Gold World News Flash |

- All the Gold In the World

- CNN Freaks Out Over Alex Jones, Roger Stone Plan to Assemble at Republican National Convention

- ZERO BANKERS JAILED – New Orleans Man Faces 20 Years for Stealing $30 in Candy

- World Economy Is Terminally Broken After 50 Years Of Misgovernment

- The Fed’s Policy Nightmare: How to Raise Rates Without Killing the Big Banks

- Crushing Myths and Building a New Case for Gold

- THE NEW CASE FOR GOLD – James Rickards

- 19 Facts That Prove Things In America Are Worse Than They Were Six Months Ago

- Asia's Largest Clothing Retailer Plummets After Slashing Guidance By A Third; Blames Strong Yen

- 20 Lies Every American Should Know...

- If Gold Price Drives Through that Wall at $1,240, it has a Chance to Push Through $1,308 this Time

- "It's Probably Nothing": Truck Orders Plunge 37% As Unsold Inventories Soar Most Since 2007

- How You're Controlled By TV

- Gerlad Celente -- If You Like Trump , You Love Hitler

- The 6 Secrets THEY Don’t Want You to Know

- Where Have All Your Tax Dollars Gone????

- Silver Price Forecast: The Interesting Relationship Between Silver Rallies and Interest Rates

- Japan and the Secret Shanghai Accord

- Why Gold is the Ultimate Hedge Against Hackers

- The New Case For Gold

- Americans spending more on taxes than food?

- THE END OF ALL THINGS IS AT HAND

- Wikileaks: ‘Panama Papers’ funded by US against Russian president

- The “Great Oil Divergence of 2016” Could Be Near

- FOMC Meeting Minutes Reveal Fed’s Dovish Nature

- BREAKING: Hillary Clinton "Bombshell" Fed Courts Rule On Benghazi Investigation"

- Student Loans the next bailout?

- Alasdair Macleod: Gold and interest rates

- 'Silk Road' Gold Demand

- The Interesting Relationship Between Silver Rallies and Interest Rates

- Surprise! A Gold Bear at Goldman Sachs

- Gold Ratio Charts Revisited

- Gold Once Again Proves To Be The Best Defense Strategy

| Posted: 08 Apr 2016 12:30 AM PDT from Junius Maltby: | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| CNN Freaks Out Over Alex Jones, Roger Stone Plan to Assemble at Republican National Convention Posted: 07 Apr 2016 11:30 PM PDT from Infowars:

"We will have demonstrations at specific hotels where there are delegates so we can let them visually see the will of the people," Stone says in a clip aired by Don Lemon. "We will have a daily protest. We will man the ramparts every day," Stone says, clarifying he is calling for peaceful, non-violent demonstrations. "That sounds slightly ominous. Is that the way you want the delegates counted?" Lemon asks CNN contributor Kayleigh McEnany and Blaze editor and former CIA intelligence officer Buck Sexton, who proceeded to launch an attack on Jones. "Some of these rules can be changed very close to the actual convention," Sexton says in response. "And I'll just point out – Alex Jones aside, who is really a conspiracy theorist, I think putting him on the right is rough for those of us who are conservatives – but nonetheless the rules in place say that either Cruz or Trump will be the Republican nominee." "If you don't give one of those candidates the GOP nomination there will be a nuclear meltdown within the entire conservative movement, the entire right wing," Sexton predicts. The media's coverage of Stone's plan for demonstrations to "stop the steal" suggests the establishment is terrified by the thought of Trump supporters showing up to influence Republican delegates. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| ZERO BANKERS JAILED – New Orleans Man Faces 20 Years for Stealing $30 in Candy Posted: 07 Apr 2016 10:01 PM PDT from RT: Jacobia Grimes, an African American male from Louisiana, was just caught shoplifting about thirty dollars worth of candy bars at a Dollar General Store. Because he was caught shoplifting before, from places like Rite-Aid and Blockbuster Video – always for less than 500 dollars worth of items – the District Attorney in the case has decided to charge Grimes with felony theft. And now, he is facing 20 years to life behind bars. Twenty years of his life, for some candy. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| World Economy Is Terminally Broken After 50 Years Of Misgovernment Posted: 07 Apr 2016 09:40 PM PDT by Egon von Greyerz, Gold Switzerland:

50 years' experience and the biggest dangers are still lurking Some of us understand the risks very clearly but the world at large just sees our message as prophecies of doom. For most people the debt explosion and the excesses are just normalcy and they believe that this will go on for ever. Little do they understand the risks and the need for taking steps to insure against these risks. And the risks are at many different levels, social, financial, economic, geopolitical including war and social unrest. There is some advantage in having almost half a century of active business life. The school of life and personal experiences can never be learned from books. As a young banker in Geneva I remember the mining boom in Australia in the late 1960s. The nickel miner Poseidon for example went from $0.80 to $270 within a year. At that time, it was valued at three times Australia's biggest bank. The stock quickly crashed and the company went bankrupt. We were fortunate to have Adolf Lundin as adviser on resource stocks. He spent a lot of his time in Australis at that time. Adolf is the deceased founder of the very successful Lundin Group. The 1970s was of course also extremely exciting for gold and silver investors with gold going from $35 to $850. In the next few years, we are likely to see much bigger moves in the metals with gold reaching in excess of $10,000 in today's money. The global problems today are immensely greater than in the 1970s. Oil embargo, miners' strike, 3-day week and stock market collapse I came to the UK in the early 1970s and experienced the Opec oil embargo in 1973. Within a year oil had gone from $3 to $12 with devastating effects for the UK and world economy. I was finance director at Dixons that we over time built to the UKs biggest electronic retailer and a FTSE 100 company. But the journey was certainly not without major setbacks. Interest rates surged and in 1974 I paid 21% interest on my mortgage. Today, in most countries nobody could afford a 5% interest rate. And as they climb to 15% or 20% which I am convinced they will, nobody will be able to afford the interest of course. By nobody I mean both individuals, corporates and sovereign states. Stock markets worldwide also collapsed in 1973-4. The FT index declined by over 60% and the Dow by nearer 50%. I had my first options in the company at 130 pence and the stock went down to 9 pence. Dixons was always profitable and had no debt problems. It was a good lesson in what can happen to stock prices even in strong companies. We also had a coal miners' strike in the UK which led to major nationwide electricity cuts. Our shops only had electricity for 3 days a week. The other days we sold TVs and radios in candle light. There was also a dustman/garbage collector strike. London was full of rubbish everywhere in the streets. We also had serious IRA bombings in London and all over the UK. Thatcher and Reagan rode the wave Eventually things improved and the cycle turned. Thatcher and Reagan were lucky to become leaders at the right time and could ride the new up cycle. I am quite cynical when it comes to leaders. I think they are instruments of their time. They are not the ones who bring about change but they are the right people to implement changes that were meant to happen due to the turn in the cycle. Clearly Thatcher and Reagan were excellent leaders to execute the changes that the cycle brought about. And so in the 1980s, the boom started with bull markets in everything from stocks, property, bonds and also in credit expansion and money printing. Financial market regulations were lifted in many Western countries and this started the major international expansion of US investment banks into worldwide dominance and their current oligopoly position. It also led to the massive build-up of financial weapons of mass destruction called derivatives. We had some serious setbacks in bubble asset markets in 1987 and 2000 but the just gave extra incentives to governments and central banks to flood markets with more credit and printed money. Everybody loved Greenspan although no one ever understood what he said. But that didn't matter because his financial shenanigans made stocks and property boom. And when Bernanke took over, everybody admired his ability to more than double US debt from $8 trillion to $17 trillion, especially since he did it in 8 years only. It had taken the US over 200 years to go from zero debt to $8T but Bernanke managed to more than double US debt in just 8 years. I am sure that this record won't last for long. Yellen and her successor will need to print much, much more to save the US and world economy. I don't think $100s of trillions will be enough but more likely quadrillions. And however much they print, it won't have any effect this time whatever Krugman and the Keynesians say. It is just not possible to solve a problem with the same means that created it in the first place. Currency debasement, manipulation and repression will lead to defaults Retuning to my 50 years' professional experience, I have been lucky to live in an era of peace and economic prosperity. But gradually since the gold backing of the dollar was abolished in 1971, real economic growth based on hard work, savings and investment has been replaced by currency debasement, credit expansion, money printing and financial manipulation or repression. And what is absolutely certain is that the unsound economic climate that we currently have cannot last. It is not a question of IF only of WHEN it will end. Of that I am 100% certain. The massive build-up of debt since the 2006-9 crisis is a futile and desperate attempt to put Humpty Dumpty back together again. But sadly the world cannot be put back together this time. If we scratch under the surface, we find a plethora of insoluble problems on every continent and in every country whether it is exponential debt explosion in Japan or China or a bankrupt EU with the added problem of the migrant crisis. Most emerging markets are on the verge of collapse as commodity prices are collapsing and China's expansion has stopped. But the biggest problem is of course the US. This is a country that has lived above its means for over 50 years. Since 1960 the US has not had a real budget surplus. Debts, including unfunded liabilities, are $230 trillion and to that we can add a worthless derivative position of at least $400-$600 trillion. This guarantees that the US will default at some point not too far away and that the dollar will sink into the ocean. I know that the US government and media are telling everyone that the US is in excellent shape. Unemployment is at 5% and the stock market is near the high. Thanks to manipulated figures and total apathy of the media no one is interested in the real figures or the truth. I know that the US government and media are telling everyone that the US is in excellent shape. Unemployment is at 5% and the stock market is near the high. Thanks to manipulated figures and total apathy of the media no one is interested in the real figures or the truth. Let me just take a few examples like US median real earnings being at the same level as in the 1970s. Real unemployment is not 5% but 23%. And S&P GAAP earnings are down 25% from the peak. If we take real S&P earnings and adjust for share buybacks, they are down 30%. But nobody looks at the real figures. Whatever the Government or Wall Street reports is accepted as the truth without any critical analysis. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Fed’s Policy Nightmare: How to Raise Rates Without Killing the Big Banks Posted: 07 Apr 2016 08:20 PM PDT by Pam Martens and Russ Martens, Wall Street On Parade:

The following then happened in short order in 2016: By Friday, January 15, Citigroup closed down on the day a gut-churning 6.41 percent, bringing its share price losses to a whopping 30 percent from its July 2015 high. Citigroup had been the largest recipient of bailout funds from the government in 2008 as well as the largest bank bailout in the history of finance, receiving $45 billion in equity infusions, over $300 billion in asset guarantees, and more than $2 trillion cumulatively in secret loans from the Fed. It could ill afford to be bleeding off its equity capital as banking regulators were attempting to convince the public that they had fixed the too-big-to-fail problem. By the close of trading on January 18, Morgan Stanley had lost 37 percent in share value from its July high; Goldman Sachs had lost 29 percent since the prior June; Bank of America was down 22 percent from July with JPMorgan Chase down by 19 percent in the same period. By January 20, a mere 35 days from the Fed's quarter point rate hike and promise of more to come, the U.S. domestic crude, West Texas Intermediate, was trading at a new 12-year low of under $28 a barrel; globally, stocks had lost $15 trillion since the prior May; the 10-year Treasury note which had closed at a yield of 2.29 percent when the Fed announced its rate hike and plan to begin gradually normalizing rates back up, had gone rogue from the Fed and moved in the opposite direction. Instead of moving up in yield, the benchmark 10-year Treasury was trading on January 20 at a yield of 1.97 percent. (This morning it's at 1.74 percent.) On that same day, January 20, Howard Silverblatt, the Standard and Poor's Dow Jones Indices Senior Index Analyst, tweeted that as of 10:30 a.m. that morning, the Dow Jones Industrial Average's loss of 10.03 percent year-to-date was the worst ever start to a new year since 1897. By the close of trading on January 27, Citigroup, Bank of America, JPMorgan Chase, Morgan Stanley and Goldman Sachs had cumulatively lost a total of $219.7 billion in market capitalization over the prior seven months as the Obama administration was attempting to convince the public that the banks had become so much stronger as a result of his Dodd-Frank financial reform. The declines in market cap were as follows: Citigroup, down $60.74 billion; Bank of America, down $53.3 billion; JPMorgan Chase, down $47.7 billion; Morgan Stanley, down $30.3 billion; and Goldman Sachs, a decline of $27.7 billion. On February 3, four of the mega Wall Street banks traded at their 12-month lows during the trading day. Those four were also among the top five holders of derivatives: Bank of America, Citigroup, Goldman Sachs and Morgan Stanley. Since the Fed began backing off its narrative of more imminent rate hikes, the Wall Street banks have recovered a little of their lost ground but are still dramatically below their 2015 highs. The Fed now finds itself in the following nightmare policy scenario. It desperately needs to reload its monetary policy bazooka by getting its benchmark rate to a level where it could actually effectuate an easing policy in the next recession or financial crash. But corporate earnings are now in serious decline and even quarter point rate hikes spawn both a perception and the real impact of tightening. On April 1, FactSet reported that earnings declines in the S&P 500 for the first quarter of this year are estimated to be a negative 8.5 percent, noting that if there is another decline this past quarter, it would "mark the first time the index has seen four consecutive quarters of year-over-year declines in earnings" since the financial crisis in the fourth quarter of 2008 through the third quarter of 2009." (Lately, comparisons to 2008 and 2009 have been popping up like crocuses in spring.) What played out in the second half of last year and earlier this year is that the Fed's incessant talk of coming rate hikes sent the price of the U.S. dollar up and crude oil prices skidding. The market perceives the ability of the Fed to raise rates as a signal that the U.S. economy is improving, which means the U.S. dollar will strengthen further as foreign money seeks a U.S. haven for higher rates of return without worry of losses when that foreign money wants to convert back into its own currency. Unfortunately, a higher U.S. dollar negatively impacts the price of oil which is priced in U.S. dollars, as the market perceives that foreign currencies that are declining against the dollar will be able to afford less oil purchases. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Crushing Myths and Building a New Case for Gold Posted: 07 Apr 2016 08:00 PM PDT from SchiffGold: Crushing Myths and Building a New Case for Gold: Peter Schiff's Gold Videocast with Albert K Lu. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| THE NEW CASE FOR GOLD – James Rickards Posted: 07 Apr 2016 07:20 PM PDT from Financial Repression Authority: Sorry for the audio quality. Jim had a new microphone for this offsite interview. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 19 Facts That Prove Things In America Are Worse Than They Were Six Months Ago Posted: 07 Apr 2016 06:20 PM PDT While we all very capable of discerning the 'recovery' facts from the peddled recovery fiction throughout President Obama's reign...

...a close up over the last six months suggests things are getting worse in a hurry. As The Economic Collapse blog's Michael Snyder details, while most people seem to think that since the stock market has rebounded significantly in recent weeks that everything must be okay, that is not true at all.

With all that being said, the following are 19 facts that prove things in America are worse than they were six months ago… #1 U.S. factory orders have now declined on a year over year basis for 16 months in a row. As Zero Hedge has noted, in the post-World War II era this has never happened outside of a recession…

#2 Factory orders have now reached the lowest level that we have seen since the summer of 2011. #3 It is being projected that corporate earnings will be down 8.5 percent for the first quarter of 2016 compared to one year ago. This will be the fourth quarter in a row that we have seen year over year declines, and the last time that happened was during the last recession. #4 Total business sales have fallen 5 percent since the peak in mid-2014. #5 S&P 500 earnings have now fallen a total of 18.5 percent from their peak in late 2014. #6 Corporate debt defaults have soared to the highest level that we have seen since 2009. #7 The average rating on U.S. corporate debt has fallen to “BB”, which is lower than it has been at any point since the last financial crisis. #8 The U.S. oil rig count just hit a 41 year low. #9 51 oil and gas drillers in North America have filed for bankruptcy since the beginning of last year, and according to CNN we could be on the verge of seeing the biggest one yet…

#10 According to Challenger, Gray & Christmas, job cut announcements by major firms in the United States were up 32 percent during the first quarter of 2016 compared to the first quarter of 2015. #11 Consumers in the United States accumulated more new credit card debt during the 4th quarter of 2015 than they did during the entire years of 2009, 2010 and 2011 combined. #12 Existing home sales in the U.S. were down 7.1 percent during the month of February, and this was the biggest decline that we have witnessed in six years. #13 Subprime auto loan delinquencies have hit their highest level since the last recession. #14 The Restaurant Performance Index in the U.S. recently dropped to the lowest level that we have seen since 2008. #15 Major retailers all over the country are shutting down hundreds of stores as the “retail apocalypse” accelerates. #16 If you take the number of working age Americans that are officially unemployed (8.1 million) and add that number to the number of working age Americans that are considered to be “not in the labor force” (93.9 million), that gives us a grand total of 102 million working age Americans that do not have a job right now #17 Since peaking during the 3rd quarter of 2014, U.S. exports of goods and services have been steadily declining. This is something that we never see outside of a recession…

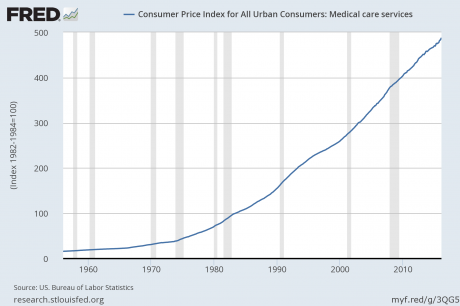

#18 The cost of everything related to medical care just continues to skyrocket even though our wages are stagnating. According to the Social Security Administration, 51 percent of all American workers make less than $30,000 a year, and yet the cost of medical care just hit a brand new all-time high…

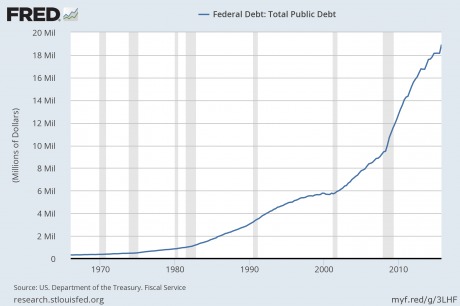

#19 Our government debt continues to spiral out of control. At this point it is sitting at a staggering total of $19,218,516,838,306.52, but when Barack Obama first entered the White House it was only 10.6 trillion dollars. That means that our government has been stealing an average of more than 100 million dollars an hour from future generations of Americans every single hour of every single day since Barack Obama was inaugurated…

How in the world can anyone look at those numbers and suggest that everything is okay? I simply do not understand how that could be possible. Part of the problem is that Americans have been trained to be irrationally optimistic. It is fine to have an optimistic outlook on life, but when it causes you to throw logic and reason out the window that is not good. For example, you can be “optimistic” about your ability to fly all you want, but if you step off a 10 story building you are going to take a very hard fall to the ground. Similarly, you can ignore all of the facts and pretend that our economic prosperity is sustainable all you want, but it won’t change the fundamental laws of economics. Who is to blame for all this disappointment? Simple...

Finally, don't forget, "There are no signs of a US recession anytime soon"... apart from these nine charts that is...

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Asia's Largest Clothing Retailer Plummets After Slashing Guidance By A Third; Blames Strong Yen Posted: 07 Apr 2016 06:14 PM PDT It didn't take long for the impact of the stronger yen, and the weak global economy, to manifest themselves on the company that is Asia largest clothing retailer. Moments ago, shares of Japan's clothing empire Fast Retailing, whose most prominent brand is Uniqlo, plunged by 10% sending its stock price to the lowest since June 2013, after the company cut its profit forecast made just four months ago by a third from JPY180 billion to JPY120 billion (well below the JPY169 consensus) a five year low, saying a stronger yen eroded the value of overseas sales and unexpectedly warm winter weather hurt demand for the company's down coats and thermal underwear. It also announced it would cut its dividend to JPY350/shr vs. JPY370 per the prior guidance.

The sellside, which completely missed the collapse in profits, was quick to come up with a narrative:

Bloomberg adds that billionaire Chairman Tadashi Yanai had bet on expanding the company's Uniqlo casual clothing brand outside Japan, opening flagship stores in shopping districts from London to Paris, Shanghai, New York and Seoul. The move, prompted by stagnating economic growth in Japan, has made the company more vulnerable to a strengthening Japanese currency. The yen's gain, which as reported earlier had wiped out all losses since the expansion of Japan's QE in October 2014 and is up over 10% in 2016, led to a JPY22.8 yen foreign-exchange loss in the first half, the retailer reported Thursday. Chief Financial Officer Takeshi Okazaki warned that there could be more exchange losses if the yen continues to strengthen. It wasn't just the stronger Yen: Fast Retailing also took a 21 billion yen impairment loss related to its J Brand premium denim label in the U.S. and its domestic and overseas stores, but the message to both its and all other investors was clear: either the BOJ steps in with some more easing, or more companies are going to suffer from comparable "shock announcements" in the coming weeks as Japan's earnings season evolves. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 20 Lies Every American Should Know... Posted: 07 Apr 2016 06:05 PM PDT 20 Lies Every American Should Know...20....lies.EVEY.........AMERICIAN ....SHOULD Know... The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many more [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| If Gold Price Drives Through that Wall at $1,240, it has a Chance to Push Through $1,308 this Time Posted: 07 Apr 2016 05:34 PM PDT

You never can be quite sure what's moving markets in the beginning, then a form emerges from the fog. Gold has been stubbornly strong in the teeth of a correction: what giveth? Today Italians in Naples rioted in response to Prime Minister Renzi's pushing through bills to bail out Italian banks. They're hopelessly choked on bad loans, so of course the Italian taxpayers and bank depositors must bail them out. Sure, sure, like the government would bail out you or me if we made imbecilic loans to obvious deadbeats. Sure. Bank stocks responded by sinking like axheads in a stock tank. Bank Stock Index ($BKX) fell 2.86% today to close at 62.05. Behold, the chart: http://schrts.co/sAeVt2 Observe that the BKX peaked last July & thereafter hath fallen like a meteor. Dropped from 80.87 to 55.99 in February. Relief rally followed, which reached resistance around 66 that stopped it cold as kraut. Has been backing down since March, but today closed below the 50 DMA. MACD turned down. RSI points down. Did I mention that it had broken the uptrend line from March 2009 in January 2015? Did I mention it's going further down? Oh. Okay. More to our tastes is the Gold/Bank Stocks Index spread. As confidence in the financial system wanes, the bank stock index wanes and gold waxes. Since the spread is a fraction, gold/Bank Stock Index, the higher gold rises and the lower the BKX falls, the higher the Gold/BKX spread rises. Lo, the chart, http://schrts.co/cF2NSf Since November 2013 Gold/BKX hasn't been able to stay above 19.50. In 2015 it made a double bottom 13.50 & 13.77. Then it hot up in 2016, complete with runaway gaps, & hit 22.36, a 62% gain. Backed down to correct, even closed below 19.50 and fell as low as 18.63. Turned back up and climbed through the 20 & 50 DMAs. Today it gapped up and closed 20.02, up 4.46%. Probably a runaway gap. MACD has turned up, & the RSI. So what is driving gold & the bank stock index? Might be the news of an Italian bank crisis has folks running into gold? That would also explain the euro's lackluster performance & the yen's lustrous performance. Euro today lost 0.22% to $1.1371. Looks like a waterfall waiting to happen. Yen, on the other hand, has since 4 April clambered from 89.83¢/Y100 to 92.43¢, up 2.9% Three days ago it gapped up, then gapped up again today. Looks like a runaway, listen to those hoof beats! Look at the chart to see the runaway, http://schrts.co/UuqBFa I reckon stocks don't pertickerly care for bank crises, not even furrin ones. Dow today somewhere squandered 174.09 (0.98%). Let us run our minds back in time & ponder. Since the 1 April Dow high, the Dow has been up as much as 112.73 yesterday, but over the four days has lost a total 250.79 or 1.4%. Pretty good example of what government & Fed economists like to church up as "negative growth." Y'all have all seen negative growth in nature. That's where a squash plant sprouts, grows up, leafs out, blooms, sets fruit, then suddenly the ground sucks it all back in. Right. S&P500 took even harder licks. Left behind 24.75 (1.2%) to close at 2,041.91. In passing I point out that the chart was already showing a top. The unknown Italian bank crisis was only part of that, the rest was the fullness of time and stocks' indwelling weakness. They topped last May, broke in August, & ain't coming back for years. I ain't got time nor space to talk about the Dow in Gold & Dow in Silver. Suffice it to say both are proving that they have turned down. Another sign of antsyness in the markets: Yield on US 10 year treasury note fell 3.65%, pretty steep and through some internal support. That shows bond prices rising, which implies the fearful are edging toward the exits, trying to beat the stampede to come. On Comex, which closes at 1:30 Eastern, gold gained $13.70 (1.12%) to $1,236.20. Silver added 10.4¢ (0.7%) to 1515.6¢. In the aftermarket Gold was trading around $1,240.70 and silver around1522.5¢. Gold barely missed closing above its 20 dma ($1,237.50). Look at the chart, http://schrts.co/ghsAJK Day by day gold continues to scale up that rising trend line intertwined with the 50 DMA. Day by day it refuses to break down. Day by day I grow nervouser and nervouser. Day by day any further correction looks less likely. Wait a minute, Moneychanger! I though you said that when a crisis drives up gold, the effect quickly wears off and the gain is given back. That's certainly true of panic caused by political crises, but a financial system crisis feeds the heart of gold demand: monetary demand. That's what drives the gold price, & drives it crazy. This Italian crisis is precisely the sort of catalyst you would imagine as a new several year long gold rally begins. More, if gold drives through that wall at $1,240, it has a chance to push through $1,308 this time. If that happens, say bye-bye: you will NEVER see gold this low again. I will NO LONGER be telling anyone to hold off buying gold or silver, unless some big drop hits. I am beginning to believer the gold correction has ended, and the next leg up begun. Hold on! Beginning to believe, I said, not certain. Aurum et argentum comparenda sunt -- -- Gold and silver must be bought. - Franklin Sanders, The Moneychanger The-MoneyChanger.com © 2016, The Moneychanger. May not be republished in any form, including electronically, without our express permission. To avoid confusion, please remember that the comments above have a very short time horizon. Always invest with the primary trend. Gold's primary trend is up, targeting at least $3,130.00; silver's primary is up targeting 16:1 gold/silver ratio or $195.66; stocks' primary trend is down, targeting Dow under 2,900 and worth only one ounce of gold or 18 ounces of silver. US $ and US$-denominated assets, primary trend down; real estate bubble has burst, primary trend down. WARNING AND DISCLAIMER. Be advised and warned: Do NOT use these commentaries to trade futures contracts. I don't intend them for that or write them with that short term trading outlook. I write them for long-term investors in physical metals. Take them as entertainment, but not as a timing service for futures. NOR do I recommend investing in gold or silver Exchange Trade Funds (ETFs). Those are NOT physical metal and I fear one day one or another may go up in smoke. Unless you can breathe smoke, stay away. Call me paranoid, but the surviving rabbit is wary of traps. NOR do I recommend trading futures options or other leveraged paper gold and silver products. These are not for the inexperienced. NOR do I recommend buying gold and silver on margin or with debt. What DO I recommend? Physical gold and silver coins and bars in your own hands. One final warning: NEVER insert a 747 Jumbo Jet up your nose. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| "It's Probably Nothing": Truck Orders Plunge 37% As Unsold Inventories Soar Most Since 2007 Posted: 07 Apr 2016 05:10 PM PDT When we last looked at order of heavy, or Class 8, truck one quarter ago - that all-important, forward looking barometer of domestic trade - we said that even with 2015 in the history books, and as we start 2016 where the base effect was supposed to make the annual comps far more palatable, the latest, January data, as abysmal: "the drop continues to be one of Great Recession proportions, manifesting in yet another massive 48% collapse in truck orders in the first month of the year as demand appears to have gone in a state of deep hibernation." Fast forward one quarter when we now have another three months of Class 8 truck data, and unfortunately the orderbook has gone from bad to worse. As the WSJ reports, orders for new big rigs plunged and inventories of unsold trucks soared to their highest levels since just before the financial crisis, as uncertainty about future demand and a weak market for freight transportation weighed on truck manufacturers. About 67,000 Class 8 trucks are sitting unsold on dealer lots, after sales in March dropped 37% from a year earlier to 16,000 vehicles, according to ACT Research. Class 8 trucks are the type most commonly used on long-haul routes. Inventories haven't been this high since early 2007, said Kenny Vieth, president of ACT.

The number of March orders was the lowest since 2012. The problem according to the WSJ? Simply not enough freight, or as some may call it, trade: "It boils down to, at present, there are too many trucks chasing too little freight," Mr. Vieth said. As the Journal adds, companies that placed large orders in late 2014, only for customers to move less freight than expected last year, are reluctant to buy more vehicles now, analysts said. Online freight marketplace DAT Solutions reported last month that spot market rates for dry vans, or the box trucks that are ubiquitous on U.S. highways, fell 18% between February 2015 and February 2016, an indication of weak demand. "Fleets are being very cautious in the current uncertain economic environment," wrote Don Ake, a vice president with FTR Transportation Intelligence, which reported similar order numbers for March. "Freight has slowed due to the manufacturing recession, so they have sufficient trucks to meet current demand." Some examples:

Meanwhile, the backlog is growing: Stifel analyst Michael Baudendistel wrote in a note Tuesday that the backlog of Class-8 trucks appears to be about six months, and said that truck and truck component manufacturers like PACCAR Inc., Navistar and Meritor Inc. are likely to see further pressure on their share prices and earnings. But it's not just trucking weakness. As BMO's Brad Wishak notes, for the first 12 weeks of 2016, U.S. railroads reported cumulative volume of 2,905,113 carloads, down 13.7% from the same point last year, while Canadian railroads reported cumulative rail traffic volume of 1,540,562 carloads, containers and trailers, down 5.3 percent yoy, largely due to a drop in coal shipments but indicative of a decline across all product lines.

An obvious conclusion is that despite all the talk of a rebound in economic growth and domestic and global trade, the facts on the ground simply do not confirm this. So, as we asked four months ago, should one be concerned by this precipitous drop? Absolutely not: as the Federal Reserve would certainly say "it's probably nothing."

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 07 Apr 2016 04:00 PM PDT Alex Jones goes in-depth on the way in which the new world order are dumbing down and destroying the population of the world. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers ,... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gerlad Celente -- If You Like Trump , You Love Hitler Posted: 07 Apr 2016 03:38 PM PDT Gerlad Celente -- China is Manipulating the Market to Prevent Collapse, Potential WW3 About Gerald Celente : Founder of The Trends Research Institute in 1980, Gerald Celente is a pioneer trend strategist. He is author of the national bestseller Trends 2000: How to Prepare for and Profit... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| The 6 Secrets THEY Don’t Want You to Know Posted: 07 Apr 2016 03:00 PM PDT The 6 Secrets THEY Don't Want You to Know. Even the dumbest person knows that the world is controlled by certain individuals. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers ,... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Where Have All Your Tax Dollars Gone???? Posted: 07 Apr 2016 02:30 PM PDT they have done that i va for over 20 year now we have tolls. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many more [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Silver Price Forecast: The Interesting Relationship Between Silver Rallies and Interest Rates Posted: 07 Apr 2016 02:10 PM PDT Hubert Moolman | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Japan and the Secret Shanghai Accord Posted: 07 Apr 2016 01:50 PM PDT This post Japan and the Secret Shanghai Accord appeared first on Daily Reckoning. One of my persistent critiques about Wall Street research is that analysts don't get away from their desks enough. They spend all day staring at screens of data, streaming news, websites, blogs, etc., watching the same thing everyone else is watching. This stifles originality and creativity. It also leads to "groupthink," which is usually associated with everyone missing obvious dangers and walking off a cliff in lock step. Even when Wall Street analysts do venture out, it's to visit clients in skyscraper offices with canned presentations and programmed scripts. The dialogue is stilted. It's still an echo chamber, just a little further from home. For real insights into foreign markets, it is necessary not only to travel but also to meet with local experts in informal settings. It's also important to get out of the major metropolitan centers and visit other cities. Riding trains and taxis, shopping locally and dropping into informal venues can all give important clues (positive and negative) about how an economy is doing and how local actors view it. This approach to foreign travel and research has huge payoffs when a local elite reveals some critical piece of information that is simply not available online. Such insights are unknown to the Wall Street crowd, and understood by very few in the source country. Often these revelations take place over drinks or dinner, away from the downtown office buildings. I've traveled from the Sahara desert to the Australian Outback and beyond and have never gone anywhere without returning with some valuable clue that the crowd is missing. It was in that spirit that the Strategic Intelligence team recently visited Japan. As you know, Strategic Intelligence is the flagship and sister publication to Rickards' Intelligence Triggers. We use the insights gained on such trips to make our best recommendations and reveal our high-profit potential trades to you and other readers of Intelligence Triggers. Our team included our publisher, Peter Coyne; contributing editor Tres Knippa, me; and several colleagues. We visited Tokyo and Kyoto and met with local elites in finance, media and economics. It was an extremely fruitful trip.

One of the reasons these visits are so important has to do with the analytical method we in our Intelligence Triggers service. We use a centuries-old applied mathematical technique called inverse probability (also known as Bayes' theorem, after a formula first discovered by Thomas Bayes). The formula looks like this in its mathematical form:

In plain English, this formula says that by updating our initial understanding through unbiased new information, we improve our understanding. I first learned this method in the CIA, and we use it today to find actionable trading recommendations for you. The left side of the equation is our estimate of the probability of an event occurring. New information goes into right-hand side of the equation. If it confirms our estimate, it goes into the numerator (which increases the odds of our expected outcome). If it contradicts our estimate, it goes into the denominator (which lowers the odds of our expected outcome). The odds are continually updated as new information arrives. Economic and market forecasts inevitably involve uncertainty and risk. Conventional statistical analysis relies on massive amounts of data used in regressions that search for correlations (which may or may not imply causation). But what happens when you don't have piles of data? How do you gain insight and reach sound conclusions when data are scarce? That's where inverse probability is extremely useful. Lately, market chatter has tended to focus on China and the relationship between the Chinese yuan and the U.S. dollar. Substantial attention has also been paid to Europe and the ECB's handling of the euro. Japan has tended to be overlooked in this mix. That's a mistake because Japan is still the third-largest economy in the world and, unlike China, is a highly developed technological economy with massive overseas investments and complex supply chains. Japan has been suffering an economic depression for almost 30 years, with technical recessions and periodic deflation along the way. Fundamentals are poor, with a debt-to-GDP ratio over 200% and an aging and declining population. The Japanese government bond market is well into negative interest rate territory. Negative rates appear to be having the opposite effect of what policymakers intended, slowing the economy even more. In plain English, Japan is a mess. On the other hand, analysts have been saying the same thing for decades. The Japan story keeps getting worse, but there's nothing really new about the debt and demographic trends. Investors have been shorting Japanese stocks and bonds for years and getting their fingers burned. So much money has been lost shorting Japan that the trade is nicknamed the "widow maker" by professional traders. Using our inverse probability technique and some facts we learned on the ground in Tokyo and Kyoto, we have picked up some specific actionable information that tips the odds in favor of a short equity position, at least for the time being. This information involves the secret "Shanghai Accord" reached on the sidelines of the G-20 central bankers meeting in Shanghai, China, on Feb. 26. The situation confronting the central bankers was the following: China needs to devalue its currency to rescue its economy. But the last two times China devalued against the U.S. dollar (August 2015 and January 2016), the U.S. stock market sank like a stone. This threatened to set off global financial contagion that could lead to a repetition of the 2008 panic, except worse. The challenge was to find a way to give China some currency relief without igniting a global stock market collapse. The solution is to recognize that the U.S. dollar and the Chinese yuan are not the only two currencies in the game. China has a larger combined trading relationship with Japan and Europe than it does with the U.S. The secret plan devised by the central banks has three parts: Tighten in Europe and Japan, ease in the U.S. and maintain the U.S.-China peg. By maintaining the U.S.-China peg, markets would not panic about Chinese devaluation. In fact, by easing the U.S. dollar, China could ease the yuan and still maintain the peg. It's just a case of follow the leader. Meanwhile, the stronger euro and yen gave China competitive relief in its trading relations with those trading giants. Voilà! The Chinese got currency devaluation, and the world hardly noticed. How do we know this? After all, this plan was never publicly disclosed. The secret summit took place on Feb. 26. Our hypothesis was that a plan to give China some relief was on the front burner. What subsequent facts enabled us to update the hypothesis (as Bayes' theorem requires) to confirm or contradict the hypothesis? We used the following:

From an analytic perspective, the case is overwhelming. We had four powerful confirmation points and no contrary evidence. The odds of these four critical events happening in a short time frame without coordination are miniscule. The odds in favor of the existence of the Shanghai Accord are high. There has been no official denial. Developments like this are meant to be long lasting. Consider the "strong dollar" episode that lasted 3½ years until February 2016. Also consider the "weak yen" episode that lasted just over three years from December 2012 (the announcement of "Abenomics") to February 2016. Based on the Shanghai Accord and the dynamics of currency cross-rates, we expect the strong yen trend to continue for several years. That's bad news for major Japanese corporations. The largest corporations in Japan may be based there, but they derive most of their earnings overseas in the U.S., China, Korea, Taiwan and Europe. This means that when overseas earnings are converted back into yen, those earnings are worth less because of the stronger yen. The strong yen also slows the Japanese economy and increases local labor unit costs. This also hurts the bottom line in Japan. One way for you to profit from the secret Shanghai Accord and the new "strong yen" phase is to target a major Japanese company with a global footprint, too much debt and weak fundamentals. Regards, Jim Rickards P.S. Be sure to sign up for The Daily Reckoning — a free and entertaining look at the world of finance and politics. The articles you find here on our website are only a snippet of what you receive in The Daily Reckoning email edition. Click here now to sign up for FREE to see what you're missing. The post Japan and the Secret Shanghai Accord appeared first on Daily Reckoning. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Why Gold is the Ultimate Hedge Against Hackers Posted: 07 Apr 2016 01:38 PM PDT This post Why Gold is the Ultimate Hedge Against Hackers appeared first on Daily Reckoning. On August 22, 2013, the NASDAQ was shut down for half a day. Investors have never been given a credible explanation as to what happened. If there were a benign or technical explanation, NASDAQ NDAQ -1.06% would have told us about it by now. They could have said there was a bad piece of code or an engineer blundered while updating software or an installation didn't go well. NASDAQ has never provided information of any substance except a few vague references to an "interface problem." Why not? NASDAQ itself must know. One likely answer is that the cause of the shutdown was nefarious, and it was probably caused by criminal hackers or, worse yet, Chinese or Russian military cyberbrigades. Investors should have no doubt about the ability of a number of foreign cyberwarfare units to close or disrupt major stock exchanges in the United States and elsewhere. In 2014, Bloomberg Businessweek broke a story with a cover article titled The NASDAQ Hack. The incident referred to in the title goes back to 2010. Yet it was only in late July 2014 that the media were able to report on what happened: with help from the FBI, NSA, and Department of Homeland Security, the NASDAQ actually found a computer virus in its operating systems, traced it back to its source, and determined it was an attack virus. It wasn't put there by a criminal gang; it was planted by the Russian state. Stories of this type are often served up to reporters from official sources with an agenda. Why did this particular story come out four years after the incident? The reporting is timely, but why did the source wait four years? One surmise is that an administration official wanted to reveal the extent of the Russian invasion of U.S. financial exchanges as a way to alert investors to the possibility of worse to come. It was a warning. A common response from analysts is that our hackers must be as good as theirs; we could close down the Moscow Exchange if Russian hackers were to close down the New York Stock Exchange. Yes, of course we could. The United States is actually better at cyberwar than any other world power. But consider how that would play out. If Russia shuts down the New York Stock Exchange and we shut down the Moscow Exchange, who loses? We lose, because our markets are more important and much larger. There's far more wealth involved on our side and greater spillover effects. Russia, financially, is in the position of not having as much to lose. One reason to avoid retaliation and escalation in cyberwarfare is because it ends badly for the United States. Russian president Vladimir Putin knows that too, and that's one of the reasons he invaded Crimea with confidence in 2014. He knew perfectly well the United States could not escalate in the financial battle because, in the end, we had more to lose than Russia. For those unfamiliar with the Cold War, an escalation dynamic existed then also. The United States had enough missiles to completely destroy Russia (then called the Soviet Union). Russia had enough missiles to completely destroy the United States. This is a highly unstable situation because there was a great temptation to launch first. If you strike first and wipe out the other guy, you win. The response to this instability was to build more missiles. With enough missiles you could withstand the first strike and still have enough left over to launch a second strike. The second strike would devastate the party that started the war in the first place. It was that second- strike capability that prevented the other player from launching his missiles first. This same dynamic as applied to financial warfare is not fully appreciated today. The weapons may be symmetric but the losses are not. The United States has by far the most to lose. Another danger is the accidental launching of a cyberfinancial war. If you ask your hackers to devise an ability to shut down the New York Stock Exchange, they have to practice that. They have to launch probes. For example, a situation could arise where Russian hackers who don't intend to start a financial panic are probing and accidentally start a financial panic or an exchange systems shutdown. That is the much more worrisome scenario, because it doesn't require irrationality. It only requires an accident, and of course, accidents happen all the time. The United States has excellent deterrent capabilities in cyberwarfare through the military's Cyber Command and the National Security Agency (NSA). However, insufficient effort has been devoted to strategic doctrine. Only a few experts such as Juan Zarate at the Center on Sanctions and Illicit Finance, and Jim Lewis at the Center for Strategic and International Studies are performing roles comparable to those that Herman Kahn and Henry Kissinger performed in the 1960s when strategic nuclear war fighting doctrine evolved. This strategic deficiency increases the risk of cyberfinancial war. That threat is one more reason to own gold because it is not digital and cannot be hacked or erased. Regards, Jim Rickards P.S. Be sure to sign up for The Daily Reckoning — a free and entertaining look at the world of finance and politics. The articles you find here on our website are only a snippet of what you receive in The Daily Reckoning email edition. Click here now to sign up for FREE to see what you're missing. The post Why Gold is the Ultimate Hedge Against Hackers appeared first on Daily Reckoning. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 07 Apr 2016 12:57 PM PDT James Rickards, Chief Global Strategist at West Shore Funds and a widely renowned author is interviewed by FRA Co-founder Gordon T. Long in which they discuss Jim’s just released book The New Case for Gold. They also delve into issues concerning the false perceptions of the world switching back to a Gold Standard and the reasons for a suspected G-20 stealth “Shanghai Accord”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Americans spending more on taxes than food? Posted: 07 Apr 2016 12:30 PM PDT Swiss Americas Trading Corp. Chairman Craig Smith on how Americans are spending more on taxes than food, clothes and housing combined. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| THE END OF ALL THINGS IS AT HAND Posted: 07 Apr 2016 10:30 AM PDT Even as DEVASTATING WORLD EVENTS of APOCALYPTIC proportions continue to pound this planet, mockers, scoffers and satanists are running rampant while apostasy, lying spirits and world chaos are climbing toward global meltdown. Are you still in doubt that we're in the very LAST DAYS of this dying... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wikileaks: ‘Panama Papers’ funded by US against Russian president Posted: 07 Apr 2016 10:00 AM PDT Washington is behind the recently released offshore revelations known as the Panama Papers, WikiLeaks has claimed, saying that the attack was "produced" to target Russia and President Vladimir Putin. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts ,... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| The “Great Oil Divergence of 2016” Could Be Near Posted: 07 Apr 2016 09:38 AM PDT This post The “Great Oil Divergence of 2016” Could Be Near appeared first on Daily Reckoning. Oil jumped 5% yesterday. Stocks also rallied. The tail's wagging the dog again. No matter how hard the market's tried to escape, stocks have been anchored to oil. A down day for oil has meant a down day for the major averages. And vice versa. The magnitudes of their fluctuations haven't matched up. But directionally, stocks and oil have been joined at the hip this year. But this relationship might be coming to an abrupt end. Today we'll explore what might happen when oil and stocks say their long goodbyes—and how it could affect your trades. Despite yesterday's action, stocks are actually attempting a daring escape from crude's clutches. "For 2016, the two had been moving in lockstep with each other, but over the last several days they have parted ways," Bespoke Investment Group reports. "Now, over the last three days as equities have come under pressure, crude oil prices have rallied." Until yesterday, the S&P 500 and oil had traveled in opposite directions for over a week. Bespoke notes the last time they diverged that frequently over an eight-day period was last July. If we take a look at a chart, you can see how startling the separation has become this month:

There are no guarantees oil and stocks go their separate ways anytime soon. We've been watching this situation for the better part of 2016. So far, any divergence has been short lived. Within a few days, these two lovebirds are locked at the hip once again… "If stocks make a clean break from oil's downward pull, it could set the stage for more stability," we said back in February. "Oil and stocks rallied in tandem instead. Now their rallies are running on fumes simultaneously. Stocks are left at the mercy of the energy meltdown once again." The last thing we need is for oil to plunge lower and drag stocks down the tube. But their recent breakup—if it lasts— could be a sign of things to come. Frankly, I'm sick and tired of everyone's obsession with this oil and stocks story. If the major averages are going to attempt a legitimate run at their highs, they'll need to break the oil shackles. Breaking up is hard. But the great divergence could be underway… Sincerely, Greg Guenthner P.S. Profit from oil's next move–sign up for my Rude Awakening e-letter, for FREE, right here. Stop missing out. Click here now to sign up for FREE. The post The “Great Oil Divergence of 2016” Could Be Near appeared first on Daily Reckoning. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| FOMC Meeting Minutes Reveal Fed’s Dovish Nature Posted: 07 Apr 2016 09:15 AM PDT This post FOMC Meeting Minutes Reveal Fed’s Dovish Nature appeared first on Daily Reckoning. And now… today's Pfennig for your thoughts… Good day, and a tub thumpin’ Thursday to you! The dollar, which had given up some gained ground after the Fed’s Meeting Minutes (FMM) printed yesterday afternoon, has rebounded overnight and is back on top again this morning, although there are a couple of currencies with gains, and gold is up $16 in early morning trading, thus the dollar isn’t in all-out assault mode, this morning. Speaking of the FMM. The Fed’s FOMC Meeting Minutes (FMM) were interesting in that the Fed members were already showing signs of being dovish, even though many of them had been out prior to the meeting talking about how the Fed could hike rates in April, and leaving rates unchanged at their April meeting. Curious isn’t it that the Fed members were out talking about a rate hike in April, but when brought together they were talking about leaving rates unchanged when they meet next in April? Were they attempting to throw the markets of the scent of a dove? Looks that way to me, because when you look under the hood, you see that the Fed members’ clearly saw global economic and financial developments as shifting the risks sharply to the downside, but refused to say that in the comment following the no rate change announcement. But IF that’s the case, it sure isn’t. No wait! I had better stop there, but I think you know where I was going with that. Speaking of gold… Recently I’ve been talking a bit about the planned beginning of a renminbi denominated Gold Fixing at the Shanghai Gold Exchange (SGE). I’ve been wary about saying for sure it would start in April, because there have been two previous dates given for the start that didn’t materialize (April & Dec 2015). I know this irks the Chinese leaders because they don’t like it when they say something is going to happen, and then is delayed. But I do believe we’ll see this new fixing soon. And when we do, things will change, folks. First of all one must be aware that there will be NO PAPER trades! Only physical gold trades accepted! So, there goes the ability of manipulators to play paper games with gold. Speaking of which… did you know that in the COMEX here in the U.S. Commercial traders on 4/1 reached an all-time record # of short contracts in gold? 207,900 short contracts that obviously represents more ounces of physical gold than is known in our universe to exist. Talk about cheating consumers! Consumers buy with an idea that negative interest rates, geopolitical tensions around the world, and weak economies, Central Banks hell-bent and whiskey bound to inject inflation in their respective economies, and an idea that there are regulations that protect them from manipulated markets, are enough fundamentals to push the price of gold higher, only to then see it lose ground because of paper trades. I loved, no wait, I absolutely loved this comment from James Rickards that came from his new book: The New Case For Gold. Let me set this up… Rickards is talking about how Central Bankers including the Fed members bash gold whenever they get the opportunity. So, what say you James? Rickards said:

The best performing currency overnight is Japanese yen, which has rallied past through the 110 figure, and the 109 figure, down to 108.25. WOW! This latest move pushes yen to the best performing currency this year! It’s up over 11% vs. the dollar year-to-date! I can see the Japanese leaders all sweating bullets, and vowing to get revenge with the yen traders that have done this dastardly deed to them and their plans for the Japanese economy that included the need for a weak yen to promote growth and inflation. Japanese leaders have jawboned about all they can, and have become the boy who cried wolf. So, now they will have to resort to the bazooka effect of monetary policy that the European Central Bank (ECB) pulled out of the closet last month. Funny thing though, that bazooka of monetary policy to weaken the euro, only riled up the currency traders and the euro has rallied since the ECB and its leader, Mario Draghi fired the bazooka. Remember me calling him Bazooka Joe? The euro is flat this morning and is trading just below the 1.14 figure at 1.1395. That’s what I call within’ spittin’ distance. I sure wish the ECB would just leave well enough alone, and allow the Eurozone economy to sink or swim. Of course I would wish that same thing for any country that has a Central Bank that thinks they know best. Whoa, there Chuck! Isn’t that just about every country? Ahhh, grasshopper, there are a couple of exceptions. let’s check those out! Singapore is a country that has long been a model of efficiency. I wrote about the Singapore dollar (S$) last month as the currency of the month in a Sunday pfennig, if you missed it or want to go back to read it you can find it here. You see Singapore uses the Monetary Authority of Singapore (MAS) to set the trading band for the S$, and the MAS uses the S$ as their main tool to combat inflation, instead of just arbitrarily raising or cutting interest rates. Next week, the MAS will probably meet to discuss the trading band. I think they’ll keep things steady Eddie, as the S$ has gained about 5% so far this year, keeping inflation in Singapore in check. And we have an old dog that’s relearning tricks it once knew – the Reserve Bank of Australia (RBA). I don’t want to spoil the soup, so I’ll stay out of the kitchen here. You see, the Aussie dollar (A$) is the subject of my next Currency of the Month that will be on the newsstands in about a week. So, I’ll just tell you that I’m impressed with the RBA’s ability to keep a lid on rate cuts. The Risk environment that was so prominent in the markets about 10 days ago, has faded away and it’s all about safe havens these days. One thing that could really change that in a hurry is a stronger than expected Chinese PMI (manufacturing index). A stronger than expected report like that would really get the risk campers all lathered up again, but anything short of that will keep the risk environment at bay. I haven’t talked about the BREXIT this week, and I’ll rectify that right now! I had an anonymous email to the banking center from someone that wanted to start an argument with me about my stance on the BREXIT. I’ve said that I thought that in reality, the U.K. Gov’t officials were for leaving the European Union (EU), and this anonymous emailer said that was wrong. Well, if he had given me his email address I would have responded to him and told him that I was going on comments that I had read from the backbench members, and not the “company line” that PM Cameron is telling the media. The pound sterling/pound, continues to be drawn and quartered every time there’s something going on that would feed the “leave the EU” campers more ammunition. And that’s exactly what happened when a referendum in Holland was rejected that would have been a trade agreement with Ukraine. Now, that seems harmless right? Well, it’s not, because this is something that the “leave the EU” campers can point to as a reason why being a part of the EU is hurting the U.K. The impeachment of Brazilian president Dilma Rousseff is gaining momentum and with every bit of information that talks about how the impeachment process is going, the Brazilian real reacts. If the information is positive for the impeachment process then the real rallies, and vice versa. I don’t like having currencies get tied up in the Political process like this. But it is what it is, and at this point with real, does it really matter? Rousseff threw everything including the kitchen sink at the real when she came into power, and ruined a lot of people’s investments, so if the real rebounds on her impeachment it seems to be KARMA to me. The price of oil inched higher in the past 24 hours, but again no one is impressed at this point. I had a back and forth conversation with my friend Dennis Miller, the retirementor, (that’s what he’s called because he is a retirement guru! ) regarding the price of oil. He’s all for the lower price of oil because of what it does to the price of gas. And the idea that this could all lead to a break up of OPEC. And allowing the markets to set the price of oil again, not OPEC. I’m all for that idea! But I worry about the oil producers, especially in this country, and all the loans they have on the books that they took out when things were going great for them, but now with the price of oil probably near or below the cost to produce, things get a little hairy, eh? The dollar has taken more of a hold on the currencies as I’ve been writing, and I can’t figure out what’s going on here. The U.S. Data Cupboard is basically empty today, and there isn’t any big data out this morning elsewhere. Hmmm… Oh well, time to head to the Big Finish. There’s basically no data in the Data Cupboard this morning, except some third tier reports, but next week we’ll get to see the March Retail Sales data. The BHI indicates to me that the report will be better than February’s negative -0.1% print, but still disappointing. And that doesn’t help the consumption data that the U.S. GDP relies on so heavily. The first QTR GDP continues to be downward revised in my GDP tracker. I told you yesterday, that after the widening of the Trade Deficit, that my GDP tracker had fallen to 0.4% for first QTR GDP. Speaking of a weak first QTR GDP. My friend, and publishing giant, and writer extraordinaire, Bill Bonner, wrote yesterday that JP Morgan Chase has revised downward their forecast for U.S. 1st QTR GDP to 0.7%… So, I have it at 0.4%, and JPMC has it at 0.7%… Neither one would be good! Bill also shared with his readers that “Globally 36 Corporate Bond issues have defaulted so far this year, up from the 25 during the same period of 2015.” Again, I don’t think the Fed needs to be so concerned with global problems, we have our own problems here in the U.S. that need to be addressed! Well, gold is up $16 this morning, and I spent a ton of time talking about gold above, so I’ll switch over to silver this morning. Silver is up 9% so far this year, as it follows gold to higher ground. The Perth Mint reported that in March, silver coin sales were the second highest level on record! Physical demand for precious metals continues to be strong, and is something I think is starting to scare the paper traders. For What It’s Worth. I came across this article when doing some research on the Bloomberg this morning, then I see it featured in Ed Steer’s letter, and I said, “I’ve got to go back and find that article on the Bloomberg” and I did! So, here is the link to an article titled: “The Coming Default Wave Is Shaping Up To Be Among The Most Painful” You knew that had to catch my eye, right? Here’s the snippet:

Chuck again. Well, it’s nice to see the rest of the world catching up to this story on corporate debt that I first started talking about a year ago! And again, this is one of those problems here in the U.S. that the Fed needs to be more focused on instead of things going on around the world. Of course that’s just my own opinion, and I could be wrong! That’s it for today. Have a tub thumpin’ Thursday, and to be good to yourself! Regards, Chuck Butler P.S. Be sure to sign up for The Daily Reckoning — a free and entertaining look at the world of finance and politics. The articles you find here on our website are only a snippet of what you receive in The Daily Reckoning email edition. Click here now to sign up for FREE to see what you're missing. The post FOMC Meeting Minutes Reveal Fed’s Dovish Nature appeared first on Daily Reckoning. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| BREAKING: Hillary Clinton "Bombshell" Fed Courts Rule On Benghazi Investigation" Posted: 07 Apr 2016 09:00 AM PDT Federal Courts allow more investigation on the Benghazi Case against Hillary Rodham Clinton The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many more [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Student Loans the next bailout? Posted: 07 Apr 2016 08:30 AM PDT More than 40% of student borrowers arent making payments. FBNs Ashley Webster and Washington Examiner Chief Political Correspondent Byron York with more. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Alasdair Macleod: Gold and interest rates Posted: 07 Apr 2016 07:26 AM PDT By Alasdair Macleod It is commonly assumed that the gold price and interest rates move in opposite directions. In other words, a tendency towards higher interest rates is accompanied by a lower gold price. Like all assumptions about prices, sometimes it is true and sometimes not. The market today is all about synthetic gold, gold that is referred to but rarely delivered. The current relationship is therefore one of relative interest rates, because positions in synthetic gold, in the form of futures and forwards, are financed from wholesale money markets. This is why a rumor that interest rates might rise sooner than expected, if it is reflected in forward interbank rates, leads to a fall in the gold price. To the extent that this happens, the gold price has been captured by the modern banking system, but it was not always so. ... ... For the remainder of the commentary: https://www.goldmoney.com/research/goldmoney-insights/interest-rates-and... ADVERTISEMENT Buy metals at GoldMoney and enjoy international storage GoldMoney was established in 2001 by James and Geoff Turk and is safeguarding more than $1.7 billion in metals and currencies. Buy gold, silver, platinum, and palladium from GoldMoney over the Internet and store them in vaults in Canada, Hong Kong, Singapore, Switzerland, and the United Kingdom, taking advantage of GoldMoney's low storage rates, among the most competitive in the industry. GoldMoney also offers delivery of 100-gram and 1-kilogram gold bars and 1-kilogram silver bars. To learn more, please visit: http://www.goldmoney.com/?gmrefcode=gata Join GATA here: Mines and Money Asia http://asia.minesandmoney.com/ Mining Investment Asia http://www.mininginvestmentasia.com/ Support GATA by purchasing recordings of the proceedings of the 2014 New Orleans Investment Conference: https://jeffersoncompanies.com/landing/2014-av-powell Or by purchasing DVDs of GATA's London conference in August 2011 or GATA's Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 07 Apr 2016 07:16 AM PDT | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Interesting Relationship Between Silver Rallies and Interest Rates Posted: 07 Apr 2016 06:18 AM PDT It is not well known, that historically silver and interest rates have actually moved together (in the long-term). When interest rates are going up, then silver is going up. When interest rates are going down, silver is going down. In the short-term, interest rates and silver can diverge (like since about 2002 to now); however, this is temporary. Interest rates have been going down for the last 34 years. Due to this long downward trend, many believe that interest rates will not rise. Unknowingly (due to the correlation between silver and interest rates), they indirectly believe that silver will not rise. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Surprise! A Gold Bear at Goldman Sachs Posted: 07 Apr 2016 06:09 AM PDT Following a lengthy discussion about the energy market (oil prices to rise this summer), at about the four minute mark Jeffrey Currie, Goldman Sachs Head of Commodities Research, reiterates his long-held bearish outlook for precious metals. I’ve read Currie’s commentary many times over the years, but never seen him speak until this clip. Granted, his [...] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 07 Apr 2016 03:34 AM PDT As the consolidation phase continues to build out from this first impulse move up in the precious metals sector lets review some of the charts we’ve looked at previously that suggested the bear market might be over. Most of these charts will be ratio charts which compare different sectors to one another These rather complex charts can give us some hidden clues that an important reversal may have taken place. The consolidation process takes its toll on both the bulls and the bears alike. As you know there are never any guarantees of anything when it comes to the markets so it’s always important to try and get the big picture right to get the odds in your favor. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold Once Again Proves To Be The Best Defense Strategy Posted: 07 Apr 2016 01:52 AM PDT Taki Tsaklanos submits: If you are used to making visits to your bank to make your credit card payments, you may find this no longer an option in the future. Some banks are no longer accepting (or limiting their acceptance) of cash deposits. The war on cash forges on. Paper money, that is indeed more or less worthless, is slowly being taken out of circulation and being replaced by digital currency forms. This shift presents of course the same fundamental problem as paper money itself: “digital money” is also not backed by gold or other precious metals or any asset representing real value. The whole concept of digitizing our transactions is being marketed as a convenience, a hassle-free payment method and a transparent, easy new way to smoothly run our lives and businesses, without the burden of carrying cash around. However, the realistic flip side of this joyful argument is more ominous than we might at first realize: Now, account monitoring or freezing, and confiscations will be easier than ever. And of course, by eliminating cash, central banks are getting rid of the last existing barrier to negative interest rates. |

CNN criticized a plan devised by political insider Roger Stone and radio host Alex Jones calling for Trump supporters to assemble at the Republican National Convention in Cleveland in July.

CNN criticized a plan devised by political insider Roger Stone and radio host Alex Jones calling for Trump supporters to assemble at the Republican National Convention in Cleveland in July. In a world of manipulated economic figures and markets, it is not always easy to maintain your sanity. The world economy is now based on fantasy and hope and has very little to do with reality. But the problem is that virtually nobody understands this. Whether it is a bank analyst or a Nobel Prize winner in economics, they are all spreading the same false message. The Western press and news media are just reporting what governments and the elite are telling them. There is no analysis and no attempt to find the truth in anything. This is why we are now in an era of indoctrination and total brainwashing of the masses. Most people are totally apathetic and incapable of realising that they are being led down a path, both morally and economically, that will make life on earth a lot more difficult not just for the present generation but probably for several generations to come.

In a world of manipulated economic figures and markets, it is not always easy to maintain your sanity. The world economy is now based on fantasy and hope and has very little to do with reality. But the problem is that virtually nobody understands this. Whether it is a bank analyst or a Nobel Prize winner in economics, they are all spreading the same false message. The Western press and news media are just reporting what governments and the elite are telling them. There is no analysis and no attempt to find the truth in anything. This is why we are now in an era of indoctrination and total brainwashing of the masses. Most people are totally apathetic and incapable of realising that they are being led down a path, both morally and economically, that will make life on earth a lot more difficult not just for the present generation but probably for several generations to come. If anyone needs one more reason to break up the mega banks on Wall Street, simply look at what happened following the Federal Reserve's quarter of a percentage point rate hike on December 16 of last year. On that date, the Fed moved off its seven year zero interest rate policy (ZIRP), which had been a bonanza for the banks and a starvation plan for seniors living on fixed income investments like Treasury notes and CDs, and raised its benchmark rate by a quarter of a percentage point to between 0.25 percent and 0.50 percent from its former 0.0 to 0.25 percent.

If anyone needs one more reason to break up the mega banks on Wall Street, simply look at what happened following the Federal Reserve's quarter of a percentage point rate hike on December 16 of last year. On that date, the Fed moved off its seven year zero interest rate policy (ZIRP), which had been a bonanza for the banks and a starvation plan for seniors living on fixed income investments like Treasury notes and CDs, and raised its benchmark rate by a quarter of a percentage point to between 0.25 percent and 0.50 percent from its former 0.0 to 0.25 percent.

| You are subscribed to email updates from Save Your ASSets First. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment