Gold World News Flash |

- Happy New Year Middle Class: The Fiscal Cliff Is Going To Rip You To Shreds

- Keiser Ethical Silver rounds

- Is Silver About to Begin a Parabolic Rally to $60+ OR Collapse to Possibly As Low As $22?

- Alasdair Macleod's Outlook for 2013

- Silver market rigging lawsuit against Morgan dismissed but may be revived

- Market Pendulum Simplified

- Robert Kiyosaki Mike Maloney Discuss Preparing for the Coming Crash 2013 – YouTube

- Why Invest In Gold and Silver Robert Kiyosaki’s Precious Metals Advisor – YouTube

- Be A Winner Dont Save Invest In Assets – Robert Kiyosaki – YouTube

- GoldSeek.com Radio: Jim Rogers & Nick Barisheff, and your host Chris Waltzek (encore show)

- JuMP YoU F*#CKeRS!

- The Agenda Of Our Leaders For The Coming 4 Years

- Silver: Another Decade of 500% Returns is Very Possible – Here's Why

- The Year That Was 2012

- The Fiscal Policy Q&A, Timeline, And Market Scenarios

- Got Gold Report - COT Chart Review for December 30

- The New Era of Oil Renaissance

- The Bright Future of Gold: The Final Solution of the 2008 Monetary Crisis

- The Charts Tell ALL and THIS Is What They're Saying About Gold & Silver for 2013

- A CANADIAN SOLUTION TO THE GUN PROBLEM

- 75 Facts Revealed – How Is America Really Doing?

- WILL YOU OBEY?

- Empires of Illusion and the Credibility Trap

- Gold and the fiscal cliff

- Diplomatic cables disclose more conspiring by Western governments to rig gold market

- Macleod and von Greyerz give their financial outlooks for 2013

- Japan lashes out over depreciating dollar and euro

- India Is Behind the Weak Price of Gold – Here's Why

- Gold & Silver: Opposing Forces Very Under-Rated

- GoldMoney article: Outlook for 2013

| Happy New Year Middle Class: The Fiscal Cliff Is Going To Rip You To Shreds Posted: 30 Dec 2012 11:30 PM PST from The Economic Collapse Blog:

| ||

| Posted: 30 Dec 2012 10:00 PM PST from NWTMint.com:

Advocating for the common man against banks and other organizations that control the economy and are "too big to fail," silver believer, financial commentator and former broker Max Keiser leads the international movement called Global Insurrection Against Banker Occupation, or GIABO. This silver bullion, minted according to Environmental Social and Corporate Governance principles ("ESG principles") and sourced from US recycled metal, is .999 pure, and a tangible symbol of the movement that Keiser intends will end the influence of the centuries-old banking establishment. Bearing the mark of "Keiser Ethical Silver," these silver rounds are intended for those who wish to invest in a higher standard of silver – silver that is pure and minted in superior quality, but also from refiners with exceptional ethical, social and environmental practices. | ||

| Is Silver About to Begin a Parabolic Rally to $60+ OR Collapse to Possibly As Low As $22? Posted: 30 Dec 2012 08:34 PM PST "Follow the munKNEE" via twitter & Facebook Is silver about to begin the parabolic rally over $60? My simple answer So writes Avi Gilburt (www.elliottwavetrader.net) in edited excerpts from his original article* on Seeking Alpha entitled Silver: Are We Ready Yet For The Rally To $60+?.

Gilburt goes on to say, in part: The current consolidation is simply just that - a consolidation - before we head to lower levels. It is my expectation that:

It will be the pattern with which we begin such [a] decline that will tell us at which of the [above] targets silver will find its next level of support. The deeper the decline, the more likely it will be that silver will ultimately be breaking down below the $26 support region. IF silver drops all the way to the $26.60 region:

For now, [however,] as long as silver maintains below the $31.60 region, it will be heading down much lower. Conclusion Any break out over the $31.65 level, which sees strong follow through over $32.65, would be my initial indication that silver has bottomed and we are beginning the rally to over $60 [although] I do not view such a break out at this time as a high probability. Rather, lower levels will likely be seen before the parabolic rally begins but, [that being said,] we have to be prepared in the event that the parabolic rally begins prematurely.

*http://seekingalpha.com/article/1086771-silver-are-we-ready-yet-for-the-rally-to-60? Related Articles: 1. Availability Of, and Demand For, Silver vs. Gold Suggests MUCH Higher Future Prices for Silver

2. Silver: 5 Forces That Should Help Polish Off the Tarnish & Propel It Higher

3. Why You Should Now Invest in Silver vs. Gold

4. Gold:Silver Ratio Suggests MUCH Higher Price of Silver in Next Few Years

| ||

| Silver market rigging lawsuit against Morgan dismissed but may be revived Posted: 30 Dec 2012 07:30 PM PST by Chris Powell, GATA:

Dear Friend of GATA and Gold (and Silver): A federal judge has dismissed the class-action silver market-rigging lawsuit against J.P. Morgan Chase & Co. that was brought a year ago in September, ruling that the complaint lacked the specifics and claims of bad intent necessary to be allowed to proceed to trial. The dismissal was ordered a week ago by Judge Robert P. Patterson Jr. in U.S. District Court for the Southern District of New York. The judge gave the plaintiffs 30 days to show cause why they should be allowed to file a substitute complaint. Judge Patterson's decision is posted in PDF format at GATA's Internet site here: http://www.gata.org/files/GATASilverClassActionDismissed-12-21-2012.pdf | ||

| Posted: 30 Dec 2012 07:28 PM PST During the past year, manynew readers from 45 countries and have found the information on this freewebsite to be extensive, detailed and intriguing on both a technical and fundamentallevel.[B][COLOR=#3d85c6][FONT=Arial] [/FONT][/COLOR][/B] [B][COLOR=#3d85c6][FONT=Arial]By category, this guide will help simplify where to look for the information you need as we approach another primary low risk area in Gold, Silver andthe XAU.[/FONT][/COLOR][/B] [CENTER]Key Charts & Technical Articles [/CENTER] Monthly charts for the XAU and S&P500 are located [COLOR=#e06666]here. [/COLOR] [COLOR=#e06666]The Market Pendulum Model explains the various technical indicators and itscompanion, The Pendulum Trading System, provides the trading methodology. [/COLOR] [COLOR=#0b5394]Key Fundamental Articles [/COLOR] [COLOR=#e06666]Breakpoint - A collection of financial analogies presentedin a manner that is readily understandable by all. It also provides timelineestimates on financial breakdown as well... | ||

| Robert Kiyosaki Mike Maloney Discuss Preparing for the Coming Crash 2013 – YouTube Posted: 30 Dec 2012 07:25 PM PST Check our website daily at http://www.figanews.com Robert Kiyosaki Mike Maloney Discuss Preparing... [[ This is a content summary only. Visit http://goldbasics.blogspot.com for full Content ]] | ||

| Why Invest In Gold and Silver Robert Kiyosaki’s Precious Metals Advisor – YouTube Posted: 30 Dec 2012 07:19 PM PST Check our website daily at http://www.figanews.com Why Invest In Gold and Silver Robert... [[ This is a content summary only. Visit http://goldbasics.blogspot.com for full Content ]] | ||

| Be A Winner Dont Save Invest In Assets – Robert Kiyosaki – YouTube Posted: 30 Dec 2012 07:11 PM PST Check our website daily at http://www.figanews.com Be A Winner Dont Save Invest In Assets –... [[ This is a content summary only. Visit http://goldbasics.blogspot.com for full Content ]] | ||

| GoldSeek.com Radio: Jim Rogers & Nick Barisheff, and your host Chris Waltzek (encore show) Posted: 30 Dec 2012 07:00 PM PST Guests: Nick Barisheff CEO at Bullion Management Group Inc Jim Rogers A Bull In China | ||

| Posted: 30 Dec 2012 05:34 PM PST

The Man in the High Choom Castle . . "With the slightest disturbance, the dream is going to collapse."--Inception | ||

| The Agenda Of Our Leaders For The Coming 4 Years Posted: 30 Dec 2012 03:06 PM PST It is the end of the year, the ideal time to look back in the past year and make a forecast of the new year. Lindsey Williams described the outlook till 2016. The remarkable things is that it was not his personal outlook but the one from the (political) top leaders. It is tricky to make these statements. However, given his background and the evidence we already see today, we believe that the outlook could be correct. Lindsey Williams is the man who, because of his contacts in the oil industry, correctly predicted that the world price for oil would fall from roughly $140.00 per barrel to less than $50.00 per barrel. He claims to be well connected to what he calls "the power elite" because of his former executive role in the oil industry. His sources in the oil industry are directly linked to the top political leaders giving them "insights" in their agenda's. In a recent video interview he confesses how the high level agenda of our leaders looks like, at least for the coming four years. The embedded video provides much more detail, specifically between minutes 5 and 33. Note that this information applies primarily to the US. Courtesy of InfoWars.

Lindsey Williams mentions also the objective for the price of gold. By 2016, it should go to $3,000 to keep pace with the debt creation. | ||

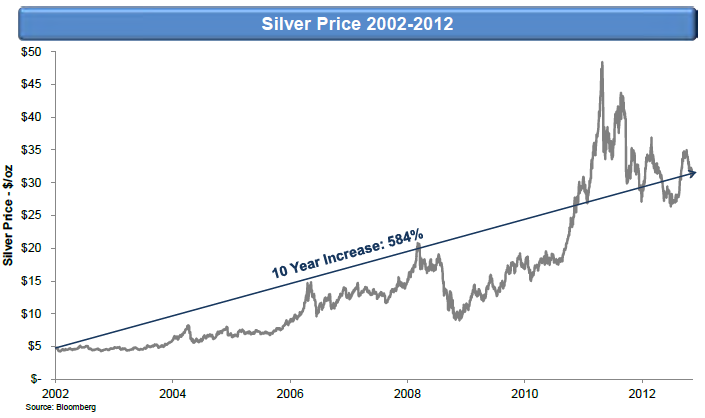

| Silver: Another Decade of 500% Returns is Very Possible – Here's Why Posted: 30 Dec 2012 03:05 PM PST "Follow the munKNEE" via twitter & Facebook Silver has given returns of 584% in the last ten years and this article So writes the Economics Fanatic (www.economicsfanatic.com) in edited excerpts from the original article* as posted on Seeking Alpha under the title Silver: Another Decade Of 500% Returns Is Possible.

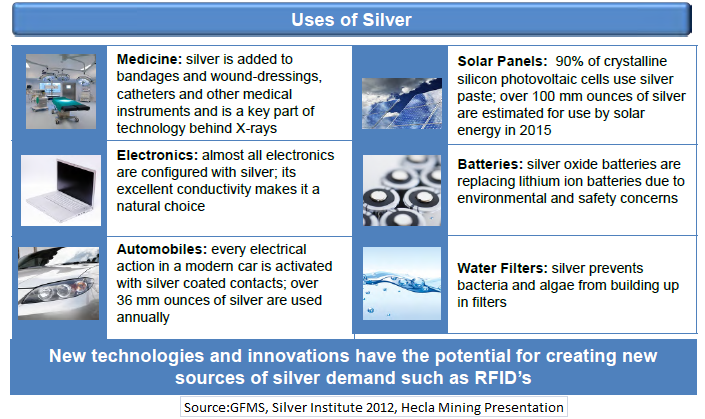

The article goes on to say, in part: Silver prices have corrected meaningfully after peaking out at near USD50 levels. A correction of over 20% is generally considered bearish and can weaken investors' interest in the metal [but] I believe that silver can produce another decade of over 500% returns [just like it did] in the last 10 years. (click to enlarge) The Current Macro-economic Scenario's Impact on Silver The global economy (especially the developed markets) is in a phase of prolonged sluggish economic growth. GDP growth has been volatile since 2007, and recession seems very likely for the U.S. without government support. Further, the eurozone is already in a recession. This scenario necessitates continued expansionary monetary policies by Central bankers globally, and is positive for hard assets like gold and silver. Industrial Demand for Silver to be a Major Driver for Silver Prices [As the graph shows below,] the demand for silver coins and medals has increased by 248% during the period 1990 to 2011…[and] industrial demand for silver has surged by 78%….I am of the opinion that Industrial demand will be the second biggest driver for silver prices after the hard asset factor. I can also say with some conviction that industrial demand for silver will grow at a greater pace than witnessed in the last two decades. (click to enlarge)

There are certain important properties that make silver a favored industrial metal.

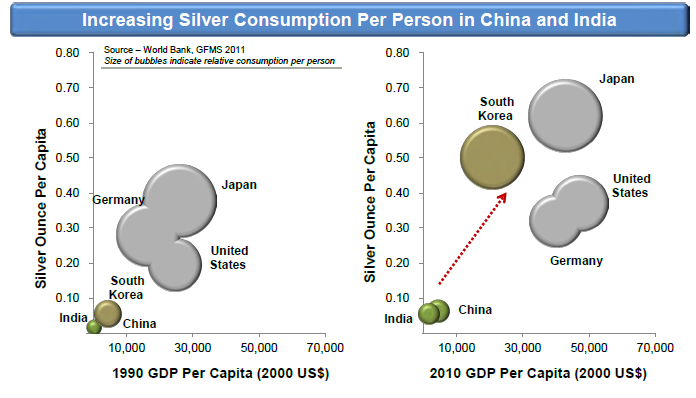

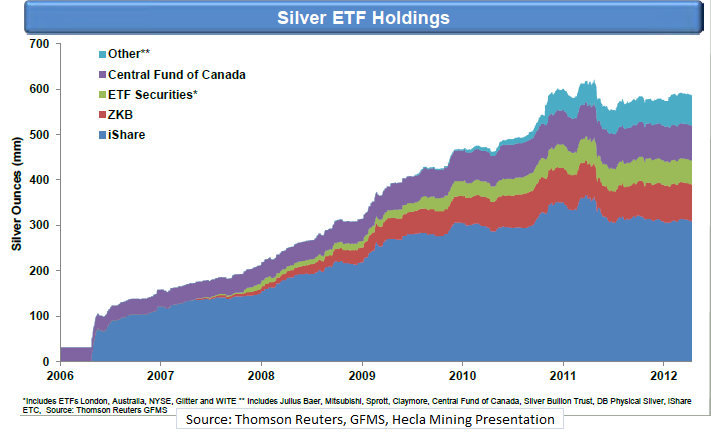

The diagram below gives a summary of the industrial application of silver and the potential new areas where silver can be utilized. (click to enlarge) I mentioned earlier that I expect the industrial demand for silver to grow at a more robust pace than before. The primary reason for this rationale is the low per capita consumption of silver in emerging markets as compared to developed markets. Even if the per capita demand for silver in China and India (home to over 2.5 billion people) comes anywhere near the per capita consumption of developed markets, the amount of silver that needs to be mined will be very significant. (click to enlarge) The huge impending growth in Asia, Africa and emerging Europe, coupled with the population factor, will be the key demand driver for silver in the long-term. The chart below gives the expected demand for silver excluding investment and ETF demand. With the above discussed industrial drivers, demand is expected to surge over the next two decades. At the same time, the silver ETF holdings have surged since 2007 to record highs. (click to enlarge) This surge in silver ETF holdings has been largely due to the financial crisis, which continues to plague the developed economies. Going forward, the silver demand will continue to increase as investors and individuals buy silver more as a currency, which is a store of value than for any other purpose. Lack of Supply of Silver to be a Major Driver for Silver Prices Coming to the supply side factors, there could be a demand-supply mismatch with growing demand for silver from Asia in 2015. The current silver demand of 1.06 billion oz is expected to rise to 1.18 billion oz by 2015. With no major silver mining project in the pipeline, surge in investment demand coupled with industrial demand has the potential to outpace the expected supply. If this scenario pans out, [the price of] silver will trend meaningfully higher over the next few years. Conclusion Considering all these fundamental factors, it makes sense to consider exposure to silver at current levels and add to the position on any correction. The metal is certainly poised for another decade of the bull market and has the potential to outperform many asset classes. In line with this expectation, I would consider exposure to physical silver as a first choice of investment. Also, investors can consider the following stocks and ETFs for exposure to silver.

*http://seekingalpha.com/article/1086891-silver-another-decade-of-500-returns-is-possible Related Articles: 1. Availability Of, and Demand For, Silver vs. Gold Suggests MUCH Higher Future Prices for Silver

2. Silver: 5 Forces That Should Help Polish Off the Tarnish & Propel It Higher

3. Why You Should Now Invest in Silver vs. Gold

4. Gold:Silver Ratio Suggests MUCH Higher Price of Silver in Next Few Years

| ||

| The Fiscal Policy Q&A, Timeline, And Market Scenarios Posted: 30 Dec 2012 02:31 PM PST Talks on the fiscal cliff have resumed, but as of this writing there is not yet an agreement. The current negotiations focus on the income threshold under which tax cuts should be extended, among other topics. As we have noted, the sides seem as far apart as ever, and as Goldman notes, while it is still possible that an agreement will be reached by year end, a retroactive deal in January looks more likely. The eventual resolution still looks likely to be a scaled down agreement that addresses only the policy changes scheduled for year-end and omits other issues, such as an increase in the debt limit or longer-term fiscal reforms. The greatest area of uncertainty is whether the spending cuts scheduled under the sequester will be addressed. The fiscal policy timeline below shows how we are rapidly approaching the more ominous debt ceiling debate and Goldman's Q&A asks and answers provides context for where we are from both an economic and ratings agency impact basis. Scenario Analysis (Via Citi's Steven Englander):

Q&A and Timeline (Via Goldman Sachs): Q: Where do things stand now? A: Talks have resumed, but as of this writing there is no agreement yet. President Obama and congressional leaders met this afternoon to discuss the possible next steps that might be taken to avoid the fiscal restraint set to take effect at year-end. It seems likely that Senate Majority Leader Reid (D-NV) will bring up legislation on the Senate floor at some point before the end of the year, but it is not yet clear whether that will be the product of a bipartisan compromise reached with Republican leaders and the President, which would have a chance of passing both chambers of Congress, or a proposal supported only by Democrats, which would be less likely to pass in either chamber, particularly the House. Q: Will there be an agreement by year-end? A: It is still possible but a retroactive deal in January looks more likely. With little time left before year end, there are two obvious obstacles to enacting an agreement by that time: the lack of a political agreement, and the short time left on the calendar to get any agreement that might be reached enacted into law. Reaching a political agreement is the tougher part. It is conceivable that Senate Republicans could allow a compromise dealing with the middle-income tax cuts and a few other items to pass in the Senate; this would happen if Republicans refrained from objecting to consideration of a bill, allowing it to pass with a simple majority (i.e., most of the 53 Senate Democrats) rather than the 60-vote supermajority that has become customary for major legislation. However, House Speaker Boehner has stated that he will not support a plan that involves passing legislation in the House with mostly Democratic votes. This may become less of a constraint after year end, since (1) taxes will have risen, allowing both parties to claim that the agreement is a "tax cut," (2) the House will vote to choose its speaker January 3, after which it may be easier for Speaker Boehner to allow legislation to pass with mostly Democratic votes, and (3) public pressure on lawmakers will have increased, making them more willing to compromise. In the somewhat less likely event that an agreement is reached before year-end, the logistics of passing it in the House and Senate will take a bit more time, but will be less relevant. Most market participants and the broader public are likely to respond more to the news of an agreement rather than the particulars of the legislative process that follows. Second, while passage using normal legislative procedures could take over one week, passage could be accomplished in just a few days if there is political will to do so. Q: If an agreement is reached, what would it look like? A: Probably a scaled-down deal. At this point, the most likely solution prior to year end (or in the first few days of 2013) would be enactment of a scaled-down agreement that addresses only the policy changes scheduled for year-end and leaves for later other issues, such as an increase in the debt limit or longer-term fiscal reforms. This might involve an extension of the 2001/2003 tax cuts for income under $400,000 or $500,000 (including capital gains and dividend tax rates at 15% for taxpayers with income under that level and a 20% rate above), relief from the alternative minimum tax (AMT) for 2012, and extension of emergency unemployment benefits, which are scheduled to expire at year end. A few other aspects of a scaled-down agreement are less clear:

Q: If there is no deal by year end, does it matter? A: Yes, but how much will depend on how uncertain the outcome remains, and how long the uncertainty lasts. In our view it seems more likely that Congress will miss the year-end deadline but will pass an agreement in January. In theory this could come as early as January 2, the last day before Congress convenes for its new session, but it seems more likely to occur between January 3 (the first day of the new session and the scheduled date for congressional leadership elections) and January 21, when the President will be inaugurated into his second term (Exhibit 1 lists key fiscal policy events over the coming months). The effect of a temporary lapse would come mainly through confidence. We have noted recently that policy uncertainty might hold back capital spending. The risks associated with the fiscal cliff also seem likely to have already weighed on consumer confidence to some extent, even before the deadline. Consumers' assessment of the current situation has become quite positive at the same time that their expectations for the future have become more pessimistic (Exhibit 2). This is likely due in part to reduced expectations of a deal by year-end; indeed, internet searches for the term "fiscal cliff" have outpaced searches related to the debt ceiling at the comparable period in 2011. (Exhibit 3). However, from a fundamental perspective, the effect of a short lapse would probably not be that significant, assuming that it lasted no more than a few weeks. This would be especially true if there is some certainty regarding the eventual outcome, and an expectation that the eventual agreement will be made retroactive (which we expect it would be).

Q: Is there anything that can be done to avoid the increase in tax withholding and decrease in spending set to take effect that doesn't involve Congressional approval? A: The administration can prevent some of the tax increase and sequester, but only for a while. The Internal Revenue Service (IRS) must decide how to instruct employers and payroll processors to withhold taxes from paychecks starting January 1. Normally the IRS transmits updated withholding information by early December to allow sufficient time for systems adjustments. While the IRS has indicated it will provide guidance by year end on appropriate withholding for 2013, to date it has not provided an update. While some larger payroll processing firms and employers may be able to adjust systems very quickly in The IRS also has discretion in how much to instruct employers to withhold. Although only Congress determines the ultimate tax liabilities individuals will face for 2013, the IRS must instruct employers on how to best withhold taxes from paychecks to match those rates. In principle, the IRS could simply instruct employers to leave withholding unchanged until an agreement is sorted out, at which point new withholding instructions could be transmitted. This is an obvious short-term solution, but it could only be used for a few weeks. If the IRS declined to update withholding instructions much longer than that, individuals could face a more serious gap between their withheld taxes and ultimate tax liabilities, resulting in significant tax liabilities at year end, or an even sharper increase in tax withholding once instructions to employers were eventually updated. On the spending side, the administration can delay the spending cuts scheduled to take effect under sequestration if a deal seems close at hand.1 However, just like a delay in the scheduled tax increase, failure to implement the cut at year end might mean an even sharper adjustment later if Congress is unable to reach an eventual agreement, since the required reduction would need to be concentrated in a shorter period (i.e., the remainder of the fiscal year that ends September 30, 2013). Q: The debt limit will be reached December 31?how does this relate to the "fiscal cliff"? A: The debt limit is separate from the fiscal cliff, but intertwined in the negotiations. The Treasury projects that the debt limit will be reached December 31, but that it will be able to tap certain funds that will allow it to continue to borrow as necessary until late February 2013, by which point Congress will need to increase the limit. The Treasury notes that if the fiscal cliff is left unresolved, the deadline for the next increase in the debt limit would be pushed beyond late February, though it does not specify how far beyond. Exhibit 4 shows our projection of debt subject to limit under our base case fiscal assumptions and a scenario in which the fiscal cliff is not resolved. The White House very much wants to avoid another disruptive debate over the debt limit similar to the one that occurred in the summer of 2011. The Administration had hoped to include a debt limit increase in the year-end agreement, first proposing an open-ended increase, and later seeking a two-year extension. However, congressional Republicans continue to insist on a dollar of spending cuts (measured over ten years) for each dollar the debt limit is increased. At this point it appears more likely that the debt limit increase will be left out of a year-end deal, as will any long-term spending reforms. Instead, these look likely to be debated in a second round of negotiations ahead of the next deadline, probably in February 2013.

Q: What should we expect from the rating agencies? A: Probably no action as a result of the fiscal cliff, but a downgrade in 2013 is possible. Two of the three major rating agencies, Standard & Poor's and Moody's Investor Service, have indicated they are unlikely to lower their rating regardless of how the fiscal cliff is resolved. While both acknowledge that a sharp fiscal contraction would lead to economic uncertainty and a likely recession, the contraction would also probably be enough to stabilize and slightly lower the debt-to-GDP ratio over the medium term, which is the most important criterion for the sovereign rating. By contrast, Fitch Ratings, which maintained a stable outlook on its AAA rating longer than the others (it shifted to a negative outlook only after the "super committee" failed to reach an agreement in late 2011) has become more downbeat, suggesting a downgrade is possible if the debt limit is not raised in a timely manner or if the fiscal cliff is allowed to take effect for long enough to have significant economic effects.

| ||

| Got Gold Report - COT Chart Review for December 30 Posted: 30 Dec 2012 02:29 PM PST Vultures (Got Gold Report Subscribers) please log in and navigate to the Got Gold Reports Section for an update containing most of the charts we review each week for the Commodity Futures Trading Commission (CFTC) commitment of traders report (COT). The charts present a visual record of the significant changes in the COT data. | ||

| The New Era of Oil Renaissance Posted: 30 Dec 2012 02:22 PM PST By EconMatters Where Nuclear Failed, Oil Succeeded

Well, the natural disaster in Japan changed that movement in the span of a week of just untenable radioactivity readings coming out of Japan. An already uphill battle for changing public sentiment towards the dangers of nuclear energy became an impractical fight from an investment standpoint that relied upon large DOE loan guarantees to attract private investment.

It is ironic, but all these companies spent a lot of time and effort from lobbying to developing strategic partnerships with each other, and in the end, most of that 7 year effort had to be written off by firms. It really shows how firms have to get the industry right; Oil was so much the smarter play. Higher margins, better technology, much easier safety hurdles, and even the environmental fight is much more manageable.

Not to mention the number of jobs created is far more with an Oil Renaissance as opposed to a Nuclear Renaissance, even with a complete buildup of the entire nuclear supply chain. Nuclear projects are just not scalable like oil projects are from a numbers standpoint due to the regulation, lead times for components, inspection, build times, and many more constraints.

No DOE Loan Guarantees: The Free Market at Work We are going to have a Renaissance in this country, it just happened under everyone`s nose. The free market of high oil prices for the last 10 years made it happen all on its own without government subsidies, and part of the reason that things are going to get real tough for the alternative energy folks over the next 5 years as those government subsidies wind down. They will not make sense from an economic standpoint once oil prices come down considerably, and from a budgetary perspective we can no longer afford this propping up industries that cannot sustain themselves on their own merit in the free market. A 16 trillion dollar debt and climbing means the environmentalists will now be facing an uphill fight on Capitol Hill to have their cause funded by the American taxpayer.

Technology Changes: Heart Surgery meets the Oil Patch The technology changes alone in the oil industry are amazing; just watch a horizontal drilling or fracking video and it is like all the advances made by the medical community for endoscopic procedures and advanced heart surgical techniques have been applied to the oil industry. And the cost is far more manageable than the medical field with all the added insurance costs, out of control bureaucracy, and government intervention all but eliminating any sense of free market principles.

Sure these constraints exist in the oil industry, but the healthcare industry is on a planet of its own and worse from a cost efficiency standpoint by a factor of at least a 100. There is not an ounce of free market in the healthcare industry!

We haven`t seen anything yet as this new technology being refined and implemented here in the US will then be fully scalable around the globe, and the amount of new projects that will come online globally with this new technology over the next ten years has yet to be priced into any market intelligence models.

Natural Gas Industry as the Model The natural gas industry is much smaller than the oil industry, and because of the new technology firms were actually continuing production with $2 natural gas because of much lower overall project costs relative to the size of the gas exploitable and other derivative products made along the way enabling these projects to be profitable.

The oil industry is much more scalable from a cost standpoint, and once these upfront costs have been committed, the size of the industry and scalability means that projects can continue and be highly profitable even with much lower oil prices.

I previously have thought that this technology would suffer as prices drop, but I am rethinking this assumption with natural gas as my guide in a much less scalable industry. So I now believe that this technology and these projects will continue and be cost effective even with oil dropping to $45 a barrel for both Brent and WTI. It won`t happen overnight, but under one scenario prices will just steadily trend down like natural gas prices, and before we realize it we have the equivalent of $2 natural gas prices for the oil industry. The China Factor: Use less Commodities for Next Decade My assumption about the trajectory of oil prices also relies on the China factor that many analysts have been toying with for the last couple of years, but the IMF and others have done some nice research on and applied some hard numbers to the conceptual idea that China has overinvested for the last decade by a large degree, and most of the previous forecasts for China`s growth trajectory from an infrastructure standpoint for the next 10 years are far too optimistic.

My conclusion is that China will use far less commodities than they did the past decade going forward for the next decade. They are coming into the constraints of large numbers where you have built for the sake of building, and you can no longer build another large new city every year because the demand just isn`t there. Basically, the easy, low hanging fruit has been eaten. Most of the new project benefits will not justify the cost based upon infrastructure constraints, logistical incongruities, and actual demand & societal need for said projects. The societal costs outweigh the societal benefits and the projects evaluated in total become a net drag on growth and GDP in the overall calculus. China can go ahead with these projects but the law of diminishing returns, means the country will pay a heavy price to do so. China will continue to grow, but they will grow in a more sophisticated way from a social perspective from within, i.e. in a metaphorical Maslow`s – Hierarchy of Needs manner, and less of a brute, infrastructure driven manner. Ergo, the lower utilization for commodities by China is another factor that will put downward pressure on Oil and other commodities over the next 5 to 10 years.

More Storage Capacity Needed Globally Make no mistake these oil and commodity projects are going to go full stream regardless of price due to sunk costs, more efficient operations, job creation, and overall profitability.

One of the takeaways out of this analysis is that storage facilities will have to be upgraded and new ones coming online for all commodities. For example in Oil, my analysis concludes that Cushing will need to upgrade capacity to over 100 million in the next couple of years, and over 150 million by 5 years' time.

My new analysis determines the need for even more pipelines being built out of Cushing as well. There will need to be at least 5 million barrels per day outflow from Cushing to refineries by five years' time; can anyone say job creation opportunities here?

The next substantial upgrade besides the paltry 300,000 per/day upgrade this year will not come online until mid-2014 and only improve capacity to 850,000 barrels per/day outflow from Cushing which is not going to be enough to counter an exponential measure of domestic production coming into the Cushing energy hub by 2014.

But I am forecasting that not only will Cushing be above 100 million in storage in three years' time, but the US will need capacity to store over 600 million barrels by four years' time, and China who is building storage currently, will need to meet their own need for storage due to a massive oversupply in their country.

China was building storage initially for strategic purposes, but my analysis concludes that because of an oversupply issue similar to copper today in China, they are going to need this additional storage for excess supply issues.

Therefore, if you're in the storage facility business, times will be good for the next five years, plenty of business for these firms. As I think storage facilities will have to be built all around the world from Iraq, Saudi Arabia, Africa, and the Scandinavian countries.

A New Price Model for Oil So how low can prices go? Let`s just say that the Renaissance in oil is going to be good for the global economy, just back in 2003 gasoline prices were $1.60 a gallon in the US and oil was trading around $30 a barrel.

It is not unreasonable to think if the Oil Renaissance takes the path that it is capable of that Oil globally trades all the way down to the $45 area.

What Price do the Saudi`s Really Need? Need & Want Confused And those that think that OPEC would need $75 to keep up production, remember that OPEC still kept pumping oil only four years ago with $33 oil in 2008. Furthermore, OPEC countries still need the overall revenue not the price per say.

Accordingly, you could very easily have a scenario where prices go lower and they pump more, violate reduction quotas because they all want the revenue net of volume and price, not just less volume but slightly higher prices.

I think the world will be surprised how the talking your book rhetoric of "we need $75 oil to justify production" is replaced with the actual, "we need the money and our real cost is so much lower than you could ever imagine" reality on the ground.

This is their one asset in these countries, some revenue stream is better than no revenue stream, and with global production picking up OPEC `s relevance, power, and influence on prices is diminishing by the day.

Great OPEC you can reduce production, your global competitors will love that, less competition for them. The only problem is that these countries need the money, every country needs the money these days, and that`s the market place you take what you can get on the market! The market goes in cycles, just as the housing market re-priced itself, so will the oil market!

The ironic point here is that often the lower prices go, the more oil that is produced trying to make up in volume for the lower price to get as much revenue as possible.

$45 Oil & $2 Gasoline: Consumers Love this New Era In conclusion, we are entering a new Renaissance in the oil market, not just in the US, but globally as well.

New technology, slower growth in the emerging markets over the next decade, and an era where a decade of high prices will finally bear some fruit with market dynamics working as their supposed to leading to more supply, and an eventual reduction in prices.

The Bright Future of Gold: The Final Solution of the 2008 Monetary Crisis Posted: 30 Dec 2012 01:08 PM PST Jim Sinclair's Mineset My Dear Extended Family, Let's keep things very simple: 1. The future of gold will not be determined by the USA. 2. The present manipulation in gold is purely Western, and any other thought is rank nonsense. This event is both short term and very short sighted in terms of people's published analysis. 3. The triumvirate of Euroland, Russia and China will determine the future of gold as financial power has shifted from the West towards the East. 4. The strategy of the flushing of Lehman Brothers was to initiate a transfer of failed and to fail debt and debit, producing obligations in all forms from the balance sheets of international banks and investment banks onto the only entity that could mechanically accept them in infinite amounts, the balance sheet of Western central banks. To avoid a total and terminal collapse of Western finance, the US Fed had to take the entirety of the problem onto its balance sheet in exchange for n... | ||

| The Charts Tell ALL and THIS Is What They're Saying About Gold & Silver for 2013 Posted: 30 Dec 2012 12:22 PM PST "Follow the munKNEE" via twitter & Facebook It is impossible not to read some source…touting the "fact" that the The charts are all-knowing, and they present everything known about the price, sans any opinion(s). Just deal with the facts and plan accordingly. Trust the markets – they never lie – [and this is what they are saying about the price of gold and silver in 2013]. Words: 1889; Charts: 6 So writes Michael Noonan (http://edgetraderplus.com) in edited excerpts from his original article* entitled Gold And Silver – Opposing Forces Very Under-Rated. Ode On A [Un]Grecian Chart.

Noonan goes on to say, in part: Follow the Market's Lead One of the better "resolutions" one can make going into 2013, and beyond, [is] to follow the market's lead…[instead of] trying to lead it, waiting for it to catch up to your trading acumen. [Sure, sure, you might reply,] but:

Yes, well, what about it! That information…has been known for quite some time so it is already "priced into the market."

The market is telling you…all you need to know. Everything finds its way into the market, and if you would just ignore all else and follow the ultimate known fact, that being the current price of anything, then you have the answer right in front of you. The problem is, too many cannot reconcile the current price of gold and silver relative to their expectations. [They cannot see the truth staring them in the face.] As John Keats, [who, incidentally,] would have made an excellent technical analyst [given his ability of]…drawing out the paradoxical nature of things, said in From 'Ode On A Grecian Urn' : 'Beauty is Truth, Truth Beauty' — that is all Ye know of earth, and all ye need to know. This is how we see charts. Everything you need to know is contained within them because they are based on truth. What truth? The ultimate decisions to buy or sell made by the collective forces of the marketplace. Anything else that does not get translated directly in the market is simply an opinion, of no factual value because the market only recognizes actual transactions. That is the truth and the beauty of the markets. They provide you factual commitments, unadorned by uncommitted interpretive opinions. That is all ye need to know on earth. Learn to listen to what the market is saying, and not what others are saying about the market. This is not to say that markets cannot be manipulated and factors grossly distorted, for even if they are, those manipulation and distortions are what is reflected in current [prices], like it or not. The Marketplace Most who speculate in the markets, to the extent they rely upon charts, look at daily or intra day time frames. Smart money, what we call the "controlling forces" of a market, use higher time frames, for they are not concerned with day-to-day activity. Their positions and influence necessitate that they move over a more extended period of time, and one can get a greater sense of their intent from the higher time frames. When we talk about collective forces of the marketplace, it includes the most well-informed insiders, central bankers, the largest dealers, with availability to information and research outsiders may never know or learn about, until after the fact, all the way down to investors, fundamentalists, speculators, even the ephemeral day-traders. What they all have in common is that they are the market, once they make a decision to execute a buy/sell that influences and determines the price at any given point in time. Those executed decisions, regardless of how well or ill-informed, become market facts that comprise fluctuations, and they show up as the high, low, and close on a chart for any chosen time frame. Despite the relentless calls for gold and silver "taking off," which they have not, of late, the elephants in the room, governments, central bankers and major brokers, plus exchanges, have been vastly under-rated in their ability to keep the prices of gold and silver suppressed as much as they have. They are not about to throw in the towel and give up their Wizard of Oz controls. Ultimately, they are doomed to fail, but when does "ultimately" kick in, and to what degree of damage before it does, remains unknown. One thing you should know about the opposition, in whatever form it is in, ultimately: It will not stop. It will not quit. It will destroy everything that gets into its way in order to suit its needs. What the Charts Are Saying The charts have been saying as much….If gold and silver are going to go to such high price levels, why are charts saying the opposite? This end of year's gold closing, actually Monday, is about mid-range the bar, a draw between the forces of supply and demand, but the range was the smallest in several years. Neither buyers nor sellers were able to extend the range further in either direction. The arrow in the chart points to the smallest range in Qtr 2, 2012. It was an attempt to go lower that failed. Fact #1: The fact, and keep in mind the focus is on the indisputable facts contained in the charts, is that price [of gold] did not go lower…[because of] strong support at that level. Fact #2: Another observable fact is how the last 5 quarterly bars have been overlapping. Anytime you see bars overlapping, it show[s] a struggle between buyers and sellers trying to exert control. The poor end of the year close for gold says buyers have not been keeping an upper hand, and sellers are maintaining relentless pressure.

Fact #3: Back to our normal chart. If we view the rally in August as a breakout from a right triangle pattern, it is taking now 3 months to correct a 2 month rally, and the bars correcting are smaller, telling us there is no downward ease of movement. This suggests sellers are meeting more resistance, but still prevailing. What To Expect in 2013 2013 will be an interesting years, and its start could be signaling more of what we have seen for the past 15 months. While accumulation of the physical metal is strongly recommended, trading in the paper futures will have to be much more select, buying breaks, not breakouts. Fact #4: There is no question that silver remains relatively weaker to gold, as the charts clearly show. Some think silver may outperform gold, moving forward, and it has, on occasion. That is an opinion that may or may not hold true. Buying and personally holding the physical is strongly recommended, as was stated for gold. For now, silver has a very large supply factor hanging over future progress, based upon the closes of 2011 and 2012.

Fact #5: The more detailed Qtrly chart [below] has one positive aspect: 26.20+ area held like a rock. We could see yet another test and possible new low. That is not a prediction but a point of view not to be dismissed for the year ahead. As with gold, the overlapping of bars shows the struggle between the forces of sellers and buyers, the edge with sellers. The comments in the following chart read as follows: The Qtrly chart is more of a mixed message. There is obviously strong support at the 26 area, and bullish spacing remains a positive. (Bullish spacing is where the current swing low is above the last swing high, indicating buyers not willing to wait to see of the last swing high will be retested. It reflects a sense of urgency to buy.) The close at the end of this year says price should make a lower low, at least nominally, (Compared to last Qtr low only). There are times when a low end close can lead to a reversal. Not sure that is the case, here. (Just another possibility of which to be aware.) The fact that silver cannot get and stay above 35 says how much work there is to overcome sellers. 2013 should be more of the same, at least for the first half. Fact #6: As with gold, an unusually large bar most often foretells of a protracted trading range to follow. Not only did that hold true for silver, the trading range was all under a 50% retracement area, telling us how rally attempts have been weak, and also a signal from the market that $50, $100, $250 silver is not on the immediate horizon. It does not take a crystal ball, nor a Seer to look ahead into 2013 and know, almost beyond a doubt, that silver has its work cut out for the next several months, and one should be very careful when trading futures, while still buying the physical with impunity.

Conclusion We did not need to know of any "story" behind either precious metal. The charts are all-knowing, and they present everything known about the price, sans any opinion(s). Just deal with the facts and plan accordingly. Trust the markets. They never lie.

Related Articles: 1. 7 Indications That Gold & Silver Bearishness Most Likely Will Continue

2. Gold Probably Has One More Curve Ball to Throw Us Before Surging to New High

3. It's Time to Seriously Consider SHORTING Gold – Here's Why

4. Gold Watch: Several Factors Suggest That 2013 Will Be a Very Good Year

6. Goldrunner: Price Target of $10,000 to $12,000 for Gold Still Holds

| ||

| 75 Facts Revealed – How Is America Really Doing? Posted: 30 Dec 2012 09:55 AM PST An amazing list of real facts was published by The Economic Collapse Blog, entitled 75 Economic Numbers From 2012 That Are Almost Too Crazy To Believe. An excellent article that presents 75 facts & figures, based on research or surveys, indicating the real state of the US. Reviewing those facts and comparing them with the messages in the mainstream media and the government, we see such a huge disconnect. We selected what we consider "fundamental facts" based on the following themes: Social drama (increasing poverty)

(Un)employment deteroriating

Economy deteroriating

Inflation

What is the government doing about it? Obviously, for the government everything is running fine, as the talks of the day are about the fiscal cliff. Indeed, this is what the talks are about (chart courtesy Marketwatch.com). Their signal is clear. Looking at the time and effort they spend on the fiscal cliff debate they clearly consider it more important than all of the above issues.

Let's hope the real issues will be addressed voluntarily in 2013 and the years after. It will very sad if they need to be addressed because of force majeur. | ||

| Posted: 30 Dec 2012 09:48 AM PST I catch myself daydreaming, or thinking at night as I try to go to sleep "what will I do when they come for my guns". I only wish to protect myself from the hordes of people that will rob, steal and murder when their SNAP cards no longer work, and they can't get their direct deposit cash anymore. Hunger makes people do animalistic things, some even resort to cannibalism. That said, our nation's police are becoming more militarized every day. The government is giving them military equipment, and the military itself is training for "urban pacification". What will you do when they come for your guns? When they roll up in an armored personal carrier? Do you think it will happen?

When They Come For Your Guns, You Will Turn Them Over "When they come for my gun, they will have to pry it out of my cold, dead hands," is a common refrain I often hear from the Neo-Cons when there is a threat, credible or otherwise, that the US government is going to take their firearms. And, when I hear this crazy talk, I agree with them openly. "You are right. They will pry your gun from your cold dead hands," which I often follow with the question, "And where will that leave you except face down in a pool of your own blood [in] the middle of the street, just another dead fool resisting the State?" This is not a question they are comfortable with, if only because the intent of their saber-rattling was to imply they would fight to keep their weapons, and win. Nice fantasy. It's not happening. If the federal government decides to disarm the public, and when the increasingly-militarized rolls down your street after a not-so-subtle request that you kindly turn over your firearms and ammunition "for the common good," it will be nothing less than suicide by cop to do anything other than what you are told. The militarization of US police forces is ongoing and escalating. Many cities and towns now own tanks, armed personnel carriers, even attack helicopters, and almost all are outfitted with military weapons not available to the general public. And, it is not just your hometown cops who are getting new boy-toys. The military itself is buying up weaponry not just for use in the current or next scheduled war, but to deal with the likes of you, citizens who don't seem to understand that the Bill of Rights has been overruled, and that specifically includes, but is not limited to, the right to protest and engage in civil disobedience. Also ignored (as if it didn't even exist) is the Posse Comitatus Act of 1878 which generally bars the military from law enforcement activities within the United States. According to Public Intelligence: "…for the last two years, the President's Budget Submissions for the Department of Defense have included purchases of a significant amount of combat equipment, including armored vehicles, helicopters and even artillery, under an obscure section of the FY2008 National Defense Authorization Act (NDAA) for the purposes of 'homeland defense missions, domestic emergency responses, and providing military support to civil authorities.' Items purchased under the section include combat vehicles, tanks, helicopters, artillery, mortar systems, missiles, small arms and communications equipment. Justifications for the budget items indicate that many of the purchases are part of routine resupply and maintenance, yet in each case the procurement is cited as being 'necessary for use by the active and reserve components of the Armed Forces for homeland defense missions, domestic emergency responses, and providing military support to civil authorities' under section 1815 of the FY 2008 NDAA." And, they are not just arming cops and weekend warriors for domestic purposes. Active duty Marines are now being trained for law enforcement operations all over the world (of which the US remains a part) specifically to deal with civil uprisings, and the US government knows that civil uprisings are coming to a town near you just as soon as the fantasy of a healing economy is shattered, the US dollar fails, and unemployment goes to 30%+ in real numbers. And, to you tough-talking Neo-Cons with your AR-15 rifles and a few thousand rounds of ammo, here is the reality: they will take your guns, and no, all your Second Amendment bluster aside, you are not going to do anything about it. You are not going to take on a platoon of Marines with state-of-the-art automatic weapons and the best body armor you cannot buy protected by armed personnel carriers and attack helicopters unless you choose to die that day — for nothing. You will either be in the country or out, and if you are in, you will stay in and you will comply. That is your choice… for the moment. Regards, Jim Karger Read more: When They Come For Your Guns, You Will Turn Them Over http://dailyreckoning.com/when-they-come-for-your-guns-you-will-turn-them-over/#ixzz2GYHVqjBn

| ||

| Empires of Illusion and the Credibility Trap Posted: 30 Dec 2012 09:31 AM PST I came across a nice, compact interview with Chris Hedges which illuminates his thesis of the decline of the American Empire and the illusory thinking that accompanies it. Can the shock and meltdown of Karl Rove on election night be any better contemporary illustration of the power of selective thinking to delude a group of seemingly rational people to their own downfall? | ||

| Posted: 30 Dec 2012 09:16 AM PST Now here's the problem with trying to apply "rational" analysis of the news headlines in making gold price predictions: because the financial markets are by nature irrational and volatile, you can never know from one day to the next how the market will react to a certain piece of news or legislation. | ||

| Diplomatic cables disclose more conspiring by Western governments to rig gold market Posted: 30 Dec 2012 09:13 AM PST Two U.S. State Department diplomatic cables from 1974 obtained by GATA researcher R.M. show Western central bank and treasury officials engaged in secret discussions -- that is, conspiring -- to control the price of gold and prevent any increase in its recognition as money. | ||

| Macleod and von Greyerz give their financial outlooks for 2013 Posted: 30 Dec 2012 09:11 AM PST 11:07a ET Sunday, December 30, 2012 Dear Friend of GATA and Gold: GATA favorities Alasdair Macleod of GoldMoney and Swiss gold fund manager Egon von Greyerz are offering their outlooks for the world economy in 2013. Macleod's is posted at GoldMoney here: http://www.goldmoney.com/gold-research/alasdair-macleod/alasdair-macleod... Von Greyerz's comes in an interview with King World News that is excerpted here: http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2012/12/28_2... CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT Opinion Around the World Is Changing When Deutschebank calls gold "good money" and paper "bad money". ... http://www.gata.org/node/11765 When the president of the German central bank, the Bundesbank, pays tribute to gold as "a timeless classic". ... http://www.forbes.com/sites/ralphbenko/2012/09/24/signs-of-the-gold-stan... When a leading member of the policy committee of the People's Bank of China calls the gold standard "an excellent monetary system". ... http://www.forbes.com/sites/ralphbenko/2012/10/01/signs-of-the-gold-stan... When a CNN reporter writes in The China Post that the "gold commission" plank in the 2012 Republican platform will "reverberate around the world". ... http://www.thegoldstandardnow.org/key-blogs/1563-china-post-the-gop-gold... When the Subcommittee on Domestic Monetary Policy of the U.S. House of Representatives twice called on economist, historian, and gold standard advocate Lewis E. Lehrman to testify. ... World opinion is changing in favor of gold. How can you learn why and what it will mean to you? Read the newly updated and expanded edition of Lehrman's book, "The True Gold Standard." Financial journalist James Grant says of "The True Gold Standard": "If you have ever wondered how the world can get from here to there -- from the chaos of depreciating paper to a convertible currency worthy of our children and our grandchildren -- wonder no more. The answer, brilliantly expounded, is between these covers. America has long needed a modern Alexander Hamilton. In Lewis E. Lehrman she has finally found him." To buy a copy of "The True Gold Standard," please visit: http://www.thegoldstandardnow.com/publications/the-true-gold-standard Join GATA here: Vancouver Resource Investment Conference * * * Support GATA by purchasing DVDs of our London conference in August 2011 or our Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: ADVERTISEMENT Fred Goldstein and Tim Murphy open All Pro Gold Longtime GATA supporters Fred Goldstein and Tim Murphy have brought their many years of experience in the precious metals and numismatic coins to All Pro Gold as metals brokers who specialize in the delivery of gold and silver bullion bars and coins as well as numismatic gold and silver coins. Fred and Tim follow these markets closely and are assisted by a team of consultants in monitoring market trends. All Pro Gold offers GATA supporters competitive pricing on all bullion products and welcomes inquiries. Tim can be reached at 602-299-2585 and Tim@allprogold.com, Fred at 602-799-8378 and Fred@allprogold.com. Ask about their ratio strategy and the relationship of generic $20 dollar gold pieces to 1-ounce gold bullion coins. Visit their Internet site at http://www.allprogold.com/. | ||

| Japan lashes out over depreciating dollar and euro Posted: 30 Dec 2012 08:49 AM PST By Takashi Nakamichi and Eleanor Warnock http://online.wsj.com/article/SB1000142412788732353040457820744047487460... TOKYO -- Japan's new finance minister upped the ante in the country's war of words against the strong yen, lashing out at the U.S. and Europe for letting their currencies weaken dramatically and calling on the U.S. to strengthen the dollar. The tirade from Taro Aso, Prime Minister Shinzo Abe's point person on currency strategy, underscores the increasingly pugnacious stance of the fledgling Abe government against what it sees as a global trend of currency devaluations. Mr. Abe made weakening an unduly strong yen a plank in his party's campaign during national elections, which he won resoundingly in mid December. The strong, explicit rhetoric on yen levels from Mr. Abe and his deputies have sparked worries recently that Japan could be fanning the flames of a global currency war. ... Dispatch continues below ... ADVERTISEMENT Fred Goldstein and Tim Murphy open All Pro Gold All-Pro Gold, run by long-time GATA supporters Fred Goldstein and Tim Murphy, offers its services to GATA supporters and anyone else interested in precious metals. The company brokers a full line of precious metals and numismatic coins. It aims to inform prospective clients about the importance of the monetary metals as part of a diversified financial portfolio and to keep prospective clients current with market trends. All-Pro Gold has competitive pricing and ships promptly to clients so they may have physical possession. Learn more by e-mailing Fred@allprogold.com or Tim@allprogold.com or telephone 1-855-377-4653 or visit www.allprogold.com. But Mr. Aso's words also highlight the deep frustration felt by many in Japan over the erosion of the country's global competitiveness from years of strong yen. "The U.S. ought to do its job and make the dollar strong. And what about the euro?" Mr. Aso said Friday, during his first set of press interviews after taking office. Mr. Aso said that the yen's value had risen sharply versus both currencies since a Group of 20 meeting of major economies three years ago in which countries made a promise not to resort to competitive currency devaluations. "But tell me how many countries in the G-20 have stuck to that promise," Mr. Aso said. "We're the only ones doing things properly. Foreign countries are in no position to lecture us." Mr. Aso also told reporters later that he conveyed his thoughts about the yen in a 30-minute phone call to U.S. Treasury Secretary Timothy Geithner, in which "I told him that there is no doubt that the yen's excessive, one-sided rally in the recent past is gradually being corrected. But I also said there is a good possibility that this situation could change again so we will keep a close watch" on the yen. Treasury spokeswoman Natalie Wyeth Earnest said Secretary Geithner and Minister Aso spoke by phone Fiday morning, and discussed "the U.S.-Japan economic relationship as well as global economic and financial developments." Mr. Aso isn't alone in airing exasperation at the level of the currency in recent years. A procession of Japanese executives and politicians have bemoaned the yen's strength, blaming it for a loss of competitiveness, dwindling earnings, bankruptcies, and the relocation of operations abroad. Since the global financial crisis of the late 2000s, the dollar has fallen 30% to around Y86, putting considerable stress on Japanese exporters, whose products become less competitive overseas when their home currency rises. Much of the dollar decline happened during Mr. Aso's tenure as the country's prime minister, which lasted a year until Sept. 2009, and was partly blamed for the severe recession Japan experienced then. According to market researcher Teikoku Databank, at least 51 companies went bankrupt in the first half of 2012 due to exchange rate-related issues, and their total debt -- one indication of the size of their operations -- was almost twice that for similar bankruptcies during the preceding four years. Japanese car makers have been some of the most vocal in calling for relief as yen strength dents profits. Nissan Motor Co., for instance, has said that every Y1 of appreciation against the dollar translates into Y20 billion ($208 million) cuts in the company's operating profit annually. "The one major obstacle to competitiveness is the exchange rate," said Nissan and Renault chief executive Carlos Ghosn, at a Tokyo forum on corporate management two months ago. "I don't think we are getting enough effort behind this. Many countries are bringing their currency to neutral territory. I'm not asking for incentives here; I'm just asking to bring the yen to neutral territory, allowing companies to do their job. ... I am facing Korean competitors in the Middle East. I can't compete." Mr. Ghosn has in the past said that he'd like to see the currency around Y100 to the dollar. The dollar has recently staged a sharp recovery, as Mr. Abe's pledge to strong-arm the Bank of Japan into easing monetary policy to weaken the yen has driven investors to sell off the yen. While that has cheered Japan's struggling exporters, Mr. Abe's drive toward a weaker currency has also raised concerns abroad that it could risk triggering a devastating global race to undercut currencies to protect export competitiveness. Mr. Aso brushed aside the concerns as misplaced. "We are not radically weakening the yen or anything like that," he said. "We still haven't taken any policies." While the previous government under the Democratic Party of Japan intervened in the market to rein in the yen's strength, inviting sharp criticism from Washington, when Mr. Aso was prime minister, the government stayed away from the market. Mr. Aso also acknowledged that a weak yen isn't without disadvantages. "The only people who are celebrating seeing the currency weaken are the exporters," he said. "For importers, if the currency were to weaken, it's a problem." Join GATA here: Vancouver Resource Investment Conference * * * Support GATA by purchasing DVDs of our London conference in August 2011 or our Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: ADVERTISEMENT Opinion Around the World Is Changing When Deutschebank calls gold "good money" and paper "bad money". ... http://www.gata.org/node/11765 When the president of the German central bank, the Bundesbank, pays tribute to gold as "a timeless classic". ... http://www.forbes.com/sites/ralphbenko/2012/09/24/signs-of-the-gold-stan... When a leading member of the policy committee of the People's Bank of China calls the gold standard "an excellent monetary system". ... http://www.forbes.com/sites/ralphbenko/2012/10/01/signs-of-the-gold-stan... When a CNN reporter writes in The China Post that the "gold commission" plank in the 2012 Republican platform will "reverberate around the world". ... http://www.thegoldstandardnow.org/key-blogs/1563-china-post-the-gop-gold... When the Subcommittee on Domestic Monetary Policy of the U.S. House of Representatives twice called on economist, historian, and gold standard advocate Lewis E. Lehrman to testify. ... World opinion is changing in favor of gold. How can you learn why and what it will mean to you? Read the newly updated and expanded edition of Lehrman's book, "The True Gold Standard." Financial journalist James Grant says of "The True Gold Standard": "If you have ever wondered how the world can get from here to there -- from the chaos of depreciating paper to a convertible currency worthy of our children and our grandchildren -- wonder no more. The answer, brilliantly expounded, is between these covers. America has long needed a modern Alexander Hamilton. In Lewis E. Lehrman she has finally found him." To buy a copy of "The True Gold Standard," please visit: http://www.thegoldstandardnow.com/publications/the-true-gold-standard | ||

| India Is Behind the Weak Price of Gold – Here's Why Posted: 30 Dec 2012 08:21 AM PST "Follow the munKNEE" via twitter & Facebook Gold just can't seem to get any traction any more. The Feds announce So writes the Macro Investor in edited excerpts from his post* on Seeking Alpha entitled Gold Cannot Seem To Make A Move Even With Fiscal Cliff.

The article goes on to say, in part: [The chart below shows]…how the yellow metal and the miners have done in the past month. Both are down about 4%. In the meantime, the S&P is up about 1.4%. …I keep seeing articles stating that 2013 will be the year for gold but, unfortunately, Indian gold merchants disagree. India, just for the record, is the world's largest consumer of gold. If the Indian gold merchants expect prices to be flat, then probably it is going to be flat. These guys know well where the demand (or lack thereof) is. Reports the Economic Times:

Gold prices in the capital fell by Rs 220 to Rs 31,000 per 10 grams on Wednesday, so there we have it. Gold per 10 grams to go up nominally by at most ~3%, from Rs 31,000 to Rs 32,000, with a good chance of falling by ~6% to Rs 29,000 as well. This, mind you, is a nominal price increase. Inflation in India runs at around 8% per year, so whichever way you cut it, investors in India are expecting a drop in the price of gold in real terms. [An expected drop in the price of gold] is not surprising, as the Indian government has been trying its level best to curb gold consumption by Indians [as I discussed in a previous posting** on Seeking Alpha entitled Can Gold Survive Lack Of Demand In India? in which I said the following:

Jewelers are expecting higher sales during the Pongal festival but Reuters reports that retail demand remains weak….and the culprit, according to Wall Street Journal reports… is that investors eye stronger gains from equities. Here is the trouble:

With the economy forecast to do better in 2013, equities will likely boom, and smart Indian investors are making the bet. Conclusion Given the above, I continue to urge caution to gold investors…. I believe both physical gold and gold mining stocks will continue to struggle in 2013 as Indians turn away from gold. However, I also know how the gold market goes – it is not in any way based on fundamentals, it is all about sentiment – so I am not about to short gold, but I must say I am sorely tempted. That said, I believe gold investors can still make upwards of 50% this year. I explained that in my article Make a 153-174% Return – With 95% Confidence – IF Gold Goes Up Just 10% in 2013! Here's How [and silver investors too - Read: If You Think Silver Is Going To Increase In 2013 Here's How to Best Maximize Your Return]. Happy investing.

*http://seekingalpha.com/article/1085551-gold-cannot-seem-to-make-a-move-even-with-fiscal-cliff **http://seekingalpha.com/article/1065141-can-gold-survive-lack-of-demand-in-india Related Articles: 1. Make a 153-174% Return – With 95% Confidence – IF Gold Goes Up Just 10% in 2013! Here's How

2. If You Think Silver Is Going To Increase In 2013 Here's How to Best Maximize Your Return

3. What's Going On With Gold & Silver?

4. The Reason Gold Has Been Declining Is Simply This…

5. Goldbugs, Here's Why Gold's Long Bull Run Could Be Over

6. Is Gold's 13 Year Run Almost Over?

8. It's Time to Seriously Consider SHORTING Gold – Here's Why

9. 7 Indications That Gold & Silver Bearishness Most Likely Will Continue

| ||

| Gold & Silver: Opposing Forces Very Under-Rated Posted: 30 Dec 2012 07:52 AM PST It is impossible not to read some source, informed or otherwise, touting the "fact" that the price of gold and silver will be [insert whatever amount you wish, here], "in the coming months", or safer, "in the next year or two," etc. Yet, the market does not echo those almost universally held sentiments. Why not? Because that is exactly what they are, sentiments. When it comes to sentiments or opinions, regardless of how close to source or how well reasoned, the market does not care. One of the better "resolutions" one can make going into 2013 and beyond it to follow the market's lead, stop trying to lead it, waiting for it to catch up to your trading acumen. But what about the shortages in silver production v demand? What about the overly re-re-hypothecated gold leases from central banks that cannot possibly cover actual demands for gold? What about the possibility that all of Germany's [and other countries?] gold is gone and so much of it is being transferred to the East? What about [insert whatever issue you wish discussed, here]? Yes, well what about it! That information is and has been known for quite some time, so it is already "priced into the market." It does not matter how well-informed your source[s] is. It does not matter how accurate the figures are for available supply v demand. The market is all knowing, and it is ahead of you, and it is responding to forces about which you are not aware, hidden deals, as an example. It does not matter how much gold there is, or isn't. It does not matter where the gold is, or isn't, the market is telling you what you all you need to know. Everything finds its way into the market, and if you would just ignore all else and follow the ultimate known fact, that being the current price of anything, then you have the answer right in front of you. The problem is, too many cannot reconcile the current price of gold and silver relative to their expectations. [From the buy side.] John Keats would have made an excellent technical analyst, for he excelled at drawing out the paradoxical nature of things, leaving us with a few of his most famous lines that apply to the above:

This is how we see charts. Everything you need to know is contained within them because they are based on truth. What truth? The ultimate decisions to buy or sell made by the collective forces of the marketplace. Anything else that does not get translated directly in the market is simply an opinion, of no factual value because the market only recognizes actual transactions. That is the truth and the beauty of the markets. They provide you factual commitments, unadorned by uncommitted interpretive opinions. That is all you need to know on earth. Learn to listen to what the market is saying, and not what others are saying about the market. This is not to say that markets cannot be manipulated and factors grossly distorted, for even if they are, those manipulation and distortions are what is reflected in current prices, like it or not. Most who speculate in the markets, to the extent they rely upon charts, look at daily or intra day time frames. Smart money, what we call the "controlling forces" of a market, use higher time frames, for they are not concerned with day-to-day activity. Their positions and influence necessitate that they move over a more extended period of time, and one can get a greater sense of their intent from the higher time frames. When we talk about collective forces of the marketplace, it includes the most well-informed insiders, central bankers, the largest dealers, with availability to information and research outsiders may never know or learn about, until after the fact, all the way down to investors, fundamentalists, speculators, even the ephemeral day-traders. What they all have in common is that they are the market, once they make a decision to execute a buy/sell that influences and determines the price at any given point in time. Those executed decisions, regardless of how well or ill-informed, become market facts that comprise fluctuations, and they show up as the high, low, and close on a chart for any chosen time frame. Despite the relentless calls for gold and silver "taking off," which they have not, of late, the elephants in the room, governments, central bankers and major brokers, plus exchanges, have been vastly under-rated in their ability to keep the prices of gold and silver suppressed as much as they have. They are not about to throw in the towel and give up their Wizard of Oz controls. Ultimately, they are doomed to fail, but when does "ultimately" kick in, and to what degree of damage before it does, remains unknown? One thing you should know about the opposition, in whatever form it is in, ultimately: It will not stop. It will not quit. It will destroy everything that gets into its way in order to suit its needs. The charts have been saying as much. The annual and quarterly charts had to be scanned because most services do not provide any beyond the monthly time frame. The comments on the charts may be hard to read, so we will put them in italics to make it easier. If gold and silver are going to go to such high price levels, why are charts saying the opposite? This end of year's gold closing, actually Monday, is about mid-range the bar, a draw between the forces of supply and demand, but the range was the smallest in several years. Neither buyers nor sellers were able to extend the range further in either direction. Chart comments: This year's close is higher, but the entire range is within last year's. The bar is one of the smallest annual ranges in five years, and the close is just under the half-bar area. The conclusion would be neutral to just a touch negative. The quarterly chart may reveal more. The arrow in the chart points to the smallest range in Qtr 2, 2012. It was an attempt to go lower that failed. The fact, and keep in mind the focus is on the indisputable facts contained in the charts, that price did not go lower speaks to strong support at that level. Another observable fact is how the last 5 quarterly bars have been overlapping. Anytime you see bars overlapping, it show a struggle between buyers and sellers trying to exert control. The poor end of the year close for gold says buyers have not been keeping an upper hand, and sellers are maintaining relentless pressure. Chart comments: Comments under the trading range cover expectations going into 2013. The one positive Qtr was 2nd, 2012, when price tried to go lower but held, and the close was mid-range the bar, a win for buyers with price higher ever since. Last 5 Qtrs are within range of 3rd Qtr 2011, and the last 4 Qtrs within 4th Q 2011. Low-end close for 2012 says sellers in control. Expect more price range activity going into 2013+. Pie-in-the-sky prices are not in the picture, for now. A retest of 1520+ area possible. Back to our normal chart. If we view the rally in August as a breakout from a right triangle pattern, it is taking now 3 months to correct a 2 month rally, and the bars correcting are smaller, telling us there is no downward ease of movement. This suggests sellers are meeting more resistance, but still prevailing. 2013 will be an interesting year, and its start could be signaling more of what we have seen for the past 15 months. While accumulation of the physical metal is strongly recommended, trading in the paper futures will have to be much more select, buying breaks, not breakouts. There is no question that silver remains relatively weaker to gold, as the charts clearly show. Some think silver may outperform gold, moving forward, and it has, on occasion. That is an opinion that may or may not hold true. Buying and personally holding the physical is strongly recommended, as was stated for gold. For now, silver has a very large supply factor hanging over future progress, based upon the closes of 2011 and 2012. Chart comments: 2011 silver close was bottom-end on very high volume. This single bar shouts out sellers were totally in control, and everything above the close is where buyers have In 2012, the range attempt to go higher was small, and another low end close shows how buyers are failing to overcome sellers, a problem for longs. The more detailed Qtrly chart has one positive aspect: 26.20+ area held like a rock. We could see yet another test and possible new low. That is not a prediction but a point of view not to be dismissed for the year ahead. As with gold, the overlapping of bars shows the struggle between the forces of sellers and buyers, the edge with sellers. Chart comments: The Qtrly chart is more of a mixed message. There is obviously strong support at the 26 area, and bullish spacing remains a positive. [Bullish spacing is where the current The fact that silver cannot get and stay above 35 says how much work there is to overcome sellers. 2013 should be more of the same, at least for the first half. As with gold, an unusually large bar most often foretells of a protracted trading range to follow. Not only did that hold true for silver, the trading range was all under a 50% It does not take a crystal ball, nor a Seer to look ahead into 2013 and know, almost beyond a doubt that silver has its work cut out for the next several months, and one should be very careful when trading futures, while still buying the physical with impunity. We did not need to know of any "story" behind either precious metal. The charts are all-knowing, and they present everything known about the price, sans any opinion[s].

| ||

| GoldMoney article: Outlook for 2013 Posted: 30 Dec 2012 03:46 AM PST The following article has today been posted at GoldMoney, here. Alasdair Macleod's Outlook for 2013 2012-DEC-30