1,800) over the past year. Within this rig count number, there are more rigs drilling for oil, the price for which has been rising, and fewer rigs drilling for natural gas, the price of which has been relatively low. The rig count decline also reflects increased efficiency of drilling operations, particularly with horizontal and fracking plays. Using current technology and overall knowledge available in the field, a well-run rig can drill significantly more wells with more efficiency than in the past. This is NOT your father's oil patch anymore. Today, things operate under an entirely different development model. Let's look at a similar chart, covering a much longer period of time. It's the rig count going back to 1973, along with a chart of oil prices over the same time frame. Notice how the rig count from the first chart (above) is reflected on the far right side of this next chart:

You can also see within the second chart reflections of other important global issues. First, note the dramatic U.S. rig count spike in the late 1970s in response to a substantial oil price increase at the time. Back then, world oil prices shot upward due to loss of over 3 million barrels per day of global oil supply when Iranian exports broke down after the Iranian Revolution. By 1985, however, the U.S. rig count crashed to below 1,000 as oil prices settled downward and traded in a relatively low range during the remainder of the 1980s and into the early 1990s. Those were also years when large volumes of new oil supply came online from places like Alaska, the North Sea, Angola and other locales. After 2000, oil prices rose along with demand from the fast-growing Chinese economy. In fact, Chinese oil demand exceeded that nation's production by a long shot and triggered a long oil price rise, eventually fueled even more by financial speculation. As the chart shows, oil prices rose over the next eight years and eventually spiked at over $147 per barrel in 2008. This energy-financial distortion had much to do with the ensuing global economic crash — although the U.S. and global housing boom was another key element. On those lines, it's fair to say that rising energy costs pushed many a household over the financial edge. As I noted at the outset, things are connected to each other. It's no coincidence that post crash, the U.S. Federal Reserve flooded the world with liquidity in the form of "quantitative easing" (QE). All that money had to go somewhere, of course, and to be sure, much of it went to bail out banks and prop up the stock market. That was the Fed idea. However, other floods of QE liquidity hit the oil patch and funded a leasing and drilling boom that has delivered significant new amounts of energy to the U.S. economy. In the aftermath of the 2008 crash and during the recovery that followed, the U.S. energy industry began to shift more and more assets and capital to directional drilling and fracking in "tight" rocks, particularly shale formations. In other words, the technological nature of the U.S. onshore drilling industry changed in a big way coming out of the 2008 crash. It's a story that has yet to be fully researched and written, although we can see the broad idea reflected in oil output charts such as this:

As the oil chart (above) makes clear, for many decades, U.S. oil output followed the classic "Hubbert curve" of Peak Oil fame. But by 2008 and afterward, with the tech revolution and "shale gale" in full gear, U.S. output began to move up sharply. New tech — coupled with significant infusions of capital — changed the shape of the Hubbert curve, and now the U.S. produces as much oil as it did back in the late 1980s, with more to come in future years. So what's the takeaway? Well, consider that every barrel of domestic U.S. oil output displaces an imported barrel, so the effect is twofold, if not more. That is, every "new" U.S. barrel is wealth created in country, at about, say, $100 per pop. Plus, each new domestic barrel displaces an imported barrel, which leads to $100 less leaving the U.S. as part of the trade deficit. Consider also that over the past three years or so, more and more barrels per day of "new" U.S. oil go through refineries and then get exported as product. In a very basic sense, U.S. refiners buy a $100 barrel of crude and export $200 of product. Again, it benefits the U.S. domestic economy and the trade economics of the country. In fact, the benefits of increased U.S. oil production have been great enough to partially offset the decline in the dollar caused by the Federal Reserve's QE policies in the first place. Given how much this influx of oil and gas has strengthened the U.S. economy, despite the banking crisis and its fallout, it's no wonder that in recent years the U.S. dollar strengthened — and given the dollar's natural relationship with precious metals, prices for the gold declined. It gets back to the idea that everything is connected to everything else. Oil relates to money and that energy-money dynamic influences the price of gold. What does this mean for you, the resource investor? It means in some respects the two sides of our investing sphere, energy and metals, are counter-balanced. And in this case when one side of the resource sector declines, we can expect the other to rise. Meanwhile you can count on us to keep you one step ahead of the market. Regards, Byron King P.S. There’s another part to the story you’ve probably missed. In today’s email edition of the Daily Reckoning, two of my colleagues, Peter Coyne and Paul Mampilly wrote about the Fed’s easy money… what’s driving the current depression… a yield stock that investors are confusing for a growth stock… and much more. If you haven’t subscribed to get the Daily Reckoning each day by email, you’re cheating yourself out of 50% of our free insights. Click here now to subscribe for FREE. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold Daily and Silver Weekly Charts - Hotel California Posted: 22 Apr 2014 01:56 PM PDT | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold Daily and Silver Weekly Charts - Hotel California Posted: 22 Apr 2014 01:56 PM PDT | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 22 Apr 2014 01:38 PM PDT Graceland Update | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 22 Apr 2014 12:15 PM PDT Copper getting pathological, suffering from SAD... RAYMOND GOLDIE is vice-president of commodity economics and senior mining analyst at Salman Partners in Canada. With extensive experience in the investment business, including more than 20 years as a mining analyst covering non-precious-non-ferrous and precious minerals – including gold and silver – plus a PhD from Queens University, Goldie now says Dr.Copper may be in a supercycle, but there are serious problems with the base metal's near-term outlook. In this interview with The Gold Report, Salman Partners' vice president explains why... The Gold Report: You are giving a presentation at the Society for Mining, Metallurgy & Exploration Current Trends in Mining Finance Conference called Diagnosing the Doctor, which refers to assessing the supply and demand problems for Dr. Copper as a way to understand what is ailing all the mining products today. Are we in a supercycle? What is the meaning of a sustainable supercycle? Raymond Goldie: I suppose it's best to answer your second question first – What is the meaning of a sustainable supercycle? – because a lot of people use the word supercycle to describe the wonderful state that we had beginning in the early part of this century, when metal prices kept going up, commodity prices kept going up, seemingly forever. I'm a little less restrictive on what I define as a supercycle. I think a supercycle is any period in which we have commodity prices higher than their long-term average values. On that basis, even allowing for overall inflation, we've been in a supercycle since 2004. We're still in it, although for a few months regrettably at the end of 2008 we popped out of it. But right now we are in a supercycle. TGR: What are the fundamentals keeping us in your definition of a supercycle? Raymond Goldie: The usual reason is China. It's the biggest consumer of most of the commodities in the world and has the biggest growth in consumption of most of the commodities in the world. But what that analysis tends to overlook is that production of most commodities in China has been increasing at roughly the same rate as consumption in China. So, on balance, China may not be as big a contributor to the supercycle as we've imagined. TGR: Does that mean that the Western world is playing a larger role in supporting the supercycle than we give it credit for? Raymond Goldie: When it comes to assessing supply and demand from Asia, it is important to consider Chinese economic data, which a recent Bloomberg article equates to some of the meat served in low-cost restaurants. We don't know where it comes from and don't really know what it means. It's not easy to put a lot of credence on Chinese economic numbers, so it's hard to tell the extent to which China does affect supply and demand. But one thing that we can count on is the diligence of people who sit at borders with clipboards looking at stuff crossing borders. They are paid to make sure that the right duties get paid and the ships are carrying what they're supposed to be carrying. If we look at China's trade with the rest of the world, those numbers are fairly reliable, even if the numbers for what's going on inside China are not reliable. Since 2008, the dark days when the world seemed to have ended, China's imports of copper from the rest of the world have grown 41% per annum. TGR: And what about the supply side? Raymond Goldie: I think the single most important reason that we're in a sustainable supercycle is that we haven't invested enough in finding more resources. The supply-side constraints are probably why prices are higher than the long-term trend in prices. TGR: Why has it been so difficult to predict how much copper will be produced in a given year if it takes so long to bring a mine to production? Raymond Goldie: Since about 2003 analysts have consistently overestimated the production of copper. My theory for the consistent shortfall is that before 2003, when strikes, landslides, earthquakes, storms, civil unrest, late trains and the like slowed down production, someone in the head office would send a cable calling for the mining of high-grade ore to make up the difference. But since 2003, there hasn't been any high-grade ore to mine because of a lack of investment in new resources. And this happens year after year. About 7% less copper is produced each year than the mines predicted at the start of the year. TGR: So why isn't that inconsistency causing the price to go up? Raymond Goldie: Maybe it is. There has certainly been what I've called a pathological situation in the copper markets because typically the relationship between copper inventories – the stuff that's sitting around in warehouses – and prices is that the lower the inventories, the higher the price. But since 2005, in the Western world – we don't know what's going on in China – inventories have gone up 185%. Typically, that would mean prices go down, right? But, no, prices have gone up 95%. That may be one of the reasons that we're consistently producing less of the stuff than we thought we could. TGR: Is that because of the role of recycling in meeting some of the demand? Raymond Goldie: I think it could be because it used to be that every pound that was in inventory was backed by all the copper that the mines would produce and all the copper that scrap yards would produce. The amount that the scrap yards produce has been declining, in large part because Asians have been very diligent about taking scrap from North America and refining it into good usable copper again. But, again, it's hard to get good figures for how much copper there is in scrap yards so that answer is probably yes, the declining use of copper in recycling is probably one of the reasons why we've seen prices go up even though inventories have also gone up. But it's hard to be more precise than that. TGR: You have also said that copper has seasonal affective disorder (SAD). What causes that? Raymond Goldie: That's right, it does. I can tell you what SAD is, but I can't tell you exactly what causes it. In the good old days of the London Metal Exchange (LME), the saying was "sell in May and go away." And that was always a wonderful excuse to take an English summer holiday and not bother coming back to trade copper until September or October. Now the peak seems to be around the end of February and the end of June tends to be the bottom in copper prices. It's pretty consistent. Year after year we see that effect, but what causes it, I don't know. TGR: Because copper is so important for growth, is it feasible that it could be used as the world reserve currency instead of gold or the Dollar? What would that look like? Raymond Goldie: Copper is being used as a reserve currency in China right now. Some of the importers will use the copper that they hold as collateral for loans that they make from various banks in China. One of the advantages of copper as collateral is that unlike wheat, silver or potash, you can store it outside. Even in the rain, copper will keep its value, and there's always a use for the stuff. But to talk about copper as a reserve currency for the whole world is not practical. If a country is holding reserves of $1 trillion, it would have to have 150 million tons on reserve. That is about eight and a half years of copper consumption just sitting there. But certainly copper is being used as a currency on a small scale, as it's being used now in China. TGR: What prices are you using for copper going forward in the rest of 2014? Raymond Goldie: Since 2003 when the fundamentals of the copper business changed so significantly, the forward prices on the LME have been a much better forecaster of copper prices than we analysts. This afternoon, the LME is telling me that if I buy copper now for delivery in 10 years, I would have to pay $3.02 per pound. That's as good as any forecast I have for the long-term price of copper. If you were to buy a pound of copper for delivery tomorrow, it's pretty much the same as where the price of copper is today. TGR: If copper prices look to be fairly flat going forward, why do copper equities tend to outperform the metal? Raymond Goldie: This gets back to the unwieldy nature of copper as a store of value. Let's say you were thinking of retiring and decided to make off with all of your fortune, say $3 million, and drive away into the sunset. Now, if you put that in the form of gold, $3m would weigh less than 200 lb; it would fit in the trunk of your car. But $3m worth of copper would weigh 450 tons. That is why when people get enthusiastic about buying gold, they often buy gold bullion. But when they're thinking of buying copper, the unwieldy nature of buying copper metal means they are better off with the equities. That's why the equities have done about the same or even a little better than the price of copper itself. That certainly has not been the case with gold. TGR: Are the copper companies less risky than some of the gold companies? Raymond Goldie: Riskiness is a feature of the things that Mother Nature can fling at us or the surprises that come with the election of a government that no one expected and that government nationalizes some of its assets. Most of the companies that I follow are managed by a lot of gray hairs; they've seen all the unpleasant things that can happen. Most of the ones that I tend to look at are well managed, and they include the big producers TGR: Do you evaluate a company in the tailing business very differently than a company with a different business strategy? Raymond Goldie: I don't actually. I generally use the standard textbook discounted cash flow valuation method. For a mine in production, I use a low discount rate. For potential expansion, I use a higher discount rate because this is an unproven technology there. I use an even higher discount rate on something that isn't in production yet, simply because of the technological, political and community risks associated with that prospect. TGR: With all of these great ideas, what advice do you have for resource investors who are looking to keep their portfolios healthy during the next two or three years while they wait for some of these things to happen? Raymond Goldie: There are two questions that investors should ask about any investment they make: Is the value there? When should I seize on that value? Most copper mining stocks are trading as if the price of copper were $2 per pound and is going to be about $2 per pound forever. But copper on the LME 10 years out is actually $3 per pound. That means the equities are definitely a value story. As to when to buy it, given the SAD cycle we mentioned earlier, investors might want to wait until the end of June. TGR: Thank you for your advice. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 22 Apr 2014 12:15 PM PDT Copper getting pathological, suffering from SAD... RAYMOND GOLDIE is vice-president of commodity economics and senior mining analyst at Salman Partners in Canada. With extensive experience in the investment business, including more than 20 years as a mining analyst covering non-precious-non-ferrous and precious minerals – including gold and silver – plus a PhD from Queens University, Goldie now says Dr.Copper may be in a supercycle, but there are serious problems with the base metal's near-term outlook. In this interview with The Gold Report, Salman Partners' vice president explains why... The Gold Report: You are giving a presentation at the Society for Mining, Metallurgy & Exploration Current Trends in Mining Finance Conference called Diagnosing the Doctor, which refers to assessing the supply and demand problems for Dr. Copper as a way to understand what is ailing all the mining products today. Are we in a supercycle? What is the meaning of a sustainable supercycle? Raymond Goldie: I suppose it's best to answer your second question first – What is the meaning of a sustainable supercycle? – because a lot of people use the word supercycle to describe the wonderful state that we had beginning in the early part of this century, when metal prices kept going up, commodity prices kept going up, seemingly forever. I'm a little less restrictive on what I define as a supercycle. I think a supercycle is any period in which we have commodity prices higher than their long-term average values. On that basis, even allowing for overall inflation, we've been in a supercycle since 2004. We're still in it, although for a few months regrettably at the end of 2008 we popped out of it. But right now we are in a supercycle. TGR: What are the fundamentals keeping us in your definition of a supercycle? Raymond Goldie: The usual reason is China. It's the biggest consumer of most of the commodities in the world and has the biggest growth in consumption of most of the commodities in the world. But what that analysis tends to overlook is that production of most commodities in China has been increasing at roughly the same rate as consumption in China. So, on balance, China may not be as big a contributor to the supercycle as we've imagined. TGR: Does that mean that the Western world is playing a larger role in supporting the supercycle than we give it credit for? Raymond Goldie: When it comes to assessing supply and demand from Asia, it is important to consider Chinese economic data, which a recent Bloomberg article equates to some of the meat served in low-cost restaurants. We don't know where it comes from and don't really know what it means. It's not easy to put a lot of credence on Chinese economic numbers, so it's hard to tell the extent to which China does affect supply and demand. But one thing that we can count on is the diligence of people who sit at borders with clipboards looking at stuff crossing borders. They are paid to make sure that the right duties get paid and the ships are carrying what they're supposed to be carrying. If we look at China's trade with the rest of the world, those numbers are fairly reliable, even if the numbers for what's going on inside China are not reliable. Since 2008, the dark days when the world seemed to have ended, China's imports of copper from the rest of the world have grown 41% per annum. TGR: And what about the supply side? Raymond Goldie: I think the single most important reason that we're in a sustainable supercycle is that we haven't invested enough in finding more resources. The supply-side constraints are probably why prices are higher than the long-term trend in prices. TGR: Why has it been so difficult to predict how much copper will be produced in a given year if it takes so long to bring a mine to production? Raymond Goldie: Since about 2003 analysts have consistently overestimated the production of copper. My theory for the consistent shortfall is that before 2003, when strikes, landslides, earthquakes, storms, civil unrest, late trains and the like slowed down production, someone in the head office would send a cable calling for the mining of high-grade ore to make up the difference. But since 2003, there hasn't been any high-grade ore to mine because of a lack of investment in new resources. And this happens year after year. About 7% less copper is produced each year than the mines predicted at the start of the year. TGR: So why isn't that inconsistency causing the price to go up? Raymond Goldie: Maybe it is. There has certainly been what I've called a pathological situation in the copper markets because typically the relationship between copper inventories – the stuff that's sitting around in warehouses – and prices is that the lower the inventories, the higher the price. But since 2005, in the Western world – we don't know what's going on in China – inventories have gone up 185%. Typically, that would mean prices go down, right? But, no, prices have gone up 95%. That may be one of the reasons that we're consistently producing less of the stuff than we thought we could. TGR: Is that because of the role of recycling in meeting some of the demand? Raymond Goldie: I think it could be because it used to be that every pound that was in inventory was backed by all the copper that the mines would produce and all the copper that scrap yards would produce. The amount that the scrap yards produce has been declining, in large part because Asians have been very diligent about taking scrap from North America and refining it into good usable copper again. But, again, it's hard to get good figures for how much copper there is in scrap yards so that answer is probably yes, the declining use of copper in recycling is probably one of the reasons why we've seen prices go up even though inventories have also gone up. But it's hard to be more precise than that. TGR: You have also said that copper has seasonal affective disorder (SAD). What causes that? Raymond Goldie: That's right, it does. I can tell you what SAD is, but I can't tell you exactly what causes it. In the good old days of the London Metal Exchange (LME), the saying was "sell in May and go away." And that was always a wonderful excuse to take an English summer holiday and not bother coming back to trade copper until September or October. Now the peak seems to be around the end of February and the end of June tends to be the bottom in copper prices. It's pretty consistent. Year after year we see that effect, but what causes it, I don't know. TGR: Because copper is so important for growth, is it feasible that it could be used as the world reserve currency instead of gold or the Dollar? What would that look like? Raymond Goldie: Copper is being used as a reserve currency in China right now. Some of the importers will use the copper that they hold as collateral for loans that they make from various banks in China. One of the advantages of copper as collateral is that unlike wheat, silver or potash, you can store it outside. Even in the rain, copper will keep its value, and there's always a use for the stuff. But to talk about copper as a reserve currency for the whole world is not practical. If a country is holding reserves of $1 trillion, it would have to have 150 million tons on reserve. That is about eight and a half years of copper consumption just sitting there. But certainly copper is being used as a currency on a small scale, as it's being used now in China. TGR: What prices are you using for copper going forward in the rest of 2014? Raymond Goldie: Since 2003 when the fundamentals of the copper business changed so significantly, the forward prices on the LME have been a much better forecaster of copper prices than we analysts. This afternoon, the LME is telling me that if I buy copper now for delivery in 10 years, I would have to pay $3.02 per pound. That's as good as any forecast I have for the long-term price of copper. If you were to buy a pound of copper for delivery tomorrow, it's pretty much the same as where the price of copper is today. TGR: If copper prices look to be fairly flat going forward, why do copper equities tend to outperform the metal? Raymond Goldie: This gets back to the unwieldy nature of copper as a store of value. Let's say you were thinking of retiring and decided to make off with all of your fortune, say $3 million, and drive away into the sunset. Now, if you put that in the form of gold, $3m would weigh less than 200 lb; it would fit in the trunk of your car. But $3m worth of copper would weigh 450 tons. That is why when people get enthusiastic about buying gold, they often buy gold bullion. But when they're thinking of buying copper, the unwieldy nature of buying copper metal means they are better off with the equities. That's why the equities have done about the same or even a little better than the price of copper itself. That certainly has not been the case with gold. TGR: Are the copper companies less risky than some of the gold companies? Raymond Goldie: Riskiness is a feature of the things that Mother Nature can fling at us or the surprises that come with the election of a government that no one expected and that government nationalizes some of its assets. Most of the companies that I follow are managed by a lot of gray hairs; they've seen all the unpleasant things that can happen. Most of the ones that I tend to look at are well managed, and they include the big producers TGR: Do you evaluate a company in the tailing business very differently than a company with a different business strategy? Raymond Goldie: I don't actually. I generally use the standard textbook discounted cash flow valuation method. For a mine in production, I use a low discount rate. For potential expansion, I use a higher discount rate because this is an unproven technology there. I use an even higher discount rate on something that isn't in production yet, simply because of the technological, political and community risks associated with that prospect. TGR: With all of these great ideas, what advice do you have for resource investors who are looking to keep their portfolios healthy during the next two or three years while they wait for some of these things to happen? Raymond Goldie: There are two questions that investors should ask about any investment they make: Is the value there? When should I seize on that value? Most copper mining stocks are trading as if the price of copper were $2 per pound and is going to be about $2 per pound forever. But copper on the LME 10 years out is actually $3 per pound. That means the equities are definitely a value story. As to when to buy it, given the SAD cycle we mentioned earlier, investors might want to wait until the end of June. TGR: Thank you for your advice. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Dollar Crash In a Matter of Months? Posted: 22 Apr 2014 10:24 AM PDT In case you were wondering there is a Comex precious metal options expiration on Thursday the 24th. Since the expiration is for the inactive month of May, I am wondering if they are not going to do an early hit with a head fake on this one as the day comes. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 22 Apr 2014 10:13 AM PDT Silver has had three bad years while the S&P has had five good years. It is time for both markets to reverse. Examine the following graph of Silver versus the Silver to S&P ratio. It tells me the ratio has returned to levels seen in 2008 and that the ratio follows the price of silver. This is interesting but not that helpful. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||