Gold World News Flash |

- China’s Record Dumping Of US Treasuries Leaves Goldman Speechless

- Understanding How The Recent Paper Gold/Silver Market Was Faked

- Monday’s Panic Selling In The Gold Market Has Only Occurred 6 Times In History – Price Moves After Each Historic Panic Are Remarkable

- Greek Prime Minister Asked Putin For $10 Billion To "Print Drachmas", Greek Media Reports

- Can You Hear the Fat Lady Singing?: The China Connection

- China's Record Dumping Of US Treasuries Leaves Goldman Speechless

- Gold Price Closed $3.30 Lower at $1,103.40

- Gold Warns Again

- Comex Registered 'Deliverable' Gold Bullion Stores - Money Is All About Power To Some

- Wall Street Prepares To Reap Billions From Another Main Street Wipe Out

- Confirmed: Obama To Confiscate Retirees Guns

- Confirmed US allies fund ISIS

- Gold Daily and Silver Weekly Charts - Whatever We Say It Is

- Mark O'Byrne: Sunday night's brazen attack on gold starts to prompt questions

- Does A Commodities Crash Mean Global Depression, Mass-Devaluation Or Both?

- The Fed, Rand Paul, and the Next Financial Crisis

- William Binney : Surveillance State Is Corrupting American Way Of Life

- The China Bubble About To Burst? Watch Out America You are next ! -- Richard Wolff

- A Strong Dollar, Not Weak Gold, Story

- John Stossel - Recycling Stupidity

- Peter Schiff : The Civil War Was Not About Slavery - We're All Slaves Now

- Onboard the TransCanada Railroad

- Gold Hammered “Unprecedented Attackâ€

- Fun With Numbers

- Gold: Breakdown Or Simple Overshoot?

- Here’s How to Profit from the Death of King Coal

- Gold, Commodities Routed

- Shamed FIFA President Sepp Blatter Showered in Dollar Bills by Lee Nelson

- Tuesday Morning Links

- Gold and Silver: The Final Capitulation Commences

- Is Gold a Stupid "Pet Rock" or a Bedrock Asset?

- Are Gold Investors Finally Capitulating?

| China’s Record Dumping Of US Treasuries Leaves Goldman Speechless Posted: 21 Jul 2015 11:39 PM PDT from Zero Hedge: On Friday, alongside China’s announcement that it had bought over 600 tons of gold in “one month”, the PBOC released another very important data point: its total foreign exchange reserves, which declined by $17.3 billion to $3,694 billion. We then put China’s change in FX reserves alongside the total Treasury holdings of China and its “anonymous” offshore Treasury dealer Euroclear (aka “Belgium”) as released by TIC, and found that the dramatic relationship which we first discovered back in May, has persisted – namely virtually the entire delta in Chinese FX reserves come via China’s US Treasury holdings. As in they are being aggressively sold, to the tune of $107 billion in Treasury sales so far in 2015. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Understanding How The Recent Paper Gold/Silver Market Was Faked Posted: 21 Jul 2015 09:20 PM PDT from GregoryMannarino: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 21 Jul 2015 08:20 PM PDT from KingWorldNews:

For the past couple of days in this report in the update on gold stocks, we’ve been watching for heavy, exhaustive selling over the next several sessions as likely signaling a wash-out. That’s what’s happening now, as Monday’s activity had many of the hallmarks of panic selling pressure. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Greek Prime Minister Asked Putin For $10 Billion To "Print Drachmas", Greek Media Reports Posted: 21 Jul 2015 07:30 PM PDT Back in January, when we reported what the very first official act of open European defiance by the then-brand new Greek prime minister Tsipras was (as a reminder it was his visit of a local rifle range where Nazis executed 200 Greeks on May 1, 1944) we noted that this was the start of a clear Greek pivot away from Europe and toward Russia. We further commented on many of the things that have since come to pass:

But most importantly, even back then we explicitly said that in order for Greece to preserve its leverage (something it found out the hard way it did not have 6 months later), it would need a Plan B, one that involves an alternative source of funds, i.e., Russia and/or China, which could be the source of the much needed interim cash Greece needs as it prints its own currency and prepares for life outside the European prison.

Somewhat jokingly, on June 27, the day after Tsipras announced the shocking referendum decision, we repeated precisely this: As it turns out, none of this was a joke, and, if Greek newspaper "To Vima" is to be trusted, a "Plan B" involving an emergency $10 billion loan from Vladimir Putin which would be used to fund a new Greek currency, is precisely what Greece had been contemplating! According to Greek Reporter, Greek Prime Minister Alexis Tsipras has asked Russian President Vladimir Putin for 10 billion dollars in order to print drachmas. In other words, if true, then Greece did just as we said it should: approach Russia and the BRICs with a request for funding to be able to exit Europe's gravitational pull...

... however, somewhat surprisingly, both Moscow and Beijing said no:

The report continues:

But the biggest stunner: it was Putin who declined the offer on the night of the referendum.

In other words it was not Tsipras' failure to predict how Greece would react to the Greek referendum nor was it his secret desire to lose it as previously suggested (expecting a Yes vote and getting 61% "No"s instead), but a last minute rejection by Putin that lead to the Greek government's capitulation, and the expulsion of Varoufakis who most certainly was the propagator of this plan. It also means that Merkel suddenly has a massive debt of gratitude to pay to Vladimir, whose betrayal of the Greek "marxists" is what allowed the Eurozone to continue in its current form. The question then is what is Vlad's pro quo in exchange for letting down the Greek government (and handing over its choicest assets to the (s)quid), whose fate was in the hands of the former KGB spy. Finally, it is very possible that To Vima is taking some liberties with truth. For confirmation we would suggest to get the official story from Varoufakis, who lately has been anything but radio silent. If confirmed, this will certainly be the biggest and most underreported story of the year, one which suggests that the perpetuation of Merkel's dream of a united Europe was only possible thanks to this man.

If confirmed, first and foremost look for a growing schism between Europe and the US (which has clearly been pushing Merkel's buttons via the IMF's ever louder demands for a debt haircut not to mention Jack Lew's rather direct intervention in the Greek bailout negotiations) and an increasing sense of friendly proximity between Berlin (and Brussels) and Moscow. The biggest loser in this game of realpolitik, once again, are the ordinary Greek people. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Can You Hear the Fat Lady Singing?: The China Connection Posted: 21 Jul 2015 06:07 PM PDT By Chris at www.CapitalistExploits.at Greece is connected to China by the very same thing which has been connecting sex, drugs, and rock'n'roll since Bretton Woods - dollars. Last week I shared some thoughts on the unintended consequences of actions taken in Europe and why Greece may matter as a result. There is zero chance that the actions taken will result in a stronger Europe, a stronger euro, or an economic strengthening in either Greece or the wider eurozone. Zero! As interesting as Greece and the euro is, my attention today is on China and how China may well be forced by events taking place globally to make some far reaching choices. Two scenarios have been widely discounted by the market with respect to China. The first is a remnimbi devaluation and the second is a hard landing for a slowing Chinese economy. We know that the Chinese economy is slowing. We know this because Beijing tells us it's so. Their last numbers were that the economy has slowed to their growth target of 7%. Bang on their target rate. How convenient! Now of course these numbers are rubbish, but it's telling that they're acknowledging a slowing economy. We account for these government numbers in the same way we account for any government numbers: by acknowledging that underneath all the pompous sophistication of bureaucrats everywhere pulsates the brain of a tree shrew. The important takeaway is that they're acknowledging they're slowing. China's Market Crash As everybody now knows, the Chinese stock market lost over 30% in 3 weeks wiping $2.8 trillion off the books. The only way to lose that much money in such a rapid period of time is by getting caught by your wife having hanky panky with her best friend. Sure, investors who bought at the top are hurting, but consider that the stock market is up roughly 80% over the last 12 months, and this is AFTER the crash. Viewed with that timeframe and taken into context this is hardly problematic. This correction is nowhere near as big a concern as it would be if we had a similar occurrence take place in the US due to who is participating. 80 – 90% of the domestic A-share market is made up of retail investors. Novices. This was a bubble waiting to burst as retail investors flooded the market with a record 40 million new brokerage accounts created in the last year. Not only were novices entering the market but they were entering it on margin. By June of this year margin lending as a percentage of market cap ran as high as 20%. While these investors make up the majority of the market they represent a small part of the population. The free float of China's markets is about a third of GDP, whereas in the developed world this number is over 100%. A soaring stock market and a crashing stock market will have little effect on the vast majority of Chinese households. This is unlike the developed world. Essentially, this is a tiny portion of the market that got burned. It really needn't be a problem unless someone does something stupid and causes unintended consequences. Sadly this is exactly what Beijing is doing. Is China or the US the Next Greece? Perhaps it's simply a matter of timing and what's racing across the news feeds but I've read quite a few articles about how the US and China are next after Greece. Debt levels are cited along with a host of other similarities. This is - how do I put this politely - rubbish. The US and China are NOT Greece. Even if the debt levels were the same the similarities end there. Greece cannot issue its own currency. In last week's missive I mentioned that:

That makes Greece unique. The US, on the other hand, can print all the currency they want and pay their debts at par. Greece can't do that. The bonds of the US, Japan and even China are not at all to be likened to the bonds of Greece. One needs to make a distinction between debt denominated in the country in questions own currency and debt denominated in some other currency. For countries sporting high debt levels and where simultaneously those debts are foreign denominated this can become a huge problem. Just ask that crazy woman in Argentina... The Asian crisis, which I discussed last week, is such an example whereby debts denominated in USD became unsustainable. Once the rout started a self-fulfilling trend developed whereby as the currencies in Southeast Asian nations moved lower this added multiples to the payments required on leveraged assets. A vicious unwinding of the carry trade. China's Reaction What I find the most fascinating is not the correction in the Chinese stock market but the actions taken by the PBOC subsequently. This can only be described as outright panic. Consider the following actions taken.

Aside from the fact that they are doing exactly the opposite of what should be done I find it telling that they are so willing to slash rates and devalue the yuan. As mentioned, this needn't be a problem if they simply let the market correct and find its equilibrium. They haven't done that and this is what has caught my attention more than anything else. The Debt Component and What This May Mean for the Yuan Debt is important to understand as debt is the "gasoline" added to any trade. Debt, or more correctly put, leverage amplifies gains and losses and as such is both the prozac as well as the viagra of global markets. I wrote extensively about the US carry trade in our USD Bull Report but will summarise an important point. China boasts an estimated US$3 trillion borrowed and invested in various Chinese assets. A decline in those assets values materially affects investors who've leveraged their positions, but what really really matters is when the funding currency appreciates and those investors who are short dollars are forced to buy back their dollar positions. Now this is where Greece and China are interconnected. Greece, as mentioned, threatens to be a poster child of Europe and the euro. This is naturally bullish for the euro in the same way that spandex pants look good on Angela Merkel - not so much!

In Europe we have intervention in the markets by Brussels. They may save Greece from introducing the drachma and devaluing it, and having German banks forced to realise losses but they can't stop the market from devaluing the euro. Risk off is "on" and the dollar is moving higher. In China we have Beijing intervening in the markets and we have to wonder what those US$3 trillion in the USD carry trade are invested in and what they look like right now. Consider that globally we are seeing liquidity drying up and global capital flows moving into shorter term paper - US paper. Two months ago I wrote about capital moving into shorter maturity paper:

When looking to understand China I believe that the probability of of a devaluation of the yuan has just risen markedly. About the Yen? I would be remiss in mentioning the yen from any discussion on global capital flows. The yen goes lower. We've been saying that for 2 years now and I won't rehash thoughts here. Few seem to understand that the devaluation of the yen exacerbates the probability of a Chinese hard landing and that increases the risks of a devaluation of the yuan. A rising dollar is globally deflationary. What happens when we get deflation in China? China absolutely cannot have deflation and will be stuck between attempting to maintain a strong currency and stimulating their economy. This threatens to rapidly become a situation where they run out of "palatable" options and the least painful will be to devalue the yuan. Both politically and economically it will be acceptable. Most importantly it will allow those in power to stay in power. To summarize, China has:

Soros famously said to "find the premise which is false and bet against it". When the market's premise is false, coincidentally the pricing of assets reflects this. Looking at the futures and options markets right now the market is NOT expecting a Chinese devaluation. We think this is a mistake. The market typically has the collective mentality of a hive, and a pool hall understanding of the global interconnectedness that drives global capital flows. At the local level it believes in the ability of central bankers to forever prop markets. It believes in imposing rules and laws to circumvent free market forces, and it believes this because it views the world through the microcosm of an extremely limited timeframe and geography, much like a field mouse in a corn field surveying its landscape, unable to see the harvesters warming up. I will leave you with one last thought. This time from the brilliant Albert Edwards of SocGen

- Chris | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| China's Record Dumping Of US Treasuries Leaves Goldman Speechless Posted: 21 Jul 2015 06:07 PM PDT On Friday, alongside China's announcement that it had bought over 600 tons of gold in "one month", the PBOC released another very important data point: its total foreign exchange reserves, which declined by $17.3 billion to $3,694 billion.

We then put China's change in FX reserves alongside the total Treasury holdings of China and its "anonymous" offshore Treasury dealer Euroclear (aka "Belgium") as released by TIC, and found that the dramatic relationship which we first discovered back in May, has persisted - namely virtually the entire delta in Chinese FX reserves come via China's US Treasury holdings. As in they are being aggressively sold, to the tune of $107 billion in Treasury sales so far in 2015.

We explained all of his on Friday in "China Dumps Record $143 Billion In US Treasurys In Three Months Via Belgium", and frankly we have been surprised that this extremely important topic has not gotten broader attention. Then, to our relief, first JPM noticed. This is what Nikolaos Panigirtzoglou, author of Flows and Liquidity had to say on the topic of China's dramatic reserve liquidation

JPM conclusion is actually quite stunning:

Incidentally, $520 billion is roughly triple what implied Treasury sales would suggest as China's capital outflow, meaning that China is also liquidating some other USD-denominated asset(s) at a feverish pace. So far we do not know which, but the chart above and the magnitude of the Chinese capital outflow is certainly the biggest story surrounding the world's most populous nation: what is happening in its stock market is just a diversion. At this point JPM goes into a tangent explaining what the practical implications of a massive capital outflow from China are for the global economy. Regular readers, especially those who have read our previous piece on the collapse in the Petrodollar, the plunge in EM capital inflows, and their impact on capital markets and global economies can skip this part. Those for whom the interplay of capital flows and the global economy are new, are urged to read the following:

Summarizing the above as simply as possible: for all those confounded by why not only the US, but the global economy, hit another brick wall in Q1 the answer was neither snow, nor the West Coast strike, nor some other, arbitrary, goal-seeked excuse, but China, and specifically over half a trillion in still largely unexplained Chinese capital outflows. * * * But wait, because it wasn't just JPM whose attention perked up over the weekend. This morning Goldman Sachs itself had a note titled "the Curious Case of China's Capital Outflows":

Granted, this is smaller than JPM's $520 billion number but this also captures a far shorter time period. Annualizing a $224 billion outflow in one quarter would lead to a unprecedented $1 trillion capital outflow out of China for the year. Needless to say, a capital exodus of that pace and magnitude would suggest that something is very, very wrong with not only China's economy, but its capital markets, and last but not least, its capital controls, which prohibit any substantial outbound capital flight (at least for ordinary people, the Politburo is clearly exempt from the regulations for the "common folk"). Back to Goldman:

