saveyourassetsfirst3 |

- The Trouble With Return Anomalies

- Seeking Refuge From Market Turbulence With Low Beta Opportunities

- 4 Top Tobacco Stocks

- The Economist on Gold

- Edward Karr Sees Opportunities in Gold: Under the Mattress and in the Ground

- LISTEN: Bob Chapman on Erskin Overnight

- Clive Maund: Silver Market Update – 10.17.11

- Yuan Gold Trading in Hong Kong on Triple Demand…

- Casey Research: Gold mining stocks are dramatically undervalued

- Credit Suisse: 11 defensive stocks to consider now

- Europe now has one week to "fix" the crisis

- Rally in Gold – Over or Yet to Be Seen?

- Gold ETFs gaining in popularity in emerging markets

- Silver Market Update

- One last sell-off for silver before we head back to $50?

- The European Union and SILVER

- Gold and silver prices lifted by Euro hopes

- Steve Rattner, Card Carrying Member of Top 1%, Tells Us We Should Lie Back and Enjoy Much Lower Wages Resulting From Globalization

- Gold & Silver Market Morning, October 17, 2011

- Hong Kong launches Chinese-currency gold trading

- Gold Market Update

- The Gold Standard (Jim Cox)

- The Emergence of the Classical gold standard

- How Gold and Stocks are About to Repeat the 2010 Bottom

- Glossary of Terms in Precious Metals

- The Death of the Cosmos

- Giving Up on Gold

- Hong Kong starts trading gold in renminbi

- MUST WATCH: Cheviot's Sound Money Conference

- Got Gold Report - Crisis Leads to Opportunity

| The Trouble With Return Anomalies Posted: 17 Oct 2011 04:17 AM PDT By James Picerno: Is the small cap risk premium dead? The question endures for a rather practical reason: sometimes the excess return on small stocks vs. large companies evaporates. No one's ever sure if it'll return. That's the nature of return "anomalies." The idea that you'll earn a higher return for owning small stocks vs. large cap stocks is perhaps the most-famous of all the known return anomalies. It's also no stranger to systematic efforts at trying to extract small cap performance gold, as the sea of dedicated funds in this niche reminds. The long run track record certainly looks encouraging, as many researchers have documented through the years. A recent study, for instance, reports a small-cap premium of roughly 200 basis points over large caps in the U.S. since 1926 ("The behaviour of small cap vs. large cap stocks in recessions and recoveries: Empirical evidence for the United States and Canada," by Complete Story » |

| Seeking Refuge From Market Turbulence With Low Beta Opportunities Posted: 17 Oct 2011 04:08 AM PDT By Jim Pyke: The S&P 500 has become increasingly volatile over the past several months. Increasing uncertainty about economic conditions across the globe have resulted in rapidly fluctuating stock prices. I've noted in earlier articles that global equity markets have become increasingly correlated, hence, the one-time refuge of foreign stocks, even emerging markets, is no longer available. The SPDR S&P 500 trust ETF (SPY) has shown an up-tick in volatility. Over the past 3 years, its monthly volatility was 5.3% while over the past 3 months it has ticked up to 6.3%. Beta measures the level of market exposure for a given security. A high beta is often used as shorthand for a risky or growth stock, while a low beta is traditionally associated with "safer" stocks, such as utilities. Gold is typically not correlated to the market as a whole and hence has a beta around 0. Betas can range from across Complete Story » |

| Posted: 17 Oct 2011 03:51 AM PDT By Stockerblog: In the state of Minnesota, there is a requirement that cigarettes have to carry a Fire Safety Compliant label, which means that the cigarettes will go out after a short period of time if they are not being smoked. One investigation shows that this fire compliance doesn't necessarily work. Whether or not this type of compliance will spread across the United States is uncertain. Certain investors, not just socially responsible investors, will avoid tobacco and cigarette stocks due to health concerns. However, many investors like the high yields of these stocks. One example is Lorillard, Inc. (LO) which has a dividend payout of 4.4%. The stock, which markets the Newport, Kent, True, Maverick, Old Gold, and Max brands, trades at 14 times forward earnings. According to WallStreetNewsNetwork.com, there are over half a dozen tobacco stocks with yields in excess of 4%. Another example is Vector Group Ltd. (VGR), a Florida Complete Story » |

| Posted: 17 Oct 2011 02:33 AM PDT |

| Edward Karr Sees Opportunities in Gold: Under the Mattress and in the Ground Posted: 17 Oct 2011 02:29 AM PDT |

| LISTEN: Bob Chapman on Erskin Overnight Posted: 17 Oct 2011 02:22 AM PDT Bob Chapman form the 10.15.11 Erskine Overnight. ~TVR |

| Clive Maund: Silver Market Update – 10.17.11 Posted: 17 Oct 2011 02:05 AM PDT From Clive Maund: CLICK IMAGE TO ENLARGE

Silver looks set to break down short-term and drop as the dollar stages a recovery rally, but the expected drop should be nowhere near as severe as the September plunge, and it will provide a final opportunity to load up with silver and Precious Metal investments generally ahead of the major rally that the COTs are presaging. Read more @ CliveMaund.com |

| Yuan Gold Trading in Hong Kong on Triple Demand… Posted: 17 Oct 2011 01:54 AM PDT |

| Casey Research: Gold mining stocks are dramatically undervalued Posted: 17 Oct 2011 01:39 AM PDT From Jeff Clark, Casey Research: By almost any measure, gold stocks are undervalued. Should we load up? After completing my research on this question, I’m convinced more than ever that we at Casey Research are in the right place. See if you agree… Let’s first get a handle on the degree of undervaluation. The more undervalued, the lower the buying risk. A fairly valued stock, on the other hand, requires added caution. Gold accelerated higher last month, peaking around $1,900/ounce, while gold stocks lagged. Here’s a chart of the HUI-to-gold ratio (HGR). In a rising gold environment, a climbing HGR indicates that gold stocks are outperforming the metal; a falling HGR means they’re trailing gold. Today’s 0.33 HGR means gold stocks as a group have not been this cheap, relative to their underlying metal, since January 2010. And a lower ratio hasn’t been seen since... Read full article... More on gold and gold stocks: Gold is approaching a "major crossroads" These gold mining stocks could lead the next rally Three ways the government will try to confiscate your gold |

| Credit Suisse: 11 defensive stocks to consider now Posted: 17 Oct 2011 01:38 AM PDT From Pragmatic Capitalism: Credit Suisse says the economy has moved into a contraction cycle. And that means the portfolio require adjustment. They use a cycle-clock indicator to determine their equity allocation based on the performance of particular sectors during various portions of the business cycle. Based on their work, they provide 11 names that are consistent with a slower growth environment: "We underline that markets are already pricing in a contraction phase, and as such, we resist a 'knee-jerk' change in asset allocation. More specifically, over the past seven contraction phases, equities have... Read full article... More on stocks: These ETFs could be great trades in the next market pullback Porter Stansberry: Don't invest another dollar before reading this Two defensive dividend payers that are trouncing the market this year |

| Europe now has one week to "fix" the crisis Posted: 17 Oct 2011 01:23 AM PDT Germany could take the brunt of responsibility... From Bloomberg: European leaders have one week to settle differences and flesh out a strategy to terminate their sovereign debt crisis as global finance chiefs warn failure to do so would endanger the world economy. Group of 20 finance ministers and central banks concluded weekend talks in Paris endorsing parts of the emerging plan to avoid a Greek default, bolster banks and curb contagion. They set an Oct. 23 summit of European leaders in Brussels as the deadline for it to be delivered. "The risk of a recession would be increased dramatically were the Europeans to fail to accomplish goals that they've set for themselves," Canadian Finance Minister Jim Flaherty said after the G-20 meeting, which ended Oct. 15. Two years to the week since Greece triggered the turmoil by revising its budget math, the inability of policy makers to stamp it out has pushed the Greek government to the edge of default and the European economy close to recession. Stocks and the euro extended last week's gains after the meeting. The Stoxx Europe 600 Index added 1.3 percent to 241.59 at 9:15 a.m. in London. The euro rose 0.2 percent to $1.3904, following a 3.8 percent weekly advance, the biggest since March 2009. Greece's Vote Hurdles to overcome for an accord include resistance from bankers to a deeper restructuring of Greek debt as well as disagreements between Europe's capitals over just how to multiply the firepower of their bailout fund and recapitalize financial institutions. Greece's parliament faces another tight vote on new fiscal measures as soon as this week, a showdown that Prime Minister George Papandreou needs to win to ease the way for more foreign financing. The Brussels meeting "has the potential to turn into a positive historic moment," Joachim Fels, London-based chief economist at Morgan Stanley, wrote in a note to clients yesterday. "But it could also easily turn into a negative catalyst." Europe's plan, which has still to be made public, includes writing down Greek bonds by as much as 50 percent, establishing a backstop for banks and magnifying the strength of the 440 billion-euro ($611 billion) temporary rescue fund known as the European Financial Stability Facility, people familiar with the matter said last week. "The plan has the right elements," U.S. Treasury Secretary Timothy F. Geithner said in Paris. "They clearly have more work to do on the strategy and the details." Cannes Summit The G-20 officials – who met to prepare for a Nov. 3-4 gathering of leaders in Cannes, France – said in a statement that the world economy faces "heightened tensions and significant downside risks." European authorities must "decisively address the current challenges through a comprehensive plan," they said. The policy makers held out the possibility of rewarding European action with more aid from the International Monetary Fund, while splitting over whether the Washington-based lender's $390 billion war chest needs topping up. Europe's latest strategy hinges on putting Greece, whose government forecasts its debt to reach 172 percent of gross domestic product in 2012, on a sustainable path. Austerity has plunged the country deeper into recession and provoked civil unrest that threatens political stability. Wage Cuts Papandreou faces the latest test of his party's unity as soon as this week when he asks Parliament to approve steps including bigger pension and wage cuts as well as plans that may lead to the dismissal of 30,000 state workers. One ruling party lawmaker, Thomas Robopoulos, said he may quit his seat ahead of the vote, exposing the tensions in Papandreou's socialist party. It has 154 seats in the 300-member chamber. Failure to limit the risk of a default to Greece led to Portugal and Ireland requiring bailouts, and markets are now targeting larger debt-strapped nations such as Italy. Investors are concerned that if the crisis keeps festering, the world economy could face a repeat of the chaos that followed the 2008 collapse of Lehman Brothers Holdings Inc. (LEHMQ) The euro area is already set to suffer a renewed recession, say economists at JPMorgan Chase & Co. and Goldman Sachs Group Inc. "We're aware of our responsibility," German Finance Minister Wolfgang Schaeuble said in Paris. "We'll solve the problems in the euro zone." Crisis Plan In the works is a five-point plan foreseeing a fix for Greece, boosting of the rescue fund, fresh capital for banks, a new push to increase competitiveness and consideration of European treaty amendments to tighten economic management. Proposals include revising a voluntary July accord struck with investors for a 21 percent net-present-value reduction in Greek debt holdings. One variant would take that reduction up to 50 percent, and a more aggressive suggestion is for investors to exchange Greek bonds for new debt at a lower face value collateralized by the euro area's AAA-rated rescue fund, the people said. The ultimate choice is a restructuring involving writedowns without collateral. Highlighting potential opposition from bankers this week, Charles Dallara, managing director of the Institute of International Finance, told the Financial Times in an article published Oct. 15 that he doesn't "see a compelling case" to reopen the July deal. The imposition of greater losses on investors may prompt them to sell other European bonds, he said. The European Central Bank has also signaled it doesn't favor a rewrite of the three-month old accord. Bank Liabilities The bank-aid model under discussion is to set up a European-level backstop capitalized by the EFSF, the people said. It would have the power to take direct equity stakes in banks and provide guarantees on bank liabilities. Such ideas are controversial in Germany, which has called for recapitalization on a country-by-country basis. European Union Economic and Monetary Affairs Commissioner Olli Rehn told Bloomberg Television on Oct. 15 that euro-area authorities are "close" to a pact. Banks may be required to maintain a 9 percent capital buffer to absorb sovereign risks, up from the 5 percent core capital level used in July's stress tests, a person with knowledge of discussions said last week. How to magnify the strength of the EFSF may also sow discord this week. Options include enabling it to borrow from the ECB or using it to partly insure new bonds issued by distressed governments. The ECB has all but ruled out the first method, making bond guarantees more likely, the people said. Bond Guarantees The guarantees of new bonds sold by distressed euro-area governments might range from 20 percent to 30 percent, a person familiar with those deliberations said. Recourse to bond insurance suggests the central bank will need to maintain its secondary-market purchases for an unspecified "interim" period, the people said. ECB President Jean-Claude Trichet, who attended his last G-20 meeting before he retires Oct. 31, reiterated the central bank hopes to stop purchasing government bonds once the EFSF is able to take over. A consensus is nevertheless emerging to accelerate the birth of a permanent aid fund by a year to July 2012. This week's discussions will also look at easing unanimity rules that permit solitary countries to block bailouts. Morgan Stanley's Fels said the steps could backfire because investors may fail to be lured by the guarantees, harsher writedowns could spark contagion and banks would likely prefer to sell assets and reduce leverage than raise capital. What's really required is leaders to take a "big step" toward fiscal integration, he said. The coming weekend "is the moment people are expecting something quite impressive," U.K. Chancellor of the Exchequer George Osborne said in Paris. To contact the reporters on this story: Simon Kennedy in Paris at skennedy4@bloomberg.net; Theophilos Argitis in Paris at targitis@bloomberg.net; James G. Neuger in Brussels at jneuger@bloomberg.net. To contact the editors responsible for this story: Craig Stirling at cstirling1@bloomberg.net; James Hertling at jhertling@bloomberg.net. More on the euro crisis: This chart says the euro crisis is not over yet The best and worst case scenarios for the euro crisis now Amazing story: One Texas investor could make 65,000% when Greece defaults |

| Rally in Gold – Over or Yet to Be Seen? Posted: 17 Oct 2011 01:00 AM PDT SunshineProfits |

| Gold ETFs gaining in popularity in emerging markets Posted: 17 Oct 2011 01:00 AM PDT Experts predict that the demand for gold exchange traded funds (ETFs) will grow significantly in emerging countries in the coming years. India's population in particular is known for its affinity for ... |

| Posted: 17 Oct 2011 12:28 AM PDT Silver's 3-wave A-B-C correction is believed to be complete, with the savage A and C waves serving to both flush out and wipe out Large and Small Specs and transfer their assets to Big Money interests. Like gold its suspected bear Pennant of a week ago now looks more like a completing base pattern, and also like gold it has risen to arrive at an important resistance level which is centered on $33. |

| One last sell-off for silver before we head back to $50? Posted: 16 Oct 2011 10:31 PM PDT By Peter Cooper of ArabianMoney: A sprightly 87-year old President Carter was on the BBC last night for a long interview, and sounded very impressive unless you are old enough to remember his abysmal presidency. The man himself comes across as a bit of a 60s dreamer with flowers in his hair and peace and love stamped on his face. He is very genuine and has not made a cent out of being an ex-president. But he was a disaster, hopelessly out of his depth in Washington during a period when the world needed leadership. Hunt Brothers So where are we today for the tiny global silver market? We still seem to be in the early days of an inflation, and could even have another deflation of asset prices on our hands if the eurozone messes up its bailout package or a rapid inflation if they double-up on money printing as most seem to expect. It is never that easy to judge is it? And markets are so confused they are not giving us much guidance. Technical analysis is only right until it it wrong as fundamentals tend to repeat but never exactly. But the silver charts are predicting another backtracking in prices, according to the singularly precient CliveMaund.com. At a fundamental level that could come from another nasty twist in the eurozone saga sending markets into a dive and a flight to the US dollar and out of silver and gold: 2008 revisited! However, trying to market time anything these days is very difficult. The good news about silver is that when this sell-down is complete the next target is very obviously the April high of $50, also the 1980 high for the metal. 1980 All-Time High If you wanted a surefire bet the idea that any commodity could stay below its 1980 all-time high forever just has to be a nonsense. Reason then to hold your silver just in case the market turns up without this expected sell-off, and it did just that a year ago. Perhaps the eurozone officials have it sussed after all. Then again even dear old Jimmy Carter could manage to up inflation.

To capture all the upside in the coming price boom you are more than likely going to do much better by staying fully invested or you might miss one or two of the best phases. Where should silver prices be and how high will they go? Who knows, silver might be worth more than gold but prices will be very, very much higher. But taking a series of leveraged punts on silver is far more likely to leave you penniless than rich as your timing will be wrong more than it is right. More @ ArabianMoney |

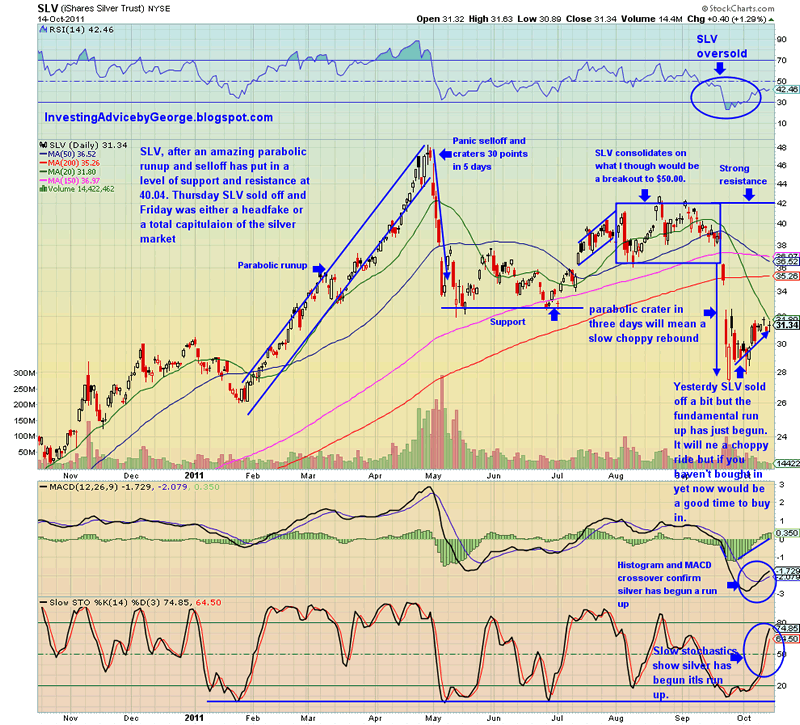

| Posted: 16 Oct 2011 10:25 PM PDT By George Maniere: There is just one small little baby hic-cup. Europe is toast! The likelihood of Europe surviving grows slimmer every day. Let's get this straight right away. Europeans are not happy with the Euro and the common citizens feel the whole creation of the European Union was a big mess. The European politicians don't see this as a political problem but rather as a logistical one because they have to somehow sell the consolidating of the bonds to the public. If the European Union is going to survive it has to make the hard choice. It must consolidate all of the existing national debts into one "Eurobond." The simple fact is that the failure to do this will cause the banks to fail and then we get to see the man behind the curtain. The truth about the accounting will rise to the surface. The lack of mark to market accounting that was installed as a quick fix following 2007 has only severed to make the bank's balance sheets even more obtuse. Remember Collateralized Debt obligations (CDO'S) and Credit Default Swaps (CDS) – that's the man behind the curtain. An interesting and potentially tradable condition is unfolding this week in the small silver market. Traders worldwide are watching to see if silver "respects" its May lows or instead falls below them to test/establish new correction lows. Just below is a chart of the largest silver ETF, (SLV) as a proxy for silver, the commodity. CLICK IMAGE FOR A LARGER VIEW A look at this chart will show a picture of Silver's (SLV) late-April sell-off of 40% the first week of May. For almost three months silver seemed to consolidate and began a run up when it ran into resistance at $42.00. I can only conclude that the investors who had bought up in this range wanted out of silver even. From there it bounced from $38.00 to $42.00 when Dr. Bernanke announced "Operation Twist." This sent the dollar up and investors fleeing gold and silver. A look at the chart will show that silver lost 25% in 1 week. It has fought its way back to close on Friday at $31.34 and that begs the question where do we go from here? There is no doubt that silver has had a tumultuous year. There is also not a doubt in my mind that silver will continue to increase in value as long as we continue the printing of fiat paper to solve our financial problems. My regular readers know that I am fond of Gerald Loeb. In his epic tome "The Battle for Investment Survival" he writes that it is human nature to see more dollars tan we had last week and think that we are doing well financially. This however is sheer folly. The true test of a currency is not how many you have but rather what is the value of the currency. Voltaire said in the 1700's "paper currencies will always revert to their intrinsic value – zero." This leaves the question where does the average man go to protect the value of his money? This leads me to gold and silver. Gold and silver have always been currency. It has always been so. There are many that would argue that gold is money and silver is an industrial metal. I would beg to differ. According to Black's Law Dictionary, it means gold, silver, or paper money used as circulating medium of exchange. In its strict technical sense money means coined metal, usually gold or silver, upon which the governments stamp has been impressed to indicate its value. I think the U.S. Mint might make a case that we can establish as to the current status, and this is what is clearly stated on their Web site. American Eagle Silver Bullion Coins are affordable investments, beautiful collectibles, thoughtful gifts and memorable incentives or rewards. Above all, as legal tender, they're the only silver bullion coins whose weight and purity are guaranteed by the United States Government. They're also the only silver coins allowed in an IRA. In an email from one of my readers he said that $1923 was the peak for gold and could spend the next few years correcting. $50 silver will depend on gold, the odds of which look extremely low. The correction in USD either finished on Friday or will soon, as with TLT. Equities and metals are set up for an interim fall. In conclusion, I try never to look at any holding in the micro lens (except leveraged ETFs like SPXU, UPRO, TZA and FAZ). I try and look out further into the future and see where a particular stock or commodity will be in one, two or three years. Bearing this in mind I will continue to do what I have always done and that is when the occasion is right I will buy physical, gold and silver and in the short term keep an eye on the trading ranges of gold (GLL and UGL) and Silver (ZSL and AGQ). More @ InvestingAdviceByGoeorge

|

| Gold and silver prices lifted by Euro hopes Posted: 16 Oct 2011 09:45 PM PDT Though many remain wary, stocks and commodities are continuing to rise on hopes that European leaders are at last arriving at a plan to address the eurozone's sovereign debt problems. Gold and ... |

| Posted: 16 Oct 2011 09:06 PM PDT A corollary to Upton Sinclair's famous saying, "It is difficult to get a man to understand something if his salary depends on his not understanding it" is "People promote ideas that help them secure or preserve a privileged position on the totem pole." A glaring example of these observations came in an op ed in the Sunday New York Times by Steve Rattner, former Lazard mergers & acquisition partner, later head of the private equity firm, Quadrangle Partners. He is best known as the chief negotiator in the auto bailouts (and he was criticized for not involving any auto industry experts). He paid $10 million to settle a kickbacks investigation and agreed not to work for a public pension fund in any role for five years. I happened to see Rattner on a panel at a Financial Times conference earlier this week and he elaborated on some of the themes in this piece, "Let's Admit It: Globalization Has Losers," which reader Brett asked me to debunk line by line. I'll spare you and focus just on the most critical and bald-facedly dishonest bits. Let's start at the top:

Apparently the NYT fact checkers give guys at Rattner's level a free pass. This is false. Where was Rattner in 2007 and 2008? Real median income peaked in 2007, and that was modestly higher than in the last cyclical peak, in 1999. The decline in income (nominal, not just inflation adjusted) is the direct result of the global financial crisis, not inflation. So his entire piece is based on an inaccurate claim which has the effect of diverting blame from bankers like him. This next bit is sneaky but worth pointing out:

We don't have a system of free trade. It's managed trade. As William Greider has pointed out, most other countries play the game in a way to produce better national outcomes (fewer lost jobs and trade surpluses). We seem to be running our trade policy not to optimize our national interest, but that of large international corporations, which is far from the same thing. The next bit is pure reductivism:

American management is also more expensive than management in Mexico or China or India. And I think you'd be hard pressed to say American management is better than management, say, from Sweden or Australia, where CEOs are vastly less well paid than here. So shouldn't we expect CEO and upper management wages also to fall? And remember, as we have said in other posts, the evidence is overwhelming that not only is CEO pay in the US not correlated with performance, it is negatively correlated with performance. The best paid CEOs deliver the worst results, and the leaders of Jim Collin's stellar performers in Good to Great all paid themselves modestly. We need to peel back several layers to debunk this notion that labor costs trump everything. First is that Rattner is implicitly arguing that the world is frictionless. But that is misleading. The US is a big market, and there are advantages in being close to the customer, in terms of rapid response, carrying smaller inventories (and thus having smaller losses when you get it wrong), lower shipping and financing costs. IKEA, which is in a low end manufacturing business, has its manufacturing for the US located in the US. Second, he is also assuming that all products are more or less commodities. But the job of management is to find a way to gain competitive advantage, and being a low cost competitor is one of many options. I'm sure you've paid a big premium to buy food or a drink at a convenience store now and again. They are competing on location, not cost. Similarly, I'm always amused at techies who hector Apple product users in comments. They seem angry that consumers will pay a big premium for ease of use or maybe just sheer coolness (and I have to say, as a Manhattan person, being able to see a live person at 3 AM and get something diagnosed and fixed is worth a lot to me). So a fixation on costs too often reveals a management lacking in imagination and gumption facing increasingly competitive and mature markets. Third, his focus on direct factory labor is disingenuous. Direct factory labor is typically just north of 10% of the cost of most manufactured goods; for cars, we are told it's 13%. Even if you can extract meaningful savings there, you have significant offsets: the upfront cost of re-orgainzing production (which in the outsourcing scenario include hiring costly outsourcing "consultants" and paying attorneys to paper up the deals), higher ongoing managerial costs, higher shipping and related inventory financing expenses. Yes, there are cases where outsourcing and offshoring have been a big success, but there are also others where the benefits have been underwhelming and have come at considerable costs to US workers, communities, and the economy (see a very good long form discussion by Leo Hindery). And in many cases where big multinationals come out ahead, it isn't due solely to labor cost savings. As Greider pointed out:

And this sort of thing continues. I discussed long form the fate of a world class coated paper mill in Escanaba, Michigan. The main culprit in its demise was overleveraging and excessive compensation to executives who knew bupkis about the paper industry. But another factor I did not include in my getting-to-be-too-long post and was pointed out by readers in comments were the considerable subsidies given by the Chinese and Indonesian governments to their papermakers. Consider the implications: if the only factor at work were factory labor, as Rattner implies, you'd see far fewer jobs ceded to foreign markets (put it another way: if the labor cost differential were a sufficient inducement, foreign governments wouldn't need to offer such generous subsidies). To put it another way, the argument that Rattner is making is basically that of the Stopler-Samuelson theorem. Let's turn the mike over to development economist Dani Rodrik:

So to give an example: Let's say that as a result of globalization, the wholesale price of a car falls from $20,000 to $15,000. Let's further assume that materials costs were $6000, direct factory labor was $3000, factory overheads were $2000, shipping is $1000, marketing is $2500, other management costs (top brass, IT, legal, accounting) were $2000, interest cost are $1000, and $1500 is for capital investment (as in repairs and replacements), with a target profit of $1000. Per Stopler-Samuelson, something has gotta give to get the manufacturing price down to $15,000. But it does not have to be worker wages. For instance, over the years, we've seen manufacturers of all sorts get smarter (and in some cases, just stingier) in their use of raw materials. And all bets are off if you increase productivity. That means you can use fewer workers, but maintain their pay levels. As Rodrik continues by discussing a paper by Broda and Romalis that found that trade with China reduced income inequality in the US. Huh? Per Rodrik:

So this is where the misdirection by Rattner is crucial. Until the 2000s, in every economic expansion, labor got the bulk of the increase in GDP, typically over 60%, via more jobs and increased pay. Post 2000, there was an astonishing change, a shift from labor share, which fell to below 30%, and a massive increase in corporate profits. In other words, there was huge shift away from labor to capital. This has little to do with globalization and much to do with the weakened bargaining power of US workers. As much as it has become fashionable to look down on unions (and their corruption and short-sightedness hasn't helped), having well paid blue collar workers helped the negotiating position of non-unionized white collar employees. Rattner also conveniently fails to discuss how the rapacious tendencies of private equity firms made matters worse. An unduly candid investor described the business model in Confidence Men: pile debt on the acquisitions, and if only one of ten made it (meaning survived!) you still made a good return for investors. So many companies in Europe have gone bankrupt thanks to the tender ministrations of PE pirates that the officialdom has read them the riot act. PE firms have to register, and they cannot either buy companies or raise money in the Eurozone unless the conform to regulations, which include strict limits on leverage. Rattner argues in his piece that we should imitate Germany and focus on high skill manufacturing. But Germany's population is roughly 1/4 ours and they already dominate certain niches. Rattner at the FT conference called for the US to start producing more engineers, which readers will laugh out of the room. Engineers don't get paid enough for more people to want to seek out that career path; many of you have told me the only way to make a good living was to get another degree, like law, and go into another line of work. And even if copying Germany might be a viable approach, it would take something like industrial policy to get there. Note the US already has industrial policy by default, with banks, the mortgage-industrial complex, military contractors, agriculture, and Big Pharma among the favored groups. But no, Rattner pooh-poohs the whole idea. Better to have industrial policy determined by lobbying effectiveness than a more thoughtful process:

I wish I had the space to discuss Solyndra in depth, but the sort form is that the failure of that deal is not an indictment of the overall program. If you are a VC investor, you expect a certain percentage (actually a pretty high percentage) to come a cropper. Solyndra was only a bit over 1% of the portfolio, and it appears to be the only loss. This looks like a classic "shit happens" deal failure: the investment looked sensible at the time, silicon prices collapsed, which had a direct, negative impact on competitiveness. Even so, a later-stage independent investor provided funding, which further confirms the original investment was not misguided (you'd get no rescue investors coming in if it looked like a hopeless turkey). Rattner apparently missed a different Rodrik article, a Financial Times op ed, in which he warned:

Yet an unfettered system is precisely what Rattner is promoting, no doubt because it works to his and his fellow rentiers's advantage.

|

| Gold & Silver Market Morning, October 17, 2011 Posted: 16 Oct 2011 09:00 PM PDT |

| Hong Kong launches Chinese-currency gold trading Posted: 16 Oct 2011 07:05 PM PDT Hong Kong on Monday introduced gold trading quoted in Chinese yuan, making it more convenient for holders of the currency to invest in the precious metal, and opening a new channel for hedging. The Chinese Gold & Silver Exchange said Monday that the service, dubbed "Renminbi Kilobar Gold," is designed to appeal to both retail and institutional investors. The product is among the latest offerings designed to tap the fast-growing pool of yuan deposits within Hong Kong banking system since an expanded settlement scheme came into effect in June 2010... Read |

| Posted: 16 Oct 2011 05:28 PM PDT |

| Posted: 16 Oct 2011 04:45 PM PDT CGE |

| The Emergence of the Classical gold standard Posted: 16 Oct 2011 04:45 PM PDT Oxford.edu |

| How Gold and Stocks are About to Repeat the 2010 Bottom Posted: 16 Oct 2011 04:36 PM PDT |

| Glossary of Terms in Precious Metals Posted: 16 Oct 2011 03:30 PM PDT CMI Gold and Silver |

| Posted: 16 Oct 2011 03:10 PM PDT --In today's Daily Reckoning we will offer a revolutionary theory that explains and predicts the life and death of economic systems. This theory will show you that any economic order must ultimately fail if it is based on the illusion of control. But before we get to that, we should probably talk about the terrestrial world and the stock market. --The stock market is stuck in a trading range. For an explanation of that range, we refer you to the inimitable Murray Dawes. The technical picture of the markets is helpful now because it strips out all the noise. It tells you what investors are actually doing. And what they're doing is vacillating between abject fear of systemic collapse and the need to preserve and grow their money before retirement. --It's not an enviable position. But no one said the road to wealth through financial asset inflation would be an easy one. More on that shortly. --What about Greece? It's still there. G-20 honchos met in Paris over the weekend. No big announcements were made. If anything, the G-20 finance ministers handballed it to the French and the Germans. This is fitting. It's a test of whether the pan-European project is going to end after 60 years and lead to a break up, or whether further "union" in Europe is possible. --Specifically, the G-20 lot has given the two pillars of the European Union the job of figuring out three things: how to organise an orderly write-down of Greek government debt, how to recapitalise European banks, and how to prevent the Greek strategic default from infecting Spain and Italy. --The deadline for having a fix in is October 23rd. That's when the political leaders of the European Union meet in Brussels to sign off on the expanded European Financial Stability Facility (EFSF). That particular European slush fund has around $600 billion in it. But Europe's leaders think it will need more to boost capital in European banks after bond holders (European banks) take a 50% write-down on their Greek government bonds. --As you can see, not much has changed in the last week. We're on the slow-road to crisis. But the spring weather in Melbourne makes it hard to worry too much. The Europeans will figure it all out, won't they? And besides, that's in Europe. We're here in Australia, which is not Europe. --Still, there are some weird and worrying signs. IMF President Christine Lagarde speaks of "precautionary credit lines" being extended to "non-consenting victims of the economic crisis". The credit lines aren't loans as such. They are a little like the Berlin Air Lift, we suppose...a way of dropping in extra liquidity to prop up the balance sheets of banks whose equity might be wiped out by a Greek default. --Once again, the use of baffling terms like "non-consenting victims of the economic crisis" tells you something funny is afoot. Does a victim ever consent? Isn't the definition of a victim someone who has a harm imposed on him or hers without consent? Obfuscation is the last stand of the intellectually bankrupt...or...when they can't win because their ideas suck...they try to baffle you with language. --This brings up a strange point about the world we're living in that MAY be in Australia's favour. The IMF is a global slush fund that normally loans money to bankrupt governments in exchange for economic policy changes that favour Europe and the United States. But the IMF is made up of the most deficit-challenged governments in the world. How can they be loaning money to anyone, much less telling anyone else how to manage their economy? --There is a shift in the global balance of power underway at the moment. In 2005, we dubbed it "The Money Migration". The G-20 has been expanded from the G-3, and the G-4, and the G-7 and the G-8 because the industrial Welfare states have become less productive over the last 30 years and grown large structural government deficits. --Now you have a world where the poorest countries - Brazil, India, and China - are creditors to the so-called rich countries, the US, the UK, much of Europe. The creditors have gained in political power as the debtors consumed their way to decadence. Which brings us back to the point of asset inflation. --One of the reasons, we reckon, so many people are sympathetic to the Occupy Wall Street sentiment (despite the sheer ignorance of many of the participants) is that they sense something in the financial system is not right. The incentives are not aligned for normal people to produce things, save money, and get wealthy. --Instead, we have a financial system built on unsound money. In that system, the incentive insists for the financial sector to expand credit and put people in debt. It can do so by creating money from virtually nothing with fractional reserve banking. It can then loan that money to households, businesses, and governments at a handsome rate of interest. --The financial sector and the investing class benefit in one shared way from a world of unsound money and credit growth: asset price inflation. In Australia, this is favourably called the nation's retirement assets saved up via superannuation. --People are now sensing that only the financial sector truly benefits from inflation. It amounts to a wealth transfer from productive people to money shufflers. Most people don't quite understand how it happened or even how it works. But they sense it. And it makes them very angry. --But we think the people bedding down with the Occupy Wall Street movement are making a crucial mistake in their thinking. We didn't realise this until we read the introduction of Lee Smolin's The Life of the Cosmos while doing laundry on St Kilda road. --Smolin makes the great point that in our age, scientists have replaced priests as the people with the most authority to explain the universe we live in. Scientists with a philosophic bent are called cosmologists. Cosmos is derived from the Greek word for order. --The idea that the universe is ordered - according to the immutable laws of Nature (or given by God) - is a standard conception of the world we live in. But herein lurks a temptation. The temptation is to meddle. Let us briefly explain. --If the world is ordered according to certain laws, then we can understand how it works in a mechanical, scientific way. And if we can understand how a machine works, certainly we can modify the machine to produce more desirable outcomes. A scientific, mechanistic view of the world, in other words, leads us to place great faith in the ability of scientists to diagnose problems and prescribe solutions (sort of like global warming). --But Smolin offers another theory. His theory is that that the universe is an evolving thing, not a static system governed by immutable laws. If he's right, then understanding the universe is more about understanding the processes of evolution. We'll have more from Smolin tomorrow. --In the meantime, what does this have to do with anything? A lot of the protesters we have heard yammering on YouTube and in the media are talking about changing the system. The most common idea is to police corporate greed by making government more powerful. They would also, we imagine, like to outlaw greed and make equality compulsory and justice absolute. --But you can't change human beings. You can only change their rules of engagement with each other and the world. The most important change you can make to a system is a change to the rules that govern it. --That system produced prosperity and wealth and improved standards of living for billions of people. It's been perverted by the introduction of unsound money, the predatory nature of the Welfare State, and relentless intervention into private and public life (as advocated by all the economists who are subsidised by and profit from the government). --Any changes to the system that don't address the soundness of money won't result in a better system. A new system that hasn't addressed the failure of fiat money and the oligarchic power of a central banking cartel will be like a Tyrannosaurus Rex with a new fluffy pink tail, or a giraffe that has been taught to roller skate...an adaptation that leaves the resulting being completely unable to compete and survive in the world. --Tomorrow, more on the origin of revolutions and how self-ordering systems are better than ones designed by people who want to control everything. The old order is ending. The cosmos is giving way to chaos. But what comes next? Find out tomorrow! Dan Denning

|

| Posted: 16 Oct 2011 02:44 PM PDT Nothing much to talk about in the markets yesterday. We had been expecting a bigger sell-off in the price of gold. The metal went down, about $300 if we recall correctly, but not as much as we expected. In the last major bull market in gold, in the '70s, the price declined by about 50% before going on to set a new record. The pullback in 1974 caused investors to question the premise of the whole bull market. Many dropped out and missed the big payoff. Markets always test their admirers. The old-timers — such as Richard Russell — refer to the "50% principle." A bull market can be expected to retrace as much as 50% of its gains...before going on to fulfill its destiny. If it goes down more than 50%, however, the bull market may be over. Unfortunately, these are not hard and fast rules. Just old timers' tales. Still, they are useful for understanding how markets work...and for keeping you from making a big mistake. This gold market barely corrected 20% of its gains. Is that all there is? We don't know. Doesn't seem like enough. We didn't feel tested at all; did you? That was part of the reason we thought the economy was sliding into a Rip Van Winkle slumber. It would be a real test. Imagine that China slows down. Imagine that Europe lurches from one crisis to another. Imagine that the US economy follows Japan down that long, slow, slumpy road. What do you have? Falling prices for almost everything — including gold. And with falling prices for other assets, investors, savers, insurance companies, pension funds all put their money into US Treasury debt. This keeps rates low and it allows the US to fund its deficits almost indefinitely. The economy never recovers, but it doesn't die either. Bernanke and crew may want to do something dramatic and foolhardy. But they wouldn't have to. As in Japan, they could just bide their time... Pretty soon, people would come to think that the world economy had entered a more or less permanent phase of low growth and low inflation. And then, what would happen to the price of gold? It would fall. People buy the inert metal to protect themselves from very ert humans. But if the humans who run central banks and Treasury departments sit still, why hold gold? The logic of the gold bull market is that the feds have done, and will do, stupid and disastrous things to the monetary system. Perhaps they will. But as long as they are able to finance large deficits painlessly, they have no reason to do so. Instead, they will take economist Richard Koo's advice and use deficit financing to pay for fiscal stimulus projects. Infrastructure projects...transfer programs...tax the rich...bread and circuses for the poor — this could go on for a long time. When speculators and savers realize that they need not hold gold to protect themselves from the feds, they will sell it. The price will fall — perhaps below $1,000. Then, we will have a real test. If the economy is stuck in a low-inflation phase, why own gold? If the feds do not have to print money, why would they? If prices — in dollar terms — are stable or going down, why not just stick with dollars? We can see the headlines now:

"Investors give up on gold." And then, you, dear reader. What will you do? The logic of the bull market will have disappeared. Will you give up on gold too? In the near term, things are actually looking up for gold. In fact, since it didn't fall as much as we expected...perhaps our Japan-like disinflationary slump has been delayed...or derailed? Right now, the central banks are all itching to meddle. Bernanke's "twist" program is a waste of time. It merely takes the Fed's money and switches it from short-term US Treasury debt to longer-term Treasury debt. It is a very bad idea — leaving the Fed itself exposed to huge losses. But that's another story. But it is unlikely to have any advantage for the economy. Mortgage rates are already the lowest in half a century. Pushing them down a little more isn't going to make any difference. Several members of Bernanke's FOMC group are already calling for more forceful intervention — some form of QE III. If the economy deteriorates, there is bound to be more action from the Fed. Meanwhile, the Europeans are "recapitalizing" their banks (see below). So are the Chinese. The capital has to come from somewhere...or they have to invent it. The more new money they create, the less their old money is worth...and the more attractive gold becomes. *** "My friends and family warned me. They thought I was making a big mistake by not buying a house." An Irish friend tells us what it was like for a renter during the great housing boom. "The idea was that housing prices always went up. Ireland is a small country. There were new people coming in from Eastern Europe. There were also a lot of Irish people coming back from overseas. We were the 'Celtic Tiger,' after all. The land of opportunity. "So people thought housing prices could only go one way — up. And you had to get on the escalator as soon as possible. Otherwise, you would be left behind. You had to buy a starter home...like one of these new apartments." We were driving by a housing development, almost in the shadow of the Wicklow mountains. On the right hand side was a very new apartment complex. "See all those apartments. They're empty. They can't sell them. They were just a little late to the party, I guess. They probably started construction in 2006 and by the time they were ready to sell, the lights had already been turned off. "You had to buy a starter home when you were in your 20s so that you could trade up to a family home when you were in your 30s. Prices were rising all the time, so if you didn't have a starter home to trade in you'd never have the money to buy a family home. I guess that meant you couldn't have a family and your life would be ruined." The Irish real estate market has gone bust. But looking in the window of a real estate agent, it appeared to your editor that the boom-time spirit had not been completely crushed. Prices — based on US equivalents — seemed reasonable. But reasonable is what you get in the middle, not what you get at the top or the bottom. At the top, the house might have sold for twice what it sells for today. At the bottom, it should sell for about half. In order to reach a real bottom, investors — and ordinary people, for that matter — need to repudiate the idea of the boom itself. That is, they have to come to believe that the premise that drove prices up is false. That is why it is so hard to be a real contrarian investor. It is one thing to recognize that prices go up and down. It is one thing to believe that you should buy when things are cheap and sell when they are expensive. But the person who can resist the logic of a major market trend is rare. The idea that Ireland's property was destined to rise was just such an idea. Was it not true that Ireland is a small island? Was it not true that its economy was growing — thanks to integration with the rest of Europe? Was it not true that Ireland had the most attractive business tax rates in all of Europe? Was it not true that people were moving to Ireland by the planeloads...and that they needed a place to live? Of course it was true. It was irrefutable. Until it wasn't true anymore. Regards, Bill Bonner,

|

| Hong Kong starts trading gold in renminbi Posted: 16 Oct 2011 01:04 PM PDT Hong Kong starts trading gold in renminbi Depositors in Hong Kong can now convert their idle renminbi deposits into gold. By Nick Ferguson | 17 October 2011 Hong Kong's Chinese Gold & Silver Exchange Society officially starts trading gold denominated in renminbi today, in a bid to attract the HK$600 billion of Chinese currency sitting on deposit in the city's banks. Haywood Cheung, president of the 101-year-old bullion exchange, said the so-called Renminbi Kilobar Gold contracts could boost trading volumes by up to 30%, or HK$40 billion a day, during the next six months. Growth has already been strong this year, with average daily electronic transactions reaching HK$136 billion after a full-year average of just HK$31 billion in 2010. "By attracting both local and international investors, the Renminbi Kilobar Gold is a significant step towards internationalising the renminbi," said Cheung. "It also consolidates Hong Kong's position as an offshore renminbi centre by providing investors with a new alternative in leveraged trading of renminbi." Investors who choose to convert their renminbi bank deposits into the new gold contracts can gear up their exposure to the currency by as much as 25 times. During a visit to the exchange on Friday, Cheung told FinanceAsia that this ability to use leverage will prove attractive to investors, who until now have lacked opportunities to put their renminbi to work. It also helps that gold and renminbi are both headline-grabbing investment trends. Cheung reckons they still offer value, arguing that gold is just half-way through a 10 to 15-year bull cycle and that renminbi will appreciate by 5% to 6% a year before it becomes freely convertible. That is an appealing proposition compared to moribund returns on bank deposits. Some critics have argued that the exchange will face tough competition from the Chinese mainland. Shanghai already hosts onshore trading of gold contracts and, according to sceptics, continued liberalisation of the domestic market will make it easier for Chinese investors to bypass Hong Kong. In response, Cheung noted that China is actively promoting Hong Kong as an offshore renminbi centre and the city enjoys a big advantage through its established role as a trusted international financial centre. Far from leaving the exchange, Chinese investors have increased their share of trading on the CGSE to 50% to 60%, up from around 30% at the start of the year. It is also possible that the Hong Kong and Shanghai bullion exchanges could cooperate in the future as the two societies have adopted the same standards with regards to purity. "When they open up, I think we can be very good associates," said Cheung. In the medium term, the exchange is even planning to launch an initial public offering of its shares to make it easier to secure international deals. "We have the vision, for sure," said Cheung. "An IPO will allow us to have more international partners. International institutions want to be able to have an exit from their investment when they come in, but right now I don't have that because the exchange is private." Trading of the Renminbi Kilobar Gold contracts will start with 25 of the exchange's member firms from various sectors, including banking and gold dealing, with Wing Hang Bank and Bank of China acting as settlement banks. The spot gold contracts are traded under the revamped electronic trading system established by the CGSE and quoted and settled in renminbi. Starting from today, members can take physical delivery of the gold upon settlement. http://www.financeasia.com/News/2769...-renminbi.aspx |

| MUST WATCH: Cheviot's Sound Money Conference Posted: 16 Oct 2011 12:30 PM PDT Cheviot's Sound Money Conference was held on Thursday January 27th 2011 at London's historic Guildhall and is a must watch for everyone.

Panel Discussion and Audience Q & A |

| Got Gold Report - Crisis Leads to Opportunity Posted: 16 Oct 2011 11:47 AM PDT HOUSTON (Got Gold Report) – Two weeks after making a marginally new lower low the S&P 500 Index is back up to the top of its crisis consolidation. Either the world crisis of confidence is not quite as bad as the doomsayers say it is or else the collective wisdom of countless thousands and millions of traders worldwide has it wrong. Incidentally, an important "tell" for this past market swoon, we believe, was a blatant non-confirmation of the new lower S&P lows turned in by the NASDAQ market. Instead of a lower low two weeks ago the "NAS" turned in a decidedly higher-low "answer." Note the higher turning low for the NAS in its consolidation and a now higher high. Over-confident shorts were taken out on stretchers on this move. The reversals can be blamed in part by a harshly flagging U.S. dollar, which careened lower and closed down more than 200 basis points for the trading week. Interestingly, and as a side note, the futures traders the CFTC classes as "commercial" had the movement in the U.S. dollar index (DXY) pegged if their futures positioning is any guide. As Vultures (Got Gold Report Subscribers) already knew, because they keep up with our technical charts on our GGR subscriber pages, the ICE exchange commercial traders were near-record net short the greenback index with more than 53,000 contracts of net short exposure this week as of Tuesday. That's 53,000 contracts of a just-under 70,000 contract open interest or about 76% of the open interest net short, representing a colossal bet that the flight into the buck as a "safe haven" was very, very overdone. So confident were the ICE commercial traders that the dollar was overbought, that even as the DXY FELL 201 basis points (a big move) Tuesday to Tuesday, from 79.59 to 77.58, the veteran currency traders ADDED yet another 3,662 contracts or 7.4% to their "net short-ness." They were amply rewarded for doing so too, as the DXY fell another 96-ticks by the Friday close, all the way back down to 76.62 (according to Stockcharts.com's data provider). Hey, wait a minute. Aren't we supposed to be in the midst of a bloody crisis? And in a worldwide sure-enough crisis isn't it conventional wisdom that the only "safe" place to be is in the under-backed, but still very liquid U.S. dollar? If capital is suddenly and very strongly exiting the greenback, if it is instead flowing back into the Euro, back into "stuff" and back into equities, does that mean that the crisis is over? More importantly for our own cause here at Got Gold Report, if the crisis is waning now, can we expect there to be a resurgence of confidence in the small, thinly traded, less liquid and more speculative junior miners and explorers we love to 'game' around here? The calendar "says" it's time for the juniors to get more attention. The recent news and deal-flow says that juniors are "hotting up," but is that translating into a bounce for the issues we affectionately call The Little Guys? The chart below is of the Canadian Venture Exchange Index or CDNX, a decent proxy for the smaller junior miners and explorers we track and trade. A bounce? In a word, yes, a little. We have definitely gone from super-buyer's strike to a bargain hunter's, insider's and deep-value trader's recoil. No question about it. Just look at that chart. But the smaller, less liquid and more speculative miners and explorers have been so mistreated, so battered and abused, so maligned by a fearful and worried-sick market (nearly cut in half since March as a group), they have a very long way to go up, just to get back to the surface of this turbulent market pond. Recall also, that the CDNX is and has been underperforming the Big Miner indexes since 2008, so the carnage shown is actually much, much worse than it looks as hard as that may be to believe. The Little Guys have an enormous amount of recovering to do as a group before the general public will have confidence in them again. By then, however … by the time the public has enough confidence to buy the heck out of the smaller issues (like they did in January of this year near the recent peak), it will likely be time to once again offload a basket of them (or at least a portion of them) to await the next crisis of opportunity – to await the next 50% to 70% off (or more) red-tag-sale for The Little Guys. Meanwhile, we are not yet certain that this crisis is done. Calendar and seasonal influences notwithstanding, we can never be certain of such things – in advance. What we can say, almost universally, is that The Little Guys are officially and undeniably "on sale." The long-term buyer's strike has wreaked market-wide slaughter on the share prices of so many of the smaller companies that the entire space seems like, walks like, and quacks like a bargain. Don't think for even a minute that the larger, better funded and more liquid companies, the mid-tiers and majors of the resource world, are not fully aware that the resource equity market is cheap right now. They do indeed know it and they are licking their chops at the prospects, we believe. The resource world is awash in "confidentiality agreements" and "non-disclosure" pacts between prospective marriage partners. We have already seen business combinations, mergers and buyouts of the friendly and hostile kind surface in recent weeks and months. Our bet is that the M & A activity we have already seen is nothing compared to what is about to get going. With $1,600-plus gold the gold producers are very cash-flow positive and that means they have the rare condition of having cash ammunition to grow their resource base from the already found and proven "stuff" held by the hard-working, but now beaten up juniors. The market is nothing if not efficient over time, and it is at times like these that we can observe how resources flow to the companies aggressively building their base for the future, and capital being distributed back into the junior market where it is needed most – for discovery of even more of the precious stuff the world needs and wants. The "rewards" to the talented and dedicated people who have risked much, personally and career-wise, to find the resources the world needs are coming. For many of them the end of the resource discovery trail will come too soon, well before the market assigns a higher (or a too-high-to-make-economic-sense) value, if history is any guide. But such is the nature of our chosen small-miner universe. We cannot know if we have reached and bounced from "The Bottom" or just "A Bottom," but we do know that the bounce signature shown in the CDNX graph above is exactly what we might look for when looking for an ultimate capitulation, selling exhaustion and reversal which is so typical of major turning points. The "V" signature on charts, a so-called "V-Bottom," if and only if confirmed with consolidation and eventual follow through, is one of the most reliable signals in charting. Confirmation of "V-bottoms" always comes swiftly (in a matter of weeks), or not at all, so at least we do not have a long wait to find out if this one is going to "stick it and run," or instead stick those who believe in it right in the left eye. On that "high note" let's pause here and move directly into the Got Gold Report. Got Gold Report First things first, the Got Gold Report – the full report – is published biweekly at least 24 times per year. Between reports we communicate more regularly on the GGR web log, which is always free and open to the public, or in our COT Flash reports and Vulture Bargain Hunter reports reserved exclusively for subscribers. COT Flash reports appear on off weeks for the Got Gold Report when there are what we consider important changes in the commitments of traders reports which cannot wait until the next full report. Vulture Bargain offerings appear ad hoc as there are developments we feel merit comment for and in the resource company issues we track closely. Our aim is to briefly summarize our positioning for the gold and silver markets, and also to highlight a few of the dozens of indicators, ratios and graphs we keep in constant touch with. Vultures, after logging in, please see the commentary in our numerous technical charts located in their own section of the password-protected subscriber pages. We update most of the Got Gold Report linked charts each week, sometimes even the weekends when we don't publish the full report. Changes to the linked charts are almost always completed by 6:00 pm ET on Sunday evening (except when Monday is a holiday) and occasionally during the week as events unfold. To continue reading, please log in or click here to subscribe to a Got Gold Report Membership. |

So if the chance to buy some silver on the cheap around $25-28 an ounce comes do seize the opportunity as CliveMaund.com suggests. But be weary of trying to trade volatility in such a capricious performer as silver where physical sales and spot-prices already point to an imminent price break out.

So if the chance to buy some silver on the cheap around $25-28 an ounce comes do seize the opportunity as CliveMaund.com suggests. But be weary of trying to trade volatility in such a capricious performer as silver where physical sales and spot-prices already point to an imminent price break out.

| You are subscribed to email updates from Gold World News Flash 2 To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment