Gold World News Flash |

- Courtesy Excerpt of the Got Gold Report for August 7

- Goldman Sachs: "QE3 Is Now Our Base Case"

- Goldman Sachs: "QE3 Is Now Our Base Case"

- All Hail The Gold Punisher

- Gold Seeker Closing Report: Gold Gains $30 before Fed Statement; Volatile Afterwards

- SGT Interviews BIX WEIR: The Main Battle Now is in the SILVER Market

- Peter Schiff: “You Can't Print Gold” – Credit Agencies Still Giving Central Bankers Too Much Credit

- JP Morgan Warns Gold to Go Parabolic and Rise to $2,500 By Year End

- U.S. Dollar Debt Crisis, Vested Interests Bad Mouth Gold

- Jim Rickards on Gold, S&P Downgrade

- Gold Resource Corporation Reports Record Second Quarter Results; Sets 2011 Precious Metal Gold Equivalent Production Target of 60,000 - 70,000 Ounce Range

- Can Precious Metals Save Your Portfolio?

- In The News Today

- “Gold is not a commodity it is a currency – and the devaluation of paper money by money printing is making it more and more attractive.”

- Marc Faber on Bloomberg TV: The Long-Term Treasury Market is a Bubble, Buy Gold

- Marc Faber: "The Best Thing The Fed Could Do For Markets Wold Be To Collectively Resign"

- Marc Faber: "The Best Thing The Fed Could Do For Markets Wold Be To Collectively Resign"

- S&P 500 Update – US Dollar Sacrificed

- Gold Price May Have Topped for this Leg Today, Silver has Further to Drop, but Will Probably Rise Tomorrow

- Faber On U.S. Downgrade: U.S. To Have "Some Kind of Default", But Market "Incredibly Oversold"

- Faber On U.S. Downgrade: U.S. To Have "Some Kind of Default", But Market "Incredibly Oversold"

- Marc Faber on Fed Decision, Treasury Market, Gold

- The Price Of A Big Mac Is Now $17.19 In Zurich

- Stephen Leeb - Silver to Hit $200 Within 24 Months

- When Buying Gold Becomes a Life-or-Death Question

- S&P 500 Update - US Dollar sacrificed

- Where Oh Where Are The Safe Havens From Yesteryear?

- We called it first. Five years ago at the height of the real estate bubble we predicted the collapse, the skyrocket in gold and silver, and the ensuing global riots per GIABO

- Is Recent Gold Hedging Activity a Warning?

- On Perpetual ZIRP

| Courtesy Excerpt of the Got Gold Report for August 7 Posted: 09 Aug 2011 06:36 PM PDT Past 4 weeks gold up 9.5% - COMEX Commercial net shorts up a whopping 42% - caution flags flying for both bulls and bears.

HOUSTON – Just below is a courtesy excerpt of the full Got Gold Report which was delivered to Vultures (Got Gold Report subscribers) Sunday, August 7, and posted to the password-protected GGR subscriber pages then.

Excerpt of the full Got Gold Report of August 7

Gold COT

The Commodity Futures Trading Commission (CFTC) issued its weekly commitments of traders (COT) report at 15:30 ET Friday, August 5. The report is for the close of trading as of Tuesday, August 2.

In a wild, very scary and unsettling week, gold overcame a lot to gain $40.23 or 2.5% for the COT reporting week, up from $1,619.00 to $1,659.23 Tues/Tues. Gold closed above $1,600 on all five trading days of the week, by the way, and seemed uncommonly well bid near $1,605 on Thursday (July 28), and near $1,610 Friday and Monday (Aug 1). In our own trader's notes we remarked that the action seemed like "a concrete floor at $1,600 or so." Perhaps we are about to get a sense of why that was so just below. At any rate on Tuesday, COT reporting day, gold was nothing but strong, up $40 on the day, and closing on its highs of the day in what was an obvious short covering rout. So the COT report we are about to view reflects a gold market on a short-covering rise Tuesday. The rumors of a CME margin rate increase did not surface and spread widely until Thursday of this week, by the way. As gold once again closed at the highest-ever price on a COT cutoff day at $1,659.23, the combined COMEX commercial traders did report a modest increase to their collective net short positioning (LCNS) of 4,661 contracts or 1.7% to 287,634 contracts net short. However, the COMEX open interest actually fell by 7,051 contracts to 529,403 contracts open. Clearly traders the CFTC classes as commercial have been selling heavily into this advance for gold. Just as clearly, we can now say with authority that, as of Tuesday's close, some of the commercial traders have been forced to cover some of those short positions. More about that in a moment, but first we note that we have reached the highest commercial net short position for gold futures since November 9, 2010, when the LCNS showed 290,953 contracts net short with gold then $1,392.94, then about to modestly correct. As of Tuesday the LCNS was within 20,597 contracts (6.7%) of the all time high commercial net short position in our records of 308,231 contracts in the September 9, 2009 report with gold then trading at $1,196.50 and about to correct sharply. Past 4 weeks gold up 9.5% - LCNS up a whopping 42%. Just below is the nominal LCNS graph for gold futures.

Rumors flew through the market this week of uncommonly strong demand for physical gold and those rumors were more or less confirmed by significant positive money flow in gold ETFs this week. The demand seems to be widespread, not just Asia or Europe, this time. The very high levels of commercial short covering mean we have reached the point where we should expect higher to maybe even extreme volatility just ahead. It is perhaps the most dangerous of setups for traders on both sides of the contest, bull or bear. No matter which side of the battle now, prudent speculators and very short-term traders need to set appropriate trading stops and mind them without fail. The market moving forces at play now are much more powerful than normal and thus the potential for overly large swings in price should be expected. We cannot be surprised by violent moves of 3% to 5% or more in a day in either direction under the circumstances. Neither should we rely too much on historical levels, including price, commercial positioning, or even relative commercial positioning when history-making events have the potential to overwhelm the mere trading history. We are living and trading in an environment no one alive has ever seen - again. Much depends on the hand of government and events that no one has even thought of yet, so our caution flags remain flying for now. That means caution to both sides. It means that we think short-term trading stops really must be at their highest, "at resistance" settings. But once again, "caution flags" is not synonymous with a sell signal. The reason we use trading stops instead of just guessing at tops is so that the trade can live on to enjoy the benefits of wild, out-of-character runaway price rises, should one occur, while protecting large gains if a bona fide breakdown occurs. A breakdown under these unstable circumstances has the potential to be major also.

Pardon the length of this section, please, but we want to be crystal clear and we also want to make clear our own intention to definitely take advantage of a market over-sell on gold just ahead, if any, but only once we are convinced the move lower has exhausted itself. Because we already hold a reasonable portion of our own resources in physical gold, we have the luxury of waiting patiently; very patiently for extreme opportunity should it occur in the days and weeks ahead. The dismal performance of mining shares this week, even with a general panic underway, suggests a harsh downward thrust is at the very least, possible (although intuition tells us to expect the opposite). So we wait patiently, like good Vultures, for an opportunistic reentry for our gold short-term trading ammo.

|

| Goldman Sachs: "QE3 Is Now Our Base Case" Posted: 09 Aug 2011 05:49 PM PDT While there is speculation whether today's historic announcement by the Fed in which it dated the beginning of the end of ZIRP, and in reality just the beginning of the beginning, is some form of shadow QE3, what is certain is that there is no Large Scale Asset Purchasing component to it yet. As such while the market immediately discounted the impact of 2 years of duration risk elimination (roughly 70 ES point equivalent), this has now been priced in, and the market must now look to mechanisms by which the it will have to absorb ~ $2.0 trillion in debt issuance over the next year without Fed help (and to those sticking to some modified version of MMT, keep in mind there is only $1.6 trillion in excess reserves so even a full recycling thereof would be insufficient to match demand of funds). Enter Goldman Sachs which puts the argument to bed: "We now see a greater-than-even chance that the FOMC will resume quantitative easing later this year or in early 2012." Why? Because what was lost in the noise today is that the US economy is contracting and the unemployment rate is rising: i.e., we are reentering a recession. And what the Fed did today is absolutely powerless to change this even from the Fed's point of view. Quote Hatzius: "This would probably mean more QE if their forecast converged to our own modal view of a flat-to-higher unemployment rate through the end of 2012, let alone our downside risk case of a renewed recession." But what about the historic dissent? Ah, therein lies the rub: "We view Chairman Bernanke's willingness to live with the dissents as a strong signal that he and the rest of the Fed leadership view the need for renewed easing as more important than the institutional norm of consensus decisionmaking." So there you go. The market will wake up tomorrow with a hangover, and say the one word it always does: "More." Absent that, the slide will, as predicted, resume, and it is none other than Goldman Sachs who has once again, just like back in 2010, set the strawman up for the Fed doing simply more of the same which does nothing to actually fix the economy, but bring us all closer to that epic meltdown discussed by Andy Lees earlier, and by Zero Hedge over the past two and a half years. From Jan Hatzius: QE3 Now Our Base Case Summary We now see a greater-than-even chance that the FOMC will resume quantitative easing later this year or in early 2012. We have changed our call because today's statement suggests that the committee's reaction function to incoming economic news is more dovish than we had previously thought. Although Fed officials still expect a gradual decline in the unemployment rate, they made a conditional commitment to keep the funds rate unchanged "at least through mid-2013" and implied that they would employ additional policy tools in case their economic forecast deteriorated further. This would probably mean more QE if their forecast converged to our own modal view of a flat-to-higher unemployment rate through the end of 2012, let alone our downside risk case of a renewed recession. Full note: It's official: the federal funds rate is highly likely to stay at its current near-0% level until 2013 (or later). Although this has been our forecast all along, today's FOMC statement was nevertheless more dovish than we had anticipated in two respects: 1. The policy commitment to keep the funds rate at "…exceptionally low levels…at least through mid-2013" was more aggressive than we had anticipated. Some commentators today expressed disappointment that this is still a conditional commitment, i.e., Fed officials kept an "out" if growth is much stronger and/or inflation much higher than expected. But that was not a surprise. The surprise was the fact that there is a date at all (for the first time ever in the history of Fed communications) and even more so the fact that the date is almost two years in the future. 2. The easing bias in the last paragraph of the statement was more explicit than we had anticipated: "The Committee discussed the range of policy tools available to promote a stronger economic recovery in a context of price stability. It will continue to assess the economic outlook in light of incoming information and is prepared to employ these tools as appropriate." The phrasing somewhat echoed the promise in the September 2010 statement "…to provide additional accommodation if needed…", which sealed the deal for QE2. In our view, the committee's explicit easing bias suggests that the threshold for additional easing in terms of downward revisions to the committee's forecast is relatively low. The implication is that the committee would probably ease policy further if its economic forecast converged to our own, more downbeat view. While the committee still expects a gradual decline in the unemployment rate, our own modal forecast is a flat-to-higher rate through the end of 2012. In addition, we see a recession risk of about one in three, and if there was indeed a recession the committee would of course ease further. If there is additional easing, it would likely take the form of QE. After all, "these tools" mentioned in the statement presumably need to be more powerful--or at least not much less powerful--than the action taken today in order to avoid a sense of anti-climax. This means that they are unlikely to consist of small incremental steps such as a commitment to keep the balance sheet large, a gradual shift of the securities portfolio into longer maturities, or a cut in the interest rate on excess reserves from 25 basis points (bp) to zero. This leaves the stronger options, which include QE as well as even more aggressive forms of easing such as rate caps (a form of QE in which the Fed promises to buy as many securities as needed to hit a longer-term yield target), a price level or nominal GDP target, or interventions in non-government securities markets (for which funding from Congress would be needed). Of these, "conventional" QE is very likely the option with the lowest hurdle, and the first one to be deployed. Although QE3 is now our base case, it is not a certainty. We see three main ways in which our revised call could turn out to be incorrect. First, of course, the economy may turn out to be stronger than our forecast. In this case, Fed officials would not need to revise down their forecast, and would probably not ease further. Second, inflation might pose a higher hurdle to additional easing than we have allowed. There are only tentative signs of deceleration in core inflation, and inflation expectations show few signs of breaking lower despite the recent weakness in the economic data and risk asset prices. This is a risk to our view, although the stickiness of inflation expectations might already reflect an assumption by the market that the Fed will ease, in which case inflation expectations would fall sharply if the Fed failed to deliver. Third, the anti-Fed backlash late last year might argue against further QE. That is possible, but the problem might be reduced via a slight tweak in the policy's design. That is, Fed officials might choose to specify the policy not as a large-and-scary upfront number but a smaller monthly flow of purchases. Although the substantive differences are small--e.g. a $600bn purchase over eight months is basically the same as a $75bn-per-month purchase that is expected to last eight months--the cosmetics of the flow approach might be more appealing. Moreover, it would also be more flexible because the committee would revisit the program from meeting to meeting. While these points could pose problems for our call, we disagree strongly with one argument against further QE that we heard frequently today--namely that the three dissents from Presidents Fisher, Kocherlakota, and Plosser indicate "the end of the line" for further Fed easing and difficulty for the chairman to get his way. On the contrary, we view Chairman Bernanke's willingness to live with the dissents as a strong signal that he and the rest of the Fed leadership view the need for renewed easing as more important than the institutional norm of consensus decisionmaking. There is no question that Bernanke will always have enough votes, and we fully expect him to use these votes to provide further support to the economy if he views it as necessary.

|

| Goldman Sachs: "QE3 Is Now Our Base Case" Posted: 09 Aug 2011 05:49 PM PDT

While there is speculation whether today's historic announcement by the Fed in which it dated the beginning of the end of ZIRP, and in reality just the beginning of the beginning, is some form of shadow QE3, what is certain is that there is no Large Scale Asset Purchasing component to it yet. As such while the market immediately discounted the impact of 2 years of duration risk elimination (roughly 70 ES point equivalent), this has now been priced in, and the market must now look to mechanisms by which the it will have to absorb ~ $2.0 trillion in debt issuance over the next year without Fed help (and to those sticking to some modified version of MMT, keep in mind there is only $1.6 trillion in excess reserves so even a full recycling thereof would be insufficient to match demand of funds). Enter Goldman Sachs which puts the argument to bed: "We now see a greater-than-even chance that the FOMC will resume quantitative easing later this year or in early 2012." Why? Because what was lost in the noise today is that the US economy is contracting and the unemployment rate is rising: i.e., we are reentering a recession. And what the Fed did today is absolutely powerless to change this even from the Fed's point of view. Quote Hatzius: "This would probably mean more QE if their forecast converged to our own modal view of a flat-to-higher unemployment rate through the end of 2012, let alone our downside risk case of a renewed recession." But what about the historic dissent? Ah, therein lies the rub: "We view Chairman Bernanke's willingness to live with the dissents as a strong signal that he and the rest of the Fed leadership view the need for renewed easing as more important than the institutional norm of consensus decisionmaking." So there you go. The market will wake up tomorrow with a hangover, and say the one word it always does: "More." Absent that, the slide will, as predicted, resume, and it is none other than Goldman Sachs who has once again, just like back in 2010, set the strawman up for the Fed doing simply more of the same which does nothing to actually fix the economy, but bring us all closer to that epic meltdown discussed by Andy Lees earlier, and by Zero Hedge over the past two and a half years. From Jan Hatzius: QE3 Now Our Base Case Summary We now see a greater-than-even chance that the FOMC will resume quantitative easing later this year or in early 2012. We have changed our call because today's statement suggests that the committee's reaction function to incoming economic news is more dovish than we had previously thought. Although Fed officials still expect a gradual decline in the unemployment rate, they made a conditional commitment to keep the funds rate unchanged "at least through mid-2013" and implied that they would employ additional policy tools in case their economic forecast deteriorated further. This would probably mean more QE if their forecast converged to our own modal view of a flat-to-higher unemployment rate through the end of 2012, let alone our downside risk case of a renewed recession. Full note: It's official: the federal funds rate is highly likely to stay at its current near-0% level until 2013 (or later). Although this has been our forecast all along, today's FOMC statement was nevertheless more dovish than we had anticipated in two respects: 1. The policy commitment to keep the funds rate at "…exceptionally low levels…at least through mid-2013" was more aggressive than we had anticipated. Some commentators today expressed disappointment that this is still a conditional commitment, i.e., Fed officials kept an "out" if growth is much stronger and/or inflation much higher than expected. But that was not a surprise. The surprise was the fact that there is a date at all (for the first time ever in the history of Fed communications) and even more so the fact that the date is almost two years in the future. 2. The easing bias in the last paragraph of the statement was more explicit than we had anticipated: "The Committee discussed the range of policy tools available to promote a stronger economic recovery in a context of price stability. It will continue to assess the economic outlook in light of incoming information and is prepared to employ these tools as appropriate." The phrasing somewhat echoed the promise in the September 2010 statement "…to provide additional accommodation if needed…", which sealed the deal for QE2. In our view, the committee's explicit easing bias suggests that the threshold for additional easing in terms of downward revisions to the committee's forecast is relatively low. The implication is that the committee would probably ease policy further if its economic forecast converged to our own, more downbeat view. While the committee still expects a gradual decline in the unemployment rate, our own modal forecast is a flat-to-higher rate through the end of 2012. In addition, we see a recession risk of about one in three, and if there was indeed a recession the committee would of course ease further. If there is additional easing, it would likely take the form of QE. After all, "these tools" mentioned in the statement presumably need to be more powerful--or at least not much less powerful--than the action taken today in order to avoid a sense of anti-climax. This means that they are unlikely to consist of small incremental steps such as a commitment to keep the balance sheet large, a gradual shift of the securities portfolio into longer maturities, or a cut in the interest rate on excess reserves from 25 basis points (bp) to zero. This leaves the stronger options, which include QE as well as even more aggressive forms of easing such as rate caps (a form of QE in which the Fed promises to buy as many securities as needed to hit a longer-term yield target), a price level or nominal GDP target, or interventions in non-government securities markets (for which funding from Congress would be needed). Of these, "conventional" QE is very likely the option with the lowest hurdle, and the first one to be deployed. Although QE3 is now our base case, it is not a certainty. We see three main ways in which our revised call could turn out to be incorrect. First, of course, the economy may turn out to be stronger than our forecast. In this case, Fed officials would not need to revise down their forecast, and would probably not ease further. Second, inflation might pose a higher hurdle to additional easing than we have allowed. There are only tentative signs of deceleration in core inflation, and inflation expectations show few signs of breaking lower despite the recent weakness in the economic data and risk asset prices. This is a risk to our view, although the stickiness of inflation expectations might already reflect an assumption by the market that the Fed will ease, in which case inflation expectations would fall sharply if the Fed failed to deliver. Third, the anti-Fed backlash late last year might argue against further QE. That is possible, but the problem might be reduced via a slight tweak in the policy's design. That is, Fed officials might choose to specify the policy not as a large-and-scary upfront number but a smaller monthly flow of purchases. Although the substantive differences are small--e.g. a $600bn purchase over eight months is basically the same as a $75bn-per-month purchase that is expected to last eight months--the cosmetics of the flow approach might be more appealing. Moreover, it would also be more flexible because the committee would revisit the program from meeting to meeting. While these points could pose problems for our call, we disagree strongly with one argument against further QE that we heard frequently today--namely that the three dissents from Presidents Fisher, Kocherlakota, and Plosser indicate "the end of the line" for further Fed easing and difficulty for the chairman to get his way. On the contrary, we view Chairman Bernanke's willingness to live with the dissents as a strong signal that he and the rest of the Fed leadership view the need for renewed easing as more important than the institutional norm of consensus decisionmaking. There is no question that Bernanke will always have enough votes, and we fully expect him to use these votes to provide further support to the economy if he views it as necessary.

|

| Posted: 09 Aug 2011 05:27 PM PDT Graceland Update

|

| Gold Seeker Closing Report: Gold Gains $30 before Fed Statement; Volatile Afterwards Posted: 09 Aug 2011 04:30 PM PDT Gold climbed as much as $69.09 to a new all-time high of $1779.39 at about 5:20AM EST before it fell back to as low as $1719.25 by late morning in New York, but it then rallied back higher in the last two and a half hours of trade and ended with a gain of 1.73%. Silver fell to as low as $37.508 before it also bounced back higher in late trade, but it still ended with a loss of 3.81%.

|

| SGT Interviews BIX WEIR: The Main Battle Now is in the SILVER Market Posted: 09 Aug 2011 04:18 PM PDT |

| Posted: 09 Aug 2011 04:12 PM PDT |

| JP Morgan Warns Gold to Go Parabolic and Rise to $2,500 By Year End Posted: 09 Aug 2011 03:09 PM PDT from GoldCode.com: Gold in USD terms is 2.4% higher and is higher against all currencies and trading at USD 1,760.40 , EUR 1,234.10, GBP 1,075.70, CHF 1,306.80 per ounce and 132,719.00 JPY. Gold’s London AM fix was USD 1,770.00, EUR 1,241.75, GBP 1,080.98. Gold reached new record nominal highs at $1,780.10/oz and new nominal highs in euros and sterling also this morning.

Asian equities were mixed with sharp falls seen on the Hang Seng but the Nikkei recovered to only finish down 1.7% and the Chinese and Australian stock markets actually managed to rise on the day. The FTSE, DAX and CAC are down 0.7%, 1.9% and 0.2% respectively but US futures are showing tentative gains. There were further signs of stagflation in the UK as manufacturing unexpectedly fell in June and the trade gap widened. This is further evidence that the economic recovery is faltering in the UK and QE has not worked.

U.S. Treasuries dropped, pushing 10-year note yields up from the lowest level since January 2009, on speculation the Federal Reserve may introduce new stimulus measures today to boost financial confidence. More ‘stimulus’, QE3 or whatever new fangled acronym is dreamed up by desperate policymakers will of course be bullish for gold and silver.

J.P. Morgan Chase & Co. (JPM) and Goldman Sachs Group (GS), raised their gold-price late yesterday. J.P. Morgan now sees gold prices at $2,500 a troy ounce by year-end, while Goldman expects gold at $1,730 in six months and $1,900 in 12 months. This may be a sign that the current sharp rally may have reached its zenith as neither bank has a great track record regarding short term trading calls on commodity markets. In the short term there is the risk of a correction as gold’s rise is now becoming front page (on front page of FT today) and headline news. The fact that silver has fallen in recent days and remains below $40/oz and the fact that gold mining equities have also not risen may also be a warning signal. Gold has risen from below $1,500/oz to nearly $1,800/oz in 5 weeks (since the start of July) and is up nearly 18% in dollar terms. Therefore, in conventional terms gold is most certainly overbought. However, we are not living in conventional or normal times and the ongoing global market crash and global currency debasement means that there is a chance that gold will go parabolic as it did in the 1970’s. Investors would be prudent to continue to make the trend their friend and any pullback should be used to buy the dip. Those wishing to take profits might do so after two days of lower prices or a weekly lower close. However, given the level or market, systemic and monetary risk, all investors are advised to maintain a core financial insurance precious metals holding. Gold’s bull market looks very secure for the foreseeable future due to strong institutional demand (from astute hedge funds and central banks) and store of wealth demand from Asia. As does silver’s due to increasing investment and safe haven demand and the continuing growth in industrial demand for the versatile precious metal. Click Here for the original source. http://www.goldcore.com/goldcore_blog/jp-morgan-warns-gold-go-parabolic-and-rise-2500-year

|

| U.S. Dollar Debt Crisis, Vested Interests Bad Mouth Gold Posted: 09 Aug 2011 03:02 PM PDT by James Quinn, Market Oracle: "Believe me, the next step is a currency crisis because there will be a rejection of the dollar, the rejection of the dollar is a big, big event, and then your personal liberties are going to be severely threatened." - Ron Paul

As usual the MSM did its usual superficial dog and pony show for the American public on Saturday and Sunday. The overall tone on every show (not journalism) was to calm the audience. Every station had a "downgrade special" to explain why you shouldn't panic over the downgrade of the United States. As we can see, it didn't work. Worldwide markets went berserk. The reactions of the various players in this saga have been very enlightening to say the least.

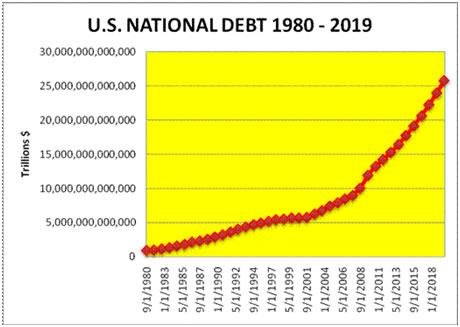

As I watched, listened and read the views of hundreds of people over the last few days, I recalled a statement by David Walker in the documentary I.O.U.S.A. This documentary was made in late 2007 before the financial crisis hit. The documentary follows Walker, the former head of the GAO, and Bob Bixby, head of the Concord Coalition, on their Fiscal Wake Up tour. In the film, Walker tells the audience: “We suffer from a fiscal cancer. If we don’t treat it there will be catastrophic consequences.” He argued the greatest threat to America was not a terrorist squatting in a cave in Afghanistan, but the US debt mountain. He was nervous about the increasing dependence on countries such as China, which are the biggest holders of US Treasury bonds. Bixby explained: “If you knew a levee was unsound and people were moving into that area, would you do nothing? Of course not.” These men were sounding the alarm when our National Debt was $9 trillion. Evidently, no one in Washington DC went to see the movie. They've added $5.5 trillion of debt to our Mount Everest of obligations. After listening to the shills, shysters, propagandists, and paid representatives of the vested interests over the last few days, Mr. Walker's response to someone pointing out Europe and other countries were in worse shape than the U.S. came to mind: “What good does it do to be the best-looking horse in the glue factory?” At the end of the documentary there was a prestigious panel of thought leaders discussing ideas to alter the country from its unsustainable fiscal path. I was shocked when Warren Buffett basically stated there was nothing to worry about: “I’m going to be the token Pollyanna here. There is no question that our children will live better than we did. But it’s just like my investments. I try to buy shares in companies that are so wonderful, an idiot could run them, and sooner or later one will. Our country is a bit like that.” Buffett has since turned into a Wall Street/Washington apologist, talking his book. He declared this weekend the US deserves a quadruple A rating. He has tried to protect his investments in GE, Goldman Sachs, Moodys and Wells Fargo by declaring their businesses as sound and their balance sheets clean. He is now just a standard issue sellout spewing whatever will protect his vast fortune. Truth is now optional in Buffett World.

The Oracle of Omaha has continuously bad mouthed gold and pumped up the economic prospects for the U.S. He trashed gold in his March 2011 report to shareholders: “Gold is a way of going long on fear, and it has been a pretty good way of going long on fear from time to time. But you really have to hope people become more afraid in a year or two years than they are now. And if they become more afraid you make money, if they become less afraid you lose money, but the gold itself doesn’t produce anything.” I guess the leadership of this country has created a bit of fear in the market, as gold has risen from $1,400 to $1,750 and Warren's beloved financial holdings have tanked, along with the stock price of Berkshire Hathaway (down 23% since March). There seems to be an inverse relationship between the barbarous relic and lying old men shilling for the vested interests. Vested Interests When you watch the corporate mainstream media, or read a corporate run newspaper, or go to a corporate owned internet site you are going to get a view that is skewed to the perspective of the corporate owners. What all Americans must understand is everyone they see on TV or read in the mainstream press are part of the status quo. These people have all gotten rich under the current social and economic structure. Buffett, Kudlow, Cramer, Bartiromo, Senators, investment managers, Bill Gross, Lloyd Blankfein, Jamie Dimon, Jeff Immelt, and every person paraded on TV have a vested interest in propping up the existing structure. They are talking their book and their own best interests. Even though history has proven time and again the existing social order gets swept away like debris in a tsunami wave, the vested interests try to cling to their power, influence and wealth. Those benefitting from the existing economic structure will lie, obfuscate, misdirect, and use propaganda and misinformation to retain their positions. The establishment will seek to blame others, fear monger and avoid responsibility for their actions. Ron Paul plainly explains why the US was downgraded: "We were downgraded because of years of reckless spending, not because concerned Americans demanded we get our finances in order. The Washington establishment has spent us into near default and now a downgrade, and here they are again trying to escape responsibility for their negligence in handling the economy." The standard talking points you have heard or will hear from the vested interests include:

Each of these storylines is being used on a daily basis by the vested interests as they try to pull the wool over the eyes of average Americans. A smattering of truth is interspersed with lies to convince the non-thinking public their existing delusional beliefs are still valid. The storylines are false. Here are some basic truths the vested interests don't want you to understand:

"As many frustrated Americans who have joined the Tea Party realize, we cannot stand against big government at home while supporting it abroad. We cannot talk about fiscal responsibility while spending trillions on occupying and bullying the rest of the world. We cannot talk about the budget deficit and spiraling domestic spending without looking at the costs of maintaining an American empire of more than 700 military bases in more than 120 foreign countries. We cannot pat ourselves on the back for cutting a few thousand dollars from a nature preserve or an inner-city swimming pool at home while turning a blind eye to a Pentagon budget that nearly equals those of the rest of the world combined."

“Wall Street bond trading desks, staffed by people making seven figures a year, set out to coax from the brain-dead guys making high five figures the highest possible ratings for the worst possible loans. They performed the task with Ivy League thoroughness and efficiency.”

And now we come to the $100 trillion question. The establishment/vested interests/status quo declares the United States as the safest place in the world for investors. They frantically point out that people are pouring money into our Treasuries and interest rates are declining. They hysterically blurt out that Europe has much bigger problems than the U.S. and China's real estate bubble will implode in the near future. These are the same people who told you the internet had created a new paradigm and NASDAQ PE ratios of 150 in 2000 were reasonable. The NASDAQ soared to 5,000 in early 2000. Today it trades at 2,358, down 53% eleven years later. These are the same people who told you they aren't making more land and home prices in 2005 were reasonable. They told you home prices had never fallen nationally in our history, so don't worry. Prices are down 35% and still falling today. Medicare and Medicaid spending rose 10% in the second quarter of 2011 from a year earlier to a combined annual rate of almost $992 billion, according to the Bureau of Economic Analysis (BEA). The two programs are likely to crack $1 trillion before the end of the year. Medicare’s unfunded liability alone amounts to $353,350 per U.S. household. The National Debt will reach 100% of GDP in the next four months as we relentlessly add $4 billion per day to our Mount Everest of debt. Federal spending in 2007 was $2.7 trillion. Today, they are spending $3.8 trillion of your money. The country does not have a revenue problem. We have a spending addiction and the addict needs treatment. Doctor Ron Paul has our prognosis: "When the federal government spends more each year than it collects in tax revenues, it has three choices: It can raise taxes, print money, or borrow money. While these actions may benefit politicians, all three options are bad for average Americans." The politicians and bankers who control the developed world have made the choice to print money and create more debt as their solution to an un-payable debt problem. Europe, Japan, the U.S., and virtually every country in the world want to devalue their way out of a debt problem created over the last forty years. It has become a race to the bottom, with no winners. Every country can't devalue their currency simultaneously without blowing up the entire worldwide monetary system. But, it appears they are going to try. The United States will never actually default on its debts |

| Jim Rickards on Gold, S&P Downgrade Posted: 09 Aug 2011 02:02 PM PDT

|

| Posted: 09 Aug 2011 12:47 PM PDT Gold Resource Corporation (GORO) (NYSE Amex: GORO) today announced a profitable and record second quarter ending June 30, 2011, despite the anomalous storm event that negatively impacted April and May production. Gold Resource Corporation is a low-cost gold producer with operations in the southern state of Oaxaca, Mexico. The Company has returned over $22 million to shareholders in special monthly dividends since declaring commercial production July 1, 2010.

|

| Can Precious Metals Save Your Portfolio? Posted: 09 Aug 2011 11:44 AM PDT by Chris Horlacher, MapleLeafMetals.ca:

Read More @ MapleLeafMetals.ca

|

| Posted: 09 Aug 2011 11:42 AM PDT My Dear Friends, You can see the importance of the $1764 Angel today. Regards, Jim Jim Sinclair's Commentary The Fed has thrown the dollar into the wind. Jim Sinclair's Commentary This is as important in the grand scheme as the downgrade of US treasuries. S&P Cuts AAA Ratings on Thousands of Continue reading In The News Today

|

| Posted: 09 Aug 2011 11:30 AM PDT The bull case for gold

|

| Marc Faber on Bloomberg TV: The Long-Term Treasury Market is a Bubble, Buy Gold Posted: 09 Aug 2011 11:21 AM PDT Speaking on the phone from Thailand, Faber said that the markets are very oversold, the Fed is 'underestimating the severity of the economic downturn' and that gold is the best investment right now. Read More...

|

| Marc Faber: "The Best Thing The Fed Could Do For Markets Wold Be To Collectively Resign" Posted: 09 Aug 2011 11:16 AM PDT In a Bloomberg TV interview following today's quixotic "QE3/non-QE3 announcement, which is Operation Twist 2, but not LSAP, and ushers in economic recession, even as it sends risk assets soaring, and somehow pushes the 2 Year a whopping 20 bps tighter so buy,buy, buy" and is really very much ado about nothing, the always outspoken Marc Faber had some very choice words about life, the universe and especially the residents of the Marriner Eccles building. While there still appears to be some confusions as to whether today's Fed decision to peg rates at zero for 2 years is QE3 or not, Faber believes that the decision to not enact more Large Scale Asset Purchases is "the right thing" although when it comes to the market, it "is more likely to move still lower. We are very oversold. We can have a rebound like we did today, maybe we'll have a rebound next week or so, but in general I think we will test the July lows of last year, the S&P at 1,010. After that, probably we'll get probably a QE3 announcement." On why Bernanke did not announce yet another asset purchasing round: "Essentially they spent their bullets. It is very difficult to follow through with QE3 right here, because you have gold prices going ballistic, and you have the dollar being very weak, and so there are unintended consequences with implementing QE3 right here." That said, the surge in markets apparently completely ignores that QE1 and 2 did nothing for the economy, although the goosing of the RUT should suffice. What is unclear is who will end up buying the $2.4 trillion in bonds coming down the tube. Faber also had some choice words about Treasurys: "I personally think the Treasury market, the long-dated, are a bubble and it will be one of the worst investments for the longer term if you buy a 10-year, a 30-year U.S. Treasury so I'm a bit puzzled that Treasuries are now yielding, are essentially near record lows." Naturally, Faber does not think gold is in a bubble, and as to what one can do with gold, his response is that "you give your girlfriend copper rings and I give them gold rings and I keep them longer." Indeed, no bubble there. As to how one should trade stocks, he says: "I think right now the technical picture is so horrible that I would use a rebound as a lightning up opportunity. I think [equities] will move lower... maybe after three months people will wake up and scratch their heads and say now, we know why it started to go down, because maybe there is geo political problems, maybe the Middle East blows up, maybe the economy is horrible." Last but not least is his suggestion what the Fed should do: "The best [the Fed] could do for markets would be to collectively resign." Precisely, which is why it will never happen. Full clip: And full transcript: Faber on whether he thinks the Fed did the right thing by keeping rates low: "I think they did the right thing that they didn't allow QE3. They can watch the reaction of assets, whether they will go lower. I think the market is more likely to move still lower. We are very oversold. We can have a rebound like we did today, maybe we'll have a rebound next week or so, but in general I think we will test the July lows of last year, the S&P at 1,010. After that, probably we'll get probably a QE3 announcement." On why he thinks the Fed is waiting on QE3: "I think the Fed is underestimating the severity of the coming economic downturn. Essentially they spent their bullets. It is very difficult to follow through with QE3 right here, because you have gold prices going ballistic, and you have the dollar being very weak, and so there are unintended consequences with implementing QE3 right here." On what Faber thinks the Fed should do: "The best [the Fed] could do for markets would be to collectively resign…I think sometimes the best is to do nothing. I welcome the decision, at least today, that they aren't doing anything worse than what they have already done." On whether it makes sense to provide any kind of stimulus: "What has QE1 and QE2 done for the labor markets? Nothing at all. It's done nothing for the housing markets. It's lifted stocks and it created wider wealth inequality in a sense that people who own assets have done very well, and people that are the lower-income recipients groups, they are hurt by rising energy prices and food prices." On what should be done for the U.S. economy: "From 1981 to 2007, we have an economy that was living beyond its means. As a result of continued debt accumulation, GDP was higher than would otherwise have been the case. Now we have a period of sub-par growth that can last for quite some time now, and like in the case of Japan after 1989, people instead of being encouraged to spend, they should be encouraged to save more, and the U.S. should save more and spend less. And then capital spending will essentially pick up." On the manic behavior in markets: "I personally think the Treasury market, the long-dated, are a bubble and it will be one of the worst investments for the longer term if you buy a 10-year, a 30-year U.S. Treasury so I'm a bit puzzled that Treasuries are now yielding, are essentially near record lows. I would rather sell Treasuries." "The stock market peaked out on the 2nd of May on the S&P at 1370. So we're now around 1010. For many stocks we're down 20% or so. We're very oversold. I think a rebound is coming but you can forget about a new high. That is out of the question. Because the technical picture is horrible, horrible. " On why investors are continuing to move to Treasuries: "I've been in this business for 40 years and on many occasions, nothing made sense to me….I think the Treasury market is another example of a gigantic bubble. The problem with the Federal Reserve policy of essentially zero interest rates is that they are essentially throwing money at the system, but they don't control where the money will flow to. It can flow at some point into commodity-related stocks. It can flow into gold, oil, treasuries, but it doesn't flow evenly into these assets. In my opinion, the Treasury, the long-dated Treasuries are essentially the short of the century thing here." On whether gold is a bubble: "I don't think it is a bubble, but I think the gold market has exploded to the upside recently and the correction is overdue. But as I have always maintained for the last 12 years, every responsible adult should gradually accumulate gold, because not owning any gold is the trouble with government. I don't understand. People of Bloomberg, I hardly know anyone who owns any gold physically. All of the Bloomberg employees are intelligent people. They listen to the news every day. They make the news every day. Hardly anyone owns any gold." On what you can do with gold: "I disagree [that you can't do anything with gold.] You give your girlfriend copper rings and I give them gold rings and I keep them longer." On how Faber would play the markets right now: "I think right now the technical picture is so horrible that I would use a rebound as a lightning up opportunity. I think [equities] will move lower. I mean, some say you should move back into emerging economies because the fundamentals of emerging economies are far better than the fundamentals of European countries and the fundamentals of the United States. This is something I will consider." "The only thing I have to say, basically the market has sold off in such a rapid way and with so much momentum that I am smelling as if something really wrong happens in the next two or three months, because the market is a discounting mechanism. Like March 2009 the market started to go up and people were baffled why it started to go up. Now it starts to go down, and maybe after three months people will wake up and scratch their heads and say now, we know why it started to go down, because maybe there is geo political problems, maybe the Middle East blows up, maybe the economy is horrible."

|

| Marc Faber: "The Best Thing The Fed Could Do For Markets Wold Be To Collectively Resign" Posted: 09 Aug 2011 11:16 AM PDT

In a Bloomberg TV interview following today's quixotic "QE3/non-QE3 announcement, which is Operation Twist 2, but not LSAP, and ushers in economic recession, even as it sends risk assets soaring, and somehow pushes the 2 Year a whopping 20 bps tighter so buy,buy, buy" and is really very much ado about nothing, the always outspoken Marc Faber had some very choice words about life, the universe and especially the residents of the Marriner Eccles building. While there still appears to be some confusions as to whether today's Fed decision to peg rates at zero for 2 years is QE3 or not, Faber believes that the decision to not enact more Large Scale Asset Purchases is "the right thing" although when it comes to the market, it "is more likely to move still lower. We are very oversold. We can have a rebound like we did today, maybe we'll have a rebound next week or so, but in general I think we will test the July lows of last year, the S&P at 1,010. After that, probably we'll get probably a QE3 announcement." On why Bernanke did not announce yet another asset purchasing round: "Essentially they spent their bullets. It is very difficult to follow through with QE3 right here, because you have gold prices going ballistic, and you have the dollar being very weak, and so there are unintended consequences with implementing QE3 right here." That said, the surge in markets apparently completely ignores that QE1 and 2 did nothing for the economy, although the goosing of the RUT should suffice. What is unclear is who will end up buying the $2.4 trillion in bonds coming down the tube. Faber also had some choice words about Treasurys: "I personally think the Treasury market, the long-dated, are a bubble and it will be one of the worst investments for the longer term if you buy a 10-year, a 30-year U.S. Treasury so I'm a bit puzzled that Treasuries are now yielding, are essentially near record lows." Naturally, Faber does not think gold is in a bubble, and as to what one can do with gold, his response is that "you give your girlfriend copper rings and I give them gold rings and I keep them longer." Indeed, no bubble there. As to how one should trade stocks, he says: "I think right now the technical picture is so horrible that I would use a rebound as a lightning up opportunity. I think [equities] will move lower... maybe after three months people will wake up and scratch their heads and say now, we know why it started to go down, because maybe there is geo political problems, maybe the Middle East blows up, maybe the economy is horrible." Last but not least is his suggestion what the Fed should do: "The best [the Fed] could do for markets would be to collectively resign." Precisely, which is why it will never happen. Full clip: And full transcript: Faber on whether he thinks the Fed did the right thing by keeping rates low: "I think they did the right thing that they didn't allow QE3. They can watch the reaction of assets, whether they will go lower. I think the market is more likely to move still lower. We are very oversold. We can have a rebound like we did today, maybe we'll have a rebound next week or so, but in general I think we will test the July lows of last year, the S&P at 1,010. After that, probably we'll get probably a QE3 announcement." On why he thinks the Fed is waiting on QE3: "I think the Fed is underestimating the severity of the coming economic downturn. Essentially they spent their bullets. It is very difficult to follow through with QE3 right here, because you have gold prices going ballistic, and you have the dollar being very weak, and so there are unintended consequences with implementing QE3 right here." On what Faber thinks the Fed should do: "The best [the Fed] could do for markets would be to collectively resign…I think sometimes the best is to do nothing. I welcome the decision, at least today, that they aren't doing anything worse than what they have already done." On whether it makes sense to provide any kind of stimulus: "What has QE1 and QE2 done for the labor markets? Nothing at all. It's done nothing for the housing markets. It's lifted stocks and it created wider wealth inequality in a sense that people who own assets have done very well, and people that are the lower-income recipients groups, they are hurt by rising energy prices and food prices." On what should be done for the U.S. economy: "From 1981 to 2007, we have an economy that was living beyond its means. As a result of continued debt accumulation, GDP was higher than would otherwise have been the case. Now we have a period of sub-par growth that can last for quite some time now, and like in the case of Japan after 1989, people instead of being encouraged to spend, they should be encouraged to save more, and the U.S. should save more and spend less. And then capital spending will essentially pick up." On the manic behavior in markets: "I personally think the Treasury market, the long-dated, are a bubble and it will be one of the worst investments for the longer term if you buy a 10-year, a 30-year U.S. Treasury so I'm a bit puzzled that Treasuries are now yielding, are essentially near record lows. I would rather sell Treasuries." "The stock market peaked out on the 2nd of May on the S&P at 1370. So we're now around 1010. For many stocks we're down 20% or so. We're very oversold. I think a rebound is coming but you can forget about a new high. That is out of the question. Because the technical picture is horrible, horrible. " On why investors are continuing to move to Treasuries: "I've been in this business for 40 years and on many occasions, nothing made sense to me….I think the Treasury market is another example of a gigantic bubble. The problem with the Federal Reserve policy of essentially zero interest rates is that they are essentially throwing money at the system, but they don't control where the money will flow to. It can flow at some point into commodity-related stocks. It can flow into gold, oil, treasuries, but it doesn't flow evenly into these assets. In my opinion, the Treasury, the long-dated Treasuries are essentially the short of the century thing here." On whether gold is a bubble: "I don't think it is a bubble, but I think the gold market has exploded to the upside recently and the correction is overdue. But as I have always maintained for the last 12 years, every responsible adult should gradually accumulate gold, because not owning any gold is the trouble with government. I don't understand. People of Bloomberg, I hardly know anyone who owns any gold physically. All of the Bloomberg employees are intelligent people. They listen to the news every day. They make the news every day. Hardly anyone owns any gold." On what you can do with gold: "I disagree [that you can't do anything with gold.] You give your girlfriend copper rings and I give them gold rings and I keep them longer." On how Faber would play the markets right now: "I think right now the technical picture is so horrible that I would use a rebound as a lightning up opportunity. I think [equities] will move lower. I mean, some say you should move back into emerging economies because the fundamentals of emerging economies are far better than the fundamentals of European countries and the fundamentals of the United States. This is something I will consider." "The only thing I have to say, basically the market has sold off in such a rapid way and with so much momentum that I am smelling as if something really wrong happens in the next two or three months, because the market is a discounting mechanism. Like March 2009 the market started to go up and people were baffled why it started to go up. Now it starts to go down, and maybe after three months people will wake up and scratch their heads and say now, we know why it started to go down, because maybe there is geo political problems, maybe the Middle East blows up, maybe the economy is horrible."

|

| S&P 500 Update – US Dollar Sacrificed Posted: 09 Aug 2011 11:16 AM PDT For more from Trader Dan visit his blog at www.TraderDan.net Dear CIGAs, The FOMC announcement this afternoon sent the equity markets into a complete turnabout from yesterday's big selloff. The catalyst? Try the fact that the Fed said that the economy is so weak that interest rates will not be raised until at Continue reading S&P 500 Update – US Dollar Sacrificed

|

| Posted: 09 Aug 2011 11:12 AM PDT Gold Price Close Today : 1740.00 Change : 29.80 or 1.7% Silver Price Close Today : 37.877 Change : (1.497) or -3.8% Gold Silver Ratio Today : 45.94 Change : 2.503 or 5.8% Silver Gold Ratio Today : 0.02177 Change : -0.001255 or -5.4% Platinum Price Close Today : 1752.50 Change : 36.50 or 2.1% Palladium Price Close Today : 727.75 Change : 8.55 or 1.2% S&P 500 : 1,119.46 Change : -79.92 or -6.7% Dow In GOLD$ : $133.53 Change : $ 2.88 or 2.2% Dow in GOLD oz : 6.460 Change : 0.139 or 2.2% Dow in SILVER oz : 296.74 Change : 22.20 or 8.1% Dow Industrial : 11,239.77 Change : 429.92 or 4.0% US Dollar Index : 73.93 Change : -0.865 or -1.2% Today's markets simply couldn't be traded. Too volatile, offering the opportunity to lose money both downside and upside. Look at these ranges: Stocks, 11,124.01 to 10,604.07 -- 519.94 points or 4.8% Gold, 1,776.95 to $1,720.85 -- $56.10 or 3.3% Silver, 3953.7c to 3697c -- 256.7c or 6.9% Yassir, yassir, that there central bank the Federal Reserve sure enough stabilizes the economy, don't it? The commissars of the Federal Open Market Committee met today and it seems the utterly unwonted honesty of their statement put heart into stock buyers. The statement admits that the economy is pretty bad, and promises to keep the federal funds rate low at least through mid-2013 [sic]. The stock market, which apparently attracts only brain dead investors , rose on this news, although it guarantees the following: 1. The Fed has learned nothing from its failures so far, since, say, 2006 or 1913, whichever starting point you prefer, and will keep on hitting the economy in the head with a ball peen hammer. 2. The Fed will not allow the economy to clear itself of bad investments induced by its previous inflation, so there will be no purging and therefore no recovery. The bankrupt will be kept alive and the price lowering that would clear the market will be stymied. Therefore instead of a one year panic and two year recession, we will get a 20 year Depression. 3. The Fed will continue to keep interest rates artificially low, thus misdirecting more capital into more bad investments. 4. The Fed will continue to inflate the money supply, and so continue to boost silver and gold. 5. The Fed commissars call rising prices "inflation," proving inconclusively that they are so abysmally ignorant that they cannot tell cause ("inflation" or increasing the money supply which only they can do) from effect ("higher prices," caused by inflating). FOLKS, THE FUTURE HAS NEVER BEEN MORE SECURE FOR SILVER and GOLD, THE OUTLOOK NEVER BRIGHTER. Morons are flying the 747 Jumbo Jet of the US economy straight into the Rocky Mountains. Fasten your seat belts. And to that list of emergency measures I published a few days ago, add this: "Reduce all cash balances in banks to an absolute minimum, the amount you need for not more than a couple of months' expenses, and pull out the rest and hold in physical green currency in your own hot hands or in silver or gold." I don't necessarily recommend this swap, but if you ever intend to swap gold for platinum, the time to do it is when the ratio of platinum/gold is 1:1. It's there now. Don't put more than 10% of your precious metals portfolio into platinum. Again, platinum supply and demand is too quirky and too much determined by industrial demand for me to buy it, but some people want it. Anent the gold/silver swap, listen carefully. Read this twice, please. Today the gold/silver closing ratio rose 5.8% to 45.938. That is a new post-May 1 correction high, above the last high at 44.84. MOST LIKELY that means the ratio will move much higher, moreso since it has climbed above the 200 day moving average at 43.85. IF and only IF you swapped silver for gold at a REALIZED ratio of 35 or lower, you ought to be thinking hard about swapping back into silver, because you have a 30%+ profit in ounces. Might want to wait a few days, just to see if it will hit 50. but then again, a bird in the hand is worth two in the shadowy future. IF you swapped gold for silver at a realized ratio ABOVE 35:1, don't swap yet. Figure your approximate profit in ounces by dividing your REALIZED ratio by today's spot ratio. If it equals 1.20, then a swap would net you roughly 20% in ounces. I am not in a hurry to swap because I'm not convinced the crisis/panic has ended yet. However, I remember the proverb, "Bears get rich, and bulls get rich, but pigs get slaughtered." If a 20% or 30% profit in ounces satisfies you, you can swap back into silver now. US DOLLAR INDEX lost a whopping 86.5 basis points (1.11%) driving it all the way back to 73.926, below psychological support at 74 and near the last low (July) at 73.42. Surely, surely the Fed struck the dollar a wicked blow with a stout cudgel, but their blow broke it not. Rally still brews on. The euro rose to 1.4341, up 1.19%. I wouldn't buy euros with your money. Yen, like Frankenstein, has risen from the dead, shaken off the samurai thrusts of the Japanese NGM, and risen nearly clean back to its all time high. Closed today at Y77.05/$ (129.78c/Y100). What's this world coming to, when everybody refuses to believe the Nice Government Men? Stocks were trying to rise today, but about 2:30 lost wind and sank underwater, only to rise 300 points in less than an hour. But before it did it hit my 10,700 Dow target and then some, falling to 10,604.07. Dow closed up 429.92 (3.98%) at 11,239.77. S&P500 gained 4.74% or 53.07 points to close 1,172.53. Friends, these are bizarre markets. Generally one only sees such extreme volatility at big market tops and bottoms, but the Fed seems to be causing this one. Fear not, Bears! The fall will resume, as suddenly as the rally began. Stocks -- they are the Stanley Steamer in the line-up of Investment Automotive Choices. The GOLD PRICE tried thrice to push thru $1,780 today and failed thrice. Support underneath lies at $1,740, stronger at $1,720, stronger still at $1,680. Do NOT count gold out yet. It might yet pierce $1,780 and run clean to $2,000. Might even do that after a couple days' retracement. As long as GOLD remains above $1,720, anything can happen. Point and Figure chart is still calling for $2,090. You don't see markets like today once in 20 years. The SILVER PRICE laboreth beneath that cloud of a breakout in the gold/silver ratio to a new high, portending lower silver value against gold. For the past two days silver has traded down from 4000c, and hit a new low today at 3697c. If it breaches 3700c, then will probably hit the 200 dma at 3381c or go lower. Y'all keep asking me why gold is out-performing silver, and I say again, silver tends to trend against gold in the same direction as stocks. In financial panics, such as what we have now, money flees to gold rather than silver. Later, silver will regain its losses against gold and then some. Silver is offering you a "golden" opportunity to buy at lower prices. You are virtually shooting fish in a barrel when you buy silver, as it will OVER THE LONG TERM rise faster than gold, if not day by day. BOTTOM LINE: Gold may have topped for this leg today, stocks may have bottomed for the move, silver has further to drop, but will probably rise tomorrow. Dollar still trying to bottom and rally. Play defense! Anything can happen. Panic not past. Y'all have mercy on me. Yesterday was brutal, I wrote the commentary, then got distracted doing something else and forgot to upload it. Sorry. Here is yesterdays commentary now posted: http://silver-and-gold-prices.goldprice.org/2011/08/gold-price-closed-at-171020.html Argentum et aurum comparenda sunt -- -- Gold and silver must be bought. - Franklin Sanders, The Moneychanger The-MoneyChanger.com © 2011, The Moneychanger. May not be republished in any form, including electronically, without our express permission. To avoid confusion, please remember that the comments above have a very short time horizon. Always invest with the primary trend. Gold's primary trend is up, targeting at least $3,130.00; silver's primary is up targeting 16:1 gold/silver ratio or $195.66; stocks' primary trend is down, targeting Dow under 2,900 and worth only one ounce of gold; US$ or US$-denominated assets, primary trend down; real estate in a bubble, primary trend way down. Whenever I write "Stay out of stocks" readers inevitably ask, "Do you mean precious metals mining stocks, too?" No, I don't. Be advised and warned: Do NOT use these commentaries to trade futures contracts. I don't intend them for that or write them with that outlook. I write them for long-term investors in physical metals. Take them as entertainment, but not as a timing service for futures.

|

| Posted: 09 Aug 2011 10:56 AM PDT  By EconMatters Markets saw its worst day since the 2008 financial crisis on Monday, Aug. 8, the first trading day since Standard and Poor's downgraded the United States' credit rating. Under the weight of a possible twin crisis in Europe and in the U.S., Dow Jones industrial plunged 634 points. Stocks have lost 15% of their value in just two and a half weeks. On a day like this, who else other than Marc Faber, publisher of the Gloom, Boom & Doom report, would be more appropriate to appear on Bloomberg to talk about the aftermath of the U.S. debt downgrade. Below are some of the highlights in the Bloomberg interview. Regarding equities, Faber believes the U.S. market is "incredibly oversold" and could bottom out in the next few days, but the rally will unlikely make new highs this year. Faber indicates a bear market already started on May 2, 2011 when S&P reached 1,370. The downgrade on U.S. debt by S&P is actually moderately positive on equities as it showed investors that in addition to the conventional interest rate risk factor, now there's another risk--sovereign credit downgrade--in government bonds anywhere in the world. So in the next 10 years, investors will be better off in equities, precious metals than in bonds. Concerning the downgrade by S&P, Faber goes beyond and says 'some kind of default" will happen for the U.S. as the country's "fiscal position is a disaster" if you include the unfunded liability. There are two ways a government can default:

On the possibility of another round of quantitative easing (QE3), Faber sees QE3 would take place when the economy shows significant weakness, or S&P index falls to 1,100 or 1,050 levels. (Note: In a CNBC interview just prior to the S&P downgrade, Faber projects S&P 500 index would hit 1,050 to 1,100 in Oct/Nov timeframe.), Currently, he's allocating his personal portfolio about 20-25% each in equities, real estate in Asia, gold or silver, and corporate bonds. Some Thoughts from EconMatters As pessimistic as Faber thinking S&P's downgrade is "backward looking" not fully reflecting the actual fiscal state of the U.S., there's Warren Buffett who's blasting S&P, ".... remember, this [S&P] is the same group that downgraded Berkshire," and said "The U.S., which was cut Aug. 5 to AA+ from AAA at S&P, merits a "quadruple A" in a separate Bloomberg interview. Buffett's Berkshire is the biggest shareholder of Moody's Corp. that just reaffirms the AAA rating of the U.S. on Monday partly responding to S&P's action. All eyes are on Fitch now to see if it will follow S&P or Moody's making it a crucial swing vote. Things (and markets) could get worse if two out of three major rating agencies end up downgrading the U.S. U.S. fiscal and debt situation is horrendous, and probably deserves a downgrade. However, to me, a downgrade action needs to be supported with charts and tables showing why the current and projected risk profile warrants a downgrade action and how to rectify, rather than the U.S. politics cited by S&P as its main downgrade thesis (Name one Western country where politics do not come into play in the decision-making process?), not to mention some indications of a possible 'unfair distribution' of this downgrade information. So far, the downgrade has only added to the stock market turmoil, while driving up Treasury demand. Is this not counter-productive and counter-intuitive? Hopefully, markets would quit panicking like Faber says so not to be dictated by one rating agency's highly debatable conclusion. Faber Bloomberg interview vid at our blog Further Reading - U.S. Should Downgrade S&P EconMatters | Dynamic View | Facebook Page | Twitter | Post Alert | Kindle

|

| Faber On U.S. Downgrade: U.S. To Have "Some Kind of Default", But Market "Incredibly Oversold" Posted: 09 Aug 2011 10:56 AM PDT

By EconMatters Markets saw its worst day since the 2008 financial crisis on Monday, Aug. 8, the first trading day since Standard and Poor's downgraded the United States' credit rating. Under the weight of a possible twin crisis in Europe and in the U.S., Dow Jones industrial plunged 634 points. Stocks have lost 15% of their value in just two and a half weeks. On a day like this, who else other than Marc Faber, publisher of the Gloom, Boom & Doom report, would be more appropriate to appear on Bloomberg to talk about the aftermath of the U.S. debt downgrade. Below are some of the highlights in the Bloomberg interview. Regarding equities, Faber believes the U.S. market is "incredibly oversold" and could bottom out in the next few days, but the rally will unlikely make new highs this year. Faber indicates a bear market already started on May 2, 2011 when S&P reached 1,370. The downgrade on U.S. debt by S&P is actually moderately positive on equities as it showed investors that in addition to the conventional interest rate risk factor, now there's another risk--sovereign credit downgrade--in government bonds anywhere in the world. So in the next 10 years, investors will be better off in equities, precious metals than in bonds. Concerning the downgrade by S&P, Faber goes beyond and says 'some kind of default" will happen for the U.S. as the country's "fiscal position is a disaster" if you include the unfunded liability. There are two ways a government can default:

On the possibility of another round of quantitative easing (QE3), Faber sees QE3 would take place when the economy shows significant weakness, or S&P index falls to 1,100 or 1,050 levels. (Note: In a CNBC interview just prior to the S&P downgrade, Faber projects S&P 500 index would hit 1,050 to 1,100 in Oct/Nov timeframe.), Currently, he's allocating his personal portfolio about 20-25% each in equities, real estate in Asia, gold or silver, and corporate bonds. Some Thoughts from EconMatters As pessimistic as Faber thinking S&P's downgrade is "backward looking" not fully reflecting the actual fiscal state of the U.S., there's Warren Buffett who's blasting S&P, ".... remember, this [S&P] is the same group that downgraded Berkshire," and said "The U.S., which was cut Aug. 5 to AA+ from AAA at S&P, merits a "quadruple A" in a separate Bloomberg interview. Buffett's Berkshire is the biggest shareholder of Moody's Corp. that just reaffirms the AAA rating of the U.S. on Monday partly responding to S&P's action. All eyes are on Fitch now to see if it will follow S&P or Moody's making it a crucial swing vote. Things (and markets) could get worse if two out of three major rating agencies end up downgrading the U.S. U.S. fiscal and debt situation is horrendous, and probably deserves a downgrade. However, to me, a downgrade action needs to be supported with charts and tables showing why the current and projected risk profile warrants a downgrade action and how to rectify, rather than the U.S. politics cited by S&P as its main downgrade thesis (Name one Western country where politics do not come into play in the decision-making process?), not to mention some indications of a possible 'unfair distribution' of this downgrade information. So far, the downgrade has only added to the stock market turmoil, while driving up Treasury demand. Is this not counter-productive and counter-intuitive? Hopefully, markets would quit panicking like Faber says so not to be dictated by one rating agency's highly debatable conclusion. Faber Bloomberg interview vid at our blog Further Reading - U.S. Should Downgrade S&P EconMatters | Dynamic View | Facebook Page | Twitter | Post Alert | Kindle

|

| Marc Faber on Fed Decision, Treasury Market, Gold Posted: 09 Aug 2011 10:34 AM PDT Marc Faber, publisher of the Gloom, Boom & Doom report, discusses today's Federal Reserve policy decision and the prospects for another asset-purchase program by the Fed. Faber, talking with Carol Massar and Matt Miller on Bloomberg Television's "Street Smart," also talks about the Treasury market and investing in gold.

|

| The Price Of A Big Mac Is Now $17.19 In Zurich Posted: 09 Aug 2011 10:24 AM PDT Submitted by Simon Black of Sovereign Man The price of a Big Mac is now $17.19 in Zurich Just a quick thought on a ridiculously volatile day: One of the things that people pick up on very quickly as they travel are how different price levels are around the world. I've been to roughly 100 countries, and I still find it amazing how much variance there is among things like food, property, and entertainment prices. There are certain places-- Cambodia, Ecuador, Tanzania-- that are so jaw-droppingly cheap that it almost seems unreal. And you wonder how these people could possibly ever survive if they came to your country. Well, the United States has just joined this proud cadre banana republics... at least if you're from Switzerland. You see, the Swiss franc is one of the few currencies that have given investors some sense of comfort recently; Switzerland inspires confidence and stability, and the worse things get in the United States and Europe, the more investors pull their money out of the dollar and euro, and park it in the Swiss franc. It's all about supply and demand. Increased demand for the Swiss franc coupled with expanded supply of dollars and euros has caused the franc to surge over the last weeks and months. It wasn't too long ago that it would take 1.20 francs to buy a US dollar. Now it takes $1.40 to buy a single franc. I can think of a lot of words to describe the performance of the US dollar. Farce. Joke. Lunacy. Embarrassment. Disgusting. But it's more clearly summed up like this: the price of a Big Mac is in Zurich is now so high (at $17.19) that a minimum wage employee in Minneapolis, Minnesota, would have to work for nearly 4-hours in order to afford it. This is what stability looks like to Ben Bernanke.

|

| Stephen Leeb - Silver to Hit $200 Within 24 Months Posted: 09 Aug 2011 10:18 AM PDT  With the Dow trading up 429 points and gold hitting new all-time highs, today King World News interviewed acclaimed money manager Stephen Leeb to get his thoughts on where things are headed. When asked about the action in the stock market Leeb replied, "Well I think the action in the market, the sharp, sharp decline, it really was an incredibly sharp decline, stems from the fact that investors started realize that no one in Washington knows what they are doing. With the Dow trading up 429 points and gold hitting new all-time highs, today King World News interviewed acclaimed money manager Stephen Leeb to get his thoughts on where things are headed. When asked about the action in the stock market Leeb replied, "Well I think the action in the market, the sharp, sharp decline, it really was an incredibly sharp decline, stems from the fact that investors started realize that no one in Washington knows what they are doing. There is no real prospect for coming to agreement...if that's the hand you are dealt and you've got an economy you want to grow, then start talking about cutting taxes or cutting expenditures. But you don't talk about things you know a big group won't agree with. What does this make America look like? What does a typical citizen feel when he sees his Congress and his administration with absolutely no plan for a future with growth in it? It makes them feel sick and I think that was really the major reason for the selloff, it was a psychological reason."

This posting includes an audio/video/photo media file: Download Now |

| When Buying Gold Becomes a Life-or-Death Question Posted: 09 Aug 2011 10:14 AM PDT By Jeff Clark, Editor BIG GOLD, Casey Research I was recently asked in an interview if I thought gold was going to $5,000 an ounce. “No,” I said bluntly. “I think it’s going higher.” “You’re that optimistic?” “No,” I replied. “I’m that pessimistic.” Imagine the condition of our world if gold reached $5,000 an ounce – and kept soaring. We’ll likely be in a mania if that happens – but what kind of mania will it be? There’ll be some greed to be sure, but I think there’s a good chance a deeper reason will be at play. And it’s the same reason that will drive you to keep buying gold at $2,000 an ounce. You’ll have to. There are 101 reasons to own gold right now. You might buy because of the debt turmoil you see around the globe. You may think it wise, like the Chinese and others, to keep some of your savings in gold. Negative real interest rates may draw yo...

|

| S&P 500 Update - US Dollar sacrificed Posted: 09 Aug 2011 10:13 AM PDT [url]http://www.traderdannorcini.blogspot.com/[/url] [url]http://www.fortwealth.com/[/url] The FOMC announcement this afternoon sent the equity markets into a complete turnabout from yesterday's big selloff. The catalyst? Try the fact that the Fed said that the economy is so weak that interest rates will not be raised until at least the middle of 2013 - a full two years away! That acknowledgement, namely, that growth is so sluggish, the economy so moribond and unemployment so chronically high, sent money flowing into BOTH stocks and bonds at the same time. How's that for a neat trick by the boyz at the Fed? Here is the deal - the FOMC is attempting to drive money out of bonds and INTO equities based on the fact that they have guaranteed practically no return as far as yields go on short term Treasuries for at least two years. Think about that. As an investor would you want to lock up money for that long for that kind of yield or would you want to buy stocks and attempt to capture a ...

|

| Where Oh Where Are The Safe Havens From Yesteryear? Posted: 09 Aug 2011 09:58 AM PDT Gold Stock Trades (GST) is witnessing the resumption of the long term uptrend in gold(GLD) and silver(SLV) bullion and precious metals mining stocks(GDX). Along the way there have been many negative voices that were counseling ... Read More...

|

| Posted: 09 Aug 2011 09:52 AM PDT Economic Uncertainty Leading to Global Unrest

|