Gold World News Flash |

- Lars Schall discusses with financial journalist Nomi Prins from the United States and fund manager Wesley Legrand from Australia issues related to the precious metal markets, central bank policies, and the parallels between our days and the age of the Gre

- Skip forward to 6 minute mark, Max and Alex Jones live from Syntagma Sq. This video is very hot in Greece right now

- James Turk Report - Why Gold Will Go Above $11,000

- Jim Rickards - Extremely High Risk of US Dollar Collapse

- Key Events In The Week Ahead

- Does One ‘Super-Corporation' Run the Global Economy?

- Fed manipulates with propaganda, dollar is at risk, Rickards tells King World News

- SLV And Silver Manipulation

- The Myth of Over-Regulation

- Lawrence Williams: Governments manipulate currencies, so why not gold too?

- Peter Koven: To boost share prices, gold miners should pay more dividends

- Weekly metals review and Davies, Embry interviews at King World News

- Jeff Christian now just makes it up as he goes along

- Silver Summit’s debate on precious metals market manipulation posted at Kitco

- 25th Anniversary Silver Eagle Coin Set Price at $299.95

- US Mint Sales: Silver Eagle Uncirculated Coin Recovers, 9/11 Medals Down

- Stock World Weekly: Fear and Loathing in the Eurozone

- Riot Granny in Athens!

- The Eurozone Wags the Gold and Silver Dog

- Savers Protect Your Deposits From Bankrupting Banks and Quantitative Inflation

- Nicolas Sarkozy Steals a Line From Max Keiser and Tells Cameron to STFU!

- Trend and Cycle Summary

- I Think This Is What They Call Fascism

- Reggie Middleton: Warning! This is going to be a highly, highly controversial post.

- Chaos in the Land of Oz, Part 2

- A New, Simple Way to Play the Dow to Gold Ratio

- A Simple (Humorous) Look At Bank Derivatives

- Guest Post: The European Financial Crisis In One Graphic: The Dominoes Of Debt

- Exclusive Interview With Diapason's Sean Corrigan

| Posted: 23 Oct 2011 06:51 PM PDT Market Manipulation and the Second Great Depression Don't be fooled by GLD or SLV. Only GoldMoney offers real bullion allocated in your name.

|

| Posted: 23 Oct 2011 06:07 PM PDT Don't be fooled by GLD or SLV. Only GoldMoney offers real bullion allocated in your name.

|

| James Turk Report - Why Gold Will Go Above $11,000 Posted: 23 Oct 2011 04:36 PM PDT  With continued uncertainty surround the gold and silver markets, James Turk, Founder & Chairman of GoldMoney put together the following piece exclusively for King World News. One of the primary reasons why Turk wanted to release this to the KWN readers globally is because he is often asked what is his basis for predicting $10,000 gold and higher in his King World News interviews. The following extraordinary piece is what resulted... With continued uncertainty surround the gold and silver markets, James Turk, Founder & Chairman of GoldMoney put together the following piece exclusively for King World News. One of the primary reasons why Turk wanted to release this to the KWN readers globally is because he is often asked what is his basis for predicting $10,000 gold and higher in his King World News interviews. The following extraordinary piece is what resulted...

This posting includes an audio/video/photo media file: Download Now |

| Jim Rickards - Extremely High Risk of US Dollar Collapse Posted: 23 Oct 2011 04:02 PM PDT  With so much uncertainty in gold, silver, stocks and currency markets, today King World News has released the eagerly anticipated audio interview KWN Resident Expert Jim Rickards, Senior Managing Director at Tangent Capital Markets. When asked about the risks of current Fed policies, Rickards replied, "What's interesting, Eric, is that it shows how this is all manipulation. I'm describing how the Fed is thinking about it, but that doesn't mean it makes sense, it doesn't mean they are right. And what it shows you is they are trying to manipulate us every way they can. The targeting policy is designed to manipulate you into thinking inflation is right around the corner." With so much uncertainty in gold, silver, stocks and currency markets, today King World News has released the eagerly anticipated audio interview KWN Resident Expert Jim Rickards, Senior Managing Director at Tangent Capital Markets. When asked about the risks of current Fed policies, Rickards replied, "What's interesting, Eric, is that it shows how this is all manipulation. I'm describing how the Fed is thinking about it, but that doesn't mean it makes sense, it doesn't mean they are right. And what it shows you is they are trying to manipulate us every way they can. The targeting policy is designed to manipulate you into thinking inflation is right around the corner."

This posting includes an audio/video/photo media file: Download Now |

| Posted: 23 Oct 2011 03:32 PM PDT You mean, aside from the relentless headline barrage? Why yes, in a vivid reminder of what used to happen when actual fact-based events mattered, here is a complete summary of the key events in the coming week. From Goldman Sachs: Last week was a week of consolidation after the short-covering rally in the two previous weeks. Range-bound price action dominated across asset classes as investors were being kept busy following the European news, while macro data continued to stabilise at low levels. In the week ahead, this pattern of stabilising macro data and Eurozone policy meetings will continue. Of course, the focus is on the EU summit on Wednesday, though expectations are not particularly high after weeks of continued negotiations and repeat summits. After the latest meetings this weekend, the details on bank recapitalisation, PSI involvement in the Greek bailout and a leverage scheme for the EFSF remain vague. While Eurozone leaders continue their debate, the week will also deliver a batch of interesting macro data in the Eurozone. Starting with the preliminary Eurozone PMI, we also get German consumer confidence and CPI data. Italy publishes consumer confidence as well and retail sales. Finally, Italy will try to issue EUR5-6bn in bonds on Thursday and Friday, possibly the first serious test of market confidence after the Summit on Wednesday. The potential for a substantial Dollar sell-off and notable Euro rally is clearly there. Positioning data suggests continued stretched Dollar shorts against pretty much any currency, including the Euro. A quick and convincing solution to the Eurozone crisis could therefore lead to a sharp reduction in the Eurozone risk premium. Having said this, uncertainty remains high and our base case is for "muddling through" rather than a quick and convincing Eurozone solution. Last week's modest strengthening of the CHF and the JPY may have been a warning sign that currency markets also remain skeptical. It may therefore take a bit longer before the September risk aversion moves can be unwound further. Beyond the focus on the Eurozone, there are a number of central bank meetings this week (HUF, CAD, NZD, SEK, JPY, INR, ILS, RUB), with only the RBI expected to tighten monetary policy in India, as inflation pressures remain high. Finally, in the US, third-quarter GDP and durable goods orders will likely be the key focus. Monday 24th Euro-zone Oct flash PMIs: Consensus expects the manufacturing PMI to fall by 0.4 to 48.5. HSBC China Flash PMI: The last reading stood at 49.9. The latest one just printed at 51.1 Also Interesting: Fed Dudley speech, Israel monetary policy meeting is expected to leave rates unchanged. Tuesday 25th Germany Consumer Confidence: Consensus expects a virtually unchanged reading at 5.1. Italy consumer confidence and retail sales: Given the focus on Italian debt sustainability in the market, retail sales and consumer sentiment may provide indications about cyclical strength. Consensus expects basically unchanged numbers. Hungary MPC meeting: We and consensus expect rates to stay on hold at 6.0%. BoC policy meeting: Consensus expects no change from 1.00%. US Oct Consumer Confidence: Consensus expects 46 after 45.4 in Sep. This is the monthly Conference Board survey. Wednesday 26th Australia Q3 CPI: We expect 3.5%yoy, in line with consensus after 3.6% in Q2. US Sep Durable goods orders: Consensus expects -0.8%mom after -0.1% in Aug. EU Summit: According to EU Commission President Barroso, final decisions about the Euro-area debt crisis will be made at this summit. Also Interesting: US new home sales. Thursday 27th US Q3 GDP: We expect 2.5%, in line with consensus after 1.3% in Q2. RBNZ Meeting: Consensus expects no change from 2.50%. Riksbank Meeting: Consensus expects no change from 2.00%. BoJ Meeting: We expect no change from 0.10%, in line with consensus. Regional German CPI data: Last month, these numbers were the first to indicate rising inflation pressures in the Eurozone core. Also interesting: US jobless claims, Speech by Bundesbank Chef Weidmann, Turkey trade balance (Sep). Friday 28th Japanese Inflation and Industrial Production: consensus expects the data to paint a deflationary picture with faster-falling price indices and a notable drop in IP (-2.1% mom) Italian Bond Auction: This could well be one of the first serious tests to see if the EU summit earlier in the week helped improve market confidence. Russia Monetary Policy meeting: We and consensus expect unchanged rates at 3.75%. US Sep Personal Income: Consensus expects 0.3%mom after -0.1% in Aug. US UMich consumer sentiment: This is the final reading, which is expected to show only very marginal improvements compared to the preliminary reading. Swiss KOF leading indicator: This is expected to drop notably to about 1.04 from 1.21, according to GS and consensus. Also interesting: UK consumer confidence.

|

| Does One ‘Super-Corporation' Run the Global Economy? Posted: 23 Oct 2011 03:00 PM PDT [Ed Note: Can you say "House of Rothschild"?]

Study claims it could be terrifyingly unstable By Rob Waugh A University of Zurich study 'proves' that a small group of companies – mainly banks – wields huge power over the global economy. The study is the first to look at all 43,060 transnational corporations and the web of ownership between them – and created a 'map' of 1,318 companies at the heart of the global economy. The study found that 147 companies formed a 'super entity' within this, controlling 40 per cent of its wealth. All own part or all of one another. Most are banks – the top 20 includes Barclays and Goldman Sachs. But the close connections mean that the network could be vulnerable to collapse.

|

| Fed manipulates with propaganda, dollar is at risk, Rickards tells King World News Posted: 23 Oct 2011 02:05 PM PDT 10:08p ET Sunday, October 23, 2011 Dear Friend of GATA and Gold: Geopolitical analyst James G. Rickards tells King World News that the Federal Reserve increasingly is trying to manipulate markets with mere propaganda and that the United States risks the collapse of the dollar if it doesn't drastically change its fiscal, monetary, and tax policies. Rickards says he buys the dips in gold. The interview is 20 minutes long and you can listen to it at King World News here: http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2011/10/24_J... CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT The United States Once Again Can Establish a Stable Dollar Worth Its Weight in Gold Lewis E. Lehrman, chairman of the Lehrman Institute, sponsor of The Gold Standard Now project, has released a plan to restore economic growth through a stable dollar. The plan, titled "The True Gold Standard: A Monetary Reform Plan Without Official Reserve Currencies," responds to the recurrent economic crises of the last century and outlines a detailed proposal for America's leadership on "how we get from here to there." That is, how we get from the present unstable paper dollar to a stable dollar as good as gold. James Grant, author and editor of Grant's Interest Rate Observer, says of the Lehrman plan: "If you have ever wondered how the world can get from here to there -- from the chaos of depreciating paper to a convertible currency worthy of our children and our grandchildren -- wonder no more. The answer, brilliantly expounded, is between these covers. America has long needed a modern Alexander Hamilton. In Lewis E. Lehrman the country has finally found him." To learn more and to sign up for The Gold Standard Now's free, noncommercial, weekly report, "Prosperity through Gold," please visit: http://www.thegoldstandardnow.org/gata Join GATA here: New Orleans Investment Conference http://www.neworleansconference.com/ Support GATA by purchasing gold and silver commemorative coins: https://www.amsterdamgold.eu/gata/index.asp?BiD=12 Or by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Or a video disc of GATA's 2005 Gold Rush 21 conference in the Yukon: Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: ADVERTISEMENT Be Part of a Chance to Discover Multi-Million-Ounce Gold and Silver Deposits in Canada Northaven Resources Corp. (TSX-V:NTV) is advancing five gold and silver projects in highly prospective and politically stable British Columbia, Canada. Check out the exploration program on our Allco gold/silver project : -- A large (13,000 hectare) property, covering more than 15 square kilometers of a regional mineralized trend just 3km from a recently announced 1.2-million-ounce gold and 15-million-ounce silver deposit. -- The property hosts historic high-grade silver workings and many mineral showings as well as former mines at the property's northern and southern boundaries. -- A deep-penetrating airborne geophysics survey has just been completed on the entire property and neighboring deposits and its results are eagerly awaited. To learn more about the Allco property or Northaven's other gold and silver projects, please visit: http://www.northavenresources.com Or call Northaven CEO Allen Leschert at 604-696-3600.

|

| Posted: 23 Oct 2011 12:30 PM PDT By Jeff Nielson, Bullion Bulls Canada JP Morgan is the largest silver short-seller in the history of the world. JP Morgan is the "custodian" for the largest "long" silver fund in the history of the world, making this one of the largest conflicts of interest in all of history. If the unit-holders of the iShares Silver Trust (or "SLV") make a small amount of profit on their holdings (per unit), JP Morgan suffers massive losses on its "short" position in the futures market – and then at least one hundred times that amount of additional losses on its unimaginably huge, leveraged, silver derivatives. We know this thanks to the loquacious banker, Jeffrey Christian, formerly of Goldman Sachs and now head of the CPM Group, one of two "consultancies" who are quasi-official record-keepers for the gold and silver markets. Obviously JP Morgan has a gigantic personal incentive to try to make sure that holders of SLV units make as little as possible on their investment. This alone should disqualify JP Morgan from serving as "custodian" for all of the silver JP Morgan supposedly holds on behalf of those unit-holders. Amazingly, with JP Morgan claiming to be sitting on the two largest, single silver-holdings in all the world it has never been required to have both of those holdings audited/verified. Thus JP Morgan has been able to indulge in this blatant conflict of interest while so-called "regulators" actually help it to conceal its activities. However, the absurdity of allowing the world's largest "silver fox" to guard the world's largest "silver henhouse" with absolutely no public scrutiny is only the beginning of this outrage. Those who follow the silver market will have noted an amazing "coincidence" in recent years since the creation of SLV: JP Morgan's massive short position always closely mirrors the size of the total holdings of SLV. This led me immediately to a rather obvious conclusion. Each time someone purchases a unit of SLV, JP Morgan uses the proceeds to acquire that one ounce of silver (as it is supposed to do). However, instead of that silver being used to "back" that unit of SLV (in JP Morgan's role as "custodian"), JP Morgan increases its short position by one more ounce – and then uses the new silver to back its own short position (in JP Morgan's role as "greedy banker"). Note that as long as the supposed "regulator" of the silver market (the CFTC) never requires JP Morgan to demonstrate that it has enough silver to "back" both its own, massive short position and its own, massive custodian obligation, then there is nothing stopping JP Morgan from permanently/perpetually using the "long" investors of SLV to fund and "back" virtually its entire shorting operation in the Comex futures market. Should an ordinary individual acquire the power of invisibility, and thus be able to monitor JP Morgan's secret silver hoard inside its bullion vault, what they would undoubtedly see is an impressive mountain of silver. On 364 of the 365 days of the year, there would be a sign in front of that stack of bullion reading "JP Morgan's short position", while on that other day of the year (when SLV's "auditor" shows up to supposedly verify that JP Morgan is honouring its duty as "custodian") the sign in front of the bullion is changed to read "iShares Silver Trust". It is a neatly symmetrical scam, and one only made possible in the U.S.'s "world" of faux-regulators. However, one aspect of this sham always bothered me despite its wonderful symmetry. Knowing how Wall Street banksters love to leverage everything they touch by at least 30:1 (and in the case of silver derivatives by more than 100:1) it always seemed oddly conservative that JP Morgan's SLV sham was leveraged by a mere 2:1. Enter (again) Jeffrey Christian. It was Jeffrey Christian who helped to confirm the existence of gold manipulation in "The Great Gold Debate" between himself and GATA stalwart, Bill Murphy. Immediately after Christian claimed that he had "never seen" any evidence of gold manipulation in all of his years as a banker, he then proceeded to describe some of those acts of manipulation. One example Christian gave was how the bullion banks would (falsely) spread rumors that a particular European central bank was about to dump more gold onto the market, in order to "spook" the longs and depress the price. When I heard that Murphy and Christian were going to reprise their roles in a second debate (at the current "Silver Summit"), this time with greater emphasis on the silver market, I couldn't wait for what new revelations would slip past Christian's lips. I wasn't disappointed, as Christian was kind enough to supply the reasoning behind JP Morgan's mere 2:1 leveraging of SLV's silver (i.e. 100% of the silver for JP Morgan, 0% of the silver for SLV unit-holders). More articles from Bullion Bulls Canada….

|

| Posted: 23 Oct 2011 12:27 PM PDT By Jeff Nielson, Bullion Bulls Canada Perhaps the worst crime committed by the corporate Oligarchs who now dominate our lives was their successful efforts to rewrite much of "history", and then use the mythology they created to brainwash us. The two most insidious and damaging of the myths they created were that unionization was bad for economies and that regulation was bad for economies. The facts are quite clear here, however. The 1960's marked the absolute zenith in the Western world for both unionization and regulation. Consequently, the 1960's also represented the all-time peak in our standard of living, and the all-time peak in the prosperity of our economies. Since that time (and during the rise of the Oligarchs), they have pursued two goals with ruthless tenacity: union genocide and the abolition of all "regulation". Consequently, over the past 40 years we have seen our standard of living plummet across the Western world, while our ever more anemic economies drowned themselves in debt. This particular piece will focus on the irreparable economic damage which the Oligarchs have caused with their myth of "over-regulation" – and the era of deregulation they spawned. The examples of the failure of this policy are practically infinite, as "deregulation mania" has engulfed the tiny minds of our politicians and (supposed) "regulators" throughout the past four decades. One of the first (and most illuminating) examples of deregulation at work was the destruction of the global airlines industry. Because of the massive capital investments required in this sector as part of the continuing costs of doing business, the oligopoly model was a necessary evil in the airline industry. Smaller nations had a single (and often public) airline which represented their entire market, while the largest of markets (the U.S. ) had a handful of companies in its own airline oligopoly. During the 1960's the airline industry represented a triumph of capitalism: an oligopoly model which was not inherently parasitic and/or self-destructive – despite the fact that roughly four centuries of capitalist theory has taught us that monopolies and oligopolies are the ultimate evil. How did the global economy avoid being victimized by the airlines oligopoly? Through a veritable straitjacket of regulation. Virtually every facet of the industry was tightly regulated – in harmony with other markets – with the result being a stable and modestly profitable industry. Then came deregulation. What has followed is four decades of bankruptcies, bail-outs, and economic chaos. The absence of regulation resulted in the Airlines Oligarchs doing what Oligarchs always do: exterminate as much of the competition as possible – and then collude with the survivors. "Customer service" has become an anachronism, as the parasitic Oligarchs take as much as possible, while giving as little as they can in return. In short, four decades of deregulation has helped no one, not even the airlines themselves. Almost simultaneously with the deregulation of the airline industry came the deregulation of the trucking industry in North America (with our vast network of highways and supply-chains). Same result: total destruction. Bankruptcies occurred across the trucking industry. The standard of living for truck-drivers plummeted (along with safety standards) as "competition" forced the drivers to put in longer and longer hours, cut corners on maintenance, and do all the other things typical of unregulated industries. More articles from Bullion Bulls Canada….

|

| Lawrence Williams: Governments manipulate currencies, so why not gold too? Posted: 23 Oct 2011 12:27 PM PDT GATA 2:47p ET Sunday, October 23, 2011 Dear Friend of GATA and Gold: MineWeb's Lawrence Williams today comments on the recent exchanges between GATA and CPM Group executive Jeffrey Christian and goes on to wonder why gold price manipulation should be so surprising. Williams writes: "If one assumes that governments as a matter of course manipulate currency exchange rates, then there is logic in their manipulating the gold price too, as many throughout the world consider gold as money (currency) and a rise in the gold price thus equates to a depreciation in currencies — notably the U.S. dollar." Williams' commentary is headlined "Gold Anti-Trust Action Committee Spat with Jeff Christian Getting Personal" and you can find it at MineWeb here: http://www.mineweb.com/mineweb/view/mineweb/en/page72068?oid=138052&sn=D… CHRIS POWELL, Secretary/Treasurer Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit:

|

| Peter Koven: To boost share prices, gold miners should pay more dividends Posted: 23 Oct 2011 12:27 PM PDT GATA Gold Paying Dividends By Peter Koven http://business.financialpost.com/2011/10/21/gold-paying-dividends/ Gold mining investors got two interesting pieces of news to chew on this week. One demonstrated why equities have largely underperformed the gold price over the last few years, and the other showed one way that trend could potentially end. The bad news came from Agnico-Eagle Mines Ltd., which stunned the street on Wednesday by shutting down its Goldex mine because of rock stability problems. As Agnico shares tumbled 18%, investors couldn't help but wonder: Why buy gold stocks when the exchange-traded funds have much less risk? The Goldex debacle seemed to embody everything wrong with the miners, who are creating little shareholder value despite record profits. The positive news got a lot less attention. On Monday, Eldorado Gold Corp. announced an enhancement to its dividend policy that links the payout more closely to the gold price. The company demonstrated that its dividend per ounce of gold sold will rise progressively from US$100 (when gold is less than US$1,549 an ounce) to US$225 (when gold reaches US$1,850). The price-linked dividend is a smart strategy, experts say, because it attracts yield-seeking investors while forcing reluctant miners to part with more of their cash when gold prices go up. "The reality is that gold mining companies have been criticized, and rightfully so, for not [offering] what people look for in real businesses. And that is yield," Eldorado chief executive Paul Wright says. "That there has been such demand for ETFs is largely a reflection of the inability of gold mining companies to provide an alternative in terms of yield." Gold miners have been raising their dividends over the past year, but they are still nominal at best. Most senior producers pay a yield between 0.5% and 1.5%, which has not been enough to draw new investors. Mr. Wright's view is that a level of about 2% would be taken more seriously, and it would provide a genuine advantage for equities that you can't get from ETFs. The price-linked dividend is one way to get there, and the leader in this strategy is Newmont Mining Corp. Under the Newmont plan, introduced in April, the company's annual dividend rises by US20 cents a share for each US$100 rise in the gold price (and the payout rises even more when gold tops US$1,700). The idea was welcomed with open arms by investors, and Newmont now has a dividend yield of roughly 2%, the highest among major producers. "If you look at the Newmont stock chart, they were adrift," says George Topping, an analyst at Stifel Nicolaus. "And in a stroke of genius, someone came up with the idea to link the dividend to the gold price. That transformed the company in the eyes of many investors and caused fund flows into the stock." That raises the obvious question of why other senior producers like Barrick Gold Corp., Goldcorp Inc., and Kinross Gold Corp. don't follow Newmont's lead. So far, only three precious metal companies (Newmont, Eldorado, and Hecla Mining Corp.) have adopted the fixed payout model. Mr. Topping does not expect the other seniors to do it for two reasons: They don't want to be seen as copycats, and they simply cannot afford it because they need to spend billions of dollars on mine construction. Ironically, Newmont's weaker growth prospects turned out to be a positive as it left the company more free cash to return to investors. That doesn't change the fact that the other seniors could pay higher dividends if they wanted to. Industry experts anticipate more increases in the months ahead, and there could be some next week as the gold miners begin reporting third-quarter earnings. But the pace of dividend hikes has been very slow, and no one thinks that is going change. Part of the reason is that gold miners made virtually no money through most of their history, so they're just not eager to give it away now. "It's almost difficult for them to release their cash," says Dennis da Silva, resource fund manager at Middlefield Capital. "It's taken years for them to get to this position where there's so much free cash flow." He likes the idea of the price-linked dividend because it provides complete visibility for shareholders; they can plug in their own expectations on the gold price and calculate the dividend for themselves. That alone could be appealing for income investors, who may be bullish on gold but need to see more yield in the stocks. "I think you would get the marginal buyer who has become disenchanted with gold companies and their seeming inability to generate stellar stock price movement," says John Stephenson, senior vice-president and portfolio manager at First Asset Investment Management. That would be just fine for gold miners, who need to find a way to build more shareholder value. They have never been in a better position to do it than they are right now. "At these prices, if it's not a healthy industry, I'm not quite sure what we're waiting for," Mr. Wright says. Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit:

|

| Weekly metals review and Davies, Embry interviews at King World News Posted: 23 Oct 2011 12:27 PM PDT GATA 5:21p ET Saturday, October 22, 2011 Dear Friend of GATA and Gold (and Silver): "Consolidation" is the word from both Bill Haynes of CMI Gold and Silver and futures market analyst Dan Norcini in their weekly review of the precious metals markets at King World News: http://www.kingworldnews.com/kingworldnews/Broadcast/Entries/2011/10/22_… Meanwhile, full audio of the recent King World News interview with Hinde Capital CEO Ben Davies can be heard here: http://www.kingworldnews.com/kingworldnews/Broadcast/Entries/2011/10/22_… And full audio of the recent King World News interview with Sprott Asset Management's John Embry can be heard here: http://www.kingworldnews.com/kingworldnews/Broadcast/Entries/2011/10/22_… CHRIS POWELL, Secretary/Treasurer Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit:

|

| Jeff Christian now just makes it up as he goes along Posted: 23 Oct 2011 12:27 PM PDT GATA 2:46p ET Saturday, October 22, 2011 Dear Friend of GATA and Gold: Debating GATA Chairman Bill Murphy yesterday at the Silver Summit in Spokane, Washington, CPM Group executive Jeffrey Christian graduated from his usual distortions to outright contrivance. The subject was one of the cables from the U.S. embassy in Beijing, China, to the State Department in Washington that were disclosed recently by the Wikileaks organization. Murphy characterized the cable as signifying the Chinese government's awareness of the Western central bank gold price suppression scheme. Christian disputed that. He replied: "What the cable said was the Chinese government asked for information related to allegations that they'd heard in the market from GATA about that, and what would the U.S. government say in response to those allegations? It didn't say that the Chinese government believed it. … That's typical of taking a piece of information and twisting it and dropping off a couple of important words and making it fit your theory as opposed to the reality." In fact the cable, quoting commentary published in a Chinese government newspaper, Shijie Xinwenbao (World News Journal), on April 28, 2009, said nothing at all about allegations heard from GATA and made no inquiry of the U.S. government. Rather, the commentary quoted in the cable was exactly as Murphy characterized it: a flat-out assertion of gold price suppression. GATA didn't "twist" it or "drop off a couple of important words." Here is the text of the quotation in the cable: "According to China's National Foreign Exchanges Administration, China's gold reserves have recently increased. Currently, the majority of its gold reserves have been located in the United States and European countries. The U.S. and Europe have always suppressed the rising price of gold. They intend to weaken gold's function as an international reserve currency. They don't want to see other countries turning to gold reserves instead of the U.S. dollar or euro. Therefore, suppressing the price of gold is very beneficial for the U.S. in maintaining the U.S. dollar's role as the international reserve currency. China's increased gold reserves will thus act as a model and lead other countries toward reserving more gold. Large gold reserves are also beneficial in promoting the internationalization of the renminbi." The cable can be found here: http://cables.mrkva.eu/cable.php?id=204405 And here: http://www.gata.org/files/USEmbassyBeijingCable-04-28-2009.txt The exchange about the cable during the debate at the Silver Summit begins at 15:40 in the video at Kitco here: http://www.kitco.com/falltour2011/debate.html During the debate Christian also sought to misrepresent Barrick Gold's motion to dismiss the federal anti-trust lawsuit brought against it by Blanchard Coin and Bullion, a motion in which Barrick sought to claim for itself the sovereign immunity of central banks against lawsuit. Indeed, for some time now Christian has been promoting a package of misrepresentations and distortions about some of the gold price suppression evidence collected by GATA, misrepresentations and distortions GATA answered in detail a year and a half ago here: The guy isn't just misrepresenting and distorting now; he's making stuff up from scratch. But maybe we're lucky that this is the best the other side can do on the rare occasions when it comes out to answer for itself. CHRIS POWELL, Secretary/Treasurer Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit:

|

| Silver Summit’s debate on precious metals market manipulation posted at Kitco Posted: 23 Oct 2011 12:27 PM PDT GATA 10:06a ET Saturday, October 22, 2011 Dear Friend of GATA and Gold: Video of yesterday's debate at the Silver Summit in Spokane, Washington, between GATA Chairman Bill Murphy and CPM Group founder Jeff Christian over whether the precious metals markets are manipulated has been posted at Kitco. It's a half hour long and you can watch it here: http://www.kitco.com/falltour2011/debate.html CHRIS POWELL, Secretary/Treasurer Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit:

|

| 25th Anniversary Silver Eagle Coin Set Price at $299.95 Posted: 23 Oct 2011 12:26 PM PDT Answering the question many collectors have been asking since the announcement of its release, the United States Mint has indicated the American Eagle 25th Anniversary Silver Five-Coin Set will initially sell for $299.95. As is standard for precious metal products from the Mint, that pricing is subject to change based on market trends leading up to the [...]

|

| US Mint Sales: Silver Eagle Uncirculated Coin Recovers, 9/11 Medals Down Posted: 23 Oct 2011 12:26 PM PDT After two straight weekly declines, sales of the American Silver Eagle uncirculated coin finally came through with a positive increase on the week. Due to their suspension in late September and resulting $9.50 price cut, their two previous weekly sales totals had been trimmed 424 and 11,476, respectively, as cancellations and returns were processed. Finally, [...]

|

| Stock World Weekly: Fear and Loathing in the Eurozone Posted: 23 Oct 2011 11:23 AM PDT Stock World Weekly: Fear and Loathing in the Eurozone Late Thursday afternoon, Jon Hilsenrath of the Wall Street Journal, a well-known sounding board for Bernanke when he wants to give signals to the markets, reported "Federal Reserve officials are starting to build a case for a new program of buying mortgage-backed securities to boost the ailing economy, though they appear unlikely to move swiftly." (Fed Is Poised for More Easing) This report builds on sentiments that Federal Reserve Governor Daniel Tarullo expressed in a speech on Thursday evening. Bloomberg reported "Federal Reserve Governor Daniel Tarullo's call for resuming large-scale purchases of mortgage bonds may boost chances the central bank will start a third round of asset buying aimed at reviving U.S. growth. "Policy makers should move the tool 'back up toward the top of the list' because it would help the economy through lower mortgage costs that would boost home purchases and spending by people who refinance their home loans, Tarullo said late yesterday in a speech in New York." Tarullo's speech and Hilsenrath's article both came out on Thursday, suggesting the Fed is making an effort to broadcast its seriousness about using its tools to jump-start the moribund U.S. economy. Any large-scale program of buying bonds will essentially be another round of quantitative easing (QE3), predictably leading to increases in stock and commodity prices. However, regarding commodity prices, one event last week may put a damper on increases in commodity prices. On Tuesday, the Commodity Futures Trading Commission (CFTC) voted to put position limits on commodity markets, as it attempts to deal with problems created by runaway speculation. Phil has repeatedly reported on the manipulation in the oil markets, with articles such as last June's "Which Way Wedne$day - Let's Break the $peculator$." Tuesday's action, while welcome, is long overdue.

Europe will be the focus of the financial news again next week. German Chancellor Merkel and French President Sarkozy will try to work out a deal to give additional funding and more discretionary power to the EFSF, while simultaneously strengthening "economic integration" and capitalization of European banks, all under the auspices of implementing "economic governance of the euro area." Achieving their goals would be historic by any measure. A primary issue at the heart of the struggle is whether the theoretically unlimited funding of the European Central Bank (ECB) can be used to 'backstop' the EFSF, thereby guaranteeing sufficient capital to recapitalize banks and buy distressed bonds. While Sarkozy is a strong proponent of backstopping the EFSF with ECB funding, going so far as to abandon his wife during childbirth to travel to Frankfurt to make his case to Chancellor Merkel, his efforts were in vain. Merkel, backed by ECB President Jean-Claude Trichet, adamantly refused to consider Sarkozy's proposal. As the UK Telegraph noted "Europe's central bank could not be used to boost the EFSF because of a 20-year EU treaty clause forbidding the union from using its cash to save European governments. Unlike the EFSF, an ad hoc inter-governmental 'special purpose vehicle' based in Luxembourg, the ECB is governed by the detailed chapter and verse of European law." According to a senior EU diplomat, "If the ECB could act like a national central bank that would make life a hell of lot easier, problem solved, but that runs up against the treaties and Germany's cult of the Bundesbank. Sarkozy was told 'game over'" (France and Germany: an unstoppable force meets an immovable object) Indeed, the mood at this weekend's summit in Brussels was somber. The impasse over the EFSF was overshadowed by a surprise announcement from Christine Lagarde, former French finance minister who is now chief of the International Monetary Fund (IMF). Lagarde warned that, without a default, the Greek debt crisis by itself could deplete the entire €440Bn EFSF fund. Her announcement further stated that the IMF was no longer willing to pick up a third of the total bill for rescuing Greece, estimated at €73Bn, unless European banks were prepared to write off at least 50% of Greek debt. One eurozone finance minister was quoted on Saturday as saying that the situation in Brussels was "Grim, the worst mood I have ever seen, a complete mess." (Eurozone summit - despair and backbiting in the corridors of power) Stock World Weekly writing and editing team, Elliott and Ilene, recently interviewed Russ Winter of Winter Watch at Wall Street Examiner. In part 1, Chaos in the Land of Oz, we established that the Fed is the Wizard, and we are living in an economic Land of Oz. This week, in part 2, we discussed the debt crisis in Europe, the too-big-to-fail (TBTF) banks, and whether there is a pathway back to Kansas. On Russ's position(s) in the stock market, Ilene asked: Are you long or short any particular stocks? Russ: Right now, I'm shorting the "Palace of Versailles" stocks, stocks like Tiffany's, Ambercrombie-Fitch, Coach, Starbucks, that sell at rich multiples, because supposedly wealthy people are doing well. Well, rich people were losing their asses in the market in the last couple of months. If you look at the polls, rich people are just as negative as poor people now. The Palace of Versailles trade makes little sense when protesters are in front of your houses, and the stores you shop at. I try to run counter to the conventional wisdom. (Click on this link to read the full interview, Chaos in the Land of Oz, part 2) Late Friday afternoon Phil took a "cashy and cautious" stance. He wrote, "Well that was a totally fun week. Congrats to all the bullish faithful and, of course, the $25KP players – CASH IS GOOD – enjoy the weekend!" In contrast to Russ and Phil's more cautious positioning, Lee Adler of the Wall Street Examiner is on the cusp of potentially turning more bullish, BUT he wants to see some proof first. He wrote to subscribers of the WSE's Professional Edition, "The market has broken a key resistance level. Unless this move whipsaws, the market could reach projections of 1280-1300 quickly. Such a breakout would in turn suggest that the 18 month 2 year cycle had entered an up phase. Unless bears mount a ferocious countermove on Monday, the likelihood is that they could be in hibernation at least through the winter months." We have a trade idea this week from Pharmboy, who writes, "Bristol Myers Squibb (BMY, $32.56) is losing its patent protection on Plavix next year, but has a blockbuster replacement in Xarelto. The company has other interesting pipeline candidates, and a hefty 4.1% dividend yield. I like starting a position by selling the January 2012 $31 puts for $1.10 or better."

(Click here for more Stock World Weekly)

|

| Posted: 23 Oct 2011 11:15 AM PDT Don't be fooled by GLD or SLV. Only GoldMoney offers real bullion allocated in your name.

|

| The Eurozone Wags the Gold and Silver Dog Posted: 23 Oct 2011 10:58 AM PDT Some market pundits would argue that gold and silver would likely benefit and I would not necessarily argue with that logic. However, the physical gold and silver markets are not that large and depending on the breadth of the situation ... Read More...

|

| Savers Protect Your Deposits From Bankrupting Banks and Quantitative Inflation Posted: 23 Oct 2011 10:27 AM PDT The Euro-zone continues to teeter over the edge of the financial abyss as bankrupting countries that cannot print Euro's threaten the collapse of its banking system that would would soon collapse the whole global banking system in a matter of hours as electronic bank runs sweep across the worlds financial system resulting in trillions of dollars worth of deposits being withdrawn in a matter of hours and thereby collapsing first the Euro-zone and then within 24 hours the UK, USA and Asia along with it. My recent article (Euro-Zone Prepares to Print Trillions in Advance of Greece Debt Default) covered the potential consequences for the world in the event of financial armageddon, this article continues on from the last article that covered the inflationary depression consequences of money printing that the likes of Britain and the United States are engaged in and that the Euro-zone WILL eventually replicate (Bank of England's Quantitative Inflation Bankster's Paradise Inflationary Depression Economy ).

|

| Nicolas Sarkozy Steals a Line From Max Keiser and Tells Cameron to STFU! Posted: 23 Oct 2011 09:29 AM PDT Nicolas Sarkozy has bluntly told Cameron to "shut up." He must be watching a certain television show hosted by none other than Max Keiser of the Silver Liberation Army! Sarkozy tells Cameron to shut up Don't be fooled by GLD … Continue reading

|

| Posted: 23 Oct 2011 09:21 AM PDT As indicated last week, the trends in gold, silver and the XAU are collectively still in a negative posture. Again, I would like to emphasize that any price improvements in the longer time frames always start first in the daily time frame. As an example, here is a daily chart of the XAU. A weekly chart of the XAU is at the bottom of this page. Monthly charts are located here. [CENTER] Trend and Cycle [FONT=Arial] [LIST] [*]Trend is demonstrated by the blue TDI (Trend Directional Indicator) and its red signal line. [/LIST] [LIST] [*]Cycle wave activity within that trend is revealed by the green Pendulum SRA cycle indicator. [/LIST] [/FONT][/CENTER] [LIST] [/LIST] [LIST] [/LIST] [CENTER]In Summary[/CENTER] Please see my general two month outlook for the gold, silver and XAU areas here. ...

|

| I Think This Is What They Call Fascism Posted: 23 Oct 2011 08:25 AM PDT I Think This Is What They Call Fascism Don't be fooled by GLD or SLV. Only GoldMoney offers real bullion allocated in your name.

|

| Reggie Middleton: Warning! This is going to be a highly, highly controversial post. Posted: 23 Oct 2011 08:02 AM PDT Bank of America Lynch[ing this] CountryWide's Equity Is Likely Worthess and It Will Rape FDIC Insured Accounts Going Bust Don't be fooled by GLD or SLV. Only GoldMoney offers real bullion allocated in your name.

|

| Chaos in the Land of Oz, Part 2 Posted: 23 Oct 2011 07:53 AM PDT Elliott and I interview Russ Winter of Winter Watch at Wall Street Examiner. ~ Ilene In part 1 of Chaos in the Land of Oz, we established that the Fed is the Wizard and we are living in an economic Land of Oz. In part 2 we discuss whether there is a pathway back to Kansas.

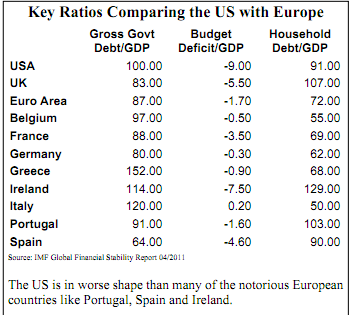

"My people have been wearing green glasses on their eyes for so long that most of them think this really is an Emerald City." L. Frank Baum, The Wonderful Wizard Of Oz Chaos in the Land of Oz, Part 2Elliott: In Part 1 of our interview, we agreed that by not allowing the too-big-to-fail (TBTF) banks to fail, the federal government is continuing its environment of corruption and moral hazard. Case in point - the scheme to force taxpayers to insure Bank of America's worthless debt via the FDIC. So, Russ, it will get worse, until TBTF banks get decapitalized? (Note: "Recapitalize" banks is code for pulling it out of the hide of German (and other) taxpayers and future generations. "Decapitalize" means: do the crime, do the time - take the losses.) Russ: Right. Take the investors out, the bondholders, and shrink the sector. Banking globally should be cut in half. That means the capital backing these institutions needs to go to money heaven. The word for it is "losses." Right now we have "too big to let lose" because of fear of a bad hair day. I was very disappointed last week when they started shilling for more bailouts. The bankers resist the restructuring, and the market rallies on that news. The market is hooked on bailouts and socializing losses. That was the basis of the 2009-2011 bull market. That can't go on forever. All these money managers are chasing stocks because they expect another bailout. It's nonsense! Elliott: As an investor, I like to look for value. But it's so hard to find real value when so much has been gimmicked by the Fed. Russ: That's my view entirely. Ilene: What do you expect the outcome will be? Russ: I'm highly cynical. We're like deer in the headlights, but we have to protect ourselves from the pump-and-dumps and avoid the herd mentality of jumping on these bailout rumors. I'd be ready to jump in [to the stock market] if the right outcome occurs - big haircuts for bond holders and decapitalizing the financial sector. Ilene: But then after Greece, there are other Eurozone countries. Are we going to go through all this again with Italy, and Spain?

Russ: Most likely. All of these countries may have some kind of debt restructuring. They can't pile the debt on the remaining few healthy countries. Look at the debt-to-GDP of Germany, for example. (Is Germany the Savior of Europe?) So who is the next patsy for the banksters? Answer: not many are left. Elliott: Every country on the list has a gross gov't debt-to-GDP of greater than 60%; most are running at close to 100% or more. Russ: Well, it's worse than that (and that's just the sovereigns). I wrote an article called "The EFSF plan in Europe is no free ride." The gross debt to GDP of the United States Government has reached 100%. The U.S. doesn't have any bullets left for this kind of policy. Politicians are talking about cutting Medicare and Medicaid and safety nets, so that they can bail out the banksters. Ilene: It looks like they're going to do exactly that, doesn't it? Russ: It kind of does. We have Presidente "Hopium", Wizard Ben, and a bunch of morons running the policy. All we need is a bankster showing up with the dynamite strapped on, and here we go again. These guys are not familiar with economic history and apparently don't understand that banks fail; banks have failed for centuries. Sometimes it triggers an economic crisis, but usually things clear up after a while. The market clears, and we get back to business as usual. Ilene: Do you think they may very well understand this, but it's not in their interests to act in favor of the country, but rather in favor of themselves? Elliott: I think the people in Congress are failing to understand a key tenant of Mises - "economics is human action." People doing stuff. That's economics. If a bank blows up, that entity called the bank goes away, but people live on. Russ: Right, and there's going to be losers. See, under Presidente Hopium, the philosophy is "you can't have losers." That's why he's such a bad president. Getting back to Europe, that whole Euro area has an 87% gross debt-to-GDP (in it's government sector). That's ironic; the whole euro area is better off than the United States. Yet the crisis is in Europe. We have Belgium with 97%. France, 88%. I don't think France has any more bullets for this. There's Germany at 80%. Greece at 152%. Ireland, 114%. Italy, 120%. Once it turns to Italy, France and Germany can't do anything about that. The ECB has had to intervene four days in a row to cap bonds rates at 6% in the Italian bond market.

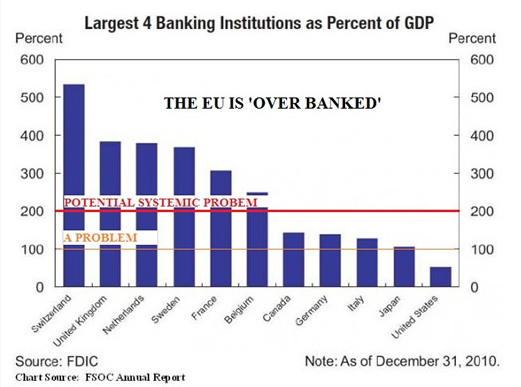

Europe is over-banked and over-leveraged, and more bailouts further socializes the losses to the already stressed sovereigns. If the banks aren't made to take the losses, governments will be throwing whole countries under the bus. Will it be the countries or the banks? Or a unhappy mix? The discussion constantly comes back to bailing out the banks. Ilene: Yes. Given the backdrop of wizardry and manipulation, how would you invest your money? Russ: I develop strategies to try to get in the ball game. I was shorting copper because I thought the China bubble would bust. And boy, it just resisted and resisted, even though the evidence for a hard-landing was substantial. Finally copper broke, and I covered. You need to be a speculator, a contrarian around the edges, and pick your openings. It's a tough environment. I would not want to be running other people's money right now. So I don't know that I have a good answer for you. Ilene: Are you long or short any particular stocks? Russ: Right now, I'm shorting the "Palace of Versailles" stocks, stocks like Tiffany's, Ambercrombie-Fitch, Coach, Starbucks, that sell at rich multiples, because supposedly wealthy people are doing well. Well, rich people were losing their asses in the market in the last couple of months. If you look at the polls, rich people are just as negative as poor people now. The Palace of Versailles trade makes little sense when protesters are in front of your houses and the stores you shop at. I try to run counter to the conventional wisdom. Elliott: I'm a fan of attempting to figure out the realistic fair value for a company, and then, when the stock goes way higher, sell; and if it goes way under, buy. Russ: That's not bad. There are some very cheap stocks in the market. Ilene: Are there any you'd buy now? Russ: I would wait until the market gets very oversold, when it looks like the direction in Greece is headed towards a serious, deep, restructured default. I'd wait for the sentiment to get more negative and certainly not when the trade is lathered up about the next Merkel-Sarkowky "meeting". I call it "weekendism". Then you could probably pick off your Sanofi's (SNY). There are many cheap European stocks, Total (TOT) perhaps, and Statoil (STO). I think oil, at an equilibrium price, will be around $75. I don't think it's going to completely collapse. At the same time, I would be shorting the Treasury market (specifically 2 and 5 year Treasuries). That's your hedge. Because if interest rates start spiking, especially U.S. Treasury rates, it's a game changer. It's going to re-value everything. I don't think we can have one-quarter percent interest rates indefinitely. Ilene: Isn't that what the Fed is doing right now, promising that very low interest rates will continue for the next few years? Russ: Right, but the first thing I said in this interview is that I consider the Fed to be like the "Wizard of Oz." It's power is overrated. I don't think that the man behind the curtain is who everybody thinks he is. How could the Fed possibly control a situation where gross government debt to GDP is 100% and climbing rapidly? How can they possibly keep interest rates down? History will show the current situation to be a fluke and a bubble. Ilene: Do you think the Fed might just keep "printing" more money and buying more Treasuries? Russ: That's stealing from real people and real consumers, the average guy in the street. It's just stealing. Even Dallas Fed Fischer said as much, just benefits speculators. Ilene: Yes, but they've been doing that, why would they stop finding new ways? Russ: Well, then we're going to keep having worse and worse economic conditions, more wealth transfers to criminals and kleptocrats and speculators. And 99% of the population will continue to sink, and you will soon see pitchforks. Ilene: Would allowing Bank of America to transfer derivatives from its Merrill Lynch unit to the retail bank subsidiary with insured deposits, count as another indication that the stealing goes on. It doesn't get much more blatant than that does it? Russ: Yes, it's absolutely outrageous, and to quote George Carlin, "nobody cares." Ilene: So Bernanke will continue this strategy of saving the banks, stealing from the taxpayers, until something forces him to stop. What might that be? Russ: It's not just Bernanke, it is a whole scheme of bankster officials and apparatchiks. He's probably going to stop when some major holder of Treasuries finally goes on strike. It's a prisoner's dilemma. You got all these entities like China trapped in the system. They've lent so much money to the United States that they're now trapped. Finally somebody at the margin will jump ship. That's how Ponzi schemes unravel. Someone eventually says, "Holy crap, let me out of here." I'm surprised the government's been able drag things out this long, except throwing trillions down the rat lines has some effect. It's probably because of the myth of the Wizard of Oz, that the Fed can control the economy, stock prices, and bond yields. People keep speculating on what the Fed will do, and sometimes it works and sometimes it doesn't. But the Fed's running out of string. When things get bad enough, other countries will help their own people over helping Bernanke. In Europe, Germany will use it's last resources for German banks, not Italian and French. Elliott: Bernanke is giving press conferences now, which is unprecedented. They've taken this entity that was remote and mysterious before, and they're putting it in the limelight. This does not strike me as a reassuring move, this strikes me as desperation. Russ: Well, the other thing is that these booms and bubbles go bust, and it pisses people off. I noticed that CNBC did a poll asking their viewers what they thought of the Fed, and 70% of viewers were negative. Elliott: Gee, I can't imagine why. Russ: The Fed (and Troika in Europe) is not very popular. But many traders are still caught up in this Wizard of Oz mentality. It seems like the hot money at the margin drives stock prices day to day. I have to admit, I thought it would end a while ago. Meanwhile, the government debt just keeps spiraling and spiraling, and many people are holding "Old Maid" cards. If there's a debt trap in the United States, would you want to be holding a bunch of 10-year Treasuries yielding 2%? Sometimes I wonder if the mom and pa investor, let alone their money managers know about prices inversing to yield. I grew up in the business in the 70's and 80's. I was a broker, and can remember quoting people: "Well, I could get you a 10-year treasury for 12%." And they'd say "no, no, I don't want that, what do you got in a one or two year?" And I'd say, "I could get you 16%." They'd take that. You could have done well locking in the 10-year at 12%. But now it's the opposite. It doesn't make sense. Any rational person looking at that would know it's a bad investment decision. The only reason someone would make that kind of investing decision is that they think the Fed has their back. And they thought the Fed had their back on the emerging market trade they had going nine months ago. They lost 30% on that. They thought the Fed had their back on commodities, now they're losing money on that, and they're going to lose money on this one. This is fun, you guys are letting me rant here. The Austrian school instinctively looks at trouble every time the government gets heavily involved in something. What the government needs to do is to be a policeman. It's a damn shame Eliot Spitzer got in trouble. Those are the kind of guys who are necessary today, people who will ride herd over these guys, sheriffs in the wild west so to speak. Elliott: If you're going to go after the big boys, you've got to be squeaky clean. You gotta be like a hermit, practically, a monk. Russ: Yeah, they'll get rid of you one way or another. I like to use the analogy of the old Soviet Union, the Soviet Union used what's called "negative selection." You go through any organization, and get rid of anybody that's a critical thinker, anybody that asks questions, anybody that has a moral compass, anybody that's highly intelligent, you get rid of them. Then you end up with these organizations that are littered with sycophants. That's what happened. Elliott: Right, a galloping mob of mediocrities, to do whatever their bosses say, without question. Russ: That's the system. Plus all the politicians are bought. That the crux of Occupy Wall Street. Elliott: The comfort that I take is the certain knowledge of "that which cannot continue, does not continue." Ilene: Why do you think it can't continue? Elliott: Because eventually when parasites get too much in control, they kill the host. Ilene: But they may survive and jump to some other host. Russ: Well, yeah, they'l |

| A New, Simple Way to Play the Dow to Gold Ratio Posted: 23 Oct 2011 07:22 AM PDT

Since I haven't noticed anyone else out there commenting on it, I thought I would offer my kudos and thanks to the folks over at Factor Shares for launching a new series of spread ETFs for traders. The product that has my attention and interest is a double leveraged spread of the Gold to S&P 500 ratio. This is a simple way to play the Gold versus paper theme that is near and dear to my blog. Though the Dow to Gold ratio is better known, an S&P 500 to Gold ratio is really no different. The new ETF I am referring to has ticker FSG and you need to do do your own due diligence if this is something that interests you. Please understand that I had never heard of the Factor Shares company before they released this product, I am not versed in the counterparty risk this product may carry, and I have no relationship with the company behind this new ETF. Like all leveraged ETFs, there is slippage that will plague this product and thus FSG is better used for trading rather than as a "buy and hold" vehicle. However, we are fast approaching a "buy" point for this ETF due to the oversold nature of the Gold to S&P 500 ratio right now. Here is a 5 year daily log scale chart of the Gold ($GOLD) to S&P 500 ($SPX) ratio (i.e. $GOLD:$SPX) through Friday's close with my thoughts:  The FSG ETF has been trading now for about 8 months and it looks like its volume is starting to pick up, which is a good thing:  Meanwhile, the bearish sentiment on precious metal stocks and precious metals is starting to get to a point where it is time to start thinking about going long. I think we may need one more plunge, but that should just about do it. If we get a "falling knife" in the Gold stock indices and precious metals over the next few weeks, I will be looking to catch it. Specific trading recommendations reserved for subscribers.  ![[Most Recent Charts from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_4.gif)

|

| A Simple (Humorous) Look At Bank Derivatives Posted: 23 Oct 2011 06:20 AM PDT A Banking Primer: Understanding 'Derivatives'Heidi is the proprietor of a bar in Detroit. She realizes that virtually all of her customers are unemployed alcoholics and, as such, can no longer afford to patronize her bar. To solve this problem, she comes up with a new marketing strategy that allows her customers to drink now and pay later; keeping track of the drinks consumed on a ledger (thereby granting the customers 'loans'). Word gets around about Heidi's "drink now, pay later" marketing plan and, as a result, increasing numbers of customers flood into her bar. Soon she has the largest sales volume for any bar in Detroit. By providing her customers freedom from immediate payment demands, Heidi gets no resistance when, at regular intervals, she substantially increases her prices for her products. Consequently, her gross sales volume massively increases. A young and dynamic vice-president at the local bank recognizes that these customer debts [accounts receivable assets] constitute valuable future assets and increases Heidi's borrowing limit. He sees no reason for any undue concern because he has the debts of the unemployed alcoholics as collateral. At the bank's corporate headquarters, expert traders figure a way to make huge commissions transforming these customer loans into DRINKBONDS [aka securities] bundling and trading them on international securities markets. Naive investors don't really understand that the securities being sold to them as "AAA Secured Bonds" really are debts of unemployed alcoholics. Nevertheless, the bond prices continuously climb – and the securities soon become the hottest-selling items for some of the nation's leading brokerage houses. One day, even though the bond prices still are climbing, a risk manager at the original local bank decides that the time has come to tell Heidi she must demand payment on the debts incurred by the drinkers at her bar. She demands payment from her alcoholic patrons; but, being unemployed alcoholics — they cannot pay back their drinking debts. Since Heidi cannot fulfill her loan obligations she is forced into bankruptcy. The bar closes and Heidi's 11 employees lose their jobs. Overnight, DRINKBOND prices drop by 90%. The collapsed bond asset value destroys the bank's liquidity and prevents it from issuing new loans, thus freezing credit and economic activity in the community. The suppliers of Heidi's bar had granted her generous payment extensions and had invested their firms' pension funds in the BOND securities. They find they are now faced with having to write off her bad debt and with losing over 90% of the presumed value of the bonds. Her wine supplier also claims bankruptcy, closing the doors on a family business that had endured for three generations, her beer supplier is taken over by a competitor, who immediately closes the local plant and lays off 150 workers. Fortunately though, the bank, the brokerage houses and their respective executives are saved and bailed out by a multi-billion dollar no-strings attached cash infusion from the United States federal government. The funds required for this bailout are obtained by new taxes levied on employed, middle-class, nondrinkers who have never been in Heidi's bar. There in a nutshell is what's going on in the banking industry called 'derivatives.' Source: club.ino.com

|

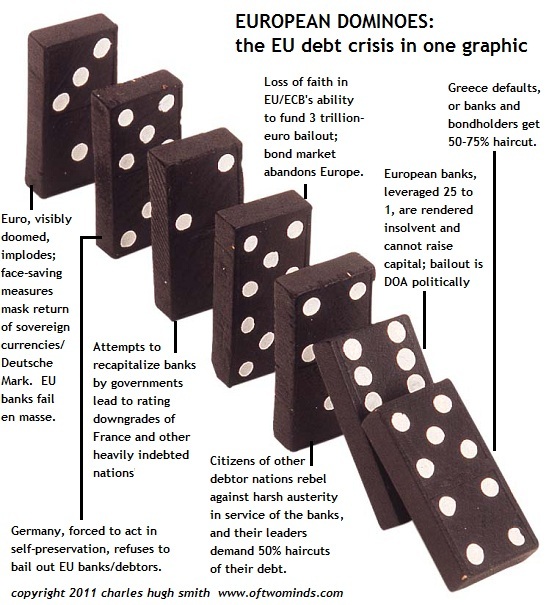

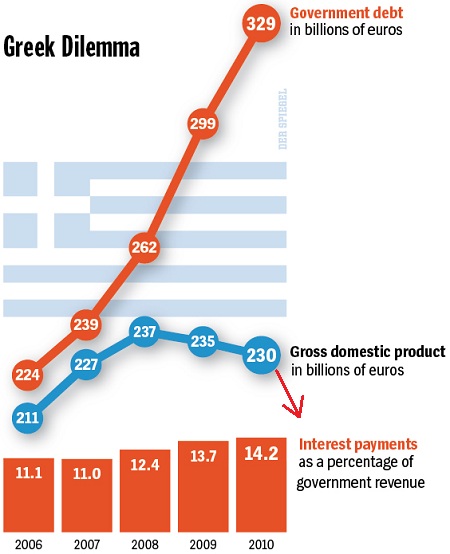

| Guest Post: The European Financial Crisis In One Graphic: The Dominoes Of Debt Posted: 23 Oct 2011 05:25 AM PDT Submitted by Charles Hugh Smith from Of Two Minds The European Financial Crisis in One Graphic: The Dominoes of Debt The dominoes of debt are toppling in Europe, and there is no way to stop the forces of financial gravity. After 19 months of denial, propaganda and phony fixes, the political and finance leaders of the European Union are claiming a "comprehensive solution" will be presented by Wednesday, October 26-- or maybe by the G20 meeting on November 3, or maybe on Christmas, when Santa Claus delivers the gift global markets are demanding: a "solution" that actually pencils out and that forces monumental writeoffs of debt and thus equally monumental losses on European banks and bondholders. There have been any number of insightful descriptions of what's going on beneath the artifice, spin and lies, for example: Four Facts that PROVE the EFSF (rescue fund) Doesn't Matter At All (Zero Hedge) Revised Troika Forecast Sees Total Greek Debt-To-GDP Peaking At 186%: Here Is What Happens Next (Zero Hedge) There Is No Bailout Spoon: The Math Behind The €2 Trillion EFSF Reveals A "Pea Shooter" Not A "Bazooka" (Zero Hedge) Citi Expects A 76% Haircut On Greek Debt (Zero Hedge) EU Bank Stress Test: When No. 1 Financial-Strength Ranking Spells Doom (Bloomberg) I have summarized the fundamentals in this one graphic: the European dominoes of debt. Simply put, there is no way the EU authorities can stop the first domino--Greek default or equivalent writedown of its impossible debt load--from toppling the over-leveraged banks which will be rendered insolvent when forced to recognize their losses.

That leaves each nation with the politically unsavory option of bailing out its premier banks with taxpayer money, and squeezing the money out of its citizenry via higher taxes and austerity. That assumption of bank debt will in turn trigger downgrades of heavily indebted sovereign nations such as France, moves that will raise rates and make the bailout even more costly to taxpayers, who will also be suffering from reductions of income due to global recession. Once the banks and bondholders accept a 50%-75% writedown in Greek debt, then the other debtor nations will be justified in demanding the same writedown in their crushing debts. This dynamic leads to estimates that 3 trillion euros will be needed to bail all the players out. Alternatively, total losses will equal 3 trillion euros, wiping out banks and bondholders of sovereign debt. The German economy is simply not big enough to fund a 3 trillion-euro bailout. Germany has 81 million people and its GDP is $3.3 trillion; the EU GDP is roughly $16 trillion. Compare those with the U.S., with 315 million people and a GDP of around $14.6 trillion. As an act of self-preservation, Germany will be forced to either exit the euro outright or cloak its withdrawal with a "euro 1 and euro 2" scheme, a scenario I first laid out in March 2010: Why the Euro Might Devolve into Euro1 and Euro2 (March 2, 2010). (Other recent entries on the end-state of the European debt crisis:) In any event, the last domino, the artifice of a single currency, will fall one way or another. It's important to understand that the supposedly "prudent" economies of France, Germany, South Korea and Canada are just as heavily indebted as the U.S. or "drowning in debt" nations such as Italy. In the long view, is Germany's load of 284% of GDP really that different from Italy's 313%? Yes, the mix of debt is different, but the point is that all of Europe, and indeed the developed world, is overloaded with debt: state, bank and private. The idea that leveraging more debt can resolve this gargantuan over-indebtedness is beyond absurd. (Source: BusinessWeek) It has recently come to light that in the worst-case scenario (i.e. reality), "solving" Greece's debt crisis would absorb the entire EFSF Rescue Fund's 400 billion euros. By all accounts, every estimate of Greek tax revenue is overstated, and every estimate of its expenses understated; Greek GDP is collapsing. In all probability, the reality is worse than anyone is willing to confess, which means this chart is already outdated and hopelessly rosy: #404040;">

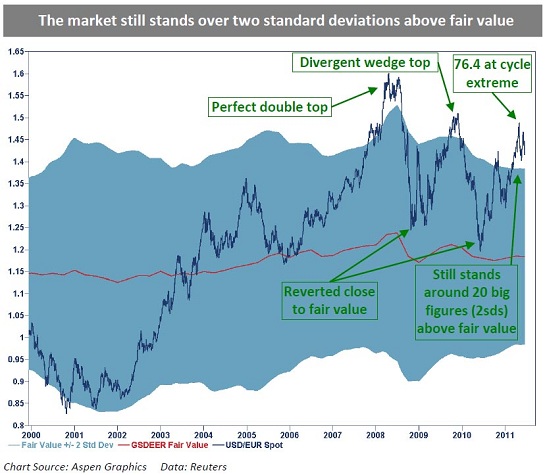

Way back in August, the euro was reckoned to be 20% above fair value of 1.15 to the U.S. dollar; once the dominoes start toppling in earnest, what will the euro's fair value be? Parity, or perhaps even lower? Why hold euros when the end-game is already visible? #404040;">

He/she who gets out first gets out best.

|

| Exclusive Interview With Diapason's Sean Corrigan Posted: 23 Oct 2011 05:17 AM PDT