In other words, for once Goldman is speechless, however it is quick to point out that what traditionally has been a major source of reserve reflow, the Chinese current and capital accounts, is no longer there. It also means that what may have been one of the biggest drivers of DM FX strength in recent years, if only against the pegged Renminbi, is suddenly no longer present. While the implications of this on the global FX scene are profound, they tie in to what we said last November when explaining the death of the petrodollar. For the most part, the country most and first impacted from this capital outflow will be China, something its stock market has already noticed in recent weeks. But what is likely the take home message for non-Chinese readers from all of this, is that while there has been latent speculation over the years that China will dump US treasuries voluntarily because it wants to (as punishment or some other reason), suddenly China is forced to liquidate US Treasury paper even though it does not want to, merely to fund a capital outflow unlike anything it has seen in history. It still has a lot of 10 Year paper, aka FX reserves, left: about $1.3 trillion at last check, however this raises two critical questions: i) what happens to 10 Year rates when whoever has been absorbing China's Treasury dump no longer bids the paper and ii) how much more paper can China sell before the entire world starts paying attention, besides just JPM and Goldman... and this website of course. Finally, if China's selling is only getting started, just what does this mean for future Fed strategy. Because one can easily forget a rate hike if in addition to rising short-term rates, China is about to dump a few hundred billion in paper on a vastly illiquid market. Or let us paraphrase: how soon until QE 4? | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold Price Closed $3.30 Lower at $1,103.40 Posted: 21 Jul 2015 05:40 PM PDT

Unlike gold, silver's RSI is not oversold, although it was more oversold than today at the 7 July low. As volume was also significantly higher on the 7 July low and lower yesterday, that's the sort of thing that suggests a double bottom, but no confirmation yet.

Silver and GOLD PRICES need to show a sharp reversal, preferably a drop into a slightly new low with a higher close for the day. Or a nice big jump over $15.00 and $1,130 would do, too. I have the oddest feeling I am witnessing 2008 in slow motion. I mean the metals markets, of course. During that fall panic premiums on all forms of silver shot up and physicals prices de-coupled from futures prices. It didn't matter that the futures price was $8.80, you couldn't buy any physical silver at all for less than $13.20, a 50% premium or higher. Delivery was delayed for eight weeks. Gold price premiums weren't as strongly affected, but gold deliveries were as badly delayed. Now US90% is carrying a 23.5% premium (350 cents/oz) at wholesale, more expensive even than silver American Eagles. The US mint has suspended silver American Eagle deliveries, and other privately minted silver rounds are two to three weeks out. I feel lucky to have a few in stock. Maybe I've been listening to the wind in the tulip poplars too long, but a weird urgency hangs over things. Somebody asked me about rumors of China dumping gold. Me, I have no way of knowing, but I doubt it. China ain't gold's problem, western central banks, and especially the Fed and US government, are. I've been thinking about that Gold price, and I got to looking at the Relative Strength Index. Invented by the great commodity trader Welles Wilder, it's a momentum oscillator that measures speed and change of price movements. RSI oscillates between zero and 100, but is overbought above 70 and oversold below 30. Yesterday, 20 July 2015, the gold RSI was more oversold at 18.46 than at any time since the fiasco days of 2013 when the nearest RSI reading to the bottom was 19.71 (15 April 13 read 15.3). Before that, you have to stretch back to 19 July 1999 bottom with an RSI at 26.26. (Readings in June 1999 were lower). Another odd thing: the RSI sometimes makes it low a day before, the price low. Yesterday the RSI closed at 18.46, today it's at 21.16. That caught my eye.

Stocks lost all their gas today and crumpled like a leaky dirigible. Dow lost 181.12 (1%) to 17,919.29, below the morale-bustin' 18,000 line. S&P500 gave up 9.07 (0.43%) to 2,119.21. Dow closed below its 50 DMA. Dow in gold and Dow in silver turned sharply down.

One day soon stocks will begin coming apart and silver and gold rising. Sometimes you don't even know the turnaround day when you see it. Aurum et argentum comparenda sunt -- -- Gold and silver must be bought. - Franklin Sanders, The Moneychanger The-MoneyChanger.com © 2015, The Moneychanger. May not be republished in any form, including electronically, without our express permission. To avoid confusion, please remember that the comments above have a very short time horizon. Always invest with the primary trend. Gold's primary trend is up, targeting at least $3,130.00; silver's primary is up targeting 16:1 gold/silver ratio or $195.66; stocks' primary trend is down, targeting Dow under 2,900 and worth only one ounce of gold or 18 ounces of silver. or 18 ounces of silver. US $ and US$-denominated assets, primary trend down; real estate bubble has burst, primary trend down. WARNING AND DISCLAIMER. Be advised and warned: Do NOT use these commentaries to trade futures contracts. I don't intend them for that or write them with that short term trading outlook. I write them for long-term investors in physical metals. Take them as entertainment, but not as a timing service for futures. NOR do I recommend investing in gold or silver Exchange Trade Funds (ETFs). Those are NOT physical metal and I fear one day one or another may go up in smoke. Unless you can breathe smoke, stay away. Call me paranoid, but the surviving rabbit is wary of traps. NOR do I recommend trading futures options or other leveraged paper gold and silver products. These are not for the inexperienced. NOR do I recommend buying gold and silver on margin or with debt. What DO I recommend? Physical gold and silver coins and bars in your own hands. One final warning: NEVER insert a 747 Jumbo Jet up your nose. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

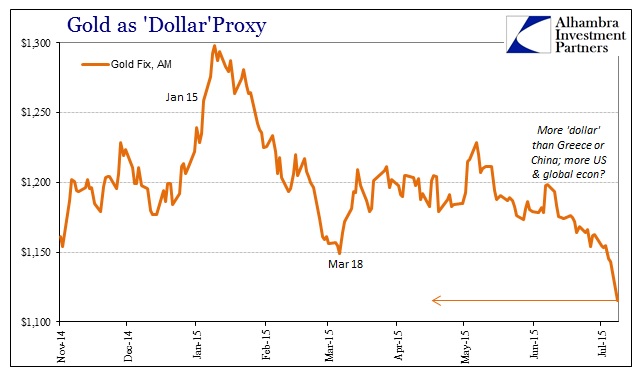

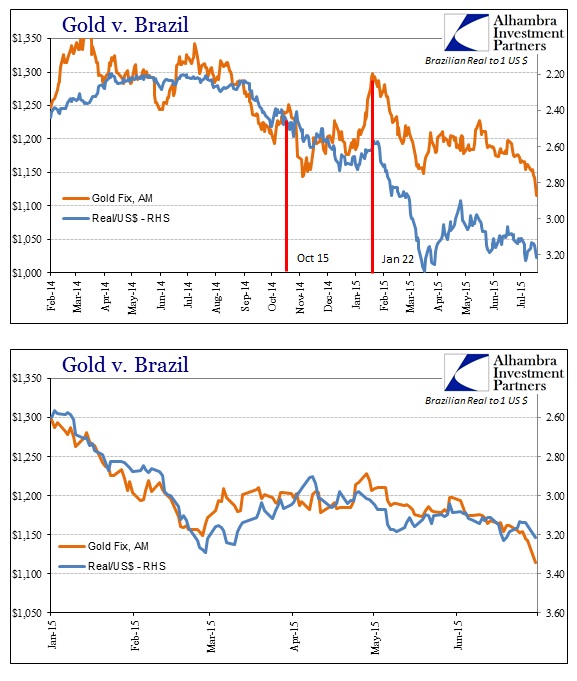

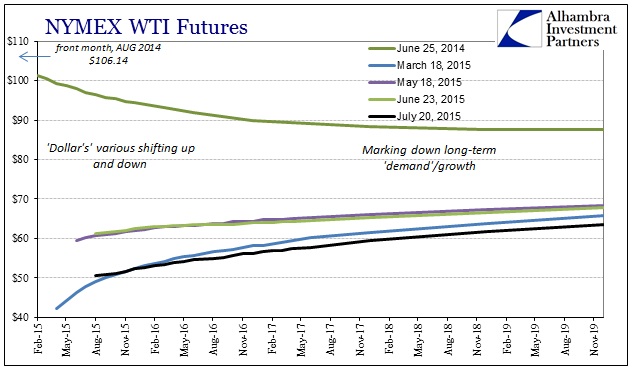

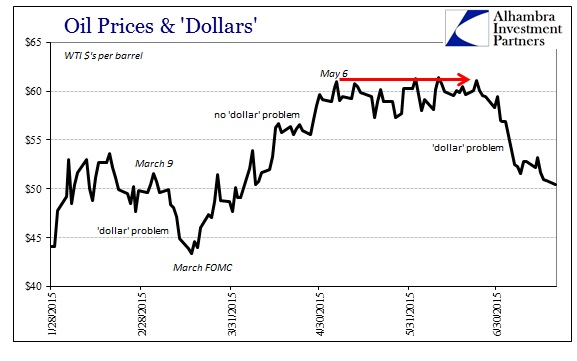

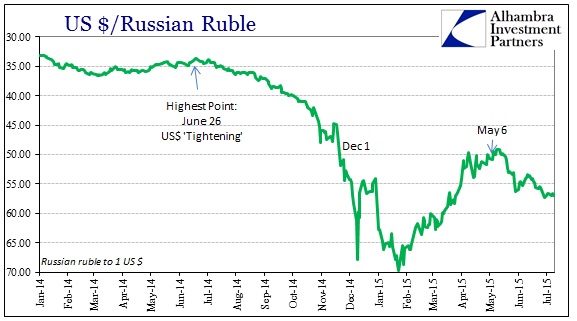

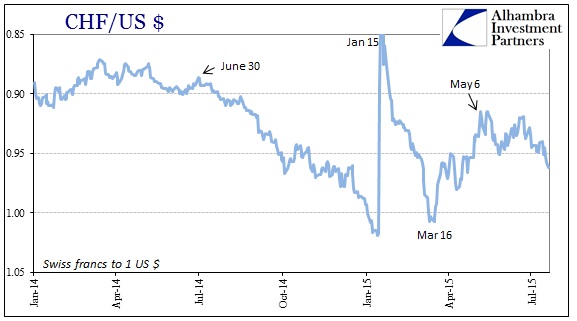

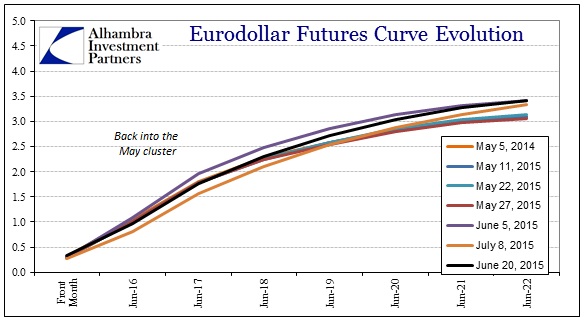

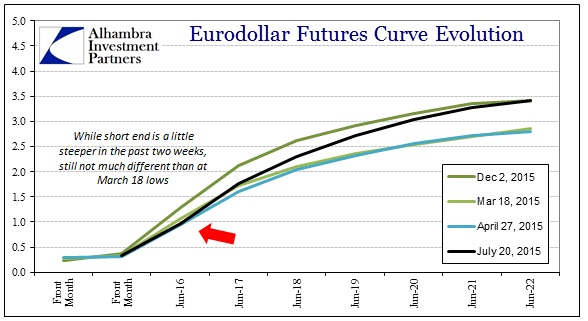

| Posted: 21 Jul 2015 05:30 PM PDT Submitted by Jeffrey Snider via Alhambra Investment Partners, With all the problems right now beyond Greece and China, from Canada’s “puzzling” recession to Brazil’s unfolding disaster, and even the still-“shocking” US economic slump, it is interesting that gold garnered the most attention in early Monday trading. The fact that gold prices were slammed in Asian trading was certainly significant, but that really isn’t why gold is being highlighted all over the world. With gold prices at a five-year low, economists have some “market” indication that finally, they think, is moving in their favor, thus distracting, minutely, from all the global conflagration.

It is far more indirect than in 2013 when economists were positively crowing about the slams in gold, but the same basic setup remains even if almost coded; “U.S. rate hikes” are supposed to occur when the FOMC judges the US economy, and the globe by extension, quite sufficient so the drastic fall in gold is once more an indication, though indirect this time, that all will be well soon enough. You would think that after being so wrong about gold in 2013 that economists would be far more careful about appealing in that direction, and maybe they are since they have so far remained, as noted above, more muted than openly projecting great economic recovery with low gold prices this time. That may itself be significant, in that while economists remain gold haters (literally) they aren’t, contra two years ago, declaring decisively its death as evidence of at the same time central bank omniscience. Of course, gold prices are not limited to simple-minded appeals upon interest rates or even differentials, as clearly mainstream commentary continues to have great trouble with gold behavior in any direction.

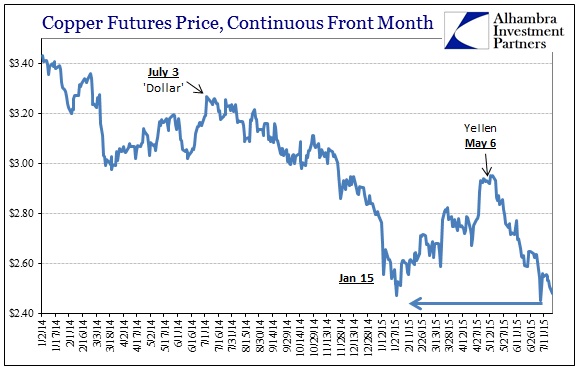

Again, 2013 provides a guide as to why gold prices may be declining in sharp moves, especially right at the open or in weaker trading hours, and it has very little to do with interest rates apart from fixed income suggesting the same factors about the “dollar.” Whether it is growing unease about the global economic picture or the “sudden” recurrence of financial irregularity almost wherever you wish to gaze, the “dollar” is once more wreaking havoc. This isn’t controversial at all, but somehow economists can miss that gold is global and universal collateral and when the eurodollar system is stressed it becomes activated in that manner. The correlations alone are strongly suggestive of these financial factors. The relationship between gold and the real, for instance, is quite indicative of eurodollar financing trends. Apart from the sharp rise in gold just before the January 15 franc event, gold and the real have been almost inseparable in both timing and degree. The damage extends beyond that affiliation, however, as the “dollar” (bank balance sheet factors) is again moving quickly. Copper has been pushed back under $2.50 and crude oil, at least at WTI spot, is nearly back into the $40’s again for the first time in months (despite recent drawdowns in both inventory and production). In other words, there was a brief respite once Greece slipped on its noose and the Chinese rewrote their stock market, but that short enthusiasm hasn’t at all disrupted the renewed wholesale retreat. Since early to mid-May, the “dollar” has been spotty in its effects, but those negative pressures have clearly started to unify into renewed irregularity in late June and early July. In that respect, Greece and China may have just been visible sideshows of all that. Even the Swiss franc has found its way below 0.963, a low not posted since April. The catalyst may be the FOMC’s increased publicity about its preferred intentions to get “markets” to reflect the recovery and economy that isn’t there, but even that is rather unclear as eurodollar futures aren’t really anymore suggestive of that potential then they were back in March. The futures curve had sunk to an unusual level in early July (maybe that was Greece), so recent trading has simply pushed the curve back into the same cluster as dominated in May. In other words, it doesn’t appear, and certainly not decisive, that “higher U.S. interest rates” is actually being predicted here, rendering the mainstream ideas about gold once more grasping at straws. In my view, the “dollar’s” destructive tendencies here are more primal rather than exclusively policy-specific. I think in this accumulated view these “dollar” proxies suggest that regardless of the FOMC’s stated tendencies there is already more than a fair amount of volatility and disorder evident not just in these markets but in the global economy (“unexpected” only to economists). Thus, any perceptions about the FOMC raising rates (whatever they think they can) is just another element of amplification of that existing and underlying syndrome and distress. The initial “dollar” behavior after the March FOMC meeting strengthens that reading as I think it amounted to not better fortune but rather just some less distant hope that the without a suicidal FOMC “dollar” pressures might on their own ease and abate – that without a forced policy shift the underlying torment might be able to in shorter order resume more stable behavior and existence free from further depressive influence. The “dollar” and fixed income world had grown so bearish especially after December 1 that it was due for at least a minor retracement on even the most marginal of hope. I really believe that was the animating factor of credit and “dollars” out of 2013; that gold correctly predicted growing eurodollar problems that were parallel and related to fomenting economic decay. The FOMC’s role was simply to further antagonize those concerns, which they did repeatedly on the flimsiest of narratives. Yellen’s May 6 speech about stock bubbles and “reach for yield” was thus damaging in that respect; that the FOMC was instead going to push on with its amplification of negative pressure and send the world further into its tailspin regardless of how much discontent and disquiet was already evident. The action in gold in 2013 was a warning about the “dollar”, a warning that went completely unheeded yet has been largely fulfilled. Current gold prices and the rest of the “dollar’s” proxies are, if only in smaller doses this time, suggesting the same tendency. In short, while the magnitude might be diminished now that is only because the time component is so much shorter and the “wavelength” so much more widespread; the point of no-return may be at hand or already surpassed. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Comex Registered 'Deliverable' Gold Bullion Stores - Money Is All About Power To Some Posted: 21 Jul 2015 05:16 PM PDT | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wall Street Prepares To Reap Billions From Another Main Street Wipe Out Posted: 21 Jul 2015 05:00 PM PDT On Monday evening, we noted that market participants are reducing the size of their trades and turning to derivatives in order to avoid the perils associated with what are increasingly illiquid markets. While we've been pounding the table on bond market liquidity for years, the rest of the world (operating on the standard 2-3 year time lag) has just begun to wake up to how thin markets have become. Now, pundits, analysts, billionaire bankers, and incorrigible corporate raiders alike are shouting from the rooftops about the pitfalls of illiquidity. The secondary market for corporate credit has received the lion's share of the attention (for reasons we outlined yesterday) and as Carl Icahn was at pains to explain to Larry Fink last week, ETFs are a large part of the problem. The story is simple. Shrinking dealer inventories (the result of a post-crisis regulatory regime wherein the term "prop trader" is taboo) have made it harder to transact in size without having an outsized effect on prices for corporate bonds. Meanwhile, artificially suppressed borrowing costs and the attendant hunt for yield have led to record corporate issuance and voracious investor demand. In short, the primary market is booming while the secondary market has become a veritable no man's land. If you need an analogy, try this: the crowded theatre is getting larger and more crowded while the exit keeps getting smaller. The proliferation of ETFs has made it easier for the retail crowd to chase yield in corners of the bond market where they might not have dared to venture before, and this has only served to create still more demand for things like high yield credit. Now, with the US staring down a rate hike cycle, and with some corners of the HY market (see HY energy for instance) facing a number of insurmountable headwinds going forward, the fear is that the retail crowd will all head for the exits at once, leaving fund managers with a very nondiversifiable, unidirectional flow which will force them to sell the underlying assets into illiquid markets. Due to a generalized lack of market depth, that selling pressure has the potential to trigger a rout. Of course a sharp decline in prices would send still more panicked retail investors to the exits necessitating even more asset sales by fund managers and so on, and so forth. But don't take our word for it, here's WSJ with more on how Wall Street is preparing to profit from an unwind in Main Street's ETF and mutual fund portfolios:

When Reuters first reported that fund managers were lining up emergency liquidity lines like the ones mentioned above, we smelled trouble and were quick to note that not only did that not bode well for the market, but that funding redemptions with borrowed cash is a fool's errand and depends upon the market stress being transitory (see here and here). But beyond that, it betrayed the extent to which the country's largest and most influential ETF issuers have become worried about just the type of meltdown the hedge funds mentioned above are banking on. If you want a candid take on just what the smart money thinks is ahead for all of the retail money that's been herded into esoteric ETFs, we'll leave you with the following from David Tawil, president of hedge fund Maglan Capital, who spoke to WSJ:

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Confirmed: Obama To Confiscate Retirees Guns Posted: 21 Jul 2015 04:00 PM PDT Alex Jones talks with Patrick Howley about the latest information regarding the ongoing attack on the 2nd Amendment and who the next target group is. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists ,... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 21 Jul 2015 03:34 PM PDT Please remind PM David Cameron before he sends UK military into Syria that friends and allies of the USA are funding ISIS. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold Daily and Silver Weekly Charts - Whatever We Say It Is Posted: 21 Jul 2015 02:12 PM PDT | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mark O'Byrne: Sunday night's brazen attack on gold starts to prompt questions Posted: 21 Jul 2015 12:56 PM PDT 3:55p ET Tuesday, July 21, 2015 Dear Friend of GATA and Gold: GoldCore's Mark O'Byrne today notes that Monday's brazen bear raid on the gold price has prompted questions from a few usually oblivious sources. His commentary is headlined "Gold Hammered Down In Sunday Night's 2-Minute, $2.7 Billion 'Unprecedented Attack'" and it's posted at GoldCore here: http://www.goldcore.com/us/gold-blog/gold-hammered-down-in-sunday-nights... CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT Buy precious metals free of value-added tax throughout Europe Europe Silver Bullion is a fast-growing dealer sourcing its products from renowned mints, refiners, and distributors. Because of a legal loophole that will close soon, you can acquire the world's most popular bullion coins free of value-added tax throughout the European Union. You can collect your order in person at our headquarters in Tallinn, Estonia, or have it delivered in any of the 28 EU countries. Europe Silver Bullion is owned and operated by North American and European experts in selling, storing, and transporting precious metals. We have an extensive product inventory of silver, gold, platinum, and palladium, and our network spans the world. Visit us at www.europesilverbullion.com. Join GATA here: New Orleans Investment Conference http://noic2015.eventbrite.com/?aff=gata The Silver Summit and Resource Expo 2015 http://cambridgehouse.com/event/50/the-silver-summit-and-resource-expo-2... Support GATA by purchasing recordings of the proceedings of the 2014 New Orleans Investment Conference: https://jeffersoncompanies.com/landing/2014-av-powell Or by purchasing DVDs of GATA's London conference in August 2011 or GATA's Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Does A Commodities Crash Mean Global Depression, Mass-Devaluation Or Both? Posted: 21 Jul 2015 12:53 PM PDT First, precious metals peaked and began drifting lower. Then copper fell, oil plunged and it became obvious that these weren’t isolated events. The entire commodities complex — that is, all the physical inputs a modern economy uses to power, transport and build stuff — was in sustained decline. Here’s the Bloomberg Commodities Index over the past five years: Now, after the past week’s free-fall, commodities are front-page news:

A few questions: Q: Why did it take so long for the commodities crash to penetrate the conventional wisdom? Because it conflicted with the general theme of global economic recovery. The US was reporting lower unemployment (though a lot of analysts continued to point out the bogus nature of that stat) and Europe and Japan had begun aggressive QE programs (which always leads to more borrowing and spending, right?). So despite the occasional hiccup, 3%+ growth was a lock going forward. Consider the opening paragraphs of this July USA Today article:

Growth of 3.3% is not bad at all, and it remains the consensus forecast for 2016. This implies fairly robust demand for commodities, so the fact that their prices are declining was easy to dismiss as an aberration soon to be rectified by rising sales. Q: Can there be growth, inflation and all the other good things that governments have been promising while raw materials prices are tanking? The answer is probably no, which means the other numbers — GDP, deficits, interest rates — will have to be adjusted to conform with the commodities complex rather than the other way around. Which in turn means that the world’s governments are about to panic. Expect some Hail Marys in 2016, including sharply negative interest rates, a serious war on cash to facilitate those negative rates, and a return to QE in the US, where the idea of raising interest rates will be quickly abandoned. Since these policies are just more aggressive versions of what has already failed, they’re unlikely to stop the carnage, leaving the developed world with one final weapon against global deflation: a coordinated devaluation of all major currencies, probably against gold. Though it’s taking a really long time, the currency war continues to play out according to Jim Rickards’ script. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Fed, Rand Paul, and the Next Financial Crisis Posted: 21 Jul 2015 12:27 PM PDT This post The Fed, Rand Paul, and the Next Financial Crisis appeared first on Daily Reckoning. Editor's Note: Peter Schiff spoke with Matt Welch of Reason.tv, where he discussed the dollar, his support of Rand Paul, and his argument that we are already living in another stock bubble (this video is part of a series — if you haven’t watched part one, make sure you do). To watch the clip, click the play button in the video above.

The post The Fed, Rand Paul, and the Next Financial Crisis appeared first on Daily Reckoning.      | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| William Binney : Surveillance State Is Corrupting American Way Of Life Posted: 21 Jul 2015 12:00 PM PDT Alex Jones talks with NSA whistle blower William Binney about how the NSA with all of its surveillance is corrupting and destroying the very essence of humanity itself. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The China Bubble About To Burst? Watch Out America You are next ! -- Richard Wolff Posted: 21 Jul 2015 11:30 AM PDT Economist Dr. Richard Wolff, Democracy At Work joins Thom. China - the world's second biggest economy - recently saw its stock market plummet 30 percent in a month. Does this mean that next big economic crisis is right around the corner? The Financial Armageddon Economic Collapse Blog... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A Strong Dollar, Not Weak Gold, Story Posted: 21 Jul 2015 11:29 AM PDT This post A Strong Dollar, Not Weak Gold, Story appeared first on Daily Reckoning. I joined Bloomberg’s Alix Steel, Joe Wiesenthal and Jeffries’ Chief Market Strategist, David Zervos, yesterday afternoon. We discussed the Fed’s path forward, the strong dollar, gold prices, deflation and some U.S. history. Is the strong U.S. dollar responsible for the gold price? Click the play button on the video above to find out in my latest interview.

Best Regards, Jim Rickards P.S. Be sure to sign up for The Daily Reckoning — a free and entertaining look at the world of finance and politics. The articles you find here on our website are only a snippet of what you receive in The Daily Reckoning email edition. Click here now to sign up for FREE to see what you're missing. The post A Strong Dollar, Not Weak Gold, Story appeared first on Daily Reckoning.    | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| John Stossel - Recycling Stupidity Posted: 21 Jul 2015 11:00 AM PDT Stossel examines the wisdom of recycling programs and the sustainability movement. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many more [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Peter Schiff : The Civil War Was Not About Slavery - We're All Slaves Now Posted: 21 Jul 2015 10:30 AM PDT Peter Schiff`s comments on the economy, stock markets, politics and gold. Schiff is the renowned writer of the bestseller Crash Proof: How to Profit from the Coming Economic Collapse. Visit the new website Schiff On The Markets for exclusive content. Peter Schiff is a well-known commentator... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Onboard the TransCanada Railroad Posted: 21 Jul 2015 10:22 AM PDT This post Onboard the TransCanada Railroad appeared first on Daily Reckoning. Onboard the TransCanada – "Have you people ever run a train before?" Sarcasm seemed appropriate. It wasn't plainly crass or vulgar. Just mildly insulting. The book we were later given on the train explained that the VIA Rail Canada – Canada's passenger rail system – was inspired by Amtrak in the U.S. This is a little like getting on a cruise line that said it drew inspiration from the Titanic. By then we hardly needed any explanation. Our tickets said we were to be in Prestige Class for the journey from Toronto to Vancouver. But there was nothing prestigious about the way we were handled. After waiting 10 hours to board, we were invited to drag our bags along a quarter mile of platform to get to the prestige car. By the time we got there, we expected to be asked to bend over so the staff could whack us with a board. The train – scheduled to leave at 10 p.m. on Saturday night – did not push off until 9 a.m. the following day. We had gotten a call advising us get to the station "no later than 6 p.m." so we wouldn't miss it! We fulfilled our part of the deal. Alas, the Canuck Amtrak failed. Rescheduled for 7 a.m., it was then rescheduled again for 7:30 a.m… and then 8 a.m… "The train got in late to the station. Then we had to wait to find a new engineer," was the word we got when we asked about it. "People have been running trains for a long time," we began a lecture. "There is nothing unpredictable about it. A train is a big object. You should know where it is. Then it's a simple matter to compute when it will arrive. You know – distance divided by speed…" We felt an elbow. It was Elizabeth telling us to knock it off. Tempted to feel sorry for ourselves, instead we said a prayer for the poor economy-class travelers. They would probably be chained to their seats and whipped with barbed wire. But now we are rolling along. Too bad about the Wi-Fi – it doesn't work. Nor does the mini-fridge. And the train has been backing up as much as it has been going forward. But, heck, the staff are friendly… and the scenery is magnificent. Word comes this morning that Greek banks have reopened. Bank customers have been separated from their money for three weeks. Even now, they are allowed only brief conjugal visits. They may take out only up to €420 ($456) a week. The Greek stock market has reopened, too. But without Wi-Fi, we have not been able to get an update. Greek stocks, as you might imagine, have gotten beaten harder than a traveler on the Canadian train system. They are down as much as 95% from their 2007 high. The average stock listed in Athens sells for a little more than two times earnings. Many sell for barely a single year's cash flow. It's not for us to know at what price Greek stocks should trade. But the Greeks have been around a long time. They're probably not going away. And neither are the companies headquartered there. And some of the biggest payoffs in the investment world have come from putting money into places no one else wanted to go. It's the beaten down, despised, sad sack of a market that has the greatest potential: It has nowhere to go but up. If you had invested in the Turkish stock market in 1988, for example, today your investment would show a 1,188,047% gain. Every dollar invested, in other words, would be worth more than $11,000. Back in 1988, Argentina was a mess, too. If you had put your money there, you'd have a 39,297,300% gain. Had you invested $10,000, you'd now have $392,973,000. But the drama isn't over in Greece. Poor Alexis Tsipras is stuck. On the one side is the hard place: Many in his coalition government are refusing to go along with the deal he just made. Heads are rolling as a result. On the other side are the rocks of Northern Europe – especially Germany. And they are proving treacherous, too. Tsipras's Syriza government could be history in a few weeks. There'll be new elections… more negotiations… more cans… more kicks… and more absurdities. It is amazing how much nonsense is published on the subject. The mainstream press has turned it into a simpleton's version of the kids' movie A Bug's Life – a struggle between Greek grasshoppers and German ants. Readers are expected to take sides – either for the poor Greeks or against them. Most economists – most prominently Paul Krugman and Thomas Piketty – weigh in on the side of the Greeks. They urge Germany to give the grasshoppers a break – more time… more money… and more rope. They believe Northern European "austerity" has doomed the Greek economy to and endless depression. But the whole show is silly. The Greeks aren't going to start acting like ants. They aren't going to pay back old loans… or new ones. And lending more money to people who already owe more than they can ever hope to repay is never going to help an ailing economy. Regards, Bill Bonner P.S. I originally posted this article at The Dairy of a Rogue Economist, right here. The post Onboard the TransCanada Railroad appeared first on Daily Reckoning.    | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold Hammered “Unprecedented Attack†Posted: 21 Jul 2015 08:18 AM PDT - Gold market comes under “unprecedented attack” – Telegraph – “Sharp drop bore similarities to bear raids by Chinese funds” – FT - Paper contracts for 57 tonnes of gold dumped onto market in two minutes - Gold still holding up in euros, Canadian dollar and other currencies - Very negative sentiment towards gold signals close to bottom - Physical gold still vital financial insurance despite simplistic anti gold narrative | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 21 Jul 2015 08:06 AM PDT This post Fun With Numbers appeared first on Daily Reckoning. Today's Pfennig for your thoughts… Good day, and a Tom terrific Tuesday to you! Well, no fireworks this morning in gold — like yesterday’s major whacking. No 5 tonnes sales on the SGE this morning, and no 7,600 short contracts on the COMEX. I had a dear reader send me a note yesterday, asking me who bought the 5 tonnes of gold that were sold, since there always has to be a buyer and a seller. Good question! And that, my friends, is the problem as I see it with gold — it’s not transparent in its trading. Which is something that I pointed out in yesterday’s missive on the Chinese gold announcement. The Chinese didn’t include their purchases of gold, which they didn’t want to be public. So, looky there! Without the market moving trades, gold is up $10 this morning. Hmmm… Would that be a bone the price manipulators are throwing us to make us forget yesterday happened? Sure appears that way to me! The dollar overall is a bit softer this morning, and not swinging its mighty hammer. The currencies for the most part have a small gain and there are no Fed members scheduled to speak today, and raise everyone’s hopes that interest rates are rising to support the dollar, nor is there any data to support the dollar today. So we could see this drifting go on the rest of the day… Well, for the second consecutive day, the New Zealand dollar/kiwi is the best performing currency overnight. I’m told by a trader friend in New Zealand that this is the continuation of a short squeeze that began the night before, after PM Key made the comments about how kiwi had dropped more than expected, and that the economy was still strong. I do have to remind you that the Reserve Bank of New Zealand (RBNZ) meets tomorrow night (Thursday morning for them) and most economists believe that the RBNZ will cut their OCR (Official Cash Rate) by 25 basis points (1/4%). So, all this euphoria in kiwi the past two nights could very well be wiped out in one fell swoop by the RBNZ tomorrow night. Across the Tasman, the Aussie dollar (A$) isn’t faring as well as its kissin’ cousin, kiwi. The A$ is flat to up a small bit this morning, just like yesterday, as the pull from kiwi is strong and overcoming what was said in the Reserve Bank of Australia’s (RBA) last meeting minutes. Things like, “The A$ is still too strong, and growth has probably slowed in the last quarter.” And to follow that up, RBA Gov. Stevens will be speaking this evening in Sydney. We will see 2nd QTR GDP print in Australia today, and right now, it is expected to rise 0.8% vs. 0.2% the previous QTR, and year on year to rise to 1.7% vs. 1.3%… I don’t see those numbers “slowing down” as the RBA suggested in their meeting minutes, but they’re closer to the action than me. HA! A currency that I don’t talk about much, because there’s not a lot to talk about — the Mexican peso — is touching a 16 handle this morning. In 1998, I was in Cancun, Mexico, and the peso was 10. I have to say that the President that took over a couple of years ago, with much promise and renewed hope for the Mexican economy, has failed miserably. But then how did he know that the price of oil would drop like it did, thus reducing the revenue for the government-owned oil sector? But you can’t place all the blame on the drop in the price of oil, here. And besides, one of the President’s (Nieto) reforms was to go public with the oil sector, so the revenue would have been reduced to tax receipts any way. The euro is a bit stronger this morning than yesterday morning, but it’s like removing a bucket of sand from the beach. Nobody notices. And apparently the Greek debacle still hasn’t gone away for now, as the Greek Parliament will vote tomorrow on civil procedures and bank resolution directive. In other things going on in Greece, the Greece government is working on a moratorium for foreclosures of private residences, and pension reforms and a whole host of other things that have to be worked out per their agreement. I found it interesting last week that friend, Bill Bonner, from the Diary of a Rogue Economist letter, said that he “wasn’t buying the Greek Austerity Myth.” You can always depend on Bill to look at things differently. As everyone is looking at Greece’s inability to pay their loans, Bill says well, they aren’t going to carry through the austerity measures anyway! The Chinese renminbi hasn’t been allowed to appreciate for a week now, but last night’s weaker move was very small. Two ticks. WOW! Why even bother?

I did want to mention that we are observing a 10 year anniversary for the renminbi. Yes, it’s been 10 years since the Peoples Bank of China (PBOC) announced that they were dropping the peg to the U.S. dollar, revaluing the renminbi upward by 2%, and that the renminbi would now be pegged to a basket of currencies. No one ever really knew the true identity of the currencies in the basket, but most observers believed that the basket consisted of the SDR (special drawing rights) currencies of the dollar, yen, euro, and pound. I find it now to be quite interesting that the Chinese thought to peg their currency against the SDR currencies 10 years ago. For 10 years later, they are optimistic that the renminbi will be added to the SDR currencies by the IMF in October. The Chinese weren’t that good at seeing 10 years into the future were they? Well, you can either think that they are that good, or that it was just dumb luck. I think I’ll choose what’s behind door #1. Let’s go back 10 years and see what’s happened in China in the past 10 years: 1. The economy is 5 times larger than it was in 2005… 2. …and has surpassed Japan and Germany to become the 2nd most used currency for trade finance. 3. The stock market has opened up to foreign investors 4. The bond market has opened up around the world 5. More currency swaps have been signed 6. The renminbi has appreciated 34% in the 10 years since the drop of the peg And then a final observance, the Chinese are making big strides toward a floating currency system for the renminbi, and making good progress in my opinion. You know, come to think of it, could it be this year? Think about that for a minute. It was 1995 when China first pegged the renminbi to the dollar. 10 years later in 2005, the Chinese dropped the peg to the dollar and pegged the renminbi to a basket of currencies. And 10 years later? Interesting don’t you agree? Well, we’re getting into the dog days of summer not only for baseball, but for the currencies. I can tell you that historically, this time of year going into and through August, is a very slow time for the currencies and metals given that most traders in Europe go on vacation. And looky here, that’s what I’m doing! But I’m no longer a trader. But I still act like one, and I’m going on vacation! But the most important thing here is to recognize that this will be a slow period for the currencies and maybe even the metals. Well, the U.S. data cupboard is bare again today, but they do have something for us to kick around later this morning. First let me set this up. Those of you who have been keeping score know all too well how badly the U.S. Industrial Production and Capacity Utilization reports have been this year. Well, today, the U.S. accountants get to make revisions to those weak numbers. That’s right, this is officially, “Revisions to U.S. Industrial Production and Capacity Utilization, Day.” So, we all know how weak those reports have been so far this year, so guess what the revision will tell us? Go ahead, you don’t have to wait for the actual print of revisions to tell you. They’ll find a way to revise them upward, that’s a given, right? If at first you don’t succeed, try again, right? Isn’t that what the U.S. government did for GDP last year? They didn’t like the results of the weak GDP, so they found a way to goose it higher? I call it Fun With Numbers! And I said above that gold was up $10 this morning. A bone, I call it. And regarding the whacking that gold took yesterday that started with the relatively low total of gold reserves that China said they had, compared to what observers that count the SGE withdrawals and production numbers thought China had, I saw this quote… David Marsh, from the monetary forum OMFIF, said, “China would risk unsettling the world gold market if it revealed bullion reserves of 2,000 or 3,000 tonnes. This might be interpreted as an unfriendly move against the dollar at a ‘delicate time.'” I received this from the GATA Folks. And I thank Ed Steer for making that happen for me. I want to make certain everyone knows that Ed is well, and still posting a daily letter on metals. You can find Ed here. Here’s Tocqueville Asset Management’s senior portfolio manager, John Hathaway, as he writes: We and others have commented at length about the contradictions between the markets for paper (synthetic) and physical gold. The declining price of paper gold quotes in NY and London doesn’t square with worldwide physical flows that reflect demand far in excess of mine production. It appears to us that gold positions traded in London and New York among bullion banks, high-frequency traders, hedge funds, and commodity traders constitute highly levered derivatives with only distant and notional relationships to the physical substance. The power of synthetic gold markets (COMEX in New York and over-the-counter in London, in conjunction with the London Bullion Market Association fix) to determine gold prices could start to ebb as physical gold migrates to Asian financial centers. A bit of history is instructive here: The collapse of the 1960s Gold Pool, the aforementioned secret and collusive effort by seven central banks to keep a lid on the gold price, preceded a most difficult decade for financial assets. A lesson to be learned from the 1960s is the unpredictability of government actions, their inherently anti-free-market nature, and the unintended consequences that can arise from them. The Gold Pool was, in retrospect, a clumsy attempt by Western democracies to disguise the deteriorating fundamentals of the U.S. dollar stemming from the Vietnam War, rising inflation, and the weakening balance of payments. The dollar had been pegged to gold at $35/ounce since the end of World War II, a number that proved too low in light of the changing fiscal realities for U.S. sovereign credit caused by the escalation of the Vietnam War and the introduction of large scale welfare policies under the umbrella of the Johnson administration’s ‘Great Society’ initiative. In retrospect, the scheme was clumsy because the manipulation of the gold price was accomplished by the exchange of physical gold for dollars held by foreign creditors who saw the writing on the wall. The objective of the Gold Pool was to disguise reality. In the long run, that price-suppression scheme did not work. The failure of the Gold Pool of course was resolved by the suspension of dollar/gold convertibility in 1971. When free-market gold trading resumed in 1974, the gold price rose by nearly 20 fold over the next eight years. Chuck again. Love those history lessons when it comes to this stuff, because you know what they say about how if you don’t learn from history you’re doomed to repeat it. I love these guys that have just about everything to lose that come out and talk about the distortions in the pricing of gold. You’ve just gotta love ’em! That’s it for today. I hope you have a Tom Terrific Tuesday. Regards, Chuck Butler P.S. The Daily Pfennig is first published everyday, right here. Editor's Note: Be sure to sign up for The Daily Reckoning — a free and entertaining look at the world of finance and politics. The articles you find here on our website are only a snippet of what you receive in The Daily Reckoning email edition. Click here now to sign up for FREE to see what you're missing. The post Fun With Numbers appeared first on Daily Reckoning.    | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold: Breakdown Or Simple Overshoot? Posted: 21 Jul 2015 08:01 AM PDT Graceland Update | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Here’s How to Profit from the Death of King Coal Posted: 21 Jul 2015 08:00 AM PDT This post Here’s How to Profit from the Death of King Coal appeared first on Daily Reckoning. If you’re a tree-hugging, granola-munching greenie with a carbon footprint the size of a walnut, I’ve got great news for you… King Coal’s reign of terror is finally over! The black, sooty stuff is finally going the way of the dodo bird. And even better, you’re about to see how you can snap up some quick double-digit gains as you get ready to dance on King Coal’s grave… There’s no fighting it any longer. Thanks to waves of new regulations and a push for cleaner energy sources, coal’s had it. It’s not even the top source of electrical power in the United States anymore… “For the first time ever, natural gas trumped coal as the top source of electric power generation in the U.S. In April, roughly 31 percent of electric power generation came from natural gas, whereas coal accounted for 30 percent, according to a recent SNL Energy report,” CNBC explains. “It’s a dramatic difference from April 2010, when coal accounted for 44 percent of the mix and natural gas just 22 percent.’ That’s atrocious news for coal–a commodity we’ve tried time and again to play every time it’s attempted to bounce over the past couple of years. With no luck… Coal’s just been one of the worst investments out there. One of the main reasons? Investors believe the government’s been trying to kill it off in favor of greener alternative energy. And they’re right… Last year, Obama’s Environmental Protection Agency announced power plants must reduce their emissions of carbon dioxide 30% by 2030. It was a declaration of war on coal — and the last straw for investors. But just when it looked like things couldn’t get any worse for the stuff, prices started plunging once again. Coal plants were shuttered. And demand from China tanked. Here’s the result of the carnage: Brutal… And it doesn’t look like anyone can save King Coal. Heck, I thought coal would catch a break back in the fall after the Republicans nabbed the Senate. But no. Even though it generates a significant portion of this country’s energy, coal’s definitely become one ugly investment. I just can’t see any opportunity to make a buck here… On the other hand…there is some serious growth potential in other emerging energy sources… Alternative energies like wind and solar are popping up all over the place. Wind is responsible for a little over 4% of our electricity generation — and solar about 0.25 percent. But it won’t stay that way for long… Just look at all the movers and shakers in the solar industry right now. The cost of solar power generation and battery storage is falling faster than I can type. In fact, Tesla’s chief technology officer just told Forbes that “battery costs will fall faster than expected, and the same for the demand for energy storage equipment that will be paired with solar panels. The combination will create a steady flow of electricity that is cheaper than energy from fossil fuel-based power plants.” So let’s wash the soot off our hands and instead shine some sunlight on quality solar stocks… and a great place to start is with the Guggenheim Solar ETF (TAN: NYSE). This fund holds a portfolio of solar companies in different weights, including many of our favorites. It's a great way to play the field without putting all the chips down on one company. Right now, TAN has been moving lower over the last couple of months, off frothy highs around $50, which gives you a nice entry point for a rebound as solar grabs market share from coal and other fossil fuels. Greg Guenthner P.S. Ever wonder how you can make a lot of money from oil without owning a well? Or whether or not you should buy gold and silver? Or is fracking just a flash in the pan? Get insight, insider scoops and actionable investment tips twice a week with Daily Resource Hunter? Just click here for a FREE subscription! The post Here’s How to Profit from the Death of King Coal appeared first on Daily Reckoning.    | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 21 Jul 2015 05:41 AM PDT Bloomberg puts together lots of opinions (none of them positive) about the recent plunge in the gold price and broader weakness in the natural resource sector. One Gina Rinehart, Australia’s commodity queen and richest woman, has been smarting, losing nearly $20 billion in net worth recently, according to this story at the Telegraph. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shamed FIFA President Sepp Blatter Showered in Dollar Bills by Lee Nelson Posted: 21 Jul 2015 05:25 AM PDT FIFA BOSS MONEY SHOWER - Shamed FIFA President Sepp Blatter Showered in Dollar Bills by Lee Nelson FIFA BOSS MONEY SHOWER - Shamed FIFA President Sepp Blatter Showered in Dollar Bills by Lee Nelson Sepp Blatter's first official press conference since announcing he is stepping down as... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 21 Jul 2015 05:17 AM PDT MUST READS Commodities crash could turn Australia into a new Greece – Telegraph Gold Leads Commodities 'Mess' That Has Investors Smarting – Bloomberg Is Gold a Stupid Pet Rock or a Bedrock Asset? – GoldSilverWorlds Liquidity deficit speeds up record Shanghai gold rout – Mineweb Bloomberg Commodity Index Falls To Lowest Point Since 2002 – Confounded Interest Puerto Rico Says Services [...] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold and Silver: The Final Capitulation Commences Posted: 21 Jul 2015 03:11 AM PDT The first 10 years of the bull market in gold was in hindsight plain sailing allowing us to generate profits by sticking with the trend. Alas all bull markets come to an end and so it did in 2011 when gold peaked at $1900/oz. Silver, despite having numerous industrial uses also felt the draft and fell dramatically along with the mining sector which lost approximately 70% of its value during a 3 year period of pure carnage. This pattern of falling stock prices interrupted by sudden price hikes has characterized the precious metals sector for the last three years or so. Unfortunately the bounces were rarely of the same magnitude of the preceding falls in prices and so we have witnessed the Gold Bugs Index, the HUI, fall from a high of 630 to a close today of 113, recording a drop of some 80% in the value of these stocks. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Is Gold a Stupid "Pet Rock" or a Bedrock Asset? Posted: 21 Jul 2015 02:51 AM PDT Greece defaulted at the end of June, and metals investors expected higher prices in July. What we expected isn’t what we got. It isn’t the first or last time markets surprised investors. Do lower spot prices mean precious metals are failing as a safe-haven investment? | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Are Gold Investors Finally Capitulating? Posted: 21 Jul 2015 02:41 AM PDT Sprott Asset Management’s Rick Rule is one of the smartest guys in the resource investing world — and one of the most reasonable — which has made his interviews of the past few years a little disconcerting. Along with the obligatory positive thoughts on the long-term value of gold and silver and the resulting bright future for the best precious metals miners, he always points out that the sector hasn’t yet endured a capitulation, where everyone just gives up and sells at any price, tanking prices and setting the stage for the next bull market. |

There were whiffs of panic selling in gold on Monday, which normally happens within days of the metal forming a short- to intermediate-term low, but it says nothing about its long-term prospects.

There were whiffs of panic selling in gold on Monday, which normally happens within days of the metal forming a short- to intermediate-term low, but it says nothing about its long-term prospects.

The euro against the USD

The euro against the USD

| You are subscribed to email updates from Save Your ASSets First To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment