Gold World News Flash |

- Richard Russell - Crime, Chaos, Collapse & Skyrocketing Gold

- Next Great Depression? MIT study predicting ‘global economic collapse’ by 2030 still on track

- Oil and Natural Gas Ratio Explodes to 52:1

- Silver Update 4/11/12 Wallstreet Looters

- Gold Seeker Closing Report: Gold and Silver End Slightly Lower

- Risk off? Having sold most of its own, IMF now lauds gold as 'safe asset'

- Europe's banks beached as ECB stimulus runs dry

- Gold Rules in Vietnam – They Will Actually PAY YOU To Store Your Gold

- Batero Gold’s first resource shows heap leach-ability and 5 - 10 million ounce potential for a porphyry cluster in Colombia’s emerging Mid-Cauca Trend

- Silver Bullion: The Most Affordable Way to Protect Your Wealth

- Graham Summers: Collapse of Europe is Guaranteed! Here?s Why

- Campbell?s Challenge: ?Think for Yourself? When Reading This Article on Gold!

- Shilling Shuns Stocks, Sees S&P At 800

- Bernanke's Right Hand Dove, Janet Yellen, Hints At ZIRP Through Late 2015

- The Silicon Valley Top

- Goldman Previews Q2: Sees 150K Jobs Per Month Created, And A Slowing Of The Economy

- Boone Pickens – Natural Gas ‘Has to be Near Bottom’

- Massive Volatility Continues in COMEX Silver Warehouses

- Europe Will Collapse in May-June

- The Gold Price Must Pierce Resistance at $1,662 or Fall Back

- Doug Casey on Tax Day

- U.S. Money Funds Threaten Financial Stability

- Opportunity Slipping Away

- Gold Equities Gaining Credibility

- Gold Daily and Silver Weekly Charts

- Gold Price vs. Platinum

- Gold Equities Gaining Credibility: Doug Groh

- Sprott On Silver From Conference Last Week

- Eurodollar Update - Hunting The Black Swan - Gold and the Eurodollar

| Richard Russell - Crime, Chaos, Collapse & Skyrocketing Gold Posted: 12 Apr 2012 04:07 AM PDT  With continued turmoil in global markets, the Godfather of newsletter writers, Richard Russell, issued some ominous warnings and gave some strong advice to investors in his latest commentary: "Save some cash, load up with gold and silver, and be patient. Get ready for a crime wave -- a large segment of the population will do 'whatever it has to' in order to obtain food. Hungry men and women can be desperate and lawless." With continued turmoil in global markets, the Godfather of newsletter writers, Richard Russell, issued some ominous warnings and gave some strong advice to investors in his latest commentary: "Save some cash, load up with gold and silver, and be patient. Get ready for a crime wave -- a large segment of the population will do 'whatever it has to' in order to obtain food. Hungry men and women can be desperate and lawless."

This posting includes an audio/video/photo media file: Download Now | ||||||||||||

| Next Great Depression? MIT study predicting ‘global economic collapse’ by 2030 still on track Posted: 11 Apr 2012 05:32 PM PDT  A renowned Australian research scientist says a study from researchers at MIT claiming the world could suffer from a "global economic collapse" and "precipitous population decline" if people continue to consume the world's resources at the current pace is still on track, nearly 40 years after it was first produced. A renowned Australian research scientist says a study from researchers at MIT claiming the world could suffer from a "global economic collapse" and "precipitous population decline" if people continue to consume the world's resources at the current pace is still on track, nearly 40 years after it was first produced.The Smithsonian Magazine writes that Australian physicist Graham Turner says "the world is on track for disaster" and that current research from Turner coincides with a famous, and in some quarters, infamous, academic report from 1972 entitled, "The Limits to Growth." Turner's research is not affiliated with MIT or The Club for Rome. Produced for a group called The Club of Rome, the study's researchers created a computing model to forecast different scenarios based on the current models of population growth and global resource consumption. The study also took into account different levels of agricultural productivity, birth control and environmental protection efforts. Twelve million copies of the report were produced and distributed in 37 different languages. Read more........

This posting includes an audio/video/photo media file: Download Now | ||||||||||||

| Oil and Natural Gas Ratio Explodes to 52:1 Posted: 11 Apr 2012 05:12 PM PDT By EconMatters

The ink on our last article is barely dry when its dire prediction actually came true 48 hours later--natural gas price dropping below $2, a level not seen in over a decade. Henry Hub natural gas front month futures declined to $1.982 per 1,000 cubic feet (mcf) on Wed. April 11, its lowest level since January 28, 2002, when the price hit $1.91. Meanwhile, WTI crude oil rose by $1.68 to finish at $102.70 per barrel; Brent rude increased by 30 cents to finish at $120.18.

The confluence of these price movements also brought the ratio between WTI and Henry Hub to a historical record high of 52:1 (see chart below) while the ratio of Brent to Henry Hub is a jaw-dropping 60:1 ! (And we thought the 25:1 ratio reached back in August 2009, also a historical high at the time, was parabolic.)

Crude oil and natural gas are both energy commodities and should logically have a high degree of correlation. Theoretically, based on an energy equivalent basis, crude oil and natural gas prices should have a 6 to 1 ratio. However, due to various market characteristics, the price of oil typically had traded 8-12x that of natural gas in the past 25 years or so (see chart above). That historical pattern has started to deteriorate since 2009 primarily due to the combination of rising domestic production from unconventional shale gas depressing price levels, while geopolitical events in the MENA region (Middle East & North Africa) adding fear premium to the global crude oil prices.

Natural gas lacks the global market structure like crude oil, and tends to be regionally based thus less impacted by external sources. Oil, on the other hand, is a commodity with global demand drivers; and along with gold, trades as an inflation hedge against a weakening US Dollar.

In most of Europe and Asia, the price of natural gas/LNG is typically linked to crude oil under multiyear contracts. So while the spike in Brent helped to boost natural gas markers elsewhere, with practically zero LNG export capacity in the U.S., not even Fed's two rounds of quantitative easing could lift the languishing Henry Hub.

The chart below illustrates just how disconnected U.S. natural gas price is vs. price levels in Asia, Europe and Brent crude oil.

LNG (liquefied natural gas) is a relatively new technology that some believe has the potential to transform natural gas into a true global commodity. Unfortunately, as discussed before:

While low prices are killing some of the natural gas producers, consumers will get a break via lower electricity costs. Meanwhile, U.S. natural gas trading at an 87% discount to Brent crude oil price is something even the oil industry appreciates. Valero (VLO), the world's largest independent refiner, said in a presentation this January that its refinery operations use up to 600,000 mmBtus/day of natural gas at full utilization. Betting on "low U.S. natural Gas prices for many years to come", Valero has several hydrogen and hydrocraker projects scheduled to complete by the end of 2012 to take full advantage of the low natural gas prices.

With the prospect of domestic natural gas prices remaining low and disconnected from global oil and gas prices for foreseeable future, U.S-based manufacturers of plastics, fertilizers and other products that use natural gas as a feedstock such as Dow Chemicals (DOW), Westlake Chemical Corp. (WLK), Potash (POT) and CF Industries (CF) are set to benefit from cheap U.S. natural gas as opposed to European and Asian competitors who do not.

©EconMattersAll Rights Reserved | Facebook| Twitter| Post Alert| Kindle

| ||||||||||||

| Silver Update 4/11/12 Wallstreet Looters Posted: 11 Apr 2012 05:11 PM PDT | ||||||||||||

| Gold Seeker Closing Report: Gold and Silver End Slightly Lower Posted: 11 Apr 2012 04:00 PM PDT Gold fell to $1652.94 in London before it edged up to $1662.42 in midmorning New York trade, but it then chopped back lower into the close and ended with a loss of 0.05%. Silver slipped to as low as $31.343 in the last hour of trade and ended with a loss of 0.5%.

| ||||||||||||

| Risk off? Having sold most of its own, IMF now lauds gold as 'safe asset' Posted: 11 Apr 2012 03:55 PM PDT IMF Warns of Fresh Global Threat By Robin Harding http://www.ft.com/intl/cms/s/0/b597638c-83e8-11e1-9d54-00144feab49a.html WASHINGTON -- A growing shortage of safe assets poses a new threat to global financial stability, the International Monetary Fund warned on Wednesday. Sovereign debt crises are reducing the number of governments that investors trust to issue "risk-free" bonds just as new financial regulations are increasing demand for safe securities from banks. The report shows how reforms in the wake of the 2007-09 crisis may create new pinch points in the global financial system that could cause trouble in the future. "Safe-asset scarcity could lead to more short-term volatility jumps, herding behaviour, and runs on sovereign debt," said the IMF in a chapter of its new Global Financial Stability Report. "In the future, there will be rising demand for safe assets, but fewer of them will be available, increasing the price for safety in global markets." ... Dispatch continues below ... ADVERTISEMENT Sona Discovers Potential High-Grade Gold Mineralization From a Company Press Release VANCOUVER, British Columbia -- With its latest surface diamond drilling program at its 100-percent-owned, formerly producing Blackdome gold mine in southern British Columbia, Sona Resources Corp. has discovered a potentially high-grade gold-mineralized area, with one hole intersecting 13.6 grams of gold in 1.5 meters of core drilling. "We intersected a promising new mineralized zone, and we feel optimistic about the assay results," says Sona's president and CEO, John P. Thompson. "We have undertaken an aggressive exploration program that has tested a number of target zones. Our discovery of this new gold-bearing structure is significant, and it represents a positive development for the company." Sona aims to bring its permitted Blackdome mill back into production over the next year and a half, at a rate of 200 tonnes per day, with feed from the formerly producing Blackdome mine and the nearby Elizabeth gold deposit property. A positive preliminary economic assessment by Micon International Ltd., based on a gold price of $950 per ounce over eight years, has estimated a cash cost of $208 per tonne milled, or $686 per gold ounce recovered. For the company's complete press release, please visit: http://www.sonaresources.com/_resources/news/SONA_NR18_2011-opt.pdf Safe assets play a range of roles in financial markets. Government bond yields are used to price other assets, banks and insurers hold highly-rated bonds as buffers of capital and liquidity against times of crisis, and they are used as collateral against derivatives and short-term loans. If there were a shortage of safe assets, it could exacerbate a future financial crisis as investors scrambled for the limited supply available, pushing their prices ever higher. The IMF said that the role of central banks in providing large amounts of short-term, safe, liquid assets may be hiding the problem in the short term. For example, the European Central Bank has supplied large amounts of short-term liquidity to its banks. The Fund identified $74.4 trillion of potentially safe assets today, including gold, investment-grade government and corporate debt, and covered bonds. But it warned that 16 per cent of the potential safe government debt supply to 2016 could disappear if governments continued to borrow at current rates and hence made their debt more risky. To address the issue the fund called on policy makers to manage the demand for safe assets and to try to increase the supply. To manage demand, it advised that banks be required to set aside some capital against sovereign debt, to avoid creating an artificial appetite for government bonds; it called for careful implementation of new liquidity rules that could increase bank demand for safe assets by $2 trillion to $4 trillion; and it said that central clearing houses should adopt flexible collateral rules so as not to tie up too many safe assets. On the supply side, it said that safe assets were another reason for countries to tackle their fiscal problems, so their debt would still be seen as safe. It also suggested reforms -- such as rules to make sure issuers share in losses or wider use of covered bonds -- so that private securitisation could become a source of safe assets again. Covered bonds have security against a portfolio of mortgages and a claim on the underlying bank, so they are seen as particularly safe. Support GATA by purchasing DVDs of our London conference in August 2011 or our Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: ADVERTISEMENT Prophecy Platinum (TSXV: NKL) and Ursa Major Minerals Company Press Release VANCOUVER, British Columbia, Canada -- Prophecy Platinum Corp. (TSX-V: NKL, OTC-QX: PNIKF, Frankfurt: P94P) and Ursa Major Minerals Inc. have signed a binding letter of agreement for a business combination through a proposed all-share transaction. In doing so Prophecy and Ursa have acted at arm's length and the transaction has been negotiated at arm's length. Prophecy will issue one common share in exchange for every 25 outstanding common shares of Ursa. Ursa options and warrants will be exchanged for options and warrants of Prophecy on an agreed schedule. Prophecy's offer represents a value of about $0.15 per each common share of Ursa based on Prophecy's share price of $3.70 as at March 1, representing a premium of 130 percent to Ursa's March 1 closing price of $0.065. Prophecy is to subscribe for $1 million common shares of Ursa by way of private placement financing at $0.06 per share, subject to regulatory approval. Upon placement completion, John Lee and Greg Hall, current Prophecy directors, will be appointed to Ursa's board. Prophecy thus will become a mid-tier resource company with a robust and -- The fully permitted open-pit Shakespeare PGM-Ni-Cu mine close to Sudbury, Ontario, infrastructure with near-term production capabilities. -- The flagship Wellgreen (Yukon) PGM-Ni-Cu project with more than 10 million ounces of Pt-Pd-Au inferred resource. Drilling is under way and a preliminary economic assessment study is pending. -- Manitoba's Lynn Lake Ni-Cu project with more than 262 million pounds Ni and 138 million pounds Cu measured and indicated. For the complete announcement, please visit Prophecy Platinum's Internet site here: http://www.prophecyplat.com/news_2012_mar02_prophecy_platinum_ursa_major...

| ||||||||||||

| Europe's banks beached as ECB stimulus runs dry Posted: 11 Apr 2012 03:39 PM PDT By Ambrose Evans-Pritchard http://www.telegraph.co.uk/finance/comment/ambroseevans_pritchard/919851... The European Central Bank's E1 trillion (L824 billion) lending spree over the winter has stored up a host of fresh problems, leaving parts of the banking system more vulnerable than before as the short-term "sugar rush" nears exhaustion. Credit experts say the Spanish and Italian banks are trapped with large losses on sovereign bonds bought with ECB funds under the three-year lending programme, or Long-Term Refinancing Operation (LTRO). Andrew Roberts, credit chief at RBS, said Spanish banks used ECB funds to purchase five-year Spanish bonds at yields near 3.5 percent in February and 4.5 percent in December. The same bonds were trading at 4.77 percent on Wednesday, implying a large loss on the capital value of the bonds. ... Dispatch continues below ... ADVERTISEMENT Prophecy Platinum (TSXV: NKL) and Ursa Major Minerals Company Press Release VANCOUVER, British Columbia, Canada -- Prophecy Platinum Corp. (TSX-V: NKL, OTC-QX: PNIKF, Frankfurt: P94P) and Ursa Major Minerals Inc. have signed a binding letter of agreement for a business combination through a proposed all-share transaction. In doing so Prophecy and Ursa have acted at arm's length and the transaction has been negotiated at arm's length. Prophecy will issue one common share in exchange for every 25 outstanding common shares of Ursa. Ursa options and warrants will be exchanged for options and warrants of Prophecy on an agreed schedule. Prophecy's offer represents a value of about $0.15 per each common share of Ursa based on Prophecy's share price of $3.70 as at March 1, representing a premium of 130 percent to Ursa's March 1 closing price of $0.065. Prophecy is to subscribe for $1 million common shares of Ursa by way of private placement financing at $0.06 per share, subject to regulatory approval. Upon placement completion, John Lee and Greg Hall, current Prophecy directors, will be appointed to Ursa's board. Prophecy thus will become a mid-tier resource company with a robust and diversified pipeline of platinum nickel projects, including: -- The fully permitted open-pit Shakespeare PGM-Ni-Cu mine close to Sudbury, Ontario, infrastructure with near-term production capabilities. -- The flagship Wellgreen (Yukon) PGM-Ni-Cu project with more than 10 million ounces of Pt-Pd-Au inferred resource. Drilling is under way and a preliminary economic assessment study is pending. -- Manitoba's Lynn Lake Ni-Cu project with more than 262 million pounds Ni and 138 million pounds Cu measured and indicated. For the complete announcement, please visit Prophecy Platinum's Internet site here: http://www.prophecyplat.com/news_2012_mar02_prophecy_platinum_ursa_major... It is much the same story for Italian banks pressured into buying Italian debt by their own government. Any further dent to confidence in Italy and Spain over coming weeks -- either over fiscal slippage or the depth of economic contraction -- could push losses to levels that trigger margin calls on collateral. "The banks are deeply under water. This is turning into a disaster for the eurozone periphery now that the liquidity tap has been turned off," said Mr Roberts. "But given the opposition in Germany, the ECB can't easily do another LTRO until there is a major crisis." Spanish banks bought E67 billion of sovereign debt between December and February, while Italian banks bought E54 billion. The purchases almost certainly continued in March. These lenders have soaked up most of debt issues in their countries over the past three months, picking up at a juicy return under the "carry trade" while at the same acting as a conduit for the ECB to shore up crippled countries by the back door. The snag is becoming evident. Weaker lenders are merely parking the ECB's ultra-cheap funds in these bonds until they need the money to roll over their own debts. That is coming due since European banks have E600 billion in redemptions over the rest of the year. Many are now stuck with losses that they cannot afford to crystalise. "It is going to be a problem if the funding market does not open soon and they have to liquidate their holdings," said Guy Mandy from Nomura. "What the LTRO has done is concentrate systemic risk even further. If everything now goes wrong, it could go wrong in a hurry." Mr Mandy said the EU's fiscal austerity is itself "self-defeating," asphyxiating growth and further entwining the perilous nexus of fragile banking systems and indebted states. "Europe still lacks a commensurate policy response. The dogged pursuit of pro-cyclical fiscal austerity could force countries into a downward spiral. To minimise risk, monetary policy needs to be exceptionally loose," he said, calling for a blitz of quantitative easing (QE) to remove assets from bank balance sheets. Mr Mandy said the LTRO is entirely different from the stimulus of the Anglo-Saxon central banks. "There has been no transfer of risk to the ECB's own balance sheet, which is what we think is needed to take away the tail risk of another EMU blowup." Benoit Coeure, France's board member at the ECB, on Wednesday hinted that Frankfurt may be willing to restart direct purchases of Spanish bonds to cap rising yields, saying the debt rout over recent weeks is unjustified. The comments triggered a recovery of Club Med debt but such action is fraught with its own risks even if the German Bundesbank is willing to help a country that is seen -- in German eyes at least -- to be dragging its feet on fiscal austerity. David Owen from Jefferies Fixed Income said that the ECB pushes other investors "down the food chain" instantly when it buys Spanish and Italian debt, raising the loss ratio if either country slides into a Greek-style restructuring. This has become a sore subject for investors following the Greek debacle where all EU bodies -- including the European Investment Bank, which is not a lender of last resort -- were exempted from having to take haircuts. Others such as the Norwegian state pension fund suffered 75 percent losses. Japanese investors have sold E48 billion of eurozone debt over the past year, according to Bloomberg, and are steering clear of any EMU states that could be given the Greek treatment. "I'm not planning to add Spanish or Italian bonds any time soon," said Masataka Horii from Kokusai Global Sovereign Open Fund. Mr Owen said the eurozone's slide into recession will intensify debt jitters and force the ECB to respond. "It will have to cut rates to near zero, and ultimately launch full-scale QE, perhaps as soon as the third quarter." Mr Owen said contortions caused by ECB intervention would not be an issue if the bank acted with force majeure and conviction, as the central banks of the US, UK, and Switzerland have. "The ECB says its action is 'temporary and limited,' and that is precisely the problem," he said. "They are making things worse with piecemeal measures. Economic historians are going to be very damning of the policy mistakes made during this whole episode." Support GATA by purchasing DVDs of our London conference in August 2011 or our Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: ADVERTISEMENT Sona Discovers Potential High-Grade Gold Mineralization From a Company Press Release VANCOUVER, British Columbia -- With its latest surface diamond drilling program at its 100-percent-owned, formerly producing Blackdome gold mine in southern British Columbia, Sona Resources Corp. has discovered a potentially high-grade gold-mineralized area, with one hole intersecting 13.6 grams of gold in 1.5 meters of core drilling. "We intersected a promising new mineralized zone, and we feel optimistic about the assay results," says Sona's president and CEO, John P. Thompson. "We have undertaken an aggressive exploration program that has tested a number of target zones. Our discovery of this new gold-bearing structure is significant, and it represents a positive development for the company." Sona aims to bring its permitted Blackdome mill back into production over the next year and a half, at a rate of 200 tonnes per day, with feed from the formerly producing Blackdome mine and the nearby Elizabeth gold deposit property. A positive preliminary economic assessment by Micon International Ltd., based on a gold price of $950 per ounce over eight years, has estimated a cash cost of $208 per tonne milled, or $686 per gold ounce recovered. For the company's complete press release, please visit: http://www.sonaresources.com/_resources/news/SONA_NR18_2011-opt.pdf

| ||||||||||||

| Gold Rules in Vietnam – They Will Actually PAY YOU To Store Your Gold Posted: 11 Apr 2012 01:22 PM PDT from Sovereign Man :

This is actually how banking used to be. The original bankers were goldsmiths– big burly guys who worked with gold on a daily basis. They had the security systems already established, and, for a fee, they were willing to let you park your gold in their safes. Eventually, goldsmiths got into the moneylending business; instead of charging a security fee, they would pay depositors a rate of interest for the right to loan out the gold at a higher rate of interest. Goldsmiths' reputations lived and died based on the quality of their loan portfolios, and their consistency of paying back depositor savings. Today that's all but a footnote in history. Except in Vietnam.

| ||||||||||||

| Posted: 11 Apr 2012 01:00 PM PDT Batero Gold Corp's [TSX-V.BAT, BELDF.PK] first NI 43-101 compliant resource estimate for their 100% owned Quinchia porphyry in Colombia was posted on SEDAR in March. Batero has an accomplished management team, excellent geology, existing infrastructure, and support from the local community. Having visited this project and reviewed the latest technical report with management, it appears their Quinchia project has outstanding underlying value that is being overlooked by today's volatile market. Eventually Batero should get re-valued similar to other companies exploring and developing large gold-copper porphyry discoveries in the emerging Mid-Cauca Trend.

| ||||||||||||

| Silver Bullion: The Most Affordable Way to Protect Your Wealth Posted: 11 Apr 2012 12:46 PM PDT from Wealth Wire:

But believe it or not, that wasn't a real financial collapse. Just ask any Argentinean. Back in 2001, after decades of a repeated inability to repay its national debts, rating agencies finally declared Argentina in "effective default." And then came the chaos. People rushed to their local banks to pull out what was left of their savings. On November 30, 2001, central bank cash reserves fell by $2 billion in just one day. The president was forced to freeze bank accounts for an entire year and imposed a strict $250 per week limitation on personal bank withdrawals. The next day, mass protests over the withdrawal restrictions began.

| ||||||||||||

| Graham Summers: Collapse of Europe is Guaranteed! Here?s Why Posted: 11 Apr 2012 12:41 PM PDT I continue to see articles in the media claiming that Europe’s problems are solved. Either the folks writing these articles can’t do simple math, or they don’t bother actually reading any of the political news coming out of Europe [so let me present 3 data points that guarantee Europe will collapse at some point in the near future]. Words: 722 So says* Graham Summers ([url]http://gainspainscapital.com/[/url]) in edited excerpts from his original article* which Lorimer Wilson, editor of www.munKNEE.com (Your Key to Making Money!), has edited below for length and clarity – see Editor's Note at the bottom of the page. This paragraph must be included in any article re-posting to avoid copyright infringement. Summers*goes on to say, in part: Below are 3 data points that guarantee Europe will collapse at some point in the near future: Fact #1: EU Banks, as a whole, are leveraged at 26 to1 This is, of course, is based on the assets the banks are reporting. According to...

| ||||||||||||

| Campbell?s Challenge: ?Think for Yourself? When Reading This Article on Gold! Posted: 11 Apr 2012 12:41 PM PDT It doesn't take a rocket scientist to figure out that the technical picture for gold has been rapidly deteriorating…and a*look at the longer term charts*makes it clear that we have just witnessed a head and shoulders formation that has dramatically failed. The chip shot on the downside for gold here is $1,500 [maybe even]*$1,450. Bring a double dip scare for the economy into the picture, which I expect to see this summer, and $1,100 is a possibility. If you get a real stock market crash in 2013, as many analysts are predicting, and you'll get another chance to buy at $750. [That being said,] long term, I still like gold and expect it to hit the old inflation adjusted high of $2,300 during the next hard asset buying binge – but remember also that long term, we are all dead. Words: 900* So says The Mad Hedge Fund Trader, one John Thomas ([url]www.madhedgefundtrader.com[/url]), in edited excerpts from his original article.*Ian R. Campbell (www.StockResearchPortal.com) present...

| ||||||||||||

| Shilling Shuns Stocks, Sees S&P At 800 Posted: 11 Apr 2012 11:41 AM PDT In an attempt to not steal too much thunder from Gary Shilling's thought-provoking interview with Bloomberg TV, his view of the S&P 500 hitting 800, as operating earnings compress to $80 per share, is founded in more than just a perma-bear's perspective of the real state of the US economy. As he points out "The analysts have been cranking their numbers down. They started off north of 110 then 105. They are now 102. They are moving in my direction." The combination of a hard landing in China, a recession in Europe, and a stronger USD will weigh on earnings and inevitably the US consumer (who's recent spending spree has considerably outpaced income growth) with the end result a moderate recession in the US. The story is "there is nothing else except consumers that can really hype the U.S. economy" and that is supported by employment but last week's employment report throws cold water in that. "Consumers have a lot of reasons to save as opposed to spend. They need to rebuild their assets, save for retirement. A lot of reasons suggest that they should be saving to work down debt as opposed to going the other way, which they have done in recent months. So if consumers retrench, there is not really anything else in the U.S. economy that can hold things up." While the argument that the US is the best of a bad lot was summarily dismissed as Shilling prefers the 'best horse in the glue factory' analogy and does not believe investors will flock to US equities - instead preferring US Treasuries noting that "everyone has said, rates cannot go lower, they will go up, they will go up. They have been saying that for 30 years."

Links to the three-part series that Shilling (and his hosts) describe can be found here (these are notes from the longer discussions): Part 1 - Shilling Describes the key factors behind his recession call: Consumers Are the Linchpin: The U.S. economy is being fueled these days by strong consumer spending, which increased in February by 0.8 percent, its best showing in seven months, after rising 0.4 percent in January. Retail sales rose 1.1 percent in February -- the fastest pace in five months -- while same-store sales advanced 4.7 percent. These numbers correlate with recent gains in consumer confidence and sentiment. ... Spending, Saving and Debt: The support that consumer spending has received from less saving and more debt appears temporary. Household debt -- including mortgages, student loans, and auto and credit-card loans -- has fallen relative to disposable personal income, though. In my analysis, this is largely because of write-offs of troubled mortgages. Nevertheless, revolving consumer credit, mostly on credit cards, is no longer being liquidated. ... Consumer Retrenchment: The data so far aren't conclusive, but evidence of U.S. consumer retrenchment is emerging. Consumer confidence has moved up recently but remains far below the levels of early 2007 before the collapse in subprime mortgages set off the Great Recession. Real personal consumption expenditures growth has been volatile in recent months and falling on a year-on-year basis. Voluntary departures from jobs, another measure of confidence, may be decreasing. And consumer spending will no doubt have a big slide if my forecast of another 20 percent drop in house prices pans out. Housing activity remains depressed, with the only signs of life coming from the multifamily component, which is being driven by the appetite for rental apartments as homeownership declines. Homeowners are losing their abodes to foreclosures; many can't meet stringent mortgage-lending standards; some worry about homeownership responsibilities in the face of job uncertainty; and many have no desire to buy an asset that continues to fall in price. What Oil Threat?: Recently, there has been great concern about $4 per gallon gasoline and whether, as in 2008, those high prices will act as a tax on consumer incomes and force drastic cutbacks in other purchases.

Part 2 - Shilling focuses specifically on the employment picture Job openings were up 16 percent in February compared with a year earlier, but in a survey by the National Federation of Independent Business, a net zero percent of small-business owners said they planned to hire over the next three months. Furthermore, would-be entrepreneurs aren't all that enthusiastic: Only 2.7 percent of job seekers started new businesses in the last quarter, down from 12 percent in the third quarter of 2009. Job openings: The U.S. has a lot of job openings, but having endured huge layoffs in recent years, employers are being very picky in new hiring. Contrary to Federal Reserve Board Chairman Ben S. Bernanke's assertion that high unemployment is mainly a cyclical concern that will be solved by economic growth, I believe that a big part of the problem is structural. ... Business Cost-Cutting: During the sluggish business recovery that began in mid-2009, sales-volume increases for U.S. business have been tiny, and the ability to raise prices was very limited even as commodity and other input prices climbed until about a year ago. As a result, profit margins were threatened. Meanwhile, foreign competition has been fierce. ... Manufacturing productivity: Labor-intensive factories producing items such as textiles or shoes have long departed American shores for low-cost venues abroad and may never return. Those that remain -- and the type of manufacturing that is coming back to the U.S. in the much ballyhooed "reshoring" -- is robot-intensive, highly automated production that requires limited labor. Manufacturing output has recovered from its recessionary low, though not to the previous peak. Yet output per person, a measure of productivity, after the usual recessionary decline, has resumed its robust upward trend. ... Jobs up, profits down: As in the past, the large share of national income accounted for by high corporate profits is unlikely to last for long. In a democracy, neither capital nor labor keeps the upper hand indefinitely. Quite apart from the Obama administration's determined effort to redistribute income in favor of lower-income households, the seeds of narrower profit margins have already been sown. In recent quarters, productivity growth has been tiny. Have we reached bottom in terms of cost-cutting? Industrial leaders say productivity- enhancing opportunities are never exhausted, but it is possible that the low-hanging fruit has all been picked, at least for now. ... Corporate earnings implications: More jobs are about the only spur to household incomes, and consumer spending is the only source of strength in the economy this year. If new employees spend their paychecks freely, they could create more consumer demand, additional corporate revenues and profits, more jobs, and so on, in a self-feeding cycle. But, as I discussed in Part 1, new and old employees are more likely to retrench and precipitate a recession. That would cause great disappointment for corporate profits. In conjunction with a major recession in Europe, a hard landing in China and foreign-earnings translation losses caused by a rising dollar, the operating earnings of S&P 500 companies could drop to $80 per share this year, compared with Wall Street analysts' expectations of $104. That would almost guarantee a major bear market with a likely price-earnings ratio low of about 10. This implies that the S&P 500 index (SPX) would be around 800, a 43 percent drop from its recent level.

In Part 3, I'll examine why the Fed may embark on a third round of quantitative easing if the economy weakens this year and whether Congress will be tempted to enact policies of its own to address a huge fiscal drag in 2013 as payroll and income taxes rise and unemployment benefits plunge.

| ||||||||||||

| Bernanke's Right Hand Dove, Janet Yellen, Hints At ZIRP Through Late 2015 Posted: 11 Apr 2012 11:23 AM PDT Last week we had the Fed's hawks line up one after another telling us how no more QE would ever happen. We ignored them because they are simply the bad cops to the Fed's good cop doves. Sure enough, here comes Bernanke's right hand man, or in this case woman, hinting that one can forget everything the hawkish stance, and that ZIRP may last not until 2014, but 2015! Which, by the way, is to be expected: since ZIRP can never expire, it will always be rolled to T+3 years, as the short end will never be allowed to rise, until the Fed has enough FRNs in circulation to absorb the surge in rates without crushing the principal, as explained yesterday. From her speech:

Oh and this:

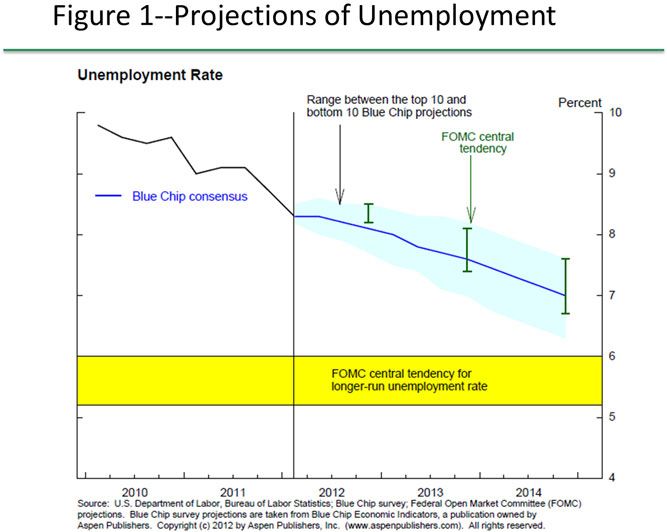

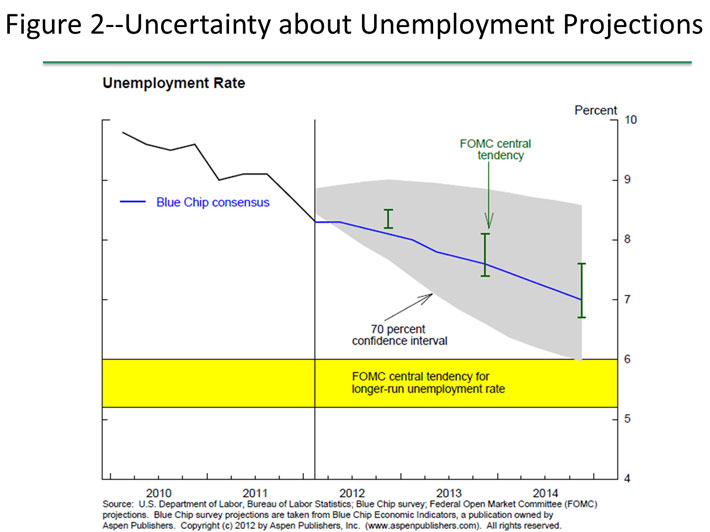

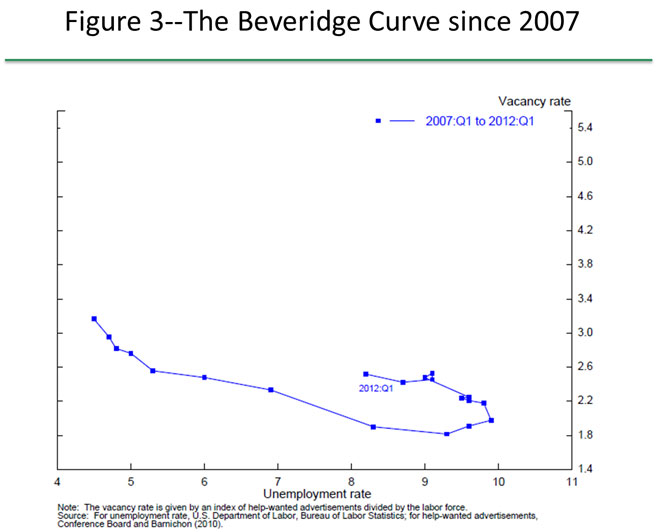

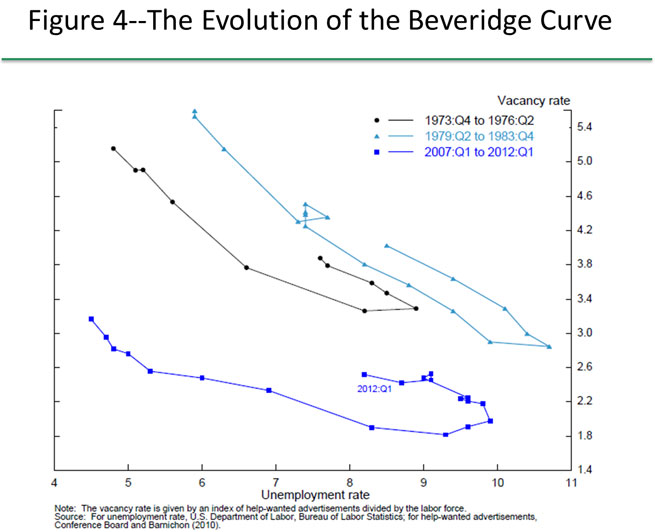

All of which explains why the EURUSD just took off. Incidentally none of this should come as a surprise to our readers: recall "Here Is Why The Fed Will Have To Do At Least Another $3.6 Trillion In Quantitative Easing" and of course "Putting It All Into Perspective." In a nutshell, there is at least another $3-4 trillion in more easing before this show is over. There is just the trivial issue of gas prices and election years to deal with but that too shall pass... in 7 months. After that, it's no holds barred CTRL+Ping. Full speech (pdf). The Economic Outlook and Monetary Policy I appreciate the opportunity to speak with you this evening. The Money Marketeers are renowned for their keen interest in the economy and monetary policy. With that in mind, I'll describe how my views concerning the stance of monetary policy relate to my assessment of the economic outlook. As you know, the Federal Open Market Committee (FOMC) issued statements following its January and March meetings indicating that it "currently anticipates that economic conditions--including low rates of resource utilization and a subdued outlook for inflation over the medium run--are likely to warrant exceptionally low levels for the federal funds rate at least through late 2014." I agreed with those judgments and, in my remarks tonight, I'll explain my views and describe some of the analytical tools that I use in making such policy decisfigure ions. I will also discuss the conditional nature of the Committee's policy stance. Let me emphasize at the outset that the remainder of my remarks reflect my own views and not those of others in the Federal Reserve System.1 The Labor Market and the Economic Outlook Starting with the labor market, as I mentioned, there have been encouraging signs of improvement in recent months. The unemployment rate had hovered around 9 percent for much of last year but moved down in the fall and averaged 8-1/4 percent in the first three months of this year, about 1-3/4 percentage points lower than its peak during the recession. And even though the latest employment report was somewhat disappointing, private sector payrolls expanded, on average, by about 210,000 per month in the first quarter, up from gains averaging around 150,000 per month during most of 2011. Other labor market indicators have shown similar improvement. This news is certainly welcome, yet it must be kept in perspective. Our economy is recovering from the steepest and most prolonged economic downturn since the 1930s, and these job gains still leave us far short of where we need to be. The level of private payrolls remains nearly 5 million below its pre-recession peak, and the unemployment rate stands well above levels that I, and most analysts, judge as normal over the longer run. Figure 1 shows the unemployment rate together with the outlook of professional forecasters from last month's Blue Chip survey.2 The solid blue line shows the Blue Chip consensus and the blue shading denotes the range between the top 10 and bottom 10 projections of forecasters in the March Blue Chip survey. The figure also shows the central tendency of the unemployment projections that my FOMC colleagues and I made at our January meeting: Those projections reflect our assessments of the economic outlook given our own individual judgments about the appropriate path of monetary policy. As in the Blue Chip consensus outlook, FOMC participants' projections indicate that unemployment will decline gradually from current levels. Included in the figure as well is the central tendency of FOMC participants' estimates of the longer-run normal unemployment rate, which ranges from 5.2 percent to 6 percent. The unemployment rate is expected to remain well above its longer-run normal value over the next several years. As you know, economic forecasts always entail considerable uncertainty. Figure 2 illustrates the degree of uncertainty surrounding projections of unemployment. The gray shading denotes a model-based 70 percent confidence interval for the unemployment rate, based on the sorts of shocks that have hit the economy over the past 40 years.3 Judging from historical experience, the consensus projection could be quite far off, in either direction. That said, the figure also shows that labor market slack at present is so large that even a very large and favorable forecast error would not change the conclusion that slack will likely remain substantial for quite some time. Some observers question just how large the shortfall from full employment really is and hence worry that further increases in aggregate demand could push up inflation. Their concern is that a large part of the rise in unemployment since 2007 is structural rather than cyclical. I agree that the magnitude of structural unemployment is uncertain, but I read the evidence as supporting the view that the bulk of the rise in unemployment that we saw in recent years was cyclical, not structural in nature. Assessments concerning the degree of slack in the labor market are highly relevant to an evaluation of the appropriate stance of policy, so I'd like to review my reasoning in some detail. First, the fact that the rise in unemployment was quite widespread across industry and occupation groups casts doubt on the hypothesis that there has been an unusually large mismatch between the types of job vacancies and the types of workers available to fill them. Certainly, job losses in the construction sector and in financial services were particularly sharp--not surprising given the collapse in the housing market and in the financial sector that we saw in 2008--but so were losses in manufacturing and other highly cyclical industries that typically are hit especially hard in recessions. Indeed, measures of the dispersion of employment changes across industries did not increase more than past experience would have predicted given the depth of the recession. Some commentators have noted that "house lock"--the reluctance or inability of homeowners to sell in a declining price environment or when underwater on their mortgages--may be preventing people from moving to find available jobs in new locations. However, evidence from migration patterns suggests that house lock is not having a significant effect on the level of structural unemployment. While migration within the United States has been trending down for some time, the reduction in mobility during the recession was not greater for homeowners than for renters, nor was it especially pronounced for areas where housing prices have declined the most and so where house lock would likely be most prevalent.4 Finally, I do not interpret data suggesting an outward shift in the Beveridge curve as providing much evidence in favor of an increase in structural unemployment. The Beveridge curve plots the relationship between unemployment and job vacancies. Cyclical variations in aggregate demand tend to move unemployment and job vacancies in opposite directions, whereas structural shifts would be expected to move vacancies and unemployment in the same direction. For instance, a structural mismatch between businesses' hiring needs and the skills of unemployed workers would tend to push up the level of vacancies for a given level of unemployment. Figure 3 plots the co-movement of unemployment and job vacancy rates since 2007.5 Consistent with a substantial decline in aggregate demand, followed by some modest recovery, movements in unemployment and vacancies since 2007 display a predominantly inverse relationship. However, figure 3 shows that as job vacancies have risen during the recovery, unemployment has declined by less than might have been expected based on the relationship that prevailed during the contraction. This outcome has led some to suggest that the Beveridge curve has shifted outward, reflecting an increase in the extent of job mismatch. In my view, a portion of this apparent outward shift in the Beveridge curve reflects increases in the maximum duration of unemployment benefits, which have been important in buffering the effects of the weak labor market on workers and their families. The influence of these benefits will dissipate as they are phased out and the economy recovers. In addition, loop-like movements around the Beveridge curve are common during recoveries. Vacancies typically adjust more quickly than unemployment to changes in labor demand, causing counterclockwise movements in vacancy-unemployment space that can look like shifts in the Beveridge curve. Figure 4 plots the relationship seen during and after the 1973 and 1982 recessions alongside the current episode. As can be seen, such counterclockwise movements also occurred during these two earlier deep recessions.6 While I do not see much evidence of any significant increase in structural unemployment so far, I am concerned that structural unemployment could increase over time if the labor market heals too slowly--a phenomenon known as hysteresis. An exceptionally large fraction of those now unemployed--more than 40 percent--have been out of work for six months or more. My concern is that individuals with such long unemployment spells could become less employable as their skills deteriorate and as they lose their connections to the labor market. This outcome does not appear to have occurred in the wake of previous U.S. recessions, but the fraction of the unemployed who have been out of work for a long period is much higher now than it has been in the past. To date, I have not seen evidence that hysteresis is occurring to any substantial degree. For example, the probability of finding a new job has not deteriorated more for individuals experiencing a long-term bout of unemployment relative to those facing shorter spells. Nonetheless, the risk that continued high unemployment could eventually lead to more-persistent structural problems underscores the case for maintaining a highly accommodative stance of monetary policy. Putting all the evidence together, I see no good reason to doubt that our nation's high unemployment rate indicates a substantial degree of slack in the labor market. Moreover, while I recognize the significant uncertainty surrounding such forecasts, I anticipate that growth in real gross domestic product (GDP) will be sufficient to lower unemployment only gradually from this point forward, in part because substantial headwinds continue to restrain the recovery. One headwind comes from the housing sector, which has typically been a driver of business cycle recoveries. We have seen some improvement recently, but demand for housing is likely to pick up only gradually given still-elevated unemployment, uncertainties over the direction of house prices, and mortgage credit availability that seems likely to remain very restricted for all but the most creditworthy buyers. When housing demand does pick up more noticeably, the huge overhang of both unoccupied dwellings and homes in the foreclosure pipeline will likely allow demand to be met for a time without a sizable expansion in homebuilding. A second headwind comes from fiscal policy. State and local governments continue to face extremely tight budget situations in light of the weak economy, depressed home prices, and the phasing out of federal stimulus grants, though overall tax revenues have been improving and that should continue as the economy expands further. At the federal level, stimulus-related policies are scheduled to wind down, while both real defense and nondefense purchases are expected to decline over the next several years under the spending caps put in place last year. A third factor weighing on the outlook is the sluggish pace of economic growth abroad. Strains in global financial markets have eased somewhat since late last year, an improvement that reflects in part policy actions taken by European authorities. Nonetheless, risk premiums on sovereign debt and other securities are still elevated in many European countries, while European banks continue to face pressure to shrink their balance sheets, and concerns about the outlook for the region remain. A further slowdown in economic activity in Europe and in other foreign economies would inhibit U.S. export growth. For these reasons, I anticipate that the U.S. economy will continue to recover only gradually and that labor market slack will remain substantial for a number of years to come. One consideration that further complicates this outlook is the inconsistency between recent movements in economic growth and employment: Unemployment has declined significantly over the past year even though growth appears to have been only moderate. This unanticipated decline in the unemployment rate presents something of a puzzle, and it creates uncertainties for the outlook and policy. To illustrate this puzzle, figure 5 plots changes in the unemployment rate against real GDP growth--a simple portrayal of the relationship known as Okun's law. It is evident from the figure that 2011 is something of an outlier, with the drop in the unemployment rate last year much larger than would seem consistent with real GDP growth below 2 percent. One possibility, highlighted by Chairman Bernanke in a recent speech, is that last year's decline in unemployment represents a catch-up from the especially large job losses during late 2008 and 2009.7 According to this hypothesis, employers slashed employment especially sharply during the recession, perhaps out of concern that the contraction could become even more severe; in particular, the figure shows that in 2009, the unemployment rate rose by considerably more than the decline in GDP would have suggested. Then, last year, employers may have become confident enough in the recovery to increase hiring and relieve the unsustainable strain that the earlier cutbacks had placed on their workforces. I think the evidence is consistent with this hypothesis, and I have incorporated it into my own modal forecast. If last year's Okun's law puzzle was largely the result of such a catch-up in hiring, I would expect progress on the unemployment front to diminish unless the pace of GDP growth picks up. After all, catch-up can go on for only so long. Of course, there are other conceivable explanations for this puzzle, including some that would point to a faster decline in unemployment in coming years. For example, GDP could have risen more rapidly over the past year than current data indicate. It will be important to pay close attention to indicators of both the labor market and GDP to try to gauge the likely pace of improvement in economic activity going forward and, hence, the appropriate stance of monetary policy over time. Let me now turn to inflation. Overall consumer price inflation has fluctuated quite a bit in recent years, largely reflecting movements in prices for oil and other commodities. For example, inflation moved up in the first part of 2011 as a rise in the price of oil and other commodities fed through to gasoline prices, and, to a lesser extent, to prices of other goods and services. Then inflation subsided after commodity prices came off their peaks. More recently, prices of crude oil, and thus of gasoline, have turned up again. But smoothing through these fluctuations, inflation as measured by the personal consumption expenditures (PCE) price index averaged 2 percent over the past two years. Using the price index excluding food and energy--another rough way to abstract from transitory fluctuations--inflation averaged about 1-1/2 percent over the past two years. These rates are lower than the inflation rates that were seen prior to the recession, and they are at or below the FOMC's long-run goal of 2 percent inflation. In my view, the subdued inflation environment largely reflects two factors. First, the substantial slack in the labor market has restrained inflation by holding down labor costs. Second, and of critical importance, longer-term inflation expectations have been remarkably stable. Like many other observers, I was concerned that inflation expectations might move lower during the recession, driving down both wages and prices in a self-reinforcing spiral. The Federal Reserve acted forcefully to resist such an outcome and, fortunately, that destructive dynamic did not take hold. Indeed, the stability of expectations has meant that the price increases driven by costs of oil and other commodities have had only temporary effects on the rate of inflation. Although firms passed higher input costs into their prices when they could do so, those one-time price increases have not led to an expectations-driven process that might have resulted in persistently higher inflation. The same key factors that have kept core inflation subdued provide the rationale for my inflation forecast. I anticipate that slack in the labor market will continue to restrain growth in labor costs and prices. And, given the stability of inflation expectations, I expect that the latest round of gasoline price increases will also have only a temporary effect on overall inflation. Indeed, if crude oil prices were to follow the downward-sloping path implied by current futures contracts, energy costs would serve as a restraining influence on overall inflation over the next several years. Figure 6 presents the central tendency of FOMC participants' projections of inflation at the time of our January meeting. Most expected inflation to be at, or a bit below, our long-run objective of 2 percent through 2014; most private forecasters also appear to expect inflation by this measure to be close to 2 percent.8 As with unemployment, uncertainty around the inflation projection is substantial. Benchmarks for Assessing Monetary Policy: Optimal Control One approach I find helpful in judging an appropriate path for policy is based on optimal control techniques. Optimal control can be used, under certain assumptions, to obtain a prescription for the path of monetary policy conditional on a baseline forecast of economic conditions. Optimal control typically involves the selection of a particular model to represent the dynamics of the economy as well as the specification of a "loss function" that represents the social costs of deviations of inflation from the Committee's longer-run goal and of deviations of unemployment from its longer-run normal rate. In effect, this approach assumes that the policymaker has perfect foresight about the evolution of the economy and that the private sector can fully anticipate the future path of monetary policy; that is, the central bank's plans are completely transparent and credible to the public.9 To show what an optimal control approach might have called for at the time of the January FOMC meeting, figure 7 depicts a purely illustrative baseline outlook constructed using the distribution of FOMC participants' projections for unemployment, inflation, and the federal funds rate that we published in January. Here, the baseline paths for unemployment and inflation track the midpoint of the central tendency of the Committee's projections through 2014. The unemployment rate gradually converges to around 5-1/2 percent--roughly the midpoint of the central tendency of participants' long-run projections of these factors--and inflation converges to the Committee's longer-run goal of 2 percent. The baseline path for the funds rate stays near zero through late 2014 and then rises steadily back to the long-run value expected by most participants. While this path is consistent with the January and March statements, I hasten to add that both the assumed date of liftoff and the longer-run pace of tightening are merely illustrative and are not based on any internal FOMC deliberations.10 Given this baseline, one can then employ the dynamics of one of the Federal Reserve's economic models, the FRB/US model, to solve for the optimal funds rate path subject to a particular loss function.11 Such a policy involves keeping the funds rate close to zero until late 2015. This highly accommodative policy path generates, according to the FRB/US model, a notably faster reduction in unemployment than in the baseline outlook. In addition, the inflation rate runs close to the FOMC's longer-run goal of 2 percent over coming years. According to the specified loss function, and in my opinion, this economic outcome would be more desirable than the baseline. One reason this exercise generates a better outcome is because it assumes that the Federal Reserve's inflation objective is fully credible--that is, all households and businesses fully understand the Federal Reserve's goals and believe that policymakers will follow the optimal policy designed to meet those goals. This belief ties down longer-term inflation expectations in the model even while it allows the lower interest rate to spur faster growth in output and employment. While optimal control exercises can be informative, such analyses hinge on the selection of a specific macroeconomic model as well as a set of simplifying assumptions that may be quite unrealistic. I therefore consider it imprudent to place too much weight on the policy prescriptions obtained from these methods, so I simultaneously consider other approaches for gauging the appropriate stance of monetary policy. Alternat | ||||||||||||

| Posted: 11 Apr 2012 11:18 AM PDT From Slope of Hope: Late last year, I paid a visit to Josh Brown ("The Reformed Broker") and had a pleasant chat. I went to his blog a week later and put up a comment, shown below, stating my belief that Facebook's IPO day would mark an important turning point in the market. I forgot all about this, but totally by chance, a few days ago, I re-visited that comment and I saw that someone had put in a snide reply. Errr, actually, Facebook only goes public one time, so I'm not sure how I could make such a declaration "a lot". It's a specific day, and I do believe that Facebook's IPO will be a seminal event. There's only one Facebook, and it has only one IPO. It's not like there are twenty other Facebook-equivalents waiting behind it, and because of the public's fascination with this offering, I do believe it'll mark a tipping point.

It got me to thinking, though, about how many data points there are pointing to a general top in everything related to the Silicon Valley. I know this Valley and its culture intimately, and I live right in the heart of it. I could throw a rock and hit Zuckerberg's house from my back yard, and I drive past the homes of tech billionaires on almost a daily basis. This isn't 1999 all over again - - - a lot of things have changed since then, so the texture of this bubble is different - - but it's a bubble (both cultural and financial) nonetheless. I offer the following anecdotal tidbits: First, Bravo (home of the "Housewives" franchise, about which I wrote this oh-so-cool post) is going to launch a reality show about the Silicon Valley. This reminds of of how Richistan was published at almost precisely the top of the financial bubble (practically to the minute). Next up is the billion (yes, billion, with a B) dollar acquisition of startup Instagram by Facebook earlier this week. Remember how people used to joke at the huge valuations companies were getting in 1999, even though the target companies had no profits? Well, Instagram is different. It doesn't even have revenue. That's right - - the P/E and P/S ratios both yield errors on any calculator you dare try. (I guess this is the kind of insane exit Color.com's investors were hoping for.....the amazing thing is that just a few days before this billion-dollar acquisition, Instagram got a fresh round of VC funding at what was considered the lunatic valuation of half that amount).

And, of course, there's Apple. The media is saturated with breathless reports about how Apple may be the world's first-ever trillion-dollar market cap company. Of course, this isn't the first time we've heard this about any particular firm (cough, Petrochina, cough, Cisco, cough), and these musings typically happen, oh, just about the time that the firm in question starts to head south. I have no idea what on Earth could slow down the Apple juggernaut, but for AAPL to simply stomp ahead and tag a trillion dollars in value now that these predictions have been wholly embraced would be, shall we say, atypical. Whether or not the NASDAQ has new highs ahead of it remains to be seen. All I can say is that, considering the extraordinarily deep and pervasive saturation of all-things-Silicon-Valley in the world at large, it just seems to me that a major contrarian event is at hand. Dennis Kneale top, anybody?

| ||||||||||||

| Goldman Previews Q2: Sees 150K Jobs Per Month Created, And A Slowing Of The Economy Posted: 11 Apr 2012 10:51 AM PDT In its latest note, Goldman is not providing any actionable "advice" which is naturally to be faded and would have been thus quite profitable, but merely updates its outlook for the second quarter, which is not pretty. The firm now expects a slowing down in the overall economy to a 2% GDP rate, and an "additional loss of momentum during the next few months", which is to be expected as every bank wants to keep the perception that NEW QE is just around the corner, as economic stagnation can rapidly become a contraction. Most importantly, the firm expects just 150,000 payrolls to be created every month, which net of the 90,000 monthly labor force increase (yes, forget what the BLS tells you - every month courtesy of demographics the American labor force grows by an average of 90k people) means that only 60k jobs will be added to offset the structural job collapse since December 2007. It also means that the pre-election rhetoric will change significantly as the economic strength from the start of the year disappears, and with it any hope of an economic upswing, providing additional ammo for exciting GOP pre-election theater. Anyway, here is the full Goldman Q2 roadmap. Which means whatever happens, the final outcome will not be what is presented below.

And the narrative:

| ||||||||||||

| Boone Pickens – Natural Gas ‘Has to be Near Bottom’ Posted: 11 Apr 2012 10:49 AM PDT Our friend, the 83-year old T. Boone Pickens says that since he was 70-years old he has paid $665 million in taxes and he doesn't like it when someone says he's not paying his 'fair share.' (We could not agree more.) Pickens says that natural gas has to be getting close to a bottom in price. He points out the rig count is plunging as the price falls. Supply will begin to tighten up, but that might take 'a little while.' We always have time to listen when Boone is talking. So should you. More in the video linked below. Source: CNBC That is all, carry on.

| ||||||||||||

| Massive Volatility Continues in COMEX Silver Warehouses Posted: 11 Apr 2012 10:44 AM PDT from Silver Doctors:

COMEX WAREHOUSE SILVER INVENTORY UPDATE 4/11/12 *Brink's reported another large withdrawal of 556,470.360 ounces out of eligible vaults

| ||||||||||||

| Europe Will Collapse in May-June Posted: 11 Apr 2012 10:43 AM PDT

The following is an excerpt from a client letter published back in mid-March. By the look of things, this forecast is playing out precisely. Starting back in August, I began suggesting that we were approaching a Systemic Crisis/ Crash scenario in the markets.

The technical and fundamentals both supported this forecast, but I completely underestimated the degree to which the Central Banks and EU would attempt to prop up the market.

At that time, I thought it likely we’d see a Crash, which would then be met with another round of stimulus, which would push the economy temporarily into the green. It seemed the most logical outcome given that we were heading into an election year with a President whose ratings were at record lows.

Instead, the Federal Reserve, particularly those Fed Presidents from Financial Centers (Charles Evans of Chicago and Bill Dudley of New York) began a coordinated campaign of verbal intervention, hinting that more easing or QE was just around the corner.

These verbal interventions coincided with coordinated monetary interventions between the Federal Reserve and other world Central Banks: first on September 15 2011 and again on November 30 2011.

The effects of both coordinated moves were short-lived in terms of equity prices, but they did send a message that the Central Banks were willing to intervene in a big way to maintain the financial system. This in turn helped to ease interbank liquidity problems in Europe (more on this in a moment) and maintain the belief that the Fed backstop or “Bernanke Put” was still in effect.

Another issue that served to push the markets higher was European leaders’ decision to go “all in” on the EU –bail out project. I’ve tracked those developments closely in previous articles.

Regarding this factor, I also underestimated the extent to which leaders would push to hold things together. After all, Greece had already received bailouts in excess of 150% of its GDP and still posted a GDP loss of 6.8% in 2011. It’s hard to believe they’d want to accept more austerity measures and more debt.

Moreover, political tensions between Greece and Germany had reached the point that Greeks were openly comparing German Chancellor Angela Merkel and Finance Minister Wolfgang Schauble as Nazis while the Germans referred to Greece as a “bottomless hole” into which money was being tossed.

Looking back on it, the clear reality was that Germany wanted to force Greece out of the EU but didn’t want to do it explicitly: instead they opted to offer Greece aid provided Greece accepted austerity measures so onerous that there was no chance Greece would go for it.

Well, Greece surprised many, including myself, and went for it. And so the EU experiment continues to exist today. However, before the end of this issue I will make it clear precisely why this will not be the case for much longer and why we are on the verge of a systemic collapse in Europe.

For starters, unemployment in Greece as a whole is now over 20%. For Greek youth (aged 15-24) it’s over 50%. The country is in nothing short of a Depression. Indeed, Greece has now experienced five straight years of contraction bringing the total contraction of Greece’s GDP to 17%. To provide some historical perspective here, when Argentina collapsed in 2001 its total GDP collapse was 20% and this was accompanied by full-scale defaults as well as systemic collapse and open riots.

With new austerity measures now in place there is little doubt Greece will see a GDP contraction of 20%, if not more. I expect we’ll see other “Argentina-esque” developments in the country as well. Put mildly, the Greek issue is not resolved.

The one thing that would stop me here would be if Greece staged a full-scale default. While the political leaders and others view a total default as a nightmare (and it would be for Greek pensions, retirees, and many EU banks), it is only a total default that could possibly solve Greece’s debt problems and allow it to return to growth.

Defaults are akin to forest fires; they wipe out all the dead wood and set the stage for a new period of growth. We’ve just witnessed this in Iceland, which did the following between 2008 and 2011:

Today, just a few years later, Iceland is posting GDP growth of 2.9%: above that of both the EU and the developed world in general. In plain terms, the short-term pain combined with moves that reestablished trust in the financial system (holding those who broke the law accountable) created a solid foundation for Iceland’s recovery.

Now, compare this to Greece which has “kicked the can” i.e. put off a default, for two years now, dragging its economy into one of the worst Depressions of the last 20 years, while actually increasing its debt load (this latest bailout added €130 billion in debt in return for €100 billion in debt forgiveness).

Iceland staged a REAL default, and has returned to growth within 2-3 years. Greece and the Eurozone in general have done everything they can to put off a REAL default with miserable results. I’ll let the numbers talk for themselves:

* Data from EuroStat

The point I’m trying to make here is that defaults can in fact be positive in the sense that they deleverage the system and set a sound foundation for growth. The short-term pain is acute (Iceland saw its economy collapse 6.7% in 2009 when it defaulted). However, a combination of defaulting and debt forgiveness (for households) can restructure an economy enough for it to begin growing again.

However, EU leaders refuse to accept this even though the facts are staring them right in the face. The reason is due to one of my old adages: politics drives Europe, NOT economics.

And thanks to the Second Greek Bailout (not to mention the talk of a potential Third Bailout which has already sprung up), we now know that EU leaders have chosen to go “all in” on the EU experiment.

Put another way, EU leaders will continue on their current path of more bailouts until one of two things happens:

Regarding #1, this process is already well underway for those countries needing bailouts. Investors must be aware that the Governments of Ireland, Portugal, Spain, and Italy have all watched/are watching the Greece situation closely.

Moreover we can safely assume that the topic of defaulting vs. asking for bailouts in return for austerity measures has been discussed at the highest levels of these countries’ respective Governments (more on this in a moment).

These discussions are also underway at those countries that are providing bailout funds. German politicians have won major political points with German voters for playing hardball with Greece. As I’ve stated before Germany may in fact be the country that ends up walking if EU continues down its current path of bailout madness.

With that in mind, there are three key political developments coming up.

Regarding #1, Ireland will be staging a referendum regarding the new fiscal requirements of the EU sometime before October. While the actual date has yet to be set, Ireland will likely stage its referendum after the French elections in (April and/or May… more on this in a moment).

Ireland has already staged two referendums which Irish citizens voted AGAINST until various concessions were made. This time around the primary concession being discussed is potential debt forgiveness (the country definitely needs it). Indeed, according the Boston Consulting Group, Ireland needs to write-off some €340 billion in debt just to make its debt levels “sustainable.”

So Ireland could easily be a wildcard here. The country is already in recession. So we need to monitor developments there as this referendum could go very, very wrong for the EU.

However, the BIG election of note is that of France where the current frontrunners are Nicolas Sarkozy (Angela Merkel’s right hand man in trying to take control of the EU) and super-socialist François Hollande.

A few facts about Hollande:

Currently polls have Sarkozy and Hollande securing the top slots in the first round of the election on April 22. This would then lead to a second election in May which current polls show Hollande winning (this has been the case in all polls for over two months).

However, there’s now another leftist wildcard coming into the mix: communist Jean-Luc Mélenchon who is now taking 11% in the polls (he was at 5% last month). And Mélenchon’s primary campaign message? Rejecting austerity measures completely via “civic uprising.”

Now, Mélenchon could end up taking votes away from Hollande therby allowing Sarkozy to win. It’s difficult to say how this will play out. But if Sarkozy loses to either of these candidates, then the EU in its current form will crumble as Germany loses its principle ally in pushing for fiscal reform and austerity measures.

Finally, let’s not forget Greece where politicians are now pushing for an election on April 29 or May 6 (the Second Bailout was passed based on new parliamentary elections being held soon after).

This could be yet another wildcard as it is around the time of the French elections, which Greek politicians will be watching closely. Remember, the key data points regarding Greece’s economy:

These facts will not play out in a victory for “pro-bailout” politicians. So the Greece deal, which is supposed to solve Greece’s problems, could actually be in danger based on a change in politics.

Remember, as stated before, politics rule Europe, not economics. And Europe now appears to be shifting towards a more leftist/ anti-austerity measure political environment. If this shift is cemented in the coming Greek, French, and Irish elections/ referendums, then things could get ugly in the Eurozone VERY quickly.

That’s the political analysis of Europe. Now let’s take a look at what the various EU economies/ markets are telling us.

Spain’s current economic condition matches that of Greece… and it hasn’t even begun to implement aggressive austerity measures. Unemployment is already 20+% without any major austerity measures having been put in place.

Anecdotal reports show Spain to be an absolute disaster. Spanish banks GREATLY underplay their exposure to the Spanish housing market (“officially” prices are down 20% but most likely it’s a lot more than that).

In simple terms, things are getting worse and worse in Spain… and the market knows it. Indeed, the charts of most EU indexes, particularly Spain, are telling us in no uncertain terms that the markets are expecting a truly horrific collapse sometime in the not so distant future. Timing this precisely is difficult but the window between May-June is the most likely time, as it will coincide with:

Now, having said all of this I have to admit I have been very early on my call for a Crash. I’m fine with admitting that. Calling a crash is difficult under normal conditions, let alone in a market that is as centrally controlled as this one. Indeed, going back to March 2009, it is clear that the Fed has been the ONLY prop under the markets as QE 1, QE lite & QE 2, and now Operation Twist 2 have all been announced any time stocks staged a sizable correction (15+%). In fact, on a weekly chart of the S&P 500 going back four years, we find two items of note:

Aside from these monetary interventions, we also have to deal with the Fed’s verbal interventions: every time stocks start to break down some Fed official (usually Charles Evans or Bill Dudley) steps forward and promises more easing… or the Fed releases some statement that it will maintain ZIRP an additional year… and VOOM! stocks are off to the races again.

With that in mind, I will admit I’ve been caught into believing a Crash was coming several times in the last few years. In some ways I was right: we got sizable corrections of 15+%. But we never got the REAL CRASH I thought we would because the Fed stepped in.

So what makes this time different?

Several items:

Let me walk through each of these one at a time.

Regarding #1, we have several facts that we need to remember. They are:

So we’re talking about a banking system that is nearly four times that of the US ($46 trillion vs. $12 trillion) with at least twice the amount of leverage (26 to 1 for the EU vs. 13 to 1 for the US), and a Central Bank that has stuffed its balance sheet with loads of garbage debts, giving it a leverage level of 36 to 1.

And all of this is occurring in a region of 17 different countries none of which have a great history of getting along… at a time when old political tensions are rapidly heating up.

So if you’re not already taking steps to prepare for the coming collapse, you need to do so now. I recently published a report showing investors how to prepare for this. It’s called How to Play the Collapse of the European Banking System and it explains exactly how the coming Crisis will unfold as well as which investment (both direct and backdoor) you can make to profit from it.

This report is 100% FREE. You can pick up a copy today at: http://www.gainspainscapital.com

Good Investing!

Graham Summers

PS. We also feature numerous other reports ALL devoted to helping you protect yourself, your portfolio, and your loved ones from the Second Round of the Great Crisis. Whether it’s a US Debt Default, runaway inflation, or even food shortages and bank holidays, our reports cover how to get through these situations safely and profitably.

And ALL of this is available for FREE under the OUR FREE REPORTS tab at: http://www.gainspainscapital.com

| ||||||||||||