Gold World News Flash |

- The Billionaires vs. The Millionaires

- Gold Sales Go Hyperbolic: The Chart That Keeps Ben Bernanke Up At Night

- Lock Your Doors And Prepare To Defend Your Family

- Next Up For A “Recovering” Europe: A 30-50% Collapse In Wages In Spain, Italy And… France

- Gold & Silver Power Bars: Silver Set to EXPLODE On QE4

- The coming silver price eruption

- New Got Gold Report Video Released Sunday, December 2

- Next Up For A "Recovering" Europe: A 30-50% Collapse In Wages In Spain, Italy And... France

- Jim's Mailbox

- Sprott – We Will Go Public If They Don’t Send Us Our Silver

- Gold Price Manipulation Proven On The Intraday Charts

- Gold, Silver and Miners in Stage 1 Accumulation Mode

- Getting tough on gold imports won't work, two former Indian central bankers say

- 2013 Silver Price Forecast: Silver Will Perform Like Gold on Steroids

- The Weekend Vigilante

- David Morgan (The Eventual Rush to Silver)

- Goldman's Top Ten Market Themes For 2013

- Guest Post: Reality Has Consequences

- China all set to launch inter bank Gold market trade

- Alasdair Macleod: The coming silver price eruption

- King World News: Sprott fund will announce if its silver isn't delivered

- Anatomy Of The End Game, Part 2: Variations On The Problem

- Geithner: Raise U.S. debt limit to infinity

- Goldman Interviews Bain Capital On The Future Of... Outsourcing And Labor

- Mark J. Grant: It's Me Baby, With Your Wake-Up Call

- Collapse Is What Is Really Taking Place Around The World

- Currency Positioning and Technical Outlook

- Sprott - We Will Go Public If They Don’t Send Us Our Silver

| The Billionaires vs. The Millionaires Posted: 02 Dec 2012 11:54 PM PST by Jeff Nielson, Bullion Bulls Canada:

Why is Warren Buffett so adamant about the need for the Tax Man to start squeezing the millionaires? So that he (and his billionaire Oligarch-buddies) can continue to avoid paying his fair share of taxes. Buffett knows that everyone below the level of millionaire has already been squeezed dry. Buffett knows that the U.S. is drowning in debt, and (in real dollars) tax revenues have totally collapsed. So unless the U.S. government comes up with a new source of revenue (and fast), Oligarchs like Buffett are facing a grim future. Either their entire Paper Empire will disintegrate in a wave of domino debt-defaults, or the exponentially increasing money-printing needed to "fund" exponentially rising deficits will quickly trigger hyperinflation – also taking their Paper Empire to zero. Read More @ BullionBullsCanada.com

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold Sales Go Hyperbolic: The Chart That Keeps Ben Bernanke Up At Night Posted: 02 Dec 2012 11:14 PM PST from Zero Hedge:

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Lock Your Doors And Prepare To Defend Your Family Posted: 02 Dec 2012 10:10 PM PST from The Economic Collapse Blog:

Read More @ TheEconomicCollpaseBlog.com

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 02 Dec 2012 10:08 PM PST from Zero Hedge:

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold & Silver Power Bars: Silver Set to EXPLODE On QE4 Posted: 02 Dec 2012 09:30 PM PST from Silver Doctors:

Quantitative easing is positive for gold, and the effects on silver are even more powerful. This chart highlights the enormous gains that silver achieved during both QE1 and QE2. My focus is physical silver, because of concerns about the banking system and growing volatility.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The coming silver price eruption Posted: 02 Dec 2012 09:00 PM PST from Gold Money:

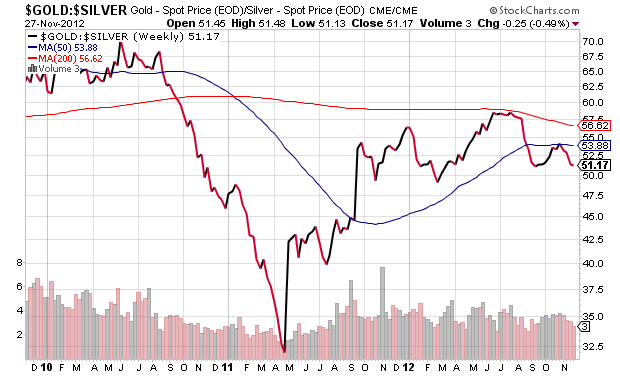

The chart is of Commercials' shorts and longs as of Tuesday November 27. The Commercial shorts (the red line) now stand at 99,317 contracts, or 496,585,000 ounces, about two thirds of 2011's worldwide mine production, and is the highest level of exposure since 2009. Because the longs have ticked up (the blue line), the net figure is not yet at record levels, but is only 9,212 contracts away from it.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New Got Gold Report Video Released Sunday, December 2 Posted: 02 Dec 2012 08:24 PM PST Vultures (Got Gold Report Subscribers) please log in to the Subscriber Pages and navigate to the Got Gold Report Video Section to view a new video offering released Sunday, December 2, 2012. (Please note: There is no appendix with this new video. )

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 02 Dec 2012 08:19 PM PST Several weeks ago Europe officially entered a double dip recession, and based on various secondary economic indicators, even Europe's primary economic powerhouse, Germany, is on the verge of negative economic growth. The reasons for Europe's woeful macroeconomic state are numerous, but boil down to two primary ones: i) massive external imbalances among Eurozone nations (think soaring peripheral debt) coupled with the inability to devalue the common currency as that would mean a failure and collapse of the joint currency union, ii) a desperate need for the periphery to regain price competitiveness (via wages and labor costs) with Germany in order to arrest and collapse an unemployment rate (general, but especially youth) that not even the most optimistic pundits dare claim is sustainable. Said otherwise, most European countries (including France) face a desperate need for external devaluation, which is impossible under a monetary union, leaving only internal devaluation as an option. This is where the much maligned concept of austerity comes in: from a macroeconomic perspective, austerity is not so much an exercise at moderating the pace of debt increase (as neither Spain nor Italy have reduced their rate of debt issuance), but of gradually becoming more price competitive with Germany: a key outcome that will be needed for the Eurozone to have any chance of survival, i.e., lowering sticky unemployment rates from levels that virtually assure social "disturbances" in the months and years ahead. And herein lies the rub: because while protests against "austerity" (which as we observed recently has still not been truly implemented in Europe, and certainly not in Portugal or Spain) are a daily event in most PIIGS nations, "you ain't seen nothing yet." The reason: to achieve the unavoidable macroeconomic rebalancing, and to collapse the spread between soaring labor costs in the periphery and those of Germany (see chart below), the bulk of European countries will need to see wages collapse by anywhere between 30% and 50% to compensate for the lack of state-level currency devaluation optionality. And yes, this includes France.

Goldman's Huw Pill explains the scary future facing peripheral European workers:

Which begs the question: how will the long-suffering workers of Greece, Spain, and Italy (and also France), who are confident they have gone to the 9th circle of hell in the past 4 years, react when they realize that none of the needed internal devaluation has actually taken place yet? In other words, what happens when Spanish wages tumble by another 30%, as they must if the EUR, and the Eurozone, is to survive? Alternatively, if there are no labor cost cuts, how many more years and months of 1%/month unemployment increases will the unemployed in the periphery suffer before it realizes that chronic 25%+ unemployment is here to stay, as is the European Depression. What is most sad is that the economic reality is that regardless of the "all clear" that central-bank-manipulated market indicators tell us, the European imbalances continue deteriorating at a rapid pace. And the paradox is that as long as market indicators aren't flashing red, no politician has the urge to enact the critical laws needed to fix the underlying problem, as that same fix will lead to an immediate end of said politician's career. Needless to say, not even Goldman thinks that kindly asking for Greek and Spanish workers to take another 30-50% pay cut is feasible and would lead to anything short of revolution (and the alternative: asking Germany to adopt a wage increase and watch German inflation surge is just as ludicrous):

So does this mean that despite all best efforts to the contrary, when one looks beyond the daily hollow rhetoric emanating from Brussels and focuses on the simple economics of it all, that the Eurozone is doomed? While our pessimistic opinion on the viability of the failed European project is well-known, not even Goldman can bring much words of encouragement:

It is worth pointing out that the ad hoc and very much informal (after all Merkel's reelection chances are much lower if the German people understand what is really happening in Europe) transfer union has worked so far primarily because it funded the relatively modest economy of Greece. Yet even ordinary Germans understand that the Bundesbank's TARGET2 claims are nothing more than Germany's implicit fiscal transfer mechanism to the rest of Europe (one which happens to benefit German exporters: i.e., a public to private transfer scheme), one which is soaring by tens of billions each month. To be sure all such indefinite ad hoc attempts to delay the day of "labor-cost equivalency"-reckoning using piecemeal and incomplete fiscal transfers from Germany to everyone else, will one day fail, when surging nationalist parties across Europe just say "nein" to ceding sovereignty to Germany which will eventually demand all Europe bow down to it in exchange for a full-blown fiscal union and Eurobond initiative in which Germany officially bears the cost of "temporary-to-permanent" Current Account imbalances, by shifting from TARGET2 to a wholesale German-funded fiscal union. This "unthinkable scenario" is quite thinkable by most, especially Europe, but in this case certainly Goldman:

The only good news to date, if one may call it so, is that Spain has already taken some modest steps to address its internal devaluation. However that former AAA-stalwart, and now bastion of resurgent socialism, France has not. And it is here that those who took offense to that recent edition of The Economist with the ticking time baguette cover should be paying attention.

And then there is that other wildcard: the UK. As CLSA's Chris Wood writes in his latest edition of Fear and Greed:

All of the above is correct: the true European fulcrum nations have now shifted from the PIIGS to France and the UK, but it will take some time for this to become evident. What is unclear is the question of timing. And with Europe hell bent on actually addressing the real underlying causes for its persistent recessionary state instead of merely attacking the symptoms (soaring yield spreads, plunging equity markets, diving EUR FX rate), one can be sure nothing will change as long as the ECB gives the impression that European imbalances are under control, courtesy of a bond purchase backstop, which sooner or later will be activated at which point this too threat will become reality, and like QEternity, will lose all potency. It is only then that Europe will have some hope of finally addressing that which is the true basis for its unsustainability: the internal imbalances which in the absence of currency adjustments can only be addressed through collapsing labor costs, and wages. Yet telling a continent, which in its desperation is hopeful and confident that the worst is behind it (as its lying politicians take every opportunity to note) that the most acute of standard of living collapses is yet to come, is borderline cruel and unusual. So we will just keep our mouths shut and let Europe's politicians bring this depressing message to their people. We are confident the reaction will be more than dignified.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 02 Dec 2012 08:16 PM PST Dear LT, This is for the community. Sometimes the truth hurts. I did some homework and remember distinctly listening briefly to this wannabe wunderkind at an investment conference. He has no clue about gold in my opinion, and worse yet he does and is sent to the gold community to confuse and dissuade would Continue reading Jim's Mailbox

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sprott – We Will Go Public If They Don’t Send Us Our Silver Posted: 02 Dec 2012 07:30 PM PST from KingWorldNews:

Eric King: "The financial system, the central planners are struggling to keep it together here, Eric. How do you see this playing out because the crises always accelerate in a phase like this? Sprott: "…Whether it's the promise of social security, Medicare, the promise of these gargantuan civil service pensions they have agreed to pay out, someone is going to find out sooner or later that what they think they are going to get, they're not going to get…" Sprott continues @ KingWorldNews.com

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold Price Manipulation Proven On The Intraday Charts Posted: 02 Dec 2012 07:00 PM PST from Gold Silver Worlds:

As a seasoned mathematician, Dimitri Speck is focused on what the charts are revealing. He looks both into intraday charts as well as seasonal charts, the former being one specific variant of the latter. Based on years of chart analysis, he could clearly pinpoint the manipulation in the gold market. In his book, he explores the subject of gold holdings of the central banks, in particular the Bundesbank. Interestingly, there is a link between all the different topics we just mentioned, which was the topic of our Q&A. Read More @ GoldSilverWorlds.com

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold, Silver and Miners in Stage 1 Accumulation Mode Posted: 02 Dec 2012 06:36 PM PST We don’t hear much about gold and silver anymore on the news. This time last year you could not go 5 minutes without a TV or radio station talking about them. Why is this? Simple really, precious metals have been building a Stage 1 Basing Pattern for the last 12 months. This boring sideways trading range is how the market gets most of those long holders out of an investment before it starts another move up. The saying is “If the market doesn’t shake you out, it will wait you out”.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Getting tough on gold imports won't work, two former Indian central bankers say Posted: 02 Dec 2012 06:00 PM PST by The Indian Express via, GATA:

The chairman of the Prime Minister's Economic Advisory Council, C. Rangarajan, said steps like banning gold imports would only push up its smuggling. Rangarajan, who served as RBI governor, said there are already indications that illegal shipments of the precious metal have gone up in the last three months after the hike in the excise duty. "That is an indication of how much gold is being smuggled in. I would say to some extent we should dissuade people from holding an asset that does not give a rate of return. However, you can't go beyond a particular point," Rangarajan said here at a function organised by the Indira Gandhi Institute of Development Research, an institution set up by the RBI.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2013 Silver Price Forecast: Silver Will Perform Like Gold on Steroids Posted: 02 Dec 2012 05:30 PM PST By Peter Krauth, Money Morning:

He confided to me that many of his clients had been asking for gold and gold-related investments over the past few years. I can't say that I was surprised. But what he told me next simply shocked me. "Gold's much too volatile, it's too risky", he said. "Sure it's up, but I try to discourage my clients from investing in it." It simply floored me that he thought gold was too volatile. Gold is only up 580% since it bottomed in 2001, without a single losing year to date.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 02 Dec 2012 04:00 PM PST by Jeff Berwick, Dollar Vigilante:

I had a rough start to my week as I was forced to go to the slave processing center (passport office) to ask permission from a group of people operating on behalf of a criminal enterprise if they would allow me to travel with my six year old daughter who had yet to be the unproud owner of a slave card (passport). We are planning a family and work vacation over Christmas and beyond through Central and Eastern Europe as well as parts of Africa and, of course, travel in the so-called free world is not allowed without permission. As we approached the passport office my wife did the same thing she does everytime we go through customs in any country we visit. She asked me to promise her I wouldn't fight with them. She said, "It's for our daughter, don't ruin this for her." I took a deep breath, as I always do after this request, then nodded my head and said, "I promise I won't fight with them."

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| David Morgan (The Eventual Rush to Silver) Posted: 02 Dec 2012 03:36 PM PST from silver investor.com:

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Goldman's Top Ten Market Themes For 2013 Posted: 02 Dec 2012 02:55 PM PST Whether you trust the squid and their thought process or believe in 'better the devil you know', Goldman's top thinkers - from Garzarelli to Himmelberg and from Stolper to Hatzius and Wilson - lay out the top ten global macro themes from their economic outlook that will dominate markets in 2013. Agree or disagree, one thing is for sure - these ten 'themes' will impact us all one way or another and for each theme, Goldman discusses the wider implications for markets, and the potential issues and options for investing around them. Aside from the ten key themes, they provide succinct macro outlooks for rates (steeper curves and seniorty shifts), FX (moderate USD weakness amid broad stability), equities (accelerating growth and risk reduction underpin a solid 2013), and credit ('search for yield' has less to find). Strawman - or investing bible - there is a little here every bull, bear, and arbitrageur...

Goldman's Top Ten Key Themes (and our annotated summary): 1. Global growth: A 'hump' to get over, then a clear road ahead - The biggest challenge from a markets perspective is that we see risks to growth concentrated early in the year, with Q1 likely to show a step-down in growth globally. Fiscal restraint plays a major role in that story: we expect a big increase early in 2013, but a significant fading on both sides of the Atlantic thereafter. 2. More unconventional easing in the G4 - The danger of positioning for a weaker JPY is that a convincing shift may require the BoJ to 'out-ease' a committed Fed, which we do not expect. 3. Termites eat away at the foundations of the 'search for yield' - Even though we expect the search for yield to continue, the risk-reward is falling. 4. Housing stabilisation and private-sector healing in the US - While we see continued healing in the household sector and ongoing gains in both housing starts (20% growth in 2013) and home prices (2%-3% growth in 2013), this may now already be priced in by markets. 5. Euro area a smaller driver of global risk, but still a source of tails - The best opportunities to take directional exposure to Europe have come either when the market believes that the system is close to collapse (as it did again in May) or when there is confidence that the key risks have been resolved. Neither is true right now. 6. Continued divergence between core and periphery in the Euro area - The divergence in growth between the Euro area core (Germany in particular) and the periphery (Spain in particular) is set to continue. Periphery weakness is already well-known, but the potential for German overheating is a more distinctive theme. 7. EM growth pick-up revisits capacity constraints - if EM equities outperform DM in an absolute sense, the outperformance is unlikely to be enough given the higher risk or variance in outcomes. 8. EM differentiation continues - The 'orthodoxy' of the central bank reaction function to inflation is also likely to vary, and so the risk in some places is that even with building inflationary pressure, policy does not necessarily tighten. 9. Commodity constraint to loosen in the medium term - we expect oil markets to return to a more structurally stable position, where the ability to bring on new supply in the $80-90/bbl range is rapidly increasing. 10. Stable China growth, but not like the old days - iron ore demand is likely to remain soft as core building demand falls, and that copper will receive a boost from the completion of new buildings in the next 6-9 months, but is likely to peak thereafter.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Guest Post: Reality Has Consequences Posted: 02 Dec 2012 12:30 PM PST Originally posted at Monty Pelerin's World blog, The world no longer makes sense to most people over forty years of age. Much of what we thought was true is now denied. What to us is obviously false (or at least always was) is now accepted as being true. Here are examples from Frick at Bias Breakdown that show obvious contradictions between popular belief and what we hold as reality:

Fantasies like these might are satisfying to many, but they are ultimately destructive. Truth cannot be changed by repeating falsehoods. Nor can it be altered by more people believing untruths. But, when these fantasizers overwhelm society with their false beliefs, society will no longer function. Society cannot invent its own truth based on convenience, prejudice or popularity. Truth, not manufactured myth, is key to survival. Societies which deviate from it, don't survive. As Ayn Rand stated:

The avoidance of reality has overtaken our society. The consequences of doing so have been building for decades and will soon overwhelm us. On our current path, much of what we knew and cared about will be destroyed.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| China all set to launch inter bank Gold market trade Posted: 02 Dec 2012 11:30 AM PST by Sajith Kumar, Bullion Street:

The move will enable traders to swap bullion in larger amounts and heighten the appeal of the metal as an alternative investment class. Shanghai Gold Exchange said trades will be cleared and delivered under the auspices of the China Foreign Exchange Trading System, a subsidiary of China's central bank.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Alasdair Macleod: The coming silver price eruption Posted: 02 Dec 2012 10:29 AM PST 12:22p ET Sunday, December 2, 2012 Dear Friend of GATA and Gold (and Silver): GoldMoney research director Alasdair Macleod reports today that the big commercial shorts in silver are approaching record levels again even as public demand seems to be at merely normal levels. Macleod writes: "On this evidence, the bullion banks short in the silver market are potentially in serious trouble, unless somewhere there is a pot of physical silver they can dip into. There isn't, if we assume that iShares Silver Trust's 315 million ounces are unavailable. There is no other identifiable source of silver, other perhaps than some producer supply, and there is anecdotal evidence that on every dip, cash silver migrates from West to East, confirmed by silver being constantly in backwardation. The odds now favor a substantial bear squeeze. And as the managed funds that lost money on their shorts in June-July sniff sweet revenge, this could rapidly escalate." Macleod's commentary is headlined "The Coming Silver Price Eruption" and it's posted at GoldMoney's Internet site here: http://www.goldmoney.com/gold-research/alasdair-macleod/the-coming-silve... CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT Opinion Around the World Is Changing When Deutschebank calls gold "good money" and paper "bad money". ... http://www.gata.org/node/11765 When the president of the German central bank, the Bundesbank, pays tribute to gold as "a timeless classic". ... http://www.forbes.com/sites/ralphbenko/2012/09/24/signs-of-the-gold-stan... When a leading member of the policy committee of the People's Bank of China calls the gold standard "an excellent monetary system". ... http://www.forbes.com/sites/ralphbenko/2012/10/01/signs-of-the-gold-stan... When a CNN reporter writes in The China Post that the "gold commission" plank in the 2012 Republican platform will "reverberate around the world". ... http://www.thegoldstandardnow.org/key-blogs/1563-china-post-the-gop-gold... When the Subcommittee on Domestic Monetary Policy of the U.S. House of Representatives twice called on economist, historian, and gold standard advocate Lewis E. Lehrman to testify. ... World opinion is changing in favor of gold. How can you learn why and what it will mean to you? Read the newly updated and expanded edition of Lehrman's book, "The True Gold Standard." Financial journalist James Grant says of "The True Gold Standard": "If you have ever wondered how the world can get from here to there -- from the chaos of depreciating paper to a convertible currency worthy of our children and our grandchildren -- wonder no more. The answer, brilliantly expounded, is between these covers. America has long needed a modern Alexander Hamilton. In Lewis E. Lehrman she has finally found him." To buy a copy of "The True Gold Standard," please visit: http://www.thegoldstandardnow.com/publications/the-true-gold-standard Join GATA here: Vancouver Resource Investment Conference * * * Support GATA by purchasing DVDs of our London conference in August 2011 or our Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: ADVERTISEMENT Fred Goldstein and Tim Murphy open All Pro Gold Longtime GATA supporters Fred Goldstein and Tim Murphy have brought their many years of experience in the precious metals and numismatic coins to All Pro Gold as metals brokers who specialize in the delivery of gold and silver bullion bars and coins as well as numismatic gold and silver coins. Fred and Tim follow these markets closely and are assisted by a team of consultants in monitoring market trends. All Pro Gold offers GATA supporters competitive pricing on all bullion products and welcomes inquiries. Tim can be reached at 602-299-2585 and Tim@allprogold.com, Fred at 602-799-8378 and Fred@allprogold.com. Ask about their ratio strategy and the relationship of generic $20 dollar gold pieces to 1-ounce gold bullion coins. Visit their Internet site at http://www.allprogold.com/.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| King World News: Sprott fund will announce if its silver isn't delivered Posted: 02 Dec 2012 09:55 AM PST 11:55a ET Sunday, December 2, 2012 Dear Friend of GATA and Gold: In the third excerpt of his recent interview with King World News, Sprott Asset Management CEO Eric Sprott says his company will make an announcement if there is any failure to deliver the silver recently purchased by the Sprott silver fund: http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2012/12/2_Sp... Full audio of the interview is 21 minutes long and can be heard at the King World News Internet site here: http://www.kingworldnews.com/kingworldnews/Broadcast/Entries/2012/12/2_E... CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT Prophecy Platinum Intercepts Best Pt+Pd+Au Grades Yet Company Press Release VANCOUVER, British Columbia -- Prophecy Platinum Corp. (TSX-V: NKL, OTC-QX: PNIKF, Frankfurt: P94P) announces more results of its 2012 drill program on the company's fully-owned Wellgreen platinum group metals, nickel, and copper project in southwestern Yukon Territory, Canada. Four surface holes and four underground holes all intercepted significant mineralized widths, ranging from 28.5 meters (WS12-201) and up to 459.5 metres (WS12-193). Highlights include WU12-540, which returned 8.9 metres of 5.36 grams per tonne platinum, palladium, and gold; 1.73 percent copper; and 1.01 percent nickel within 304.5 meters of 0.66 g/t platinum-palladium-gold, 0.20 percent copper, and 0.27 percent nickel. The surface drill program started in June and has completed 16 holes (assays pending for 12 holes) with two rigs now on site. The surface program continues to progress at a steady pace. Prophecy Chairman John Lee commented: "Wellgreen is a very large nickel, copper, and platinum group metals project with near-surface high-grade zones. High-grade intercepts will be incorporated into resource modeling and mine planning in the pre-feasibility study. We expect further positive drill results from Wellgreen shortly." Wellgreen features a low 2.59-to-1 strip ratio, is situated at an altitude of 1,300 meters, and is only 15 kilometers from the two-lane paved Alaska Highway. Those factors significantly minimize the project's indirect costs. For the complete company statement with full tabulation of the drilling results, please visit: http://prophecyplat.com/news_2012_sep11_prophecy_platinum_drill_results.... Join GATA here: Vancouver Resource Investment Conference * * * Support GATA by purchasing DVDs of our London conference in August 2011 or our Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: ADVERTISEMENT GoldMoney adds Toronto vaulting option In addition to its precious metals storage facilities in Hong Kong, Switzerland, and the United Kingdom, GoldMoney customers now can store their gold and silver in a high-security vault operated by Brink's in Toronto, Ontario, Canada. GoldMoney also has recently partnered with Rhenus Freight Logistics to offer another gold storage option in Switzerland. The Rhenus vault is in the secured zone of Zurich Airport and offers customers superb security as well as the ability to inspect their gold. Storage at the new vaults in Canada and Switzerland is available at GoldMoney's lowest fees. Customers can select their storage location when placing their buy order. GoldMoney customers can take delivery of any number of gold, silver, platinum, and palladium bars from any GoldMoney vault, as well as personally collect their bars stored in the Hong Kong, Switzerland, and U.K. vaults. It's easy to open an account, add funds, and liquidate your investment. For more information, visit: http://www.goldmoney.com/?gmrefcode=gata

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Anatomy Of The End Game, Part 2: Variations On The Problem Posted: 02 Dec 2012 08:38 AM PST Authored by Martin Sibileau of A View From The Trenches blog,

The intention today was to do a revision of what I had expected in 2012, what happened and what I think will happen. However, we may have to put this aside one more time, given the feedback received on the last post, titled "Anatomy of the End Game". I seem to have been misinterpreted and to clarify this very important topic, I present a second part to make absolutely clear that:

The End Game in a world without shadow banking There are continuous attempts at further regulating money market funds and central counterparties (i.e. clearinghouses), based on the belief that their operations entail risk of a systemic nature. But the systemic nature of the risk is simply due to the leverage built upon the collateral that these players use to provide funding. There is nothing particularly intrinsic to either the players, the markets that use that collateral or the collateral (i.e. sovereign debt, mortgages, etc.) itself, to make them "systemic". To coerce these players to increase their capitalization or to prevent them from freely disposing of their liquidity as risk varies only increases costs and volatility. Let's assume the extreme case where the "shadow banking" sector disappears and banks become the sole providers of funding in the repo market. The figure below describes the situation. In stage 1, we can see the consolidated balance sheets of the financial institutions, traders, and non-financial institutions (private sector). Traders have US Treasuries as assets, which in stage 2, they sell to source cash. This cash is expressed as deposits (in stage 2), which are liability of the financial institutions. Deposits then, are backed by US Treasuries. When these are repudiated (our main assumption) the sustainability of the financial institutions is challenged, precisely at the same time that traders may be suffering a short squeeze on short commodities positions and margins are called. This short squeeze would also affect the commodities and futures markets' clearinghouses (not shown in the figure). From stage 3, it is easy to see that depositors (non-financial institutions) who are not part of the aggregate "traders" class are the ones who are most at risk. The faith in the US dollar system is lost and a run on the banks is triggered. We must clarify that the US dollar zone/system is not bound by geographical or jurisdictional borders. A Hong Kong or Brazil based bank that relied on US dollar funding to generate relevant net interest income would be equally affected by the liquidity squeeze, as so many European banks learned in 2008 and 2011.

Under this scenario, and unlike the case where the shadow banking system funds the repo market, the Fed would not have the luxury of choosing whether or not to intervene. It would simply be their duty to do so, and they may believe that they have the option to purchase the US Treasuries from the banks with or without sterilization. But in the end, it would not matter…sadly. Let's go through the process: a) The Fed purchases US treasuries without sterilizationThis is the easiest option to understand. As the figure shows below, the Fed purchases US Treasuries from the financial institutions and their reserves grow. As the whole context in which this would occur is not positive for economic growth, to say the least, and the private sector delevers: Loans outstanding, on a net basis, decrease. Deposits decrease and the non-financial private sector increases cash on hand. The equity of the financial sector, naturally, suffers. This cash on hand will keep rising as long as the US debt remains repudiated and US Treasuries need to be monetized by the Fed. Eventually, in the absence of alternative investments (as in the current context, with zero to negative interest rates), the cash is simply spent on consumption. In an environment of financial repression, where companies use whatever liquidity preferably to distribute back to owners via share buybacks or dividends (as we expected back in March), the higher consumption facing lower production ends up driving prices higher.

b) The Fed purchases US treasuries with sterilizationIf the Fed decided to sterilize the purchase of US Treasuries being repudiated, the market would immediately begin to discriminate between those banks who get the benefit of carrying Fed debt and those who don't. This is similar to what we see in the Eurozone: Deposits flee banks which are seen at risk of being caught on the wrong side of the tracks, should a break up of the Euro zone occur, to banks in the core of the Euro zone (i.e. banks with continuous access to liquidity lines of the European Central Bank). This arbitrage (why carry cash, which pays no interest, rather than Fed debt?) would drive all banks to buy distressed US Treasuries to make a difference exchanging them for Fed debt. This would be a very perverse process, because banks would drive deposit rates higher to maximize the sourcing of US Treasuries. At this point, I am aware you may be confused: It doesn't seem to make sense to first assume that Treasuries are being repudiated and later say that banks seek to raise deposits to purchase them. But this makes perfect sense, when we realize that in this context, the market for US Treasuries would be simply broken, segmented. Only banks with the privilege of access to the Fed's window would be interested in US Treasuries, because only they would have access to the interest-paying debt of the Fed. The US Treasuries, effectively, would be marked to model by the Fed and as the private sector gets crowded out and deposits drop, the need for liquidity and profitability of the financial institutions would demand that higher interest be paid by the Fed on its debt. You may ask why should the Fed be forced to pay higher rates, when the private sector would seem to be out of investment alternatives. First, we must remember that in this context, commodity prices would be rising and the nominal rate of return in gold would be a benchmark, just like simply holding US dollars in the '80s was a benchmark shaping inflation expectations in Latin America. Secondly, the Fed would be forced to pay higher rates to keep deposits from dropping in a context of decreasing trust in the solvency of the banking system. Those living today in the periphery of the Euro zone understand this. Why should deposits not drop? Because if they do, more currency will be circulating and available to buy real assets (i.e. gold) and the outstanding stocks of US Treasuries being repudiated would not be cleared from the market into the balance sheet of the Fed. Their increasing yield (as the price drops) would be a price signal to the market that the Fed would have every reason to kill.

However, if the value of the US Treasuries falls and the interest the Fed has to pay to sterilize their purchase rises, the Fed will face a net interest loss. The Fed may chose to keep accumulating these losses or may also decide to simply convert its debt in legal tender, to end the arbitrage between currency (not paying interest) and its interest-paying debt. In the first case, we end up with a plain monetization of US Treasuries, which we just analyzed above. The second case (enforcing Fed debt as legal tender) would truly mark the end of the game in terms that would make historians of the 21st century would devote entire volumes… Why fiscal austerity would be irrelevant without a surplusA logical outcome, which I think is clear from the two scenarios above, is that no matter how far the spending cuts go, the only way to compensate for the monetization of EXISTING INVENTORY of US Treasuries, is to reach a fiscal SURPLUS. Being only frugal won't cut it! In order to avoid being dragged to double digit inflation, there will have to be a fiscal surplus to offset the quasi fiscal deficit of the Fed. However, the implementation of austerity measures (i.e. spending cuts), will necessarily lead to a decrease in activity which would only be temporary if the same are accompanied by a widespread liberalization of markets. It is possible but unlikely, for reasons beyond the scope of this post. All sorts of negative feedback mechanisms could be triggered in this situation, only enhancing the repudiation of the US sovereign debt and the resolve of the Fed to monetize it (For instance, the so called Olivera-Tanzi effect postulates that as inflation rises, access to working capital is restricted and firms delay their tax payments, to get them devalued by inflation. The government therefore receives depreciated tax revenue while its operating costs increase, facing deficits that need to be further monetized, thereby fueling even higher inflation). In Argentina, this negative feedback was always resolved with the plain confiscation of citizens' assets: Savings accounts in 1989, chequing accounts in 2001, pension funds in 2008, etc. (I can't stress enough how important it is for anyone in the financial markets today to study the monetary developments in Argentina between 1972 and 1991) Policy makers look the wrong wayThe natural reaction from policy makers, so far, has not surprised me. Rather than addressing the source of the problem, they have and continue to attack the symptoms. The problem, simply, is that governments have coerced financial institutions and pension plans to hold sovereign debt at a zero risk-weight, assuming it is risk-free. This problem truly brings western civilization back to the time of Plato, when there was nothing "…worthy to be called knowledge that could be derived from the senses…" and when "…the only real knowledge had to do with concepts…". In the view of policy makers, the statement "the probability of US sovereign default is zero" is genuine knowledge, but a statement such as "The US government needs to issue about $100 billion per month to finance its fiscal deficit" is so full of ambiguity and uncertainty that it cannot find a place in their universe of truths…(Note: I am paraphrasing Bertrand Russell here. I am certainly not erudite)…and just like since the beginning of the 17th century almost every serious intellectual advance had to begin with an attack on some Aristotelian doctrine, I fear that in the 21st century, we too will have to begin attacking anything supporting the belief that the issuer of the world's reserve currency cannot default, if we are ever to free ourselves from this sad state of affairs. The following paragraph, from a speech by Paul Tucker (currently Deputy Governor at the Bank of England) says it all: "…Two strategies come to mind which I am airing for debate. The first would be 'recapitalizing' the CCP (i.e. central clearing counterparty) so that it can carry on. The second would be to aim to bring off a more or less smooth unwinding of the CCP's book of transactions…" P. Tucker, Bank of England, "Clearing houses as system risk managers", June 2011 Policy makers then believe in recapitalization and coercive smooth unwinds. With regards to recapitalization, I will just say that we are not facing a "stock", but a "flow" problem. US Treasuries would be repudiated because of fiscal deficits, which are flows. No matter how capitalized a clearinghouse is, once the repudiation starts, the break-up of the repo market and the short squeeze would unfold and develop. Whether there is or not a capital buffer is irrelevant to the problem. In fact, in my view, it would be better that there wasn't: Why would you want to add more resources to a lost cause? With regards to smooth unwinds, I think it is obvious by now that the unwind of a levered position cannot be anything but violent, like any other lie that is exposed by truth. Establishing restrictions to delay the unmasking would only make the unwinds even more violent and self-fulfilling. But these considerations, again, are foreign the metaphysics of policy making in the 21st century.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Geithner: Raise U.S. debt limit to infinity Posted: 02 Dec 2012 08:00 AM PST by Ethan A. Huff, Natural News:

During a recent interview on Bloomberg TV, Geithner told Political Capital's Al Hunt that the Congressionally-established debt ceiling, which was specifically designed to establish reasonable limits on the amount of money the federal government can borrow, should be completely abolished. Even though Congress is the only entity that can make such a decision, Geithner expressed his belief that the limit be scrapped to avoid its being used as "a tool for political advantage."

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Goldman Interviews Bain Capital On The Future Of... Outsourcing And Labor Posted: 02 Dec 2012 07:41 AM PST After this year's presidential campaign, private equity and certainly Bain Capital, will likely be the last entity that those pandering to populist agendas will go to advice over the future of the business cycle in broad terms, and the future of US labor, most certainly including outsourcing, in narrow terms. And Goldman - that staunch defender of the superiority of capital over labor - will hardly be confused as ever taking the role of workers in any discussion. Which is why we read the following interview by Goldman's Hugo Scott-Gall with Bain Capital partners Michael Garstka and Alan Bird on such topics as corporate restructurings and the future of outsourcing with great interest, as it is very much unlikely that any of the conventional media sources would carry it. And while one may have ideological biases in whatever direction, the truth as presented previously, is that US private equity is a massive "behind the scenes" juggernaut, whose portfolio holding companies account for a whopping 8% of US GDP, and is directly and indirectly responsible for tens of millions of currently employed US workers! At the end of the day, it may well be that what private equity firms such as Bain think about the future of US labor prospects is the most important thing that matters for the future of the so very critical US unemployment rate. Which is why we present, for your reading pleasure, the somewhat unorthodox interview below... From Goldman's Hugo Scott-Gall Michael Garstka is a Partner at Bain & Company in London, where he is a senior member of the firm's global Telecoms, Media and Technology Practice and its Energy and Utility Practice. He has previously worked across Asia for a decade, being based out of the firm's Tokyo and Singapore offices. He has worked with senior executives and shareholders on strategy-driven corporate transformations and turnarounds. Alan Bird is a Partner at Bain & Company in London and Johannesburg and the lead partner for the UK's Organisation Practice. He also heads the firm's global Mining Practice and has over 20 years consulting experience across a wide range of industries and geographies. His particular focus has been on growth strategy, broad-scale transformation and organisation effectiveness, with a special interest in performance and effective leadership supply. Hugo Scott-Gall: Do you think the time is ripe for restructuring? Michael Garstka: Yes. What we are seeing in our work with clients is an increased recognition of the need for and appetite for major, structural change in their businesses, be that strategically or operationally in nature. This is driven by an number of factors impacting companies simultaneously. Some of these factors are very cyclical in nature, and the macroeconomic environment, particularly here in Europe, continues to be challenging. But there are more significant, longer-term secular trends that are driving major disruptions across multiple sectors, and these are being amplified by the cyclical environment. These include technology evolution, regulatory and government intervention, demographic and geopolitical changes. For example, a government policy agenda of driving lower carbon emissions in many markets is not just leading to major investment shifts in generation to renewables from fossil fuels, but is also driving significant investments in smart meters, "connected-homes" technologies, smart grids, and even loft and wall insulation. Multi-decade long trends such globalisation and demographics are still opening up lower-cost labour pools in different parts of the world, impacting labour-intensive industries, their location and competitive dynamics. So while the cyclical trends are increasingly forcing change in the short term, it's the undercurrent of these longer-term secular trends that is going to impact value creation and value destruction. Take the media sector for example. The ongoing shift towards digitisation is significantly impacting the traditional print media. Newsweek, the 80-year old flagship media brand in the US announced last month that it would stop producing its print edition and instead move towards a wholly digital platform. Yes, revenues and earnings were aggravated by the cyclical downturn in print advertising, but this was less significant that the impact on print media profit pools of online advertising. This trend is hitting magazines, newspapers and yellow page companies. In consumer electronics, the Apple-led shift to a software platform led mode vs. a hardware-centric mode within handsets has completely changed the market dynamics in favour of Apple and Samsung (which has enthusiastically embraced the Google Android platform) and away from Nokia, which just 4-5 years ago enjoyed disproportionate share of market and profit pool. In mobile telecom equipment, technology shifts such as IP, a shift to common global standards vs. national standards, and the entry of Chinabased low cost players ZTE and Huawei have come at the same time. The cyclical softness in telco capital spending has been challenging, but is not the major story. Rather, this has exacerbated the changes in the industry. Today, at one end of market we have Ericsson that continues to be successful, and at the other end we have insurgent competitors like Huawei which are leveraging their lower cost structure and taking share from the bottom, while companies in the middle such as Nokia Siemens Networks and Alcatel-Lucent are facing pressure on both margins and operating cash flow. So, it's usually secular trends prodded by cyclical factors that drive restructuring, and this accounts for a lot of what we're seeing right now. Hugo Scott-Gall: And what about in the resources sector? Alan Bird: While the underlying trend in commodities is for future growth, the headwinds encountered over the last 12 months as demand has slowed in China and elsewhere have accentuated investor demands for immediate cash returns - patience has run out for "jam tomorrow" promises. This has driven a significant emphasis on restructuring, broadly on three levels. First, companies are reshaping their portfolios (witness Gold Fields' announcement this week of its intent to unbundle its legacy South African assets), rationalising their asset mix and getting rid of some non-core assets. This has led to the entry of some unusual and new players, including private equity firms, into the industry. For example, BHPBilliton recently sold its Canadian diamond mine (Ekati) to Harry Winston Jewellers, which also has share in a diamond mine with Rio in Canada. Second, mining companies are reviewing their growth projects on a cash generation and quality basis. A good example of this is BHPBilliton's shelving of its US$40 bn Olympic Dam expansion project in Australia. Third, increased price volatility is driving a shift in the profit pools in some sectors (for example, thermal coal) away from asset owners to traders. Traditional miners in these sectors need to rethink their business models. Hugo Scott-Gall: How hard is it for corporates to restructure today, particularly in Europe? Michael Garstka: There is a clear difference in the pace at which you can drive change, depending on the country in which you are based. It's not that you can't drive change in less liberal labour market economies as in Mediterranean Europe, it's just that you have to follow a different route. The legal, trade union and government engagement is different, as is the out of pocket cost. So what takes a couple of months in the UK or some of the Northern European countries, could take more than six months cost you more in the South. Not being able to restructure quickly is a constraint, but not should not prevent you from taking these tough choices. Overall, we don't see it getting harder. In fact, the imperative to restructure is getting stronger, but what we are seeing in our work with clients is a shift in the way companies think about what they need to do to drive growth. There is a strong emphasis on the growth portfolio, not just in the BRICs, but increasingly in the next tier of Africa, Mexico, Indonesia, especially among the consumer products companies. Instead of trying to increase their presence more broadly, our clients are increasingly allocating capital to a limited number of attractive growth markets. In order to win there, they also want to grow domestic talent rather than relying on expat talent pools. And so, while it isn't significantly harder nor easier for companies to restructure now, the type of measures they are taking is changing quite significantly. Hugo Scott-Gall: How do you restructure a company that's facing a structural decline in its business? Michael Garstka: You first need clarity on the path forward and then you need the confidence, and frankly the courage, to make uncomfortable decisions. Many companies built sets of assets, often through acquisitions during the boom years, but have made only limited efforts to rationalise their portfolio of businesses, product lines, manufacturing facilities or suppliers. When you are facing these secular trends, however, you need to approach this in a quite dispassionate way, and accept that there are parts of the business that are not going to earn desired returns or even survive. Of course, there maybe exit barriers or high costs in some cases, like large liabilities, labour contracts and pension obligations. But it is increasingly dawning on executives that they need to make these decisions sooner rather than later, because they are facing an extended period of slow or no growth, which will only make it tougher to get out of these businesses. At least in Europe, there is no "V-shaped" recovery that is going to let them off the hook. Hugo Scott-Gall: Does that mean that there's a reasonable amount of restructuring that has been put off and therefore still needs to happen? Michael Garstka: Broadly, I think that's correct. Most executives don't wake up and come into the office wanting to make a decision to exit a product line or a factory that they've operated for decades. Few executives enjoy having to take 20% plus out of their cost structure, or wants to fundamentally change the way they've always manufactured their product or approached the market. These decisions are hard, and successfully executing on them is even harder. So executives often convince themselves that their market conditions are temporary and there will be a bounce back, and hence there is a tendency to delay some of these tough decisions. But as it becomes increasingly clear that we are either having a series of very short cycles or an extended down cycle, the secular issues tend to become more important. And in a number of sectors, we will see restructuring that has been delayed come back under focus. Alan Bird: The shorter term, cyclical actions typically get more attention at first, because they are immediate and more easily addressed. They broadly relate to multi-industry type solutions like supply chain rationalisation, cutting administration expenses, realigning R&D portfolios etc. Then there are industry-specific actions which many companies have been pursuing, such as ringfencing toxic assets in the banking sector. The more challenging actions for companies to take are those industry breakout or industry reshaping strategies which are unique to a specific company in a specific industry. This is typically the heartland for our consulting services and we are increasingly seeing our clients move towards seeking these breakout restructuring opportunities. Michael Garstka: So to answer your question, more restructuring is coming and it will be greater in some sectors versus others. But the key question that companies will focus on will be how to position themselves to take advantage of the underlying secular trends we have discussed. Not all companies will make those decisions and not all of those that do will s successfully execute such more radical restructuring. But those that do will come out in fundamentally stronger positions five to ten years down the line. Hugo Scott-Gall: How can we identify companies that can execute restructuring well? Michael Garstka: It's important to pay attention to what management is actually saying when they meet with investors, analysts and the press. If the conversation is focused only on things like supply chain, R&D levels and admin costs like Alan mentioned in the previous answer, it is worth pausing for a moment. That's appropriate for a company in an industry isn't facing any secular changes, and their primary issue is the macroeconomic headwinds. But if you realise that there is some fundamental technological, regulatory or demographic change which management is not considering, then that is not enough. In these circumstances, when the focus is not on a 3-5 year horizon, but rather on what can be done for the next couple of quarters, that is watch out. On the other hand, companies that are considering taking actions that would really take their company forward or those that are trying to understand how they are performing versus their direct competitors irrespective of being in a boom or a doom time, are the ones that can lead the industry in terms of costs and create genuine value. Typically it's the number one or number two company in the industry, but there are other sources of leadership economics too, whether it's through superior customer loyalty,platform control or intellectual property. Hugo Scott-Gall: Given rising wages in Asia and associated transport costs and IP theft risks, do you think there's a strong enough argument for some types of manufacturing to come back to the West? Alan Bird: There are two competing trends here. The first is improving the quality and cost-effectiveness of products and services from these 'low-cost' locations. I have had the privilege recently of visiting some of these outsourcing locations in places such as India and the degree of sophistication they now provide is simply amazing. The second trend is for developed markets to reassess their supply chains to enable greater agility by returning to source more locally and in the process becoming more green. On balance, the overall trend is still towards outsourcing to lower-cost countries, but it will be interesting to see how this play out. Michael Garstka: And it goes beyond just labour arbitrage. Now it is increasingly about a shift in channels. The activities handled by call centres that initially moved to low-cost locations for cheaper employee costs are now moving online. An increasing number of customer segments now prefer shopping, paying their bills, and managing "self service" online. Especially with smartphones penetration, which is providing customers internet access everywhere, the shift to online platforms is very real and happening quite quickly. This is fundamentally driving companies' unit costs down while also improving customer service. We are working with clients on this major transition in the telecoms, financial services, The most forward looking companies are looking at the total cost of their value chains, which includes the issues of security and stability as opposed to just the traditional elements of cost. For example, if a company had all of its memory chips being made in one province of Taiwan, an earthquake could disrupt production significantly. Intellectual property rights security is another concern that a number of companies have raised, particularly in some of the Asian markets. Historically, the more labour intensive functions are the ones that have moved to offshore locations , but another major issue today, especially for Europe, is the relative cost of energy. Companies in energy-intensive industries are increasingly concerned about the emerging gap in relative energy prices across geographies, and particularly with the dramatic fall in energy costs in the US resulting the shale gas boom. Labour cost arbitrage was the story of the last ten years, but "energy cost arbitrage" could be a major differentiator of national competitiveness going forward. Hugo Scott-Gall: Is a private equity-owned company easier to restructure than a publicly listed one? Alan Bird: I don't really see a major difference between the two. It really is down to the calibre of the management team and the confidence and the decisiveness of action. I don't think being publicly listed creates a massive impediment in terms of restructuring.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mark J. Grant: It's Me Baby, With Your Wake-Up Call Posted: 02 Dec 2012 07:00 AM PST Via Mark J. Grant, author of Out of the Box, Alarm clock starts ringing

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Collapse Is What Is Really Taking Place Around The World Posted: 02 Dec 2012 07:00 AM PST from KingWorldNews:

Fasten your seat belts, here is what Egon von Greyerz, founder of Matterhorn Asset Management in Switzerland, had this to say: "Eric, I'm looking around the world and what is happening in France is quite amazing. We all know Hollande is in charge and he is now threatening French steel producer ArcelorMittal. Business is weak and they are looking to lay off some employees." Egon von Greyerz continues @ KingWorldNews.com

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Currency Positioning and Technical Outlook Posted: 02 Dec 2012 06:44 AM PST

Our assessment of macro fundamentals leave us inclined to favor the dollar on a medium term basis. However, we continue (see here and here) to recognize that near-term technical considerations favor the major foreign currencies, but the yen.

It seems many participants lack conviction about the price action. As our review of the Commitment of Traders shows, outside of the euro and yen, positioning by the momentum players and trend followers in the futures market was little changed. Moreover' the euro's rise appears to be driven by short-covering rather than the establishment of new longs.

The yen seems to be the exception. Here many participants believe a major turn has taken place. We are less convinced and are sensitive to the distinction between declaratory policy (what officials say) and operational policy (what official do). With the Japanese election still two weeks away, we recognize there is more opportunity to sell the yen on the "rumor" and later "buy the fact".

Increasingly, in the coming weeks, we anticipate US developments to eclipse events elsewhere. First, the recent economic data points to a marked slowing in the US economy here in Q4, with growth tracking about half of the 2.7% revised pace in Q3. As part of this, we see high risks of a poor employment report at the end of the week. This will encourage expectations of the second important event: the Federal Reserve will likely expand QE3+ by rolling into it the long-term purchases that have been conducted under Operation Twist. This will essentially double the Fed's monthly purchases to $85 bln a month.

This brings us to the third important development and that is, of course, the fiscal cliff. It strikes us as unreasonable to expect any deal until the very last minute, and even then, political considerations and brinkmanship tactics, seem to suggest that a resolution may be easier after the fact than preventative. Perhaps a bit counter-intuitively, the knee-jerk market reaction to news of the lack of progress has been to buy the dollar, perhaps on safe haven ideas. Yet that reaction function seems to have reached the point of diminishing returns with such reactions becoming shorter and shallower.

Euro: New mutli-week highs were recorded before the weekend. The $1.3000-30 objective cited in this space last week was met. Look for a move above here in the coming days and we suggest a $1.3140 target. A break of $1.2935-50 would call this constructive view into question.

Separately, we note that implied volatility has picked up from very depressed levels in recent days. It finished last week above its 20-day average for the first time in almost three months. The 60-day correlation between 3-month implied volatility and the euro has turned positive in recent days after being inversely correlated since early September. The correlation was positive in the Jan-Feb period, but turned inverse from late-Feb through late-July. It then remained positive until early September.

It appears that the euro's advance is being met with call buying (either for protection of underlying shorts or as a way to benefit from a euro advance rather than getting caught up in the vagaries of spot action.). The risk-reversals (euro calls relative to puts equidistant from the forward strike) now show the smallest discount for euro calls (smallest premium of euro puts) since the Greek crisis first surfaced in late 2009. Anticipate additional near-term euro gains.

Yen: The main weight on the yen continues to come from anticipation that Japan is on the precipice of a more aggressive policy that purposefully seeks to debase the currency. There is plenty of time before the December 16 election for Abe's campaign rhetoric to continue to encourage new yen sales. The price action seems to reflect good yen selling into even modest bounces. Dollar support identified in this space last week in the JPY81.60-80 area was successfully tested. The dollar's gains ahead of the weekend, recording new highs for the week, appear to have begun a new leg higher. We are monitoring a trend line drawn off the 2011 high near JPY85.50 and this year's high near JPY84. It comes in just above JPY83 next week.Anticipate further yen weakness.

Sterling: Given the narrowness of the recent ranges, we are choosing not to emphasize the outside day recorded on Friday when sterling trading on both sides of Thursday's range. In the past week, it was confined to a one cent range .The initial support we identified last week near $1.5960 held on the midweek test. The resistance we anticipated near $1.6050 was frayed intra-day, but held on a close basis. Technical indicators are neutral. However, with euro-sterling bid, and looking poised to test the GBP0.8150-60 area, sterling may under perform. Neutral outlook, but likely a laggard in moves against the dollar.

Swiss franc: The franc was dragged higher by the euro. The franc may under-perform the euro going forward as the euro had approached the SNB's floor. The dollar decline stalled out near CHF0.9250, though we see potential toward CHF0.9200. Resistance is seen around CHF0.9300. It is, frankly, uninspiring. The franc is function of the euro, but without the liquidity.

Canadian dollar: The US dollar traded within about half a cent range against the Canadian dollar. Trend line support we identified, drawn off the Sept 14 and Oct 18 lows has been frayed, but the violation has been minor and the CAD0.9900 level remains intact. No compelling technical signal.Neutral.

Australian dollar: The failure ahead of $1.05 disappointed Aussie bulls and the subsequent pullback saw it fall to the week's lows on Friday just above $1.04. Of the five central banks (ECB, BOE, BOC, RBNZ and RBA) that meet in the week ahead, the RBA is only one that is likely to deliver a rate cut. The Australian dollar could, counter-intuitively rally on a stand pat stance or a 25 bp rate cut that would still leave Australia with the highest nominal and real rates among the major economies. A 25 bp cut is nearly fully discounted in the indicative pricing in the forward market. Signs of the Chinese economy stabilizing and talk of continued reserve managers' interest, leaves us inclined to buy the Australian dollar on pullbacks, provided the $1.0380 area remains intact. More constructive after rate decision.

Mexican peso: In subdued markets, the Mexican peso offered a good place to park funds. The dollar fell to its lowest level against the peso since late October, but the MXN12.90 support area we identified remained intact. A break of the MXN12.90 area should be respected as it would open the door for another 1% dollar slide. On the top side, the MXN13.07-MXN13.10 should contain dollar bounces. Like the yield pick up in quiet markets. Minimal spot appreciation expected near-term.

* Theeuro'sadvance has been a function of short covering rather than the establishment of new longs. Gross shorts fell by 20%, which is the largest weekly adjustment of the year. Note that gross long euro positions actually fell. *Gross shortyenpositions rose by a third to the largest level in five years. The net short position is also the largest since the financial crisis began. *The small net (long)sterlingposition conceals the fact that the gross long position is larger than the gross long euro position. *The reduction of net shortSwiss francpositions was a function of new longs entering and more than twice as many gross shorts covering. * Although the net longCanadian dollarposition increased, the market continued to trim exposure, with gross longs and gross shorts falling slightly. *Despite the efforts by the RBA to talk theAustralian dollarlower, the gross long position continues to grow and is now 5% off the August record high. * The net long peso position increased for the first time in two months as a function of both new longs and a covering of shorts.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sprott - We Will Go Public If They Don’t Send Us Our Silver Posted: 01 Dec 2012 10:01 PM PST  Today billionaire Eric Sprott spoke with King World News about his latest silver offering and how much physical silver it will vacuum out of the market. He also issued further warnings on the crumbling financial system. This is the third and final in a series of interviews with Sprott which reveals what is going on behind the scenes with the increasingly desperate Western central planners and their gold and silver price suppression scheme. Today billionaire Eric Sprott spoke with King World News about his latest silver offering and how much physical silver it will vacuum out of the market. He also issued further warnings on the crumbling financial system. This is the third and final in a series of interviews with Sprott which reveals what is going on behind the scenes with the increasingly desperate Western central planners and their gold and silver price suppression scheme.

This posting includes an audio/video/photo media file: Download Now | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Warren Buffett was

Warren Buffett was  What changed in the last 30 days? Did the world just wake up to the idea that the only way out of this quagmire is a twisted currency war that appears to have re-ignited thanks to Abe's efforts? Something appears to have snapped in the American psyche as the last 30 days have seen the largest physical gold sales on record. Between the

What changed in the last 30 days? Did the world just wake up to the idea that the only way out of this quagmire is a twisted currency war that appears to have re-ignited thanks to Abe's efforts? Something appears to have snapped in the American psyche as the last 30 days have seen the largest physical gold sales on record. Between the  Do you think that is an alarmist headline? Well, I am not the one saying this. Law enforcement authorities all over the country are telling citizens that they can no longer deal with all the crime and that people need to lock their doors and prepare to defend their families. Just recently, the city attorney of San Bernardino, California told citizens to "

Do you think that is an alarmist headline? Well, I am not the one saying this. Law enforcement authorities all over the country are telling citizens that they can no longer deal with all the crime and that people need to lock their doors and prepare to defend their families. Just recently, the city attorney of San Bernardino, California told citizens to " Europe is supposedly fixed and/or well on the path to being competitive and "rebalanced." Or so they say every day. What they don't say, is that to complete the process of rebalancing, in the absence of external devaluation mechanisms under a currency union, is that wages in countries such as Spain, Italy and even France, will have to drop by another 30%-50% for internal imbalances between the Eurozone's nation states to be evened out. What they certainly don't say is how this could ever possible be achieved…

Europe is supposedly fixed and/or well on the path to being competitive and "rebalanced." Or so they say every day. What they don't say, is that to complete the process of rebalancing, in the absence of external devaluation mechanisms under a currency union, is that wages in countries such as Spain, Italy and even France, will have to drop by another 30%-50% for internal imbalances between the Eurozone's nation states to be evened out. What they certainly don't say is how this could ever possible be achieved… Many market pundits seem to have forgotten how strongly QE can affect the price of gold. This gold chart highlights those effects, with a broad green "chart brush". Note the thick green bars. They highlight the gold price action during QE1 & QE2. I believe QE3 (and possibly QE4) will produce very similar results.

Many market pundits seem to have forgotten how strongly QE can affect the price of gold. This gold chart highlights those effects, with a broad green "chart brush". Note the thick green bars. They highlight the gold price action during QE1 & QE2. I believe QE3 (and possibly QE4) will produce very similar results.  There was a degree of predictability about the knockdown in gold and silver at the US futures market (Comex) last Wednesday. The reason is that the Commercials (together the producers, processers, fabricators, bullion banks and swap dealers) have large short positions, so they have a vested interest in lower prices. This is particularly noticeable in silver, which is shown below.

There was a degree of predictability about the knockdown in gold and silver at the US futures market (Comex) last Wednesday. The reason is that the Commercials (together the producers, processers, fabricators, bullion banks and swap dealers) have large short positions, so they have a vested interest in lower prices. This is particularly noticeable in silver, which is shown below.

Today billionaire Eric Sprott spoke with King World News about his latest silver offering and how much physical silver it will vacuum out of the market. He also issued further warnings on the crumbling financial system. This is the third and final in a series of interviews with Sprott which reveals what is going on behind the scenes with the increasingly desperate Western central planners and their gold and silver price suppression scheme.

Today billionaire Eric Sprott spoke with King World News about his latest silver offering and how much physical silver it will vacuum out of the market. He also issued further warnings on the crumbling financial system. This is the third and final in a series of interviews with Sprott which reveals what is going on behind the scenes with the increasingly desperate Western central planners and their gold and silver price suppression scheme.  A lot has been written lately about the

A lot has been written lately about the  Two former governors of the Reserve Bank of India warned Saturday against taking tough measures to rein in gold imports — a major reason for the persistently high current account deficit.

Two former governors of the Reserve Bank of India warned Saturday against taking tough measures to rein in gold imports — a major reason for the persistently high current account deficit. This past March, I asked a highly successful investment advisor what he thought about gold. Since he deals almost exclusively with very high net-worth individuals, his point of view was especially intriguing.

This past March, I asked a highly successful investment advisor what he thought about gold. Since he deals almost exclusively with very high net-worth individuals, his point of view was especially intriguing. Hello from Acapulco,

Hello from Acapulco,

Three months behind schedule,China would finally launch interbank trading with gold contracts on Monday that will help more market forces to influence the countries commodities exchange.

Three months behind schedule,China would finally launch interbank trading with gold contracts on Monday that will help more market forces to influence the countries commodities exchange.

The elaborate Ponzi scheme officially known as the U.S. financial system is set to completely transform into a Monopoly-style fantasy economy where money and debt are both meaningless and limitless. U.S. Treasury Secretary Timothy Geithner has actually come out with a proposal that the American debt ceiling be completely eliminated, allowing the crooks that run the federal government to print as much phony debt currency as their hearts desire, and spend away into oblivion.

The elaborate Ponzi scheme officially known as the U.S. financial system is set to completely transform into a Monopoly-style fantasy economy where money and debt are both meaningless and limitless. U.S. Treasury Secretary Timothy Geithner has actually come out with a proposal that the American debt ceiling be completely eliminated, allowing the crooks that run the federal government to print as much phony debt currency as their hearts desire, and spend away into oblivion. After a wild week of trading, King World News is pleased to share with its global readers the kind of interview you will never see in the mainstream media. This piece lays out the harsh reality of what is really taking place around the world, not the sugar-coated version you see on TV and read in the papers.

After a wild week of trading, King World News is pleased to share with its global readers the kind of interview you will never see in the mainstream media. This piece lays out the harsh reality of what is really taking place around the world, not the sugar-coated version you see on TV and read in the papers. | You are subscribed to email updates from Save Your ASSets First To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment