Gold World News Flash |

- The Coming Cashless Society

- The Economic Facts Are Pointing To An Economic Collapse

- Retail Apocalypse: 2016 Brings Empty Shelves And Store Closings All Across America

- Keeping an Eye on Gold Bullion Supply and Demand

- Silver and Gold Prices Stalled Today with the Gold Price Ending Down at $1,127.30

- Time Running Out for China on Capital Flight, Warns Bank Chief

- Gold In Japan, Tokugawa Coins – 鎖国 Sakoku

- The Coming Revaluation Of Gold

- "We Need To Rise Up": Bilked Chinese Investors Call For Nationwide Uprising After Massive Ponzi Uncovered

- Why Bernie Sanders Has To Raise Taxes On The Middle Class

- The Bank Of Japan Has Betrayed Its People

- "Hidden Planet X" Could Be In Orbit!!

- TF Metals Report: Connecting the Comex dots

- Here's How Much The Strong Dollar Hurts US Companies

- Gold Daily and Silver Weekly Charts - More 'Flight To Safety' - Active February

- Nostradamus : What Will Happen When The Dollar Collapse In 2016

- Defying Wall Street for “Knock Your Socks off” Returns

- America is like Israel – Chris Steinle at The Prophecy Club Radio

- Slouching Toward The Dark Side

- Global Economy Could Fall Farther and Faster Than Pundits Expect

- Bron Suchecki: Would you risk going to jail to fix the fix?

- Saudi Arabia and Oil’s Future

- How the Blockchain and Gold Can Work Together

- Epic Battle: Hedge Funds Versus China

- My Global Financial Road Map For 2016

- RBA and RBI Leave Rates Unchanged

- New Indian rule backfires, boosts unofficial gold trade

- Have Stocks Broken the Oil Curse? Here’s the Answer…

- The Next Generational Bust Is Coming, Stock Market 70% Collapse

- How and Why To Move Your Assets Offshore Before the Financial Collapse

- Krinsky on Stock Market: Primary Trend Has Shifted to the Downside

| Posted: 02 Feb 2016 11:09 PM PST Seal the Exits!: The Coming Cashless Society Employing behavioral psychology to force you to spend Swedish Riksbank: Charge penalties those who use cash The bosses are liquidating: High volume Insider selling The Financial Armageddon Economic Collapse Blog tracks trends and forecasts ,... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Economic Facts Are Pointing To An Economic Collapse Posted: 02 Feb 2016 11:00 PM PST from X22Report: Euro zone manufacturing starts to slow and decline. Spending down and savings at its highest since 2012. Revenue and earnings for corporations are in a decline, 4 of the 10 indicators showing signs of recession. Manufacturing and employment declining. Baltic Dry Index declines once again. The Atalanta FED reports GDP is only going to be 1.2 for 1st quarter of 2016. The call for a cashless society begins, the central bankers will consider cash worthless.Senate to vote on TPP. Obama and the Treasury department hid the facts from congress in regards to the debt ceiling hike. Iran has more banks using SWIFT. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Retail Apocalypse: 2016 Brings Empty Shelves And Store Closings All Across America Posted: 02 Feb 2016 10:25 PM PST by Michael Snyder, End of the American Dream:

Major retailers in the United States are shutting down hundreds of stores, and shoppers are reporting alarmingly bare shelves in many retail locations that are still open all over the country. It appears that the retail apocalypse that made so many headlines in 2015 has gone to an entirely new level as we enter 2016. As economic activity slows down and Internet retailers capture more of the market, brick and mortar retailers are cutting their losses. This is especially true in areas that are on the lower portion of the income scale. In impoverished urban centers all over the nation, it is not uncommon to find entire malls that have now been completely abandoned. It has been estimated that there is about a billion square feet of retail space sitting empty in this country, and this crisis is only going to get worse as the retail apocalypse accelerates. We always get a wave of store closings after the holiday shopping season, but this year has been particularly active. The following are just a few of the big retailers that have already made major announcements… -Wal-Mart is closing 269 stores, including 154 inside the United States. -K-Mart is closing down more than two dozen stores over the next several months. -J.C. Penney will be permanently shutting down 47 more stores after closing a total of 40 stores in 2015. -Macy's has decided that it needs to shutter 36 stores and lay offapproximately 2,500 employees. -The Gap is in the process of closing 175 stores in North America. -Aeropostale is in the process of closing 84 stores all across America. -Finish Line has announced that 150 stores will be shutting down over the next few years. -Sears has shut down about 600 stores over the past year or so, but sales at the stores that remain open continue to fall precipitously. But these store closings are only part of the story. All over the country, shoppers are noticing bare shelves and alarmingly low inventory levels. This is happening even at the largest and most prominent retailers. I want to share with you an excerpt from a recent article by Jeremiah Johnson. The anecdotes that he shares definitely set off alarm bells with me. Read them for yourself and see what you think… ***** I came across two excellent comments upon Steve Quayle's website that bear reading, as these are two people with experience in retail marketing, inventory, ordering, and purchases. Take a look at these: #1 (From DJ, January 24, 2016)

#2 (From a Commenter following up #1 who didn't provide a name, January 26, 2016)

***** Yes, this is just anecdotal evidence, but it lines up perfectly with hard numbers that I have been discussing on The Economic Collapse Blog.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Keeping an Eye on Gold Bullion Supply and Demand Posted: 02 Feb 2016 09:56 PM PST Clint Siegner writes: A lot is riding on the demand side of the equation when it comes to metals' price performance this year. Demand is the bigger wildcard with signals thus far being mixed in gold and silver bullion markets. The outlook for supply is more certain, and it isn't pretty. Endeavor Silver, one of the largest primary silver mining companies, announced last week that it expects to reduce production of the white metal by roughly 30%. The company's El Cubo mine is not profitable despite efforts to reduce costs. Endeavor plans to halt development and exploration at the mine and process accessible ore only. By year end, the mine will be placed on “care and maintenance.” | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Silver and Gold Prices Stalled Today with the Gold Price Ending Down at $1,127.30 Posted: 02 Feb 2016 09:55 PM PST

No market is infinitely flexible. Can't put off a decision forever. Therefore silver and gold prices must move decisively.

In January 2015 the GOLD PRICE rallied nearly to that downtrend line, even crossed above its 200 DMA, but failed. In May it reached again toward the line, peeked through the 200 DMA, but fell back. In October it pierced both barriers, only to fizzle out and waterfall to new lows.

Understand, when I say gold must fish or cut bait, I'm not just flapping my gums. As in life, if you're not moving forward you're falling back -- soon. SILVERS story is similar. It has formed a bowl since November, and a bowl usually resolves by breaking upward. Lip of the bowl lies about $14.40 - $14.65. Call it $14.65 to get plumb clear. Silver tried in December, and failed. Tried again in December, and failed, and has failed twice in January. Keep failing, and the bowl turns into the type that flushes. I think silver and gold are trying to rally, but no breakout, no rally. Stocks lost big today. Dow tumbled 295.64 (1.8%) to 16,153.54. S&P500 lapsed 36.35 to 1,903.03, down 1.87%. Both closed BELOW their 20 day moving averages, so short term momentum is down although some indicators still point up. Greater volatility points out lower strength. Right now they need lows below 15,450 and 1,812 to turn them down. Probably will work higher so the bear can lure more incautious bovines into his lair, where he can maul them at will. US dollar index is working hard to appear weak. Today again it tried to break down out of that wedge (or channel) formation earthward. closed below 20 and on the 50 day moving averages, down 16 basis points at 98.86. Where is the strength by which it vaulted on Friday? Vanished. Gone. If the dollar index breaks that 50 DMA (98.85) and that pattern's bottom boundary, there will be nothing to hold it up but Nice Government Men, and I hope they ain't the skinny, wormy ones. Many thanks for your prayers for Susan's eye surgery last Tuesday. It was successful but more painful in recovery than we anticipated. Today it's improving, but still painful. Please remember her in your prayers. Aurum et argentum comparenda sunt -- -- Gold and silver must be bought. - Franklin Sanders, The Moneychanger The-MoneyChanger.com © 2016, The Moneychanger. May not be republished in any form, including electronically, without our express permission. To avoid confusion, please remember that the comments above have a very short time horizon. Always invest with the primary trend. Gold's primary trend is up, targeting at least $3,130.00; silver's primary is up targeting 16:1 gold/silver ratio or $195.66; stocks' primary trend is down, targeting Dow under 2,900 and worth only one ounce of gold or 18 ounces of silver. or 18 ounces of silver. US $ and US$-denominated assets, primary trend down; real estate bubble has burst, primary trend down. WARNING AND DISCLAIMER. Be advised and warned: Do NOT use these commentaries to trade futures contracts. I don't intend them for that or write them with that short term trading outlook. I write them for long-term investors in physical metals. Take them as entertainment, but not as a timing service for futures. NOR do I recommend investing in gold or silver Exchange Trade Funds (ETFs). Those are NOT physical metal and I fear one day one or another may go up in smoke. Unless you can breathe smoke, stay away. Call me paranoid, but the surviving rabbit is wary of traps. NOR do I recommend trading futures options or other leveraged paper gold and silver products. These are not for the inexperienced. NOR do I recommend buying gold and silver on margin or with debt. What DO I recommend? Physical gold and silver coins and bars in your own hands. One final warning: NEVER insert a 747 Jumbo Jet up your nose. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Time Running Out for China on Capital Flight, Warns Bank Chief Posted: 02 Feb 2016 08:00 PM PST 'The Chinese have not been very convincing. There is a perception that the renminbi could weaken drastically,' warns the Institute of International Finance

by Ambrose Evans-Pritchard, The Telegraph: China is rapidly losing the confidence of global lenders and capital outflows risk turning virulent if the current policy paralysis continues, the world's top banking body has warned. "There is a perception that the renminbi could weaken drastically," said Charles Collyns, the managing-director of the Institute of International Finance in Washington. Mr Collyns said the authorities have so far failed to articulate a coherent strategy, and there are serious worries that outflows of capital could accelerate, broadening into a flood beyond Beijing's control. "The Chinese have not been rigorous and they have not been very convincing," he told The Telegraph. Mr Collyns said China has already allowed the renminbi (yuan) to weaken against the country's new trade-weighted basket of currencies, stoking suspicions that the recent shift from a crawling dollar-peg to a more opaque foreign-exchange regime is really a cover for devaluation. The IIF, the chief global body for the banking industry, calculates that capital outflows from China reached $676bn last year. The central bank has been burning through foreign exchange reserves to offset the bleeding and shore up the currency, culminating in intervention of $140bn in December, by some estimates. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold In Japan, Tokugawa Coins – 鎖国 Sakoku Posted: 02 Feb 2016 07:40 PM PST from Junius Maltby: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Coming Revaluation Of Gold Posted: 02 Feb 2016 07:25 PM PST Submitted by Hugo Salinas Price via Plata.com.mx, The current melt-down of the world's debt bubble is likely to continue in the course of the next months. The secular trend to expansion of credit has morphed into contraction and liquidation. It is my opinion that the new trend is now established and no action by any of the Central Banks (CB) that issue reserve currencies will do anything at all to reverse that trend. Sandeep Jaitly thinks that the desperate reserve-issuing CBs - the US Fed, the ECB, the Bank of England and the Japanese CB - may resort to programs of QEP, by which he means "Quantitative Easing for the People". This quantitative easing will mean putting money into the hands of the populations by rebates on taxes, invented make-work schemes or any other excuse to furnish the people with the famous "helicopter money", to get them to spend. As the present crisis deepens and given our experience with the way our so-called “economists” think, we can reasonably expect such programs to be launched. Nevertheless, the present trend of world economic contraction will not be reversed by any ad hoc program. The world’s expectations - positive for growth since WW II - have turned negative. This is an event of such magnitude that no “QE” will have any effect upon the final outcome: debt collapse. The growing fear in the world's markets arises from the recognition on the part of indebted corporations and individuals that their debt burdens are increasing due to devaluations of their national currencies. International investors are attempting to reduce their exposure. “Hot money”, invested in countries which offered higher interest rates, now wants to go home. In recent years of bonanza, foreigners borrowed some $11 trillion dollars, in various Reserve Currencies, to invest in their own countries. Of this total, it is calculated that about $7 trillion of those dollars are denominated in dollars. The debtors are now attempting to pay-off their dollar loans, and this has the effect of lowering the value of their own currencies with respect to the US Dollar, thus aggravating the situation. There is a loss of confidence in national currencies, producing Capital flight to the rising Dollar, because the countries that issue those currencies are no longer able to maintain export surpluses against the reserve-issuing countries, and are thus unable to increase reserves and are actually losing these reserves. The export-surpluses are disappearing in the "rest of the world" because the reserve-currency countries, plus China, are in an economic slump (essentially attributable to excessive debt) and are reducing their consumption of imports, thus reducing the exports of the export-surplus countries. The loss of Reserves on the part of the countries which depend on export-surpluses for economic health makes the accumulated debt burden in the world increasingly unsustainable; investors around the world are worried that some of their assets (which are actually debt instruments, that is to say various sorts of promises to pay) may turn out to be duds, and they are trying to find ways to protect themselves - and Devil take the hindmost! Whatever expedients are implemented, the final outcome of the unprecedented economic contraction in the world will have to be the revaluation of gold reserves, as desperate governments of the world resort to gold to preserve indispensable international trade. The revaluation of gold reserves held by Central Banks will be the only alternative for countries seeking to retain a minimum of international trade to supply their economies, whether they are based on agriculture, on manufacturing or on mining. The amount of gold held by any particular country will not be the important factor in maintaining operating economies, because even a small amount of gold will be sufficient for that purpose; the reason being, that gold coming into newly rediscovered importance, no country will be able to maintain either trade surpluses or trade deficits. The first case would imply that other countries are sending their precious gold to the surplus export countries, but the scarcity of gold and its vital importance will not permit other countries to lose their gold to the (would-be) surplus-producing countries. In the second case, the trade-deficit countries would immediately correct their activity by devaluing their currencies ipso facto, rather than continue to lose their precious gold to cover their trade-deficits: devaluation would put an immediate stop to the excess of imports over exports. Governments resorting to credit-creation to fund their deficits would find themselves limited to balanced budgets; otherwise, their budget deficits funded by credit-creation would spill over into excessive imports and the consequent necessity for immediate devaluation of their currency. Only gold-producing countries will be able to run trade deficits, limited to the amount of gold they produce to pay for such deficits. Thus, the revaluation of gold will have the beneficent effect of restoring the world to a healthy condition, lost a century ago, of balanced trade and balanced national budgets. The discipline of gold as Reserves backing currency at a revalued price will restore order to a world that has refused to adopt the necessary discipline until forced to do so in the desperate situation now evolving, where there will be no other alternative but to accept the detested fiscal and financial discipline imposed by gold. We do not know the true amount of gold held by the world's central banks, because it is a closely held secret. However, we need not know that figure. Whatever gold there is in CB vaults will be sufficient, for the reasons we have given. Nor do we know at what price, in dollars, the price will be set, or how it will be set. However, given the truly astronomic amounts of debt in existence, a very high price will be necessary to "liquefy" i.e. make payable remaining debt, whatever the amount remaining after the purge which is now in process. The very high price of gold will mean that all debt instruments will be subject to large losses in terms of gold value. The revaluation of gold will reduce the weight of the present debt overhang upon the world. The revaluation of gold does not mean that prices of goods and services will rise in tandem with the higher price of gold. Established prices will by and large remain the same prices that existed before the revaluation. However, prices will have to re-adjust to reflect the new economic realities. Many goods that we have taken for granted will disappear, as their artificial cheapness vanishes. Another characteristic of a world that has begun to trade with gold-backed currencies as money, will be that one-way flows of gold from one region to another, or from groups of countries to a single country, will be impossible; such a flow would become a permanent drain on gold for some region or some country, and a permanent increase in gold for some region or some country. Eventually the gold would tend to pile up in some region or country, leaving the rest of the world with a lack of gold. The oil-producing countries will have to adjust the gold price of their oil exports to balance with the gold price of their imports, plus the gold value of their investments abroad. For a visual appreciation of the coming conditions, we have provided a few graphs. The first column illustrates the present condition, with present CB Reserves at $11.025 Trillion dollars, plus an estimate of CB Reserves of 31,110 tons of gold at $1,100 Dollars an ounce (according to an authoritative calculation of 183.000 tons of gold in existence at present, of which 17% are calculated to be held as Reserves by Central Banks around the world). The second column presents the present CB Dollar Reserves, below CB reserve gold revalued at $22,000 Dollars an ounce. The third column presents the present CB Dollar Reserves, below 50,000 tons of reserve gold revalued at $50,000 Dollars an ounce. We use the larger figure for CB gold, because some analysts think that China, and also Russia, have far larger gold reserves than they disclose publicly.

Why do we use $22,000 and $50,000 Dollars an ounce? Because other thinkers have estimated a necessary revaluation of gold, with various figures between a low price of $10,000 Dollars and ounce and a high price of $50,000 Dollars an ounce. So we arbitrarily selected $22,000 Dollars an ounce and $50,000 Dollars an ounce. Take your pick. The price and the quantity of gold in Central Bank vaults are really immaterial; the facts will be known eventually, and the result will be what we have pointed out above: the restoration of balanced trade and balanced budgets in our present highly disorderly world. Once the world's currencies are "gold-backed", then the gold held by individuals, trusts or corporations will cease to lie lifeless in stocks of gold. All gold will have become money and will spring to life in furthering economic activity: the revaluation of gold by Central Banks will also revalue, simultaneously, the 151,890 tons of gold which are thought to be in private hands at present - 183,000 tons total, minus 31,110 tons held by Central Banks = 151,890 tons in private hands. For China, the revaluation of gold means an end to the great export trade of Chinese manufactures, with the consequent inevitable, and surely very wrenching re-ordering of its economy. Perhaps this explains why the Chinese government has been urging the population of China to purchase gold. China, which is rumored to have far more gold in its Reserves than it says it does, might have the opportunity to lend say, 50 tons of the yellow metal to each of 50 hard-hit countries, for a total of an insignificant 2,500 tons out of its large stash. In return, the recipient countries would place Chinese on the Boards of their Central Banks and as supervisors in their National Treasuries; in addition, China might obtain privileges to invest in the extraction of scarce natural resources or in agriculture - China has a huge population that will require establishing sources of food. Nothing comes without a price, and "he who has the gold makes the rules". The Chinese are well-known as consummate merchants and as people who know how to live unobtrusively in foreign countries. China's influence may extend around the world, with the world's return to gold-backed currencies. For the US, the revaluation of gold means an end to its ability to obtain any goods it desires, in any quantity, in any place, at any price by simply tendering today's mighty fiat Dollar in mock-payment, in exchange for those goods. The US economy will have to suffer a huge and also painful, wrenching adjustment to its new situation in a different world, where balanced trade and balanced budgets are relentlessly imposed by the new status of gold as international money. On the positive side, US manufacturing will immediately spring to life to supply the US market; employment and incomes will surge with the rebirth of US manufactures. Once all currencies are "gold-backed" by revalued gold reserves, then gold is once again the international money, and the Dollar becomes nothing more than the national currency of the US, as quantities of gold become the international means of settling trade. We need not worry ourselves about how this will take place, because that it will happen is a certainty. All prices of goods and services around the world will really be gold prices, since all currencies will be redeemable at sight, in gold. Such is the significance of the coming revaluation of gold.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 02 Feb 2016 06:50 PM PST Well, don't say we didn't warn you. Just yesterday, in the course of documenting the largest ponzi scheme the world has ever known (in terms of number of victims), we remarked that if China's beleaguered masses needed yet another excuse to rise up and stage massive street protests, they got one in the form of online P2P lender Ezubao, which defrauded nearly a million people. Ezubao's model wasn't exactly complicated. Investors, they said, could earn between 9% and 15% by funding a variety of projects presented on the company's website. When the money came in, management simply absconded with it all and attempted to repay old investors with new investors' money. 34-year-old Ding Ning - the company's founder - had a penchant for spending investors' hard earned money on things like CNY12 million pink diamond rings. "Among gifts that Yucheng Chairman Ding Ning gave his president, Zhang Min, were a $20 million Singapore villa, a $1.8 million pink diamond ring, luxury limousines and watches and more than $83 million in cash," Reuters recounts, before adding that "Zhang, the group president who was marketed as 'the most beautiful executive in online finance', said on state broadcaster CCTV that Ding asked her to buy up everything from every Louis Vuitton and Hermès store in China, "and go overseas to buy more if that wasn't enough."

(Ding Ning at an "undisclosed location") According to a highly amusing Google translation of a Xinhua story, Ding Ning and "several closely related groups of female executives, their private life extremely extravagant, spendthrift to suck money." Yes, "spendthrift to suck money" and if there was anything Ezubao was particularly adept at, it was "sucking money" - from 900,000 unsuspecting Chinese who staged protests in December following the government's move to freeze the company's assets. "Expect more protests to come," we warned. Well sure enough, disgruntled investors are now uniting in a nationwide "rights protection" movement. Their first order of business: to call for three days of protests. "If we don't protect our rights, make appeals and take other drastic action within three days, we will recover little," said a bulletin making the rounds among Ezubao investors. "We need to rise up across the country and let the government know that the people's bottom line is the return of their capital. If it is not returned our movement will not stop!" Many investors were lured in by the company's flashy advertising campaigns and gimmicks. "Ezubao expanded rapidly across the country by advertising extensively on Chinese Central Television." FT writes. "It sponsored a forum about the country's parliament on Xinhua's website and sponsored popular events such as the China Open tennis tournament and emblazoned high-speed rail cars with its logo." "When you got on the train, there was an announcement saying: "'Welcome aboard Train Ezubao'," a company employee who lost about CNY100,000 yuan in the scheme told Reuters. Investors who put up at least CNY150,000 were given five-gram commemorative gold bars. "I feel terrible," an Ezubao investor surnamed Liu who said she lost CNY800,000 lamented. "I haven't dared tell my husband yet." "I gave Ezubao Rmb250,000 because of their association with government activities and news outlets," one investor told FT. "Of course we invested because of the advertising on CCTV and the high-speed trains," another said. "Of course" they invested. They saw an ad on a train. This mirrors the sentiments expressed by the millions of retail investors who watched helplessly last summer as their life savings were vaporized by the harrowing decline on the SHCOMP. It also reminds us of what happened to Fanya Metals chief Shan Jiuliang who was kidnapped by a mob of angry investors and dropped off at the police station back in August. Although Fanya was probably less of a fraud than Ezubao, the underlying story is the same: unsophisticated Chinese investors were bamboozled and once they realized they had been had, they were out for blood. It's not likely that Ding Ning will see the light of day anytime soon, but if he were to go free, he might quickly wish he was back in prison given the fate Shan Jiuliang suffered early one morning last summer...

So stay tuned, because judging from the tone of the "rights protection movement" bulletin excerpted above, the villagers may be about to rise up in China. Oh, and as for whether there may be other Ding Nings and Ezubaos lurking around in China just waiting to buckle under the weight of their own extraordinary ponzi-ness, consider this from Reuters:

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Why Bernie Sanders Has To Raise Taxes On The Middle Class Posted: 02 Feb 2016 06:15 PM PST Submitted by Daniel Bier via The Foundation for Economic Education, Willie Sutton was one of the most infamous bank robbers in American history. Over three decades, the dashing criminal robbed a hundred banks, escaped three prisons, and made off with millions. Today, he is best known for Sutton’s Law: Asked by a reporter why he robbed banks, Sutton allegedly quipped, “Because that’s where the money is.” Sutton’s Law explains something unusual about Bernie Sander’s tax plan: it calls for massive tax hikes across the board. Why raise taxes on the middle class? Because that’s where the money is. The problem all politicians face is that voters love to get stuff, but they hate to pay for it. The traditional solution that center-left politicians pitch is the idea that the poor and middle class will get the benefits, and the rich will pay for it. This is approximately how things work in the United States. The top 1 percent of taxpayers earn 19 percent of total income and pay 38 percent of federal income taxes. The bottom 50 percent earn 12 percent and pay 3 percent. This chart from the Heritage Foundation shows net taxes paid and benefits received, per person, by household income group:

But Sanders’ proposals (free college, free health care, jobs programs, more Social Security, etc.) are way too heavy for the rich alone to carry, and he knows it. To his credit, his campaign has released a plan to pay for each of these myriad handouts. Vox’s Dylan Matthews has totaled up all the tax increases Sanders has proposed so far, and the picture is simply staggering. Every household earning below $250,000 will face a tax hike of nearly 9 percent. Past that, rates explode, up to a top rate of 77 percent on incomes over $10 million.

Paying for Free Sanders argues that most people’s average income tax rate won’t change, but this is only true if you exclude the two major taxes meant to pay for his health care program: a 2.2 percent “premium” tax and 6.2 percent payroll tax, imposed on incomes across the board. These taxes account for majority of the new revenue Sanders is counting on. But it gets worse: his single-payer health care plan will cost 80 percent more than he claims. Analysis by the left-leaning scholar Kenneth Thorpe (who supports single payer) concludes that Sanders’ proposal will cost $1.1 trillion more each year than he claims. The trillion dollar discrepancy results from some questionable assumptions in Sanders’ numbers. For instance:

So unless pharmaceutical companies start paying you to take their drugs, the Sanders administration will need to increase taxes even more. Analysis by the Tax Foundation finds that his proposed tax hikes already total $13.6 trillion over the next ten years. However, “the plan would [only] end up collecting $9.8 trillion over the next decade when accounting for decreased economic output.” And the consequences will be truly devastating. Because of the taxes on labor and capital, GDP will be reduced 9.5 percent. Six million jobs will be lost. On average, after-tax incomes will be reduced by more than 18 percent. Incomes for the bottom 50 percent will be reduced by more than 14 percent, and incomes for the top 1 percent will be reduced nearly 25 percent. Inequality warriors might cheer, but if you want to actually raise revenue, crushing the incomes of the people who pay almost 40 percent of all taxes isn’t the way to go. These are just the effects of the $1 trillion tax hike he has planned — and he probably needs to double that to pay for single payer. Where will he find it? He’ll go where European welfare states go. Being Like Scandinavia Sanders is a great admirer of Scandinavian countries, such as Denmark, Sweden, and Norway, and many of his proposals are modeled on their systems. But to pay for their generous welfare benefits, they tax, and tax, and tax. Denmark, Norway, and Sweden all capture between 20-26 percent of GDP from income and payroll taxes. By contrast, the United States collects only 15 percent. Scandinavia’s tax rates themselves are not that much higher than the United States’. Denmark’s top rate is 30 percent higher, Sweden’s is 18 percent higher, and Norway’s is actually 16 percent lower — and yet Norway’s income tax raises 30 percent more revenue than the United States. The answer lies in how progressive the US tax system is, in the thresholds at which people are hit by the top tax rates. The Tax Foundation explains,

The reason European states can pay for giant welfare programs is not because they just tax the rich more — it’s because they also scoop up a ton of middle class income. The reason why the United States can't right now is its long-standing political arrangement to keep taxes high on the rich so they can be low on the poor and middle.

Where the Money Is – And Isn’t As shown by the Laffer Curve, there is a point at which increasing tax rates actually reduces tax revenue, by discouraging work, hurting the economy, and encouraging tax avoidance.

Bernie’s plan already hammers the rich: households earning over $250,000 (the top 3 percent) would face marginal rates of 62-77 percent — meaning the IRS would take two-thirds to three-quarters of each additional dollar earned. His proposed capital gains taxes are so high that they are likely well past the point of positive returns. The US corporate tax rate of 40 percent is already the highest in the world, and even Sanders hasn’t proposed increasing it. The only way to solve his revenue problem is to raise rates on the middle and upper-middle classes, or flatten the structure to make the top rates start kicking in much lower. You can see why a “progressive” isn’t keen on making more regressive taxes part of his platform, but the money has to come from somewhere. The bottom fifty percent don’t pay much income tax now (only $34 billion), but they also don’t earn enough to fill the gap. Making their taxes proportionate to income would only raise $107 billion, without even considering how the higher rates would reduce employment and income. The top 5 percent are pretty well wrung dry by Sanders’ plan, and their incomes are going to be reduced by 20-25 percent anyway. It’s hard to imagine that there’s much more blood to be had from that stone. But households between the 50th and the 95th percentile (incomes between $37,000 to $180,000 a year) earn about 54 percent of total income — a share would likely go up, given the larger income reductions expected for top earners. Currently, this group pays only 38 percent of total income taxes, and, despite the 9 percent tax hike, they’re comparatively spared by the original tax plan. Their incomes are now the lowest hanging fruit on the tax tree. As they go to the polls this year, the middle class should remember Sutton’s Law.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Bank Of Japan Has Betrayed Its People Posted: 02 Feb 2016 05:05 PM PST The Bank of Japan’s unexpected rate cuts to negative are a desperate attempt to help out the FED and to support the dollar at the expense of the aging Japanese population. The negative market reaction to the FED’s rate hike of December shows that investors do not believe an economic recovery in the US is underway. Two reasons make central banks start to raise interest rates.

We saw this last pattern happening in the US economy after the December FED’s rate hike. As a result, the dollar-yen exchange rate is starting to decline, with the value of the dollar falling off as Japanese investors start panicking and fleeing the US market. Surely, Japanese investors know that a rate hike without an accompanying economic growth will erode every existing investment. There is a general misconception according to which countries drive their currency down to generate growth. People adhere to the simplistic belief that a weak currency drives exports and helps the nation to prosper. The fact is that a cheap currency creates growth by giving away real goods in exchange for IOU (I Owe Yous) or paper debt obligations that will never be repaid. The US is the beneficiary or the receiving end of the weak yen policy. Because the US continues to maintain its world hegemony, it needs a strong dollar. A strong dollar makes everything the US empire buys in the world cheap. A strong dollar causes the world to be willing to exchange real goods for printed paper dollars that have no intrinsic value, and that are issued by a country that does not have the industrial capacity to ever repay what it owes its debtors. The endless trade deficit the US has with Japan shows how the Japanese are prepared to provide the US with real goods without demanding tangible goods in return. Because the international press publishes trade data in dollars, the trade balance deficit seems to have been shrinking over the last years. The actual situation becomes apparent if we look at the trade deficit in yens.

The US trade deficit with Japan is growing bigger and bigger year after year, as Japanese producers are giving away a big chunk of their production to US consumers in return for more and more US paper debt. By manipulating the yen, Japanese authorities are giving away a real part of their GDP that they take from their people to the US empire. In January, the yen started to appreciate because Japanese investors withdrew their money from the shaky US economy. Not only does an expensive yen lower the purchasing power of US consumers, but it can also render the US, Asian military pivot, quite expensive. It looks like Kuroda-san, president of the Bank of Japan, got new marching orders from his US masters during his Davos visit. The submissive Japanese leaders have no choice but to obey their US masters and come up with a next trick to keep the yen cheap. The Bank of Japan does not have much room to maneuver, so it lowered the excess-deposit rate into negative territory. It was marginal from 0.1 to -0.1 and only applicable to a small number of the Japanese bank deposits at the Bank of Japan; nevertheless, the music started playing again. It will be harder for Kuroda-san to press the yen lower and come up with new tricks indefinitely. Investors may be fooled by the vast amount of public debt of the Japanese government, not realizing that the Japanese nation as a whole has a massive saving surplus. Some day the Bank of Japan will run out of tricks, and the yen will explode as Japanese savers will try to repatriate their savings. It will affect not only the financial markets but also the US ability to counter its Chinese rival in the Yellow Sea. For now, the desperate move of the Central Bank of Japan will not help the aging Japanese population. It will keep the financial markets happy for a short period. ...or not even that...

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| "Hidden Planet X" Could Be In Orbit!! Posted: 02 Feb 2016 04:30 PM PST Scientific American explains the process of the coming Planet X The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many more [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TF Metals Report: Connecting the Comex dots Posted: 02 Feb 2016 04:20 PM PST 7:20p ET Tuesday, February 2, 2016 Dear Friend of GATA and Gold: The TF Metals Report's Turd Ferguson today finds what seems like confirmation that Comex gold deliveries are just metal passed back and forth among the same bullion banks -- a charade. Ferguson's commentary is headlined "Connecting the Comex Dots" and it's posted at the TF Metals Report here: http://www.tfmetalsreport.com/blog/7420/connecting-comex-dots CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT Silver Coins and Rounds with Employee Pricing and Free Shipping Grab your Silver Starter Kit at cost from Money Metals Exchange, the company named "Precious Metals Dealer of the Year" by industry ratings group Bullion Directory. Simply go to MoneyMetals.com and type "GATA" in the radio box at the top of the page. This special silver offer contains 4 ounces of silver coins and rounds in the most popular 1-ounce, half-ounce, and 10th-ounce forms. Claim yours now, because GATA readers get employee pricing and free shipping. So go to -- -- and type "GATA" in the radio box at the top of the page. Support GATA by purchasing recordings of the proceedings of the 2014 New Orleans Investment Conference: https://jeffersoncompanies.com/landing/2014-av-powell Or by purchasing DVDs of GATA's London conference in August 2011 or GATA's Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Here's How Much The Strong Dollar Hurts US Companies Posted: 02 Feb 2016 04:00 PM PST Submitted by Tony Sagami via MauldinEconomics.com, “At current spot rates, we would expect a significant impact to revenue and profit again in 2016.” We’re in the middle of earnings season, and one of the themes I am hearing over and over from American companies is how the strong dollar is killing their profits. How strong? Since mid-2014, the US dollar has appreciated about 15% against a basket of trade-weighted foreign currencies. In 2015 alone, it was up 12%, the biggest one-year gain since the 1970s.

If you’ve traveled abroad recently, you know exactly what I’m talking about. While a strong dollar is a positive for vacationing Americans, it is bad, bad news for American companies with significant international business because it makes US exports more expensive to foreign buyers and reduces the conversion of foreign profits from foreign currencies into dollars.

And it is only going to get worse. Wall Street economists predict that the US dollar will appreciate by another 4% against the euro and by another 6% against the Japanese yen. In the third quarter of 2015, the strong US dollar decreased the average American company’s earnings by 12 cents per share, and a growing list of American companies are suffering even more dollar-related pain. Dollar Casualty #1: Kimberly-ClarkKimberly-Clark sells a lot of Huggies diapers all around the world. However, it reported that its 2015 revenues were down by 6%. Worse yet, it warned Wall Street that its 2016 revenues would fall by another 3%. That sounds like business is bad, but Kimberly-Clark is actually pulling in more sales than ever. It is just the currency impact that makes its business look awful—if it weren’t for the effect of the strong US dollar, management said sales would actually be up 3%–5%.

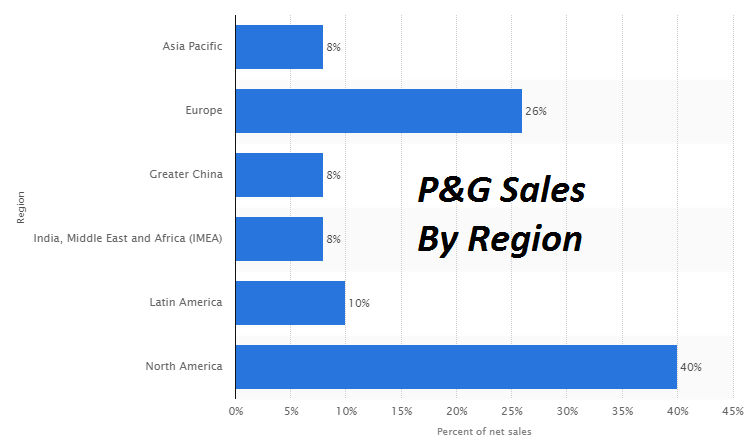

Dollar Casualty #2: Procter & GambleProcter & Gamble gets 60% of its revenues from outside of North America, so it is one of the most vulnerable companies to a rising US dollar.

The company reported a 9% drop in quarterly revenues to $16.9 billion because of the dollar.

Dollar Casualty #3: Johnson & JohnsonJohnson & Johnson said its revenues were reduced by 7.5% in 2015 by currency losses.

Dollar Casualty #4: MonsantoMonsanto is the world's largest seed company and gets 43% of its revenues from outside the US. The company just reported a loss for the fourth quarter of 2015, citing the strong dollar as one of the main reasons. It also cut its 2016 profit forecast from $4.44–$5.01 per share to $4.12–$4.79 per share.

Dollar Casualty #5: DuPontChemical company DuPont reported a quarterly loss of $0.29 per share, compared with a net income of $0.74 per share a year earlier. Sales slid 9.3% to $5.3 billion, but without the effect of the strong dollar, sales would have been down only 1%.

A 1% decline isn’t good, but a 9.3% is horrendous. Dollar Casualty #6: 3M3M, the maker of Post-it Notes, gets about two-thirds of its revenues from outside the US, and that global reach has cost it dearly. 3M reported an 8.3% drop in profits to $1.66 per share and expects the currency effects to reduce this year’s earnings by 5%. “The Dollar Dog Ate My Homework”Those are just a few examples from last week. We are certainly going to hear a lot more companies blaming the strong dollar for disappointing earnings. And those the-dog-ate-my-homework excuses are going to continue for the rest of 2016. Here’s what you need to do: Take a look at every stock you own and find out what percentage of the company’s revenues comes from outside the US. If the answer is more than 40%, you should consider dumping the stock before the dollar shrinks profits (and stock price) even more. There are always exceptions—but fighting the strong dollar is going to be a battle that your portfolio is going to lose.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold Daily and Silver Weekly Charts - More 'Flight To Safety' - Active February Posted: 02 Feb 2016 02:01 PM PST | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Nostradamus : What Will Happen When The Dollar Collapse In 2016 Posted: 02 Feb 2016 02:00 PM PST Nostradamus : What Will Happen When The Dollar Collapse In 2016This collapse will be global and it will bring down not only the dollar but all other fiat currencies,as they are fundamentally no different. The collapse of currencies will lead to the collapse of ALL paper assets. The... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Defying Wall Street for “Knock Your Socks off” Returns Posted: 02 Feb 2016 01:53 PM PST This post Defying Wall Street for "Knock Your Socks off" Returns appeared first on Daily Reckoning. We did it! "The national debt hit $19 trillion for the first time ever…" reports the Washington Examiner." It clocked in at $19.012 trillion, to be exact. At this rate, Obama will have no problem at all eclipsing $20 trillion by the time Trump or Clinton takes office next year. To think, the debt was "only" $8 trillion while we were filming our documentary I.O.U.S.A. It was before the bailouts and stimulus… before Obamacare… before protracted wars in the Middle East… Before the Federal Reserve printed trillions of dollars out of thin air, too, and kept interest rates close to 0%. So doing, it's earned its keep as a bubble machine. Ever since I wrote my best-selling book Financial Reckoning Day in 2003, I've been warning about the dangers of government market manipulation and excessive debt. While the day of reckoning hasn't arrived yet, it's hard to deny the dangers of our financial system. With the boom-and-bust environment created by the Fed, it seems the next market collapse is just around the corner. More important, making money in the markets has become extremely difficult. You can't simply follow the traditional "buy and hold" strategy. If you park your cash in "safe" government bonds, CDs or other money market accounts, you'll collect almost nothing in income. On the other hand, if you "buy and hold" stocks, you risk losing half of your portfolio or more during the next market crash. "Price" matters. Knowing when to get into a trade is important. Knowing when to get out has never been more vital. It could mean the difference between a comfortable retirement and just getting by. And that brings us back to yesterday's topic… "Add a '+' in the right column getting Michael Covel to join your team" writes one reader after yesterday's Daily Reckoning. "I am serious, nicely done!" The response to yesterday's announcement has been gratifying. To show why, let me give you some more background on why we thought it so important to bring Michael Covel's work to you. Turns out that Michael and I both had a penchant for economic documentaries — not just watching them but making them. I'd just finished releasing my attempt, the aforementioned I.O.U.S.Α., a "big budget" movie arduously detailing the four great deficits the U.S. faces: savings, trade, fiscal, and, the worst, leadership deficits. While the film was nominated for a Golden Globe and shortlisted for an Academy Award, it turned out to be a very expensive education in filmmaking, marketing, and dealing with Hollywood. Likewise, Michael had a similar experience. While chatting over drinks at Richard Russell's birthday party, Michael told me about a documentary film he'd written and produced on his own on a similar subject. Michael's take was simply titled Βroke: The New Αmerican Dream. Through both films, we explored the depths of the debt-fueled global economy and the often-disastrous outcomes people get when they expect a free-ride gravy train to continue indefinitely. During one scene in Βroke, Michael visits the largest open-air fish market in the world, the Tsukiji Market in Tokyo. Fishmongers bellow and screech at each other until prices are reached for fish hauled in fresh from the trawlers by the ton. It's here Michael explores one of the second things we discovered we have in common — a passionate awe for free markets. A properly functioning free market allows millions of buyers and sellers to determine prices between themselves, without the heavy thumb of government regulation or coercion of monopolies and price-fixing schemes. (If you haven't seen Broke, the fish market scene alone is worth the effort.) To kick off this partnership, I asked Michael to develop a simple proprietary trading system for our readers… one that will help you make money in up and down markets. Luckily for you, he's accepted and even relishes the challenge. You can click here to see how to put it to work for you. We dispatched our publisher, Pete Coyne, to talk with Covel about it. Read on for an excerpt… Cheers, Addison Wiggin P.S. Whither goes the economy and the financial markets, so goes The Daily Reckoning. You'd think "contrarian" opinions would react counter to the broader trends in the marketplace, but that's just not true. When the markets — stock, bond, housing, credit, you name it — are on fire, the marketplace for new and interesting ideas is on fire too. To make sure you're accessing that entire marketplace — rather than just the small sliver offered you by the mainstream financial media — we invite you to join us in our email edition by signing up for FREE, right here. The post Defying Wall Street for "Knock Your Socks off" Returns appeared first on Daily Reckoning. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| America is like Israel – Chris Steinle at The Prophecy Club Radio Posted: 02 Feb 2016 01:33 PM PST Stan Johnson interviews the author of "Come Out of Her My People", Chris Steinle. Air date: 2012-08-13 The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Slouching Toward The Dark Side Posted: 02 Feb 2016 12:27 PM PST This post Slouching Toward The Dark Side appeared first on Daily Reckoning. Last Wednesday we noted there is something rotten in the state of Denmark, meaning that the world's great potemkin village of Bubble Finance is unraveling. The evidence piles up by the day. To wit, now comes still another story about the Red Paddy Wagons rolling out in China. This time they are rounding-up the proprietors of a $7.6 billion peer-to-peer (P2P) lending Ponzi called Ezubao Ltd.

The particulars of this story are worth more than a week of bloviating by the Wall Street economists, strategists and other shills who visit bubblevision the whole day long. That's because it exposes the rotten foundation on which the entire Red Ponzi and the related world central bank regime of Bubble Finance is based. Needless to say, these dangerous, unstable and incendiary deformations are not even visible to the Keynesian commentariat and policy apparatchiks. They blithely assume that what makes modern economies go is the deft monetary, fiscal and regulatory interventions of the state. By their lights, not much else matters——and most certainly not the condition of household, business and public balance sheets or the level of speculation and leveraged gambling prevalent in financial markets and corporate C-suites. As that pompous fool and #2 apparatchik at the Fed, Stanley Fischer, is wont to say—–such putative bubbles are just second order foot faults. These prosaic nuisances are not the fault of monetary policy in any event, and can be readily minimized through a risible scheme called "macro-prudential" regulation. After all, if the Keynesians had any inkling that debt was a problem they wouldn't have attempted to radically subsidize it with 84 straight months of ZIRP. In that respect, they might especially have noted that US credit outstanding has soared from $54 trillion to $63 trillion or 17% since the eve of the financial crisis. That is, since the nation's mountain of debt blew-up the first time around.

So here's what happened with Ezubao. It's parent (Yucheng Group) was an equipment leasing operation, having gotten started way back near the dawn of the Red Ponzi. That is, it apparently started about 2012 in the business of supplying rentable equipment and factoring services via the shadow banking system during China's fixed asset boom. Yucheng Group was definitely not China's equivalent of General Electric; it was apparently organized by a gang of military buccaneers who have occupied a certain Chinese speaking province of northern Myanmar. But by July 2014 the infrastructure boom and leasing demand were cooling so it opened up a new operation in P2P lending. Quicker than a flash it became China's #2 player in that suddenly flourishing sector, or as the company described it:

Well, not exactly. Ezubao was shutdown on December 8th by Chinese authorities, meaning that in just 18 months it had bilked 900,000 investors of nearly $8 billion in a fraud that was so blatant that it now appears upwards of 95% of investor deposits never were invested at all. Some of the money was just send back to earlier investors, upwards $1 billion apparently went to fund the company's military adventures in Myanmar and the rest to fund the chairman's lavish lifestyle. The company's leader was perhaps appropriately named Ding Ning, and according to today's Wall Street Journal,

Charles Ponzi himself might have been impressed, but apparently not its gullible P2P lenders. As one smaller investor told a Caixin reporter,

No, Ezubao wasn't a one-off outlier. It reflects the sum and substance of the craziest credit and construction boom in human history. As I noted last week:

Or as Jim Kunstler put it this morning,

Accordingly, China has become such a den of speculative madness that one giant scam after another literally springs up over night. During about 60 trading days between March and mid-June of 2015, for instance, China's stock market soared by $4 trillion and margin loans and other speculative capital poured into its 379 million trading accounts literally like lemmings surging toward the sea. At the peak, margin debt accounted for 18% of the entire market cap of traded stocks. Most of that $4 trillion disappeared in less than 20 trading days through the June/early July crash last year. And not withstanding the subsequent massive stock buying by the authorities and the police state dragnet thrown up against stock sellers, more than $8 trillion has now completely evaporated after January's wipeout on the Shanghai market. The P2P lending story is the same. As investors sought alternatives to the sagging real-estate market and volatile stocks, they poured into online peer-to-peer lending platforms with alacrity. According to the WSJ, there were 2,600 platforms operating at the end of 2015 compared to only 800 twenty-four months earlier. More significantly, the outstanding volume of loans soared from $5 billion to $67 billion during the same period. That's right. Another 14X eruption in no time flat——so not surprisingly P2P lending has become one steaming pile of financial crap:

Nor is this the only scam that came to light over the weekend with respect to the Red Ponzi. It turns out that a certain kind of shadow banking system instrument called Directional Asset Management Plans (DAMPs) or Trust Beneficiary Rights (TBRs) have soared from $300 billion in 2012 to $1.8 trillion at present. Yes, this is another 6X eruption in record time, but it doesn't take much investigation to see what is going on. Bad loans are literally being vacuumed off bank balance sheets into phony SIV-like entities of Citigroup circa 2007 vintage, and then carried not as loans but "investment receivables". And then, presto, the challenges of NPLs, capital support and bad debt charges to the income statements disappear entirely. As explained by one journalistic account,

Needless to say, there is an endless amount of financial madness where Ezubao, DAMPs and TBRs came from. Yet China is only the tip of the iceberg. If China's buccaneers and gamblers are slightly more crude, what they are doing is essentially no different than the outpouring of OTC structured finance deals manufactured day in and day out by Goldman Sachs and the rest of the world's financial market banksters. And they don't even compare to the financial scam that is at the very heart of present day central banking. No one with a passing acquaintance with history and logic could believe that any Ponzi can be sustained for very long; nor is it possible to believe that massive debt monetization via printing press credit and a sustained regime of negative real, and now nominal, interest rates will not eventually end in catastrophe—–most especially in a world where governments positively cannot stop accruing unrepayable and soon unserviceable debt. Yet after last Friday's lunatic move to negative interest rates by the BOJ, the Japanese 10-year bond is now trading at just 6 basis points; and it will be in negative territory along with all of the government's shorter maturities any day now. So why would Mr. Ding Ning not have a go at the blatant Ponzi reflected in Ezubao? Japan's work force and population is disappearing into a colossal demographic bust; its fiscal deficit is still upwards of 40% of its annual budget outlays; and its national debt is off the charts. So as its retirees liquidate their savings at an accelerating rate, Japan will desperately need to borrow from the rest of the world to support its old age colony.

What it has elected to do, however, is trash its currency and ensure that in a few short years its monetary system will collapse. There can be no other result because negative interest rates will cause capital to flee, even as its massive bond purchase programs swallows up most of the public debt, along with an increasing quotient of corporate bonds and even ETFs and stock. In a word, the utter fools running Japan Inc. have become so befuddled by Keynesian groupthink that they are self-inflicting a monetary Hiroshima on their entire economy and society. Likewise, the madness of NIRP is probably no longer containable since it already infects the eurozone, Sweden, Switzerland, Denmark, Japan——-and, after last night's shocking trade report for January, South Korea can't be far behind. Its exports are now down 18.5% year over year, and have plunged to levels not seen since the bottom of the Great Recession. Literally speaking, world trade is being asphyxiated by the deflationary burden of the $225 trillion credit bubble created by the Fed and its fellow-traveling convoy of global central banks over the last two decades. And now they are aggressively making matters worse by doubling down on a monumentally failed experiment in crank economics. Already they have driven nearly $6 trillion of sovereign debt below the zero bound. Even a decade ago every student of economics 101 knew that is a recipe for calamity.

Yet now just a few dozen monetary apparatchiks in the world's major central banks and their shills in the world's financial casinos are driving the system straight toward the monetary dark side. What will be uncovered when it finally blows will cause the depredations of Charles Ponzi and Mr. Ding Ning to be reduced to mere footnotes in the annals of monetary infamy. Regards, David Stockman P.S. Be sure to sign up for David Stockman's Contra Corner —the only place where mainstream delusions about the Warfare State, the Bailout State, Bubble Finance and Beltway Banditry are ripped, refuted and rebuked. Click here and subscribe to receive David Stockman's latest posts by email each day as well as his personally curated insights and analysis from leading contrarian thinkers. The post Slouching Toward The Dark Side appeared first on Daily Reckoning. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Global Economy Could Fall Farther and Faster Than Pundits Expect Posted: 02 Feb 2016 09:46 AM PST This post Global Economy Could Fall Farther and Faster Than Pundits Expect appeared first on Daily Reckoning. The core narrative of central bank/cartel capitalism is centralized agencies have the power to limit downturns and extend credit-based “good times” almost indefinitely. The centralized power bag of tricks includes fiscal policies such as deficit spending to boost “aggregate demand” in downturns and monetary policies such as lowering interest rates to zero and buying assets, a.k.a. quantitative easing. If we crawl under the barbed wire and escape the ideological Keynesian Concentration Camp, we find thinkers such as Ugo Bardi, John Michael Greer and Dimitry Orlov, whose work explores the dynamics of collapse, resilience and sustainability. All three have added a great deal to my own (emerging) understanding of the many dynamics of collapse. We can summarize the dynamics of collapse in many ways; here’s one: collapse is latent fragility manifesting. A familiar (and tragic) health analogy offers an example: a middle-aged man doesn’t appear ill, a bit thick around the middle perhaps, but neither he nor his intimates can see the fragility of his clogged arteries and blood-starved heart. Seemingly “out of the blue,” the man has a massive heart attack and passes from this Earth, to the shock of everyone who knew him. Financial collapse isn’t “out of the blue,” any more than a heart attack is “out of the blue.” Actions and choices have consequences, and as resilience and redundancy are slowly stripped from complex systems, systemic fragility builds beneath the surface. At some difficult-to-predict point, a threshold is reached and the complex system fails. In the financial realm, fragility builds as the system relies ever more heavily on marginal lenders, borrowers, buyers and investments for its “growth.” The current “recovery” (smirk) is completely dependent on marginal lenders (China’s shadow banking), borrowers (auto buyers taking subprime 7-year loans), buyers (corrupt Chinese officials buying $3 million homes in Vancouver B.C. with their ill-gotten gains) and investments (empty malls, empty factories, stock buy-backs, etc.). The problem for “growth” based on the fragile margins is that the entire system becomes fragile as a direct result of this dependence on fragile margins. The current global real estate bubble is predicated on one condition: that the supply of corrupt Chinese officials fleeing China with ill-gotten millions to invest overseas is endless. But no supply of corrupt officials, even in China, is truly endless, and markets based on this thin edge of corrupt capital will collapse once the corrupt capital dries up. The same can be said of marginal oil production, marginal auto/truck buyers, marginal cafes, marginal malls, etc. When fragile (i.e. highly risky) shadow banking becomes a dominant force in credit, the system itself becomes fragile. Conventional economists are entirely blind to system fragility. There is no ready Keynesian Cargo Cult econometric formula that measures systemic fragility, so it simply doesn’t exist within conventional economics. This is why financial panics and collapses always appear (like fatal heart attacks) to be “out of the blue” to conventional economics. I propose that the Global Recession of 2016 will trace the Seneca Cliff as described by Ugo Bardi. This application may not align with Bardi’s own work, and I want to make it clear this application is my own, not Bardi’s. But I think a strong case can be made that the global financial/economic system is primed for a ride down the Seneca Cliff:

Recall that the global “recovery” 2009 – 2015 was entirely based on the expansion of debt taken on by marginal borrowers. Systemic fragility doesn’t respond to central bank jawboning or Keynesian claptrap; unlike those “policy tools,” fragility is real. Regards, Charles Hugh Smith P.S. Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible. And like most of you, the way I've moved toward my goal has always hinged not just on having a job but a career. You don't have to be a financial blogger to know that "having a job" and "having a career" do not mean the same thing today as they did when I first started swinging a hammer for a paycheck. Even the basic concept "getting a job" has changed so radically that jobs–getting and keeping them, and the perceived lack of them–is the number one financial topic among friends, family and for that matter, complete strangers. So I sat down and wrote this book: Get a Job, Build a Real Career and Defy a Bewildering Economy. It details everything I've verified about employment and the economy, and lays out an action plan to get you employed. I am proud of this book. It is the culmination of both my practical work experiences and my financial analysis, and it is a useful, practical, and clarifying read. The post Global Economy Could Fall Farther and Faster Than Pundits Expect appeared first on Daily Reckoning. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Bron Suchecki: Would you risk going to jail to fix the fix? Posted: 02 Feb 2016 09:28 AM PST 12:27p ET Tuesday, February 2, 2016 Dear Friend of GATA and Gold: Perth Mint research director Bron Suchecki today compiles many criticisms and complaints about the new London silver price fix, whose seeming malfunction last week has become a bit scandalous. There seems to be much opinion that bullion banks and traders, fearing accusations of market manipulation, are increasingly unwilling to trade simultaneously off the fix when they might need to hedge their trades with futures contracts. If so, one might think that this serves all of them right, since so much of the monetary metals market is secretive and its bigger participants are essentially agents of central banks, whose objectives long have included currency and commodity market rigging: http://www.gata.org/node/14839 Let them trying doing their rigging in the open again, as they did in the era of the London Gold Pool. Suchecki's commentary is headlined "Would You Risk Going to Jail to Fix the Fix?" and it's posted at the Perth Mint's research page here: http://research.perthmint.com.au/2016/02/02/would-you-risk-going-to-jail... CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT Free Storage with BullionStar in Singapore Until 2016 Bullion Star is a Singapore-registered company with a one-stop bullion shop, showroom, and vault at 45 New Bridge Road in Singapore. Bullion Star's solution for storing bullion in Singapore is called My Vault Storage. With My Vault Storage you can store bullion in Bullion Star's bullion vault, which is integrated with Bullion Star's shop and showroom, making it a convenient one-stop-shop for precious metals in Singapore. Customers can buy, store, sell, or request physical withdrawal of their bullion through My Vault Storage® online around the clock. Storage is FREE until 2016 and will have the most competitive rates in the industry thereafter. For more information, please visit Bullion Star here: Support GATA by purchasing DVDs of GATA's London conference in August 2011 or GATA's Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 02 Feb 2016 09:08 AM PST This post Saudi Arabia and Oil’s Future appeared first on Daily Reckoning. Is Saudi Arabia cash strapped? Saudi Arabia still has money, but if the oil price stays here for another three years the country’s basically bankrupt. In my opinion, the whole Middle East will go back to where they came from — deserts. The oil price for the Middle East, considering the huge population increase they had since 1970, needs to be around $80 a barrel. But maybe for world peace it’s better if the oil prices are nearer to $30 or $40 and the Saudis can’t finance ISIS or other adventures that may not be very desirable. But at $40 they have a huge problem. Their reserves will come down substantially. Now instead of drawing down their reserves they can borrow money. I wouldn’t necessarily lend money to Saudi Arabia personally. But maybe some governments will do so. As for the price of oil, it’s very oversold and sentiment is very bearish. Many analysts – to whom actually investors shouldn’t listen – said when the oil price was around $90 that it would go to $150. Now they are saying it will go down to $10. They were wrong once; they will probably be wrong another time. But I don’t know. The problem with modern central banking is that the Keynesianism upon which they are essentially intervening rests on the argument that their fiscal and monetary interventions can smooth out the business cycle. In other words, you have less fluctuations, you have less booms and you don’t have depressions. But in reality, the central banking forces have created much more volatility. When you think, the euro is the second largest currency in the world and it dropped 40% in less than two years. Same for the yen. So they have actually created more volatility, not less, and because commodity prices went up for a while while there were artificially low interest rates, everybody was exploring for oil and also for gold and silver and other commodities. That’s why the supply now is quite large. The demand was driven mostly by China. But China had a massive capital spending boom — also because of easy credit, and so they overbuilt capacities. Now the demand is less and the supply is increasing so the prices dropped a lot. My view would be that the equilibrium price is somewhere between $30 and, say, $50. Oil could drop if there is a lot of liquidation to, say, $20 or even $15. It’s possible. But to realign demand and supply in the long run, I think an oil prices of around or more than $60 is required because at $40 nobody makes money so nobody will explore for oil. That will then tighten the market over time, but not immediately. That could take time. A client just asked me whether he should buy oil. I told him I don’t know. Regards, Marc Faber P.S. Be sure to sign up for The Daily Reckoning — a free and entertaining look at the world of finance and politics. The articles you find here on our website are only a snippet of what you receive in The Daily Reckoning email edition. Click here now to sign up for FREE to see what you're missing. The post Saudi Arabia and Oil’s Future appeared first on Daily Reckoning. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| How the Blockchain and Gold Can Work Together Posted: 02 Feb 2016 08:51 AM PST A look into monetary history shows that people, when given freedom of choice, opted for precious metals as money. This doesn’t come as a surprise. Precious metals have the physical properties a medium must have to serve as legal tender: They are scarce, homogenous, durable, divisible, mintable, and transportable. They are held in high esteem and represent considerable value per unit of weight. Gold fulfills these requirements par excellence, and this is why it has always been peoples’ first choice in terms of money. Gold has proven its merits as money for millennia; it is the ultimate means of payment. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Epic Battle: Hedge Funds Versus China Posted: 02 Feb 2016 08:24 AM PST George Soros’ successful bet against the British pound back in 1992 remains one of financial history’s epic tales. The short version of the story begins with Britain linking its currency, the pound, to the German deutschmark via the European Exchange Rate Mechanism (ERM). But Britain’s inflation rate was higher than Germany’s, which created a growing mismatch between the currencies’ real value. In order to maintain the peg Britain raised interest rates and spent its foreign exchange reserves. But hedge funds, with Soros in the lead, sensed imminent failure and placed big bets against the pound. They were right: After some official bluster and shrill denials, Britain was in the end forced to withdraw from the ESM and devalue its currency, thus making fortunes for its hedge fund tormentors ($1 billion for Soros alone). Now fast forward to 2016. China has pegged its currency, the yuan, to the US dollar, but as the dollar rises — taking the yuan along with it — China’s economy is slowing down and many believe the only way to stop the slide is to devalue. Some high-profile hedge funds (including an older but apparently still bold Soros) now view China as another Great Britain and are trying for a replay by shorting the yuan.

China, of course, isn’t taking this lying down. Remember that its leaders are essentially central planners with at best a vague understanding of markets, who do not see how private individuals can or should get away with attacking their financial system. This, to them, is a declaration of war. They point out that they’ve got some weapons, including $3+ trillion of foreign exchange reserves and total control of the regulatory apparatus, and are not afraid to use them. The hedge funds, meanwhile, don’t seem too worried. Fascinating stuff! But what does it mean for the rest of us? Well, if China is forced to devalue the yuan by the 40% the hedge funds expect (and that fundamentals seem to require), China will have fired not just a bazooka but an ICBM in the currency war. For the world’s second biggest economy to devalue on that scale would send shock waves through Europe, Japan and the US. If, for instance, today’s strong dollar is already creating a US corporate earnings recession, imagine what a much stronger dollar would do. And the US is the least vulnerable of the three main victims. Europe is already on the edge of an economic/geopolitical/demographic abyss, and a spike in the euro might be the last straw. Japan, meanwhile, is trying to devalue its own currency and would either have to admit defeat and accept deflation forever or respond in kind, with massively-negative interest rates. To sum up, a big yuan devaluation might force the same decision on much of Asia, Europe and North America — all at once. So instead of a drawn-out, back-and-forth currency war over the next few years, the process would be compressed into just a few trading days. If, on the other hand, China succeeds in keeping a stable yuan/dollar peg, then some big and highly- leveraged hedge funds will lose a bet from which they may not be able to cover. Temporary stability in foreign exchange markets will have been bought at the cost of turmoil in the leveraged speculating/money center banking community. Whoever says finance isn’t fun just isn’t paying attention. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||