Gold World News Flash |

- Can Gold Do Now What The Rentenmark Did For Germany In 1923?

- International Forecaster November 2010 (#4) - Gold, Silver, Economy + More

- First, Let's Lower the Bar

- Anticipating Volatility and the Rise of Emerging Markets

- Buy A Silver Coin - Destroy J.P. Morgan

- What revalations can we expect from Pierre Jovanovic's new book about Blythe Masters?

- James Grant: How to make the dollar sound again

- Volume on CME's Comex last Tuesday equal to 1 bn. Oz's, or 166% of annual world production

- “Gold has suffered from the same manipulation in the past, but the silver market is even more tightly controlled, at least, until this year…”

- Is the Rally Losing Steam?

- NEW! Crash JP Morgan buy silver

- MKC Replay! “500 Silver Eagle rounds . . . I will open it for the first time, right now”

- Jim?s Mailbox

- Jim's Mailbox

- The CATO Institute Finds That The Fed Must Be Abolished

- Gold: The Market’s Global Currency

- From Bill Murphy’s Newsletter

- Sinclair, Haynes, Norcini, Arensberg, and Davies interviewed at KWN

- I'M NOT BUYING IT

- Health-Care Realities, The Chinese Renminbi is Going Down, Not Up

- The Tale of André Prenner, a Parable for our Times (Part One of Two)

- Volume Signals Gold and U.S. Dollar Counter Trend Move

- Gold To Swing $100 To $300 In A Day

- Crude, Gold Suffer Biggest Losses in Weeks as G20, European Troubles Weigh

- MERS ATTACK!!! (Updated With Must Have Fraudclosure Flow Chart)

- Not So Shiny Today

- Price Volume Action Signals Counter Trend Move In U.S. Dollar and Gold

- Gold Daily Chart

- Using a Long-Term Calendar Spread to Trade Gold

| Can Gold Do Now What The Rentenmark Did For Germany In 1923? Posted: 14 Nov 2010 01:00 PM PST Just as the Rentenmark anchored currency in a post-hyperinflation nation, gold can bring such an anchor to global money. It will be unpopular until it is sorely needed because of one or more major nation's profligate behavior regarding their own currencies. This has already started as we can see in the G-20 nation meeting of this week. The cautionary note is that it worked because the nation was desperate having exhausted all other alternatives.

| ||||

| International Forecaster November 2010 (#4) - Gold, Silver, Economy + More Posted: 14 Nov 2010 05:00 AM PST Mr. Bernanke is trying to avoid the Japanese experience of the past 20 years. Underlying deflation is being offset again, as it has been for the past eight years, by creating more money and credit. The only one lose to our prediction of mid-May of $5 trillion over two years is Keynesian economist Paul Krugman. He said the Fed would need $6 trillion. The Republicans seized the House and all that has really been accomplished is gridlock, the end of stimulus and a cut of perhaps $100 billion in debt.

| ||||

| Posted: 14 Nov 2010 03:00 AM PST China's currency is rising ever so slowly against the dollar. But is that hurting China? We will look at a very interesting chart and some research. And then we'll gain some more insight into why the employment numbers seemed to surprise. I guess if you lower the bar, it's easier to jump over. I also deal with the pushback from last week's Outside the Box! And Ireland is on my radar. There is a lot to cover, so let's jump in.

| ||||

| Anticipating Volatility and the Rise of Emerging Markets Posted: 13 Nov 2010 03:11 PM PST By Frank Holmes CEO and Chief Investment Officer U.S. Global Investors Life is about managing expectations and we believe understanding market cycles helps investors navigate through the volatility of their investments. We often remind investors to "Anticipate Before You Participate" and I strongly urge you to read through our special presentation on managing volatility. Read the presentation here. This table shows the monthly volatility based on 10 years of data for a number of different investments. You can easily see each asset class has its own unique DNA of volatility. Standard Deviation Based on 10 Years of Data Rolling 1 MonthAs of 11/12/2010 Source: U.S. Global ResearchNYSE Arca Gold BUGS Index (HUI)11.1%MSCI Emerging Markets (MXEF)7.2%S&P 500 Index (SPX)5.1%Gold Bullion4.9%U.S. Dollar (DXY)2.5% For gold stocks, it's a normal event to see a positive or negative move of 11 percent over just one month's time. For emerging markets, it's just over 7 percent. Und...

| ||||

| Buy A Silver Coin - Destroy J.P. Morgan Posted: 13 Nov 2010 02:57 PM PST "A bad day for the precious metals, but the HUI takes it in stride. Ireland's financial woes go supernova. No inflation? Tell it to your Thanksgiving turkey. Richard Russell: Speculative Phase of Gold Bull Lies Ahead... and much more. " Yesterday in Gold and Silver Well, the big sell-off that started in Asia on Friday morning found an intermediate bottom shortly after London opened for trading yesterday morning. Then shortly before the London p.m. gold fix rolled around at 10:00 a.m. Eastern time, gold had recovered about eight bucks from the London opening low. But that was it for the day, as the selling began anew... and by 12:35 p.m. Eastern time, another $35 had been shaved off the gold price. This was its low of the day [$1,359.00 spot]... and the price recovered a few dollars doing into the close, but still finished the day down $40.10... 2.85%. Silver, which is the center of the universe for JPMorgan et al, really got it in the neck. The pri...

| ||||

| What revalations can we expect from Pierre Jovanovic's new book about Blythe Masters? Posted: 13 Nov 2010 02:00 PM PST from: Pierre Jovanovic Max Ready to have an interview of you for my new book (january 2011) i am working on the last chapter blythe masters and silver Blythe Sally Jess Masters is an economist and current head of global commodities at J.P. Morgan Chase, and led the development of so-called Credit Default Swaps (CDSs).

| ||||

| James Grant: How to make the dollar sound again Posted: 13 Nov 2010 01:10 PM PST By James Grant http://www.nytimes.com/2010/11/14/opinion/14grant.html By disclosing a plan to conjure $600 billion to support the sagging economy, the Federal Reserve affirmed the interesting fact that dollars can be conjured. In the digital age, you don't even need a printing press. This was on Nov. 3. A general uproar ensued, with the dollar exchange rate weakening and the price of gold surging. And when, last Monday, the president of the World Bank suggested, almost diffidently, that there might be a place for gold in today's international monetary arrangements, you could hear a pin drop. Let the economists gasp: The classical gold standard, the one that was in place from 1880 to 1914, is what the world needs now. In its utility, economy and elegance, there has never been a monetary system like it. It was simplicity itself. National currencies were backed by gold. If you didn't like the currency you could exchange it for shiny coins (money was "sound" if it rang when dropped on a counter). Borders were open and money was footloose. It went where it was treated well. In gold-standard countries, government budgets were mainly balanced. Central banks had the single public function of exchanging gold for paper or paper for gold. The public decided which it wanted. ... Dispatch continues below ... ADVERTISEMENT Sona Drills 85.4g Gold/Ton Over 4 Metres at Elizabeth Gold Deposit, Company Press Release, October 27, 2010 VANCOUVER, British Columbia -- Sona Resources Corp. reports on five drillling holes in the third round of assay results from the recently completed drill program at its 100 percent-owned Elizabeth Gold Deposit Property in the Lillooet Mining District of southern British Columbia. Highlights from the diamond drilling include: -- Hole E10-66 intersected 17.4g gold/ton over 1.54 metres. -- Hole E10-67 intersected 96.4g gold/ton over 2.5 metres, including one assay interval of 383g of gold/ton over 0.5 metres. -- Hole E10-69 intersected 85.4g gold/ton over 4.03 metres, including one assay interval of 230g gold/ton over 1 metre. Four drill holes, E10-66 to E10-69, targeted the southwestern end of the Southwest Vein, and three of the holes have expanded the mineralized zone in that direction. The Southwest Vein gold mineralization has now been intersected over a strike length of 325 metres, with the deepest hole drilled less than 200 metres from surface. "The assay results from the Southwest Zone quartz vein continue to be extremely positive," says John P. Thompson, Sona's president and CEO. "We are expanding the Southwest Vein, and this high-grade gold mineralization remains wide open down dip and along strike to the southwest." For the company's full press release, please visit: http://sonaresources.com/_resources/news/SONA_NR19_2010.pdf "You can't go back," today's central bankers are wont to protest, before adding, "And you shouldn't, anyway." They seem to forget that we are forever going back (and forth, too), because nothing about money is really new. "Quantitative easing," a.k.a. money-printing, is as old as the hills. Draftsmen of the United States Constitution, well recalling the overproduction of the Continental paper dollar, defined money as "coin." "To coin money" and "regulate the value thereof" was a congressional power they joined in the same constitutional phrase with that of fixing "the standard of weights and measures." For most of the next 200 years the dollar was, in fact, defined as a weight of metal. The pure paper era did not begin until 1971. The Federal Reserve was created in 1913 -- by coincidence, the final full year of the original gold standard. (Less functional variants followed in the 1920s and '40s; no longer could just anybody demand gold for paper, or paper for gold.) At the outset, the Fed was a gold standard central bank. It could not have conjured money even if it had wanted to, as the value of the dollar was fixed under law as one 20.67th of an ounce of gold. Neither was the Fed concerned with managing the national economy. Fast forward 65 years or so, to the late 1970s, and the Fed would have been unrecognizable to the men who voted it into existence. It was now held responsible for ensuring full employment and stable prices alike. Today the Fed's hundreds of Ph.D.s conduct research at the frontiers of economic science. "The Two-Period Rational Inattention Model: Accelerations and Analyses" is the title of one of the treatises the monetary scholars have recently produced. "Continuous Time Extraction of a Nonstationary Signal with Illustrations in Continuous Low-pass and Band-pass Filtering" is another. You can't blame the learned authors for preferring the lives they lead to the careers they would have under a true-blue gold standard. Rather than writing monographs for each other, they would be standing behind a counter exchanging paper for gold and vice versa. If only they gave it some thought, though, the economists -- nothing if not smart -- would fairly jump at the chance for counter duty. For a convertible currency is a sophisticated, self-contained information system. By choosing to hold it, or instead the gold that stands behind it, the people tell the central bank if it has issued too much money or too little. It's democracy in money, rather than mandarin rule. Today, it's the mandarins at the Federal Reserve who decide what interest rate to impose, and what volume of currency to conjure. The Bank of England once had an unhappy experience with this method of operation. To fight the Napoleonic wars of the early 19th century, Britain traded in its gold pound for a scrip, and the bank had to decide unilaterally how many pounds to print. Lacking the information encased in the gold standard, it printed too many. A great inflation bubbled. Later a parliamentary inquest determined that no institution should again be entrusted with such powers as the suspension of gold convertibility had dumped in the lap of those bank directors. They had meant well enough, the parliamentarians concluded, but even the most minute knowledge of the British economy, "combined with the profound science in all the principles of money and circulation," would not enable anyone to circulate the exact amount of money needed for "the wants of trade." The same is true now at the Fed. The chairman, Ben Bernanke, and his minions have taken it upon themselves to decide that a lot more money should circulate. According to the Consumer Price Index, which is showing year-over-year gains of less than 1.5 percent, prices are essentially stable. In the inflationary 1970s people had prayed for exactly this. But the Fed today finds it unacceptable. We need more inflation, it insists (seeming not to remember that prices showed year-over-year declines for 12 consecutive months in 1954 and '55 or that, in the first half of the 1960s, the Consumer Price Index never registered year-over-year gains of as much as 2 percent). This is why Mr. Bernanke has set out to materialize an additional $600 billion in the next eight months. The intended consequences of this intervention include lower interest rates, higher stock prices, a perkier Consumer Price Index and more hiring. The unintended consequences remain to be seen. A partial list of unwanted possibilities includes an overvalued stock market (followed by a crash), a collapsing dollar, an unscripted surge in consumer prices (followed by higher interest rates), a populist revolt against zero-percent savings rates and wall-to-wall European tourists on the sidewalks of Manhattan. As for interest rates, they are already low enough to coax another cycle of imprudent lending and borrowing. It gives one pause that the Fed, with all its massed brain power, failed to anticipate even a little of the troubles of 2007-09. At last week's world economic summit meeting in South Korea, finance ministers and central bankers chewed over the perennial problem of "imbalances." America consumes much more than it produces (and has done so over 25 consecutive years). Asia produces more than it consumes. Merchandise moves east across the Pacific; dollars fly west in payment. For Americans, the system could hardly be improved on, because the dollars do not remain in Asia. They rather obligingly fly eastward again in the shape of investments in United States government securities. It's as if the money never left the 50 states. So it is under the paper-dollar system that we Americans enjoy "deficits without tears," in the words of the French economist Jacques Rueff. We could not have done so under the classical gold standard. Deficits then were ultimately settled in gold. We could not have printed it, but would have had to dig for it, or adjusted our economy to make ourselves more internationally competitive. Adjustments under the gold standard took place continuously and smoothly -- not, like today, wrenchingly and at great intervals. Gold is a metal made for monetary service. It is scarce (just 0.004 parts per million in the earth's crust), pliable and easy on the eye. It has tended to hold its purchasing power over the years and centuries. You don't consume it, as you do tin or copper. Somewhere, probably, in some coin or ingot, is the gold that adorned Cleopatra. And because it is indestructible, no one year's new production is of any great consequence in comparison with the store of above-ground metal. From 1900 to 2009, at much lower nominal gold prices than those prevailing today, the worldwide stock of gold grew at 1.5 percent a year, according to the United States Geological Survey and the World Gold Council. The first time the United States abandoned the gold standard -- to fight the Civil War -- it took until 1879, 14 years after Appomattox, to again link the dollar to gold. To reinstitute a modern gold standard today would take time, too. The United States would first have to call an international monetary conference. A chastened Ben Bernanke would have to announce that, in fact, he cannot see into the future and needs the information that the convertibility feature of a gold dollar would impart. That humbling chore completed, the delegates could get down to the technical work of proposing a rate of exchange between gold and the dollar (probably it would be even higher than the current price of gold, the better to encourage new exploration and production). Other countries, thunderstruck, would then have to follow suit. The main thing, Mr. Bernanke would emphasize, would be to create a monetary system that synchronizes national economies rather than driving them apart. If the classical gold standard in its every Edwardian feature could not, after all, be teleported into the 21st century, there would be plenty of scope for adaptation and, perhaps, improvement. Let the author of "The Two-Period Rational Inattention Model: Accelerations and Analyses" have a crack at it. ----- James Grant, editor of Grant's Interest Rate Observer, is the author of "Money of the Mind." Support GATA by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Or a video disc of GATA's 2005 Gold Rush 21 conference in the Yukon: * * * Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: ADVERTISEMENT Prophecy Receives Permit To Mine at Ulaan Ovoo in Mongolia VANCOUVER, British Columbia -- Prophecy Resource Corp. (TSX-V:PCY, OTCQX: PRPCF, Frankfurt: 1P2) announces that on November 9, 2010, it received the final permit to commence mining operations at its Ulaan Ovoo coal project in Mongolia. Prophecy is one of few international mining companies to achieve such a milestone. The mine is production-ready, with a mine opening ceremony scheduled for November 20. Prophecy CEO John Lee said: "I thank the government of Mongolia for the expeditious way this permit was issued. The opening of Ulaan Ovoo is a testament to the industrious and skilled workforce in Mongolia. Prophecy directly and indirectly (through Leighton Asia) employs more than 65 competent Mongolian nationals and four expatriots. The company also reaffirms its commitment to deliver coal to the local Edernet and Darkhan powerplants in Mongolia." The Ulaan Ovoo open pit mine is 10 kilometers from the Russian border and within 120km of the Nauski TransSiberian railway station, enabling transportation of coal to Russia and its eastern seaports. Thermal coal prices are trading at two-year highs at Russian seaports due to strong demand from Asian economies. For the complete press release, please visit: http://prophecyresource.com/news_2010_nov11.php

| ||||

| Volume on CME's Comex last Tuesday equal to 1 bn. Oz's, or 166% of annual world production Posted: 13 Nov 2010 12:19 PM PST 5 ALARM FIRE AT COMEX: SILVER WILL SOAR ONCE AGAIN

| ||||

| Posted: 13 Nov 2010 12:00 PM PST Still The Investment Of A Lifetime

| ||||

| Posted: 13 Nov 2010 10:48 AM PST

Ben Levihsohn and Jane J. Kim of the WSJ wrote an interesting weekend piece, How to Play a Market Rally:

Bonds are a hell of a lot more risky right now, but as Randall Forsyth of Barron's notes, Bonds Are Not Dead Yet:

I'm not so sure about the municipal bond market where systemic credit risk is very high, causing a great deal of anxiety among bond investors. But at the end of the day, the Fed will do whatever it takes -- even buy municipal bonds -- to head off any systemic crisis. As far as the stock market, I just see this as another opportunity to load up on shares. My personal favorites remain Chinese solar stocks which sold off strongly after most reported stellar earnings. One of my top picks in this group is LDK Solar, which smashed its estimates and then sold off (warning: these stocks are not for the faint of heart). Tim Hayes, chief investment strategist at Ned Davis Research, spoke with Carol Massar and Matt Miller on Bloomberg Television's "Street Smart" saying he expects a 3-5% correction in stocks in the next few weeks (click here to watch the interview). Hayes is one of the best strategists in the business, and a great guy too, and I think he's probably right. It's only normal for portfolio managers to lock in profits going into year-end, but I warn you, if you think this the beginning of some sort of systemic collapse, you're in for a big surprise. This market is heading higher -- much, much higher. And all of you trying to time these markets will get your heads handed to you. Buy and hold maybe dead for the overall market, but it certainly isn't dead for some sectors and stocks. If you pick your spots well, you'll make decent profits as this rally still has steam. The only thing is you need to accept a lot more volatility. There is is nothing you can do about that.

| ||||

| NEW! Crash JP Morgan buy silver Posted: 13 Nov 2010 09:33 AM PST

| ||||

| MKC Replay! “500 Silver Eagle rounds . . . I will open it for the first time, right now” Posted: 13 Nov 2010 09:00 AM PST I've posted this video before, it's a favorite. It's an intoxicating cocktail of an Eastern European accent, 1970′s Bee Gees music, a boxcutter, a whole shitload of silver – caressed with immaculate white gloves. For paper bugs, cover your eyes, this is PURE Ag PORN.

| ||||

| Posted: 13 Nov 2010 08:40 AM PST View the original post at jsmineset.com... November 13, 2010 11:32 AM Physical Silver Demand Straining Paper Proxies CIGA Eric Physical silver demand continues to strain paper proxies. The London pm fixed (physical) to paper proxy ETF (paper) ratio, illustrated below, has already pushed beyond the June 2006 and March 2008 premium extremes. November’s 'mini scramble' for physical silver is only exceeded by those of August and October 2008. The recent adjustment to margin requirements and paper hit to price intended to cool off the market. The rising premium spread since 2010 suggests that the cool down won't last long. The next surge will be more difficult to stop. Physical to Paper Proxy Spread: More…...

| ||||

| Posted: 13 Nov 2010 06:32 AM PST Physical Silver Demand Straining Paper Proxies Physical silver demand continues to strain paper proxies. The London pm fixed (physical) to paper proxy ETF (paper) ratio, illustrated below, has already pushed beyond the June 2006 and March 2008 premium extremes. November's 'mini scramble' for physical silver is only exceeded by those of August and October 2008. The recent adjustment to margin requirements and paper hit to price intended to cool off the market. The rising premium spread since 2010 suggests that the cool down won't last long. The next surge will be more difficult to stop. Physical to Paper Proxy Spread:

| ||||

| The CATO Institute Finds That The Fed Must Be Abolished Posted: 13 Nov 2010 05:19 AM PST

A must read paper from George Selgin and the Cato Institute, which confirms what Zero Hedge has been saying since inception: the Fed must be abolished immediately: "The Federal Reserve System has not lived up to its original promise. Early in its career, it presided over both the most severe inflation and the most severe (demand-induced) deflations in post-Civil War U.S. history. Since then, it has tended to err on the side of inflation, allowing the purchasing power of the U.S. dollar to deteriorate considerably. That deterioration has not been compensated for, to any substantial degree, by enhanced stability of real output... A genuine improvement did occur during the sub-period known as the "Great Moderation." But that improvement, besides having been temporary, appears to have been due mainly to factors other than improved monetary policy. Finally, the Fed cannot be credited with having reduced the frequency of banking panics or with having wielded its last-resort lending powers responsibly. Its record strongly suggests that the Federal Reserve‘s problems go well beyond those of having lacked good administrators. Although it has manifested itself in different ways during different decades, the Fed‘s failure has been chronic. The problems appear to reside with the institution, and not with particular personalities who have been placed in charge of it. Hence the record would not be likely to improve substantially even with complete turnover in the Board of Governors. The only real hope for a better monetary system lies in regime change."

Ending the Fed is the only hope America now has. The outcome will be painful, but it will be surmountable. The alternative is the unquestionable end of America's status as a superpower. Has the Fed Been a Failure? (pdf)

This posting includes an audio/video/photo media file: Download Now | ||||

| Gold: The Market’s Global Currency Posted: 13 Nov 2010 04:00 AM PST World Bank president Robert Zoellick has stirred up a hornet's nest with his recent call for a return to a gold anchor in the global financial system. The usual suspects immediately denounced him, with Keynesian Brad DeLong anointing Zoellick the "Stupidest Man Alive." In the present article I'll explain the resurging interest in the yellow metal. I'll also explain the dangers of Zoellick's proposal, and why fans of the classical gold standard should be wary. The Limitations of the Printing Press In order to make sense of our current situation – and why Zoellick would timidly call for a return to a pseudo-gold standard – we need to first think through the logic of fiat money. Fiat money is not "backed up" by anything; it is intrinsically useless paper (or nowadays, mere electronic bookkeeping entries) that is valuable only because of its anticipated purchasing power. In contrast, a market-based commodity money, such as gold or silver, is a useful good in its own right, serving industrial and consumer purposes. The critical difference between fiat and commodity money is that fiat money can be produced in virtually unlimited quantities at very low cost. In this respect, the person who controls the printing press of a fiat currency is in a much stronger position than the person who owns a gold mine. With just some ink and paper, the printing press can create a million new dollars quite easily, whereas the owner of the gold mine would need to hire workers to operate expensive equipment in order to bring forth new amounts of gold having the same market value. Yet we shouldn't conclude that the owner of a printing press has unlimited power. For one thing, prices would eventually rise in response to large amounts of new money creation. So printing off, say, $1 million in fresh new currency would buy fewer and fewer goods and services with each successive round of inflation. Even more problematic, the people in the community would abandon the currency if the inflation became too excessive. For example, if a brilliant counterfeiter developed a machine to produce perfect $100 bills in his basement, he wouldn't be able to literally buy the whole world. Long before that point – even if the authorities didn't track him down – people would have ditched the dollar and switched to the use of other currencies. Although our scenario sounds farfetched, it's actually very close to the real world, right now. The only difference is that instead of our hypothetical, brilliant counterfeiter in the basement, we have our actual, less-than-brilliant economist in the Federal Reserve. His name, of course, is Ben Bernanke. The Bretton Woods System The original Bretton Woods system – so named because of the location of the meetings that established it in 1944 – governed international monetary arrangements in the postwar era until Richard Nixon's fateful decision to close the gold window in 1971. Under the Bretton Woods agreement, other nations would use US dollars as their "reserves." The Bank of England, Bank of France, etc., would issue their own domestic currencies, but would maintain stockpiles of US dollars with which they could regulate the value of their own currencies. If the British pound sterling began to depreciate against the US dollar, for example, then the Bank of England could enter the foreign-exchange market and use some of its dollar holdings to "buy pounds," thus bringing the value of the pound back within target. In this way, investors across the globe could feel comfortable with their British financial holdings, because the pound was tied to the dollar. Note the tremendously advantageous position that the Bretton Woods system assigned to the United States. As issuer of the world's reserve currency, the United States had a very captive market. If the Bank of England wanted to increase its dollar reserves by another $1 million, then ultimately Great Britain had to sell $1 million worth of goods and services to Americans in order to earn the dollars. The Bretton Woods system effectively expanded the scope for US inflation to the entire world, thus magnifying the benefits to those who controlled the American printing press. Of course, the other members of Bretton Woods understood these details. The US achieved its privileged outcome in the negotiations because of its economic and military might at that point in world history. But in order to restrain the natural temptation for runaway inflation by US officials, the Bretton Woods system linked the dollar itself to gold. Specifically, any central bank could redeem its dollars for gold at the fixed rate of $35 per ounce. The Bretton Woods system has been described as a "gold-exchange standard," in contrast to the classical gold standard. In the original framework – which was smashed, like so many other aspects of Western civilization, in World War I – each nation tied its own currency to gold. Then, the currencies in turn traded at fixed exchange rates against each other, because of their mutual ties to gold. Individual citizens could present the currencies for redemption in gold, keeping a very tight check on inflation. If any central bank began to issue too much currency in relation to its gold reserves, speculators would begin depleting the reserves, causing the central bank to quickly reverse course. Under the diluted Bretton Woods system, individual citizens had no right of redemption. Most currencies were only indirectly linked to gold (via their link to the dollar). And, of course, even this tenuous link was destroyed when Richard Nixon abandoned the dollar's convertibility to gold in 1971. At this point, the entire global financial system was based utterly on fiat money. No longer shackled by the peg to gold, the Federal Reserve began printing money with reckless abandon. The obvious results were an acceleration in US consumer prices, and an explosion in the US trade deficit, trends that noticeably worsen after 1971:

Consumer Price Index (Blue Line, Right Scale) and Balance of Payments as a Share of GDP (Red Line, Left Scale) The Reluctant Return to Gold Say what you will about the powerful people running the global monetary system, but they aren't stupid. They can see as well as the rest of us that there is no "exit strategy" for Bernanke's bouts of massive inflation, or "quantitative easing" as they now call it. At some point, the trillion(s) in excess reserves will begin leaking back into the broader monetary aggregates. At that point, Bernanke or a successor will need to choose between saving the dollar or saving major Wall Street institutions. I predict that he will sacrifice the dollar, and it seems many elites around the world have come to the same conclusion. It is in this context that World Bank president Zoellick writes: The G20 should complement [a] growth recovery programme with a plan to build a co-operative monetary system that reflects emerging economic conditions. This new system is likely to need to involve the dollar, the euro, the yen, the pound and a renminbi that moves towards internationalisation and then an open capital account. The system should also consider employing gold as an international reference point of market expectations about inflation, deflation and future currency values. Although textbooks may view gold as the old money, markets are using gold as an alternative monetary asset today. (emphasis added) To repeat, gold is the bane of central bankers; it ties their hands and limits their discretion when conducting monetary policy. However, the game collapses if people lose faith in the fiat currency underpinning the whole system. As the recklessness of Bernanke's moves becomes apparent to more and more people, the central planners around the world will need to throw a bone to the fearful public. A "basket of currencies," each of which is still fiat-paper money, will not suffice. As Zoellick is a member of the Council on Foreign Relations, and a participant in the notorious Bilderberg meetings, some analysts are understandably suspicious of his motives. After all, if powerful people were trying to introduce a regional currency to replace the dollar – in the same way that the euro has supplanted the traditional European currencies – then it would be necessary to first wreck the dollar. In its place, it would be very tempting to offer a new currency with a tie to gold. In this light, what appear to be "inexplicable" and contradictory actions by the Federal Reserve and other powerful figures would make perfect sense. Conclusion Regardless of the machinations of the political insiders, the laws of economics cannot be denied. Central bankers cannot be trusted with the printing press, especially when there is no formal check on their inflationary policies. It is no coincidence that gold is hitting such heights as investors the world over hunker down for what may very well be a collapse of the dollar system. Robert Murphy Gold: The Market's Global Currency originally appeared in the Daily Reckoning. The Daily Reckoning, offers a uniquely refreshing, perspective on the global economy, investing, gold, stocks and today's markets. Its been called "the most entertaining read of the day."

| ||||

| Posted: 13 Nov 2010 03:22 AM PST The following is automatically syndicated from Grandich's blog. You can view the original post here. Stay up to date on his model portfolio! November 13, 2010 08:21 AM I wrote to Bill after reading the total garbage Tokyo Rose is peddling again. This is what I said and Bill’s comment about it: [B][B]GATA's good friend Peter Grandich on The Nitwit, the one he calls Tokyo Rose…[/B][/B] [B][B]a gold believer … 60 to 80% of prices what a total piece of crap this fraud is and you can quote me bill in your newsletter if you show his quote and mind…[/B][/B] [B][B] [/B][/B] [B][B]Jon Nadler, senior analyst at Kitco.com, a gold believer but with a more conservative outlook, believes that without a real crisis gold prices are due for a deeper correction. “The going has gotten fairly tough around $1,425 or so … these were largely sentiment and momentum-based gains … [/B][/B] [B][B]Nadler believes that gold’s “parabolic rise” will only ...

| ||||

| Sinclair, Haynes, Norcini, Arensberg, and Davies interviewed at KWN Posted: 13 Nov 2010 03:19 AM PST 11:21a ET Saturday, November 13, 2010 Dear Friend of GATA and Gold (and Silver): Start your weekend at King World News, where Jim Sinclair says that the increasing volatility of the precious metals markets is characteristic of markets "about to go ballistic": http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2010/11/12_J... Or try this abbreviated link: Meanwhile, Eric King's weekly precious metals audio interview with Bill Haynes of CMI Gold & Silver, Dan Norcini of JSMineSet.com, and Gene Arensberg of the Got Gold Report can be found here: http://www.kingworldnews.com/kingworldnews/Broadcast/Entries/2010/11/13_... And King interviews Hinde Capital's Ben Davies about the prospects for gold and silver here: http://www.kingworldnews.com/kingworldnews/Broadcast/Entries/2010/11/13_... CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT Prophecy Receives Permit To Mine at Ulaan Ovoo in Mongolia VANCOUVER, British Columbia -- Prophecy Resource Corp. (TSX-V:PCY, OTCQX: PRPCF, Frankfurt: 1P2) announces that on November 9, 2010, it received the final permit to commence mining operations at its Ulaan Ovoo coal project in Mongolia. Prophecy is one of few international mining companies to achieve such a milestone. The mine is production-ready, with a mine opening ceremony scheduled for November 20. Prophecy CEO John Lee said: "I thank the government of Mongolia for the expeditious way this permit was issued. The opening of Ulaan Ovoo is a testament to the industrious and skilled workforce in Mongolia. Prophecy directly and indirectly (through Leighton Asia) employs more than 65 competent Mongolian nationals and four expatriots. The company also reaffirms its commitment to deliver coal to the local Edernet and Darkhan power plants in Mongolia." The Ulaan Ovoo open pit mine is 10 kilometers from the Russian border and within 120km of the Nauski TransSiberian railway station, enabling transportation of coal to Russia and its eastern seaports. Thermal coal prices are trading at two-year highs at Russian seaports due to strong demand from Asian economies. For the complete press release, please visit: http://prophecyresource.com/news_2010_nov11.php Support GATA by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Or a video disc of GATA's 2005 Gold Rush 21 conference in the Yukon: * * * Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: ADVERTISEMENT Sona Drills 85.4g Gold/Ton Over 4 Metres at Elizabeth Gold Deposit, Company Press Release, October 27, 2010 VANCOUVER, British Columbia -- Sona Resources Corp. reports on five drillling holes in the third round of assay results from the recently completed drill program at its 100 percent-owned Elizabeth Gold Deposit Property in the Lillooet Mining District of southern British Columbia. Highlights from the diamond drilling include: -- Hole E10-66 intersected 17.4g gold/ton over 1.54 metres. -- Hole E10-67 intersected 96.4g gold/ton over 2.5 metres, including one assay interval of 383g of gold/ton over 0.5 metres. -- Hole E10-69 intersected 85.4g gold/ton over 4.03 metres, including one assay interval of 230g gold/ton over 1 metre. Four drill holes, E10-66 to E10-69, targeted the southwestern end of the Southwest Vein, and three of the holes have expanded the mineralized zone in that direction. The Southwest Vein gold mineralization has now been intersected over a strike length of 325 metres, with the deepest hole drilled less than 200 metres from surface. "The assay results from the Southwest Zone quartz vein continue to be extremely positive," says John P. Thompson, Sona's president and CEO. "We are expanding the Southwest Vein, and this high-grade gold mineralization remains wide open down dip and along strike to the southwest." For the company's full press release, please visit: http://sonaresources.com/_resources/news/SONA_NR19_2010.pdf

| ||||

| Posted: 13 Nov 2010 02:43 AM PST The general consensus now appears to be that all asset classes have put in an intermediate top and that the dollar has made an intermediate bottom. I jumped to that conclusion myself the other day. After further consideration I'm not buying it any more for several reasons. First, the cyclical structure of the stock market is not set up for an intermediate top unless we are on the verge of another 2 month horror show like we saw this summer. I don't think for a second that with another 900 billion scheduled to be thrown at the market, of which 110 billion will come in the first month, that we are going to see the market roll over into an extended correction during the traditionally bullish Christmas season. The intermediate gold and dollar cycles also aren't set up for an intermediate top. Ever since March of `09 the Fed's QE programs have stretched cycles, not caused them to contract. Here are the last 5 intermediate gold cycles.  Every single one of them has run long except one and that one was followed by a very stretched 30 week cycle. If the current cycle follows the pattern of the last two years then it's too early to expect an intermediate top, and the current correction is nothing more than the normal move down into a daily cycle low. Once that bottom is in place (possibly sometime next week) it should be followed by one more daily cycle higher before putting in the larger degree intermediate top. But more importantly the dollar cycle is way too short to be looking for an intermediate bottom. In order for stocks and gold to form an intermediate top we would need to see the dollar form an intermediate bottom.  You can see in the above chart that the Fed's monetary policy has led to normal to slightly stretched dollar cycles also. The current cycle would have to have bottomed on the 13th week. This would also have to correspond to the yearly cycle low. Now what are the odds of a yearly cycle low, a major bottom, being put in above 74, in a shortened cycle, with sentiment never hitting true bearish extremes? (The recent public opinion poll had bulls at 29% and I've seen it as low as 22% at prior yearly cycle lows) Pretty slim in my opinion. There is no question the dollar is now in the grip of the three year cycle decline and in the beginning stages of a currency crisis. That being the case I seriously doubt the dollar will be able to move significantly above major resistance at the 80 pivot. It's already half way there now. If this is an intermediate bottom the rally is about to hit a brick wall that I have serious doubts it will be able to penetrate for more than a day or two, if at all. Far more likely in my opinion that the dollar rally will fail at 80 and roll over into the natural timing band for an intermediate cycle low sometime in mid to late December. This should drive stocks and gold higher into December before finally rolling over into intermediate degree corrections in January or early February. Finally, to top it off, we still haven't seen the large selling on strength day or days that occur at virtually all intermediate tops. Until we see signs that big money is sneaking out the back door I'm going to assume the intermediate rally is still intact.

This posting includes an audio/video/photo media file: Download Now | ||||

| Health-Care Realities, The Chinese Renminbi is Going Down, Not Up Posted: 13 Nov 2010 12:47 AM PST Health-Care Realities The Chinese Renminbi is Going Down, Not Up First, Let's Lower the Bar They Need to Borrow How Much? Really? Irish Eyes Are Not Smiling China's currency is rising ever so slowly against the dollar. But is that hurting China? We will look at a very interesting chart and some research. And then we'll gain some more insight into why the employment numbers seemed to surprise. I guess if you lower the bar, it's easier to jump over. I also deal with the pushback from last week's Outside the Box! And Ireland is on my radar. There is a lot to cover, so let's jump in.

| ||||

| The Tale of André Prenner, a Parable for our Times (Part One of Two) Posted: 13 Nov 2010 12:25 AM PST Today, we take a brief pause from our normal economic and financial market commentary with this tale of common sense economic calculation and action. And no, we do not believe that the world is any more complex than we present it here. If you want to understand economics, you need first understand two things: That the human condition is one of scarcity and uncertainty; and that absent rational economic calculation and a certain degree of passionate risk-taking, nothing good can ever come of it. Yeoville was a small Midwestern town of farmers, a few shops and cottage industries. It had grown slowly through the years and had not changed much. Once in a while there was a good year, less frequently a bad one. On occasion these were related to poor weather or other reasons for a poor harvest. There was also the difficult time when a large portion of the young men went off to fight in a war. Fortunately, most returned, although their absence put a huge strain on the remaining residents to make ends meet. But on the whole the townsfolk thought well of their position and went about their business with a healthy mix of realism for today and optimism for the future. Mr. André Prenner was one of the more successful small businessmen in Yeoville. He was now in his 60s. His father had been a baker and manager of the town bakery, Yeoville Bakers. He was descended from immigrants from France, or so he was told by his parents, hence his first name. André learned the baker's profession from a young age, at first informally, assisting his father outside school hours and, after graduating the local high school, working part-time while taking a degree course in business at the local community college in the larger town a few miles downriver. As time would tell, André was not only given to work, but to greater ambition. Taking advantage of youth, some savings from his part-time work, and a strong dollar, André celebrated completion of his business degree by taking an extensive trip to France–back to where, supposedly, his family was from–and also around various other countries in Europe. What he found astonished him: Unlike at home, where bread was simple, white and cheap, in France and in Europe generally, there was an endless variety of breads, in all shapes, sizes and even colors. It was as if the bread changed village to village. Even breads that looked the same tasted somehow different. André returned to Yeoville some months later with a passion and a plan. He was going to turn Yeoville Bakers into something far greater than just a typical, small-town Midwestern bakery. He was going to introduce a range of European breads for distribution all over the state! Now this was easier said than done. Anyone could, with enough searching around in a large city library, find a book with recipes for various types of European breads. But where to source the ingredients? And just because he loved the variety, would a range of pricey European breads sell well to a customer base which had lived its entire life chewing on the basic, cheap white stuff? André promptly answered each such question with his passion. He was just going to have to give it a go. He was young; he knew the trade; he had learned to love European breads in short order; he had the support of his father even, who had a soft spot for his presumed French heritage. The worst that could happen is that he would go bankrupt and, as an experienced young baker, would then seek an assistant manager's job at one of the many small-town bakeries in the state. In other words, his worst case was really quite similar to what he would do if he didn't even give it a try. So give it a try he did. It didn't take long to discover that, if you knew where to look, ingredients for European breads were not difficult to come by. Indeed, the bigger US cities, in particular on the mid-Atlantic coast, were home to some well-established bakeries producing European-style breads. He soon found how to get access to those same ingredients, transported to Yeoville for what he believed reasonable cost. He also researched the cost of distributing his breads to other towns in the region and how to partner with local shopkeepers to sell his product. That was the easy part. More difficult was that he was going to need to expand the existing bakery by adding new equipment. If he simply stopped producing basic white bread, the bakery would generate no income at all during an uncertain transition period and risk losing its client base. No, he would need to develop the new range of breads in parallel. As the bakery had not generated enough retained earnings to cover the purchase of the required new equipment, André was going to have to go to the local bank for a loan. Business plan in hand, he took his years of experience, good local reputation and enthusiasm into the bank. When he departed that day, he had secured a business loan, itself secured on the new equipment he was about to acquire. Once he had arranged for the purchase of the new equipment–which would be delivered, installed and operational within just two months–he set out looking for the three new employees that would be required to run it. Only one needed experience, as he had that himself in spades. The other two could just be hard-working, reliable and willing to learn. He found the experienced employee at a bakery in a nearby town who was keen on a new challenge. The other two he found locally, both of whom had been doing odd jobs since graduating high school a year before, but according to their references they did quality work when they could get it and were quick to learn new skills. For the first few months André didn't give a thought to making a profit from the new operation. He wanted to sample customers' tastes and make the decision regarding on which breads to focus for the first year so that he could secure the needed ingredients in affordable bulk rates. He travelled to many towns and even some small villages in his bakery truck, giving away free, fresh samples everywhere he went. Once it became clear what people liked and were willing to pay a bit more for, he contacted his suppliers, ordered the necessary ingredients for regular, weekly deliveries over the coming year, arranged for the printing and distribution of promotional material, finalized agreements with shopkeepers all over the state, and sent the new baking operation into high gear. Already in the first year the new breads were contributing a substantial portion of the overall Yeoville Bakers' profit and André repaid one-third of the bank loan. The business was growing rapidly, but now all costs were variable, internally-generated cash was substantial and, as such, the loan was no longer required. He paid it down fully within three years, two years ahead of schedule. This freed up additional cash which was used the following year to finance the lease for a new bakery, in another town about 50 miles away, which would make full statewide distribution a reality. André was pleased with his success as a businessman but nothing pleased him more than when he entered the bakery at 5am each morning–bakers are notoriously early risers due to their need to prepare for everyone else's breakfast–and smelled those European breads that he had first encountered several years prior on that auspicious trip to Europe. Bread was his business but remained his passion. Many years later André was the most prominent baker in the state. He even distributed some to neighboring states. He employed nearly 100 bakers and a handful of young apprentices. But then came hard times: A major national recession. Budget cutting was the norm and, when it came to bread, customers were buying far less of his gourmet European breads. The operation was losing money rapidly and something had to be done. Setting his passion aside for expediency, André took immediate action to protect his business. Having learned his trade by baking the simplest, cheapest bread possible, he went back to his roots. He cancelled his contracts with his suppliers for the gourmet ingredients and, once existing supplies were depleted, reoriented his entire operation toward making basic bread again. A dozen employees focused on the gourmet breads business were let go on the understanding that they would be re-hired once business turned for the better again. Other staff was expected to take a temporary pay cut. A few resisted but, once it was clear most of their fellow employees were willing to accept it, they went along. To be continued… Regards, John Butler, [Editor's Note: The above essay is excerpted from The Amphora Report, which is dedicated to providing the defensive investor with practical ideas for protecting wealth and maintaining liquidity in a world in which currencies are no longer reliable stores of value.] The Tale of André Prenner, a Parable for our Times (Part One of Two) originally appeared in the Daily Reckoning. The Daily Reckoning, offers a uniquely refreshing, perspective on the global economy, investing, gold, stocks and today's markets. Its been called "the most entertaining read of the day."

| ||||

| Volume Signals Gold and U.S. Dollar Counter Trend Move Posted: 12 Nov 2010 10:41 PM PST Price action that comes after a major announcement reveals a lot about underlying economic trends and the psychology of the market. Leading up to the election investors became enthusiastic on precious metals and commodities as QE2 was celebrated. Then the official announcement of QE2 caused the precious metals to gap higher as euphoria of the Fed's move were celebrated. As the celebration continued for gold bugs, as hard as it was, I believed was time to fight the investment herd and take profits. I warned readers that a healthy correction could begin and do not buy the recent breakout. Key high volume reversal days and negative divergences indicated there could be 15-20% correction and a countertrend rally in the dollar.

| ||||

| Gold To Swing $100 To $300 In A Day Posted: 12 Nov 2010 08:32 PM PST View the original post at jsmineset.com... November 12, 2010 06:20 PM Dear CIGAs, Eric King of KingWorldNews.com was kind enough to interview me on today's market action. Click here to listen to the interview…...

| ||||

| Crude, Gold Suffer Biggest Losses in Weeks as G20, European Troubles Weigh Posted: 12 Nov 2010 08:06 PM PST courtesy of DailyFX.com November 12, 2010 04:16 PM The commodity markets plummeted into the end of the week. While the backdrop of risk appetite was far more restrained, we can see there were many unique factors exacerbating the selling pressure on both oil and gold Friday. North American Commodity Update Commodities - Energy A Financial Crisis and Calls for an Increase in Margin Spooks Oil Traders Crude Oil (LS Nymex) - $84.88 // -$2.93 // -3.34% Without a sense of exaggeration, crude plummeted on Friday. While technically this was only the largest percent decline since October 19th, its performance was made all the worse for the fact that the drop can be construed as a potential major reversal. After weeks of choppy advance (on a close-to-close basis, the market has only fallen two out of the past ten active trading days), the explosion in volatility and subsequent shift in direction paints a far more meaningful picture of the market. We could simply chalk the s...

| ||||

| MERS ATTACK!!! (Updated With Must Have Fraudclosure Flow Chart) Posted: 12 Nov 2010 03:54 PM PST

"GET READY FOR THE GREAT MERS WHITEWASH BILL" "Wall Street money is pouring into the coffers of those who are receptive (i.e., almost everyone in Congress). The legislation is already being drafted under the interstate commerce clause to ratify MERS and everything it did retroactively. It appears that the Obama administration is ready to pardon all the securitization deviants by signing this bill into law. This information is corroborated by several people who are in sensitive positions — persons who would be the first to know such proposals. Fortunately, there are some people in Washington who have a conscience and do not want to see this happen." John Carney, CNBC--"When Congress comes back into session next week, it may consider measures intended to bolster the legal status of a controversial bank owned electronic mortgage registration system that contains three out of every five mortgages in the country. The system is known as MERS, the acronym for a private company called Mortgage Electronic Registry Systems. Set up by banks in the 1997, MERS is a system for tracking ownership of home loans as they move from mortgage originator through the financial pipeline to the trusts set up when mortgage securities are sold. The system has come under scrutiny by critics who charge MERS with facilitating slipshod practices. Recently, lawyers have filed lawsuits claiming that banks owe states billions of dollars for mortgage recording fees they avoided by using MERS... Now it appears that Congress may attempt to prevent any MERS meltdown from occurring. MERS is owned by all the biggest banks, and they certainly do not want it to be sunk by huge fines. Investors in mortgage-backed securities also do not want to see the value of their bonds sink because of doubts about the ownership of the underlying mortgages. So it looks like the stage may be set for Congress to pass a bill that would limit MERS exposure on the recording fee issue and perhaps retroactively legitimate mortgage transfers conducted through MERS private database...."

Here is the CNBC article:

For maximum drama and effect, I recommend you play all the sirens at once ;-)

[UPDATE: This is fresh from the Lab, enjoy ;-)]

WB7

| ||||

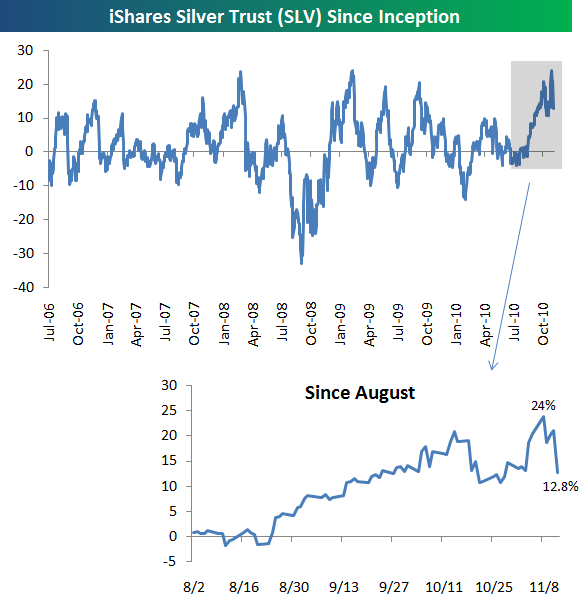

| Posted: 12 Nov 2010 02:24 PM PST  Hickey and Walters (Bespoke) submit: Hickey and Walters (Bespoke) submit: On Monday we did a post highlighting how overbought the iShares Silver Trust (SLV) had gotten. Its share price got to 24% above its 50-day moving average, which was the same level as two prior peaks for SLV since inception in 2006. It didn't take long to work off these overbought levels, however. After a couple big down days since Monday, SLV has basically cut its 50-DMA spread in half to 12.8%.

Complete Story »

| ||||

| Price Volume Action Signals Counter Trend Move In U.S. Dollar and Gold Posted: 12 Nov 2010 09:15 AM PST Price action that comes after a major announcement reveals a lot about underlying economic trends and the psychology of the market. Leading up to the election investors became enthusiastic on precious metals and commodities as QE2 was ... Read More...

| ||||

| Posted: 12 Nov 2010 08:27 AM PST | ||||

| Using a Long-Term Calendar Spread to Trade Gold Posted: 12 Nov 2010 08:15 AM PST At this point anyone following financial markets realizes that current market conditions are directly impacted by the movement of the U.S. dollar. Recently the dollar has shown strength and could potentially be putting in an ... Read More...

|

{kind=link}

{kind=link}

| You are subscribed to email updates from Save Your ASSets First To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment