If you are going to celebrate something, shouldn't you at least know what you are celebrating? Submitted by Michael Snyder, The Economic Collapse Blog: Most people that celebrate Halloween have absolutely no idea what they are actually celebrating. Even though approximately 70 percent of Americans will participate in Halloween festivities once again this […]

Stop Thanking Me for My Service… Submitted by Michael Krieger, Liberty Blitzkrieg: Starbucks Chairman Howard Schultz has said of the upcoming Concert for Valor: "The post-9/11 years have brought us the longest period of sustained warfare in our nation's history. The less than one percent of Americans who volunteered to serve during this time have […]

As promised to you, the crooked bankers continue with their criminal ways with a MASSIVE RAID on gold and silver on the week of options expiry. Let's head immediately to see the major data points for today: Submitted by Harvey Organ: Gold: $1198.10 down $26.20Silver: $16.39 down 83 cents In the access market 5:15 pm: Gold $1199.00silver […]

Since 1985, U.S. college costs have surged by about 500 percent, and tuition fees keep rising. In Germany, they’ve done the opposite.

The country’s universities have been tuition-free since the beginning of October, when Lower Saxony became the last state to scrap the fees. Tuition rates were always low in Germany, but now the German government fully funds the education of its citizens — and even of foreigners.

What might interest potential university students in the United States is that Germany offers some programs in English — and it’s not the only country. Let’s take a look at the surprising — and very cheap — alternatives to pricey American college degrees.

Germany

Americans can earn a German undergraduate or graduate degree without speaking a word of German and without having to pay a single dollar of tuition fees: About 900 undergraduate or graduate degrees are offered exclusively in English, with courses ranging from engineering to social sciences.

Finland

This northern European country charges no tuition fees, and it offers a large number of university programs in English. However, the Finnish government amiably reminds interested foreigners that they “are expected to independently cover all everyday living expenses.” In other words: Finland will finance your education, but not your afternoon coffee break.

France

There are at least 76 English-language undergraduate programs in France, but many are offered by private universities and are expensive. Many more graduate-level courses, however, are designed for English-speaking students, and one out of every three French doctoral degrees is awarded to a foreign student. “It is no longer needed to be fluent in French to study in France,” according to the government agency Campus France.

Sweden

This Scandinavian country is among the world’s wealthiest, and its beautiful landscape beckons. It also offers some of the world’s most cost-efficient college degrees. More than 300 listed programs in 35 universities are taught in English. However, only Ph.D programs are tuition-free.

Norway

Norwegian universities do not charge tuition fees for international students. The Norwegian higher education system is similar to the one in the United States: Class sizes are small and professors are easily approachable. Many Norwegian universities offer programs taught in English.

Slovenia

About 150 English programs are available, and foreign nationals only pay an insignificant registration fee when they enroll.

Brazil

Some Brazilian courses are taught in English, and state universities charge only minor registration fees. Times Higher Education ranks two Brazilian universities among the world’s top 400: the University of Sao Paulo and the State University of Campinas. However, Brazil might be better suited for exchange students seeking a cultural experience rather than a degree.

That excellent information (more in the above link) is from Washington Post foreign affairs writer Rick Noack.

I believe it’s near-crazy to pay $30,000 (or far more) in the U.S. for what can be had in Europe for free. Eventually costs will crash in the U.S. for the simple reason, they must. Online education ensures that outcome.

Last week, we argued that the underperformance of the gold miners during gold's rebound was a bad sign. Since then, the miners have plunged to new lows while gold appears to be at the doorstep of a major breakdown below $1180.

When the White House didn't like her reporting, it would make clear where the real power lay. A flack would send a blistering e-mail to her boss, David Rhodes, CBS News' president — and Rhodes's brother Ben, a top national security advisor to President Obama. Submitted by Michael Krieger, Liberty Blitzkrieg: Journalists should be dark, […]

It appears that TPTB do not wish to allow retail investors to take advantage of today’s historic gold and silver take-down as gold has been smashed to new lows of $1160 breaking through the triple bottom at $1180, with silver plunging to $15.61, as the cartel hit SDBullion with a DDoS attack precisely as gold […]

It was the greatest investment mistake of all time… a cumulative loss of more than $200 billion.

It started out as a lie. Then it got worse. It got worse every year for 20 years. But even that lesson didn’t really stick. The same investor repeated these same mistakes again and again. The first mistake happened in 1965. The last one didn’t liquidate until 2001. That’s 36 years of making the same mistake.

As you know, in the Friday Digest, I do my best to show you the things I would most want to know if our roles were reversed. Over the years, I’ve produced hundreds of essays and free podcasts about the risks foolhardy investors take when they buy outlandishly expensive stocks.

We even track the most notably expensive shares – those with market capitalizations of more than $10 billion, that trade at a price-to-sales ratio of more than 10 times – in our Investment Advisory “Black List.” But carefully studying the career of investing legend Warren Buffett has taught me that buying very cheap stocks can be every bit as dangerous as buying very expensive ones.

I hope you’ll read today’s Digest a few times and discuss it with your friends. You have my permission to forward this along to anyone who might be interested. It has a few big surprises below. Some of the things you’ve been taught about value investing just aren’t true…

Let’s start with this fact… The investor I describe above – the one who lost $200 billion, who made the same basic investment error again and again – is Buffett. Yes, he’s widely admired as the greatest investor of all time. But he also made some of the biggest errors of all time, too.

As you’ll see, the core error that Buffett made several different times was getting caught in “value traps.” That same error, in at least three instances over 36 years, resulted in catastrophic losses. If you’ve ever lost money buying what you thought was a cheap (and therefore safe) stock, my bet is you have made the exact same error.

Today, I’ll show you the details of this particular kind of investment mistake and a few simple rules for permanently removing value traps from your investing. But as I always remind you, there is no such thing as teaching, there is only learning. So… only keep reading if you’re truly ready to think about what I’m saying below and reconsider much about what you’ve been taught about deep-value investing.

I’m currently writing a book about Buffett’s investing errors, called Warren’s Mistakes. Researching the book is easy: Buffett wrote continuously about his investing from the mid-1950s until today. Most (but not all) of his annual letters are available for free at www.berkshirehathaway.com.

I have copies of all of the others and a few personal letters that Buffett wrote to his investment partners over the years, too. In addition, a plethora of articles are available on all of Buffett’s deals from about 1970 onward in Fortune magazine, the Wall Street Journal, and Forbes. You can also find about a dozen different major books on his career. The best is The Snowball by Alice Schroeder.

Most people don’t know the most important and most basic fact of Buffett’s investment career. He began his career in the 1950s and early 1960s as a deep-value investor – someone who looked for stocks trading well below their net asset value (book value). His original strategy was to buy the cheapest stocks and find a way to liquidate his holdings at a fair market value. He used the metaphor of finding a cigar butt on the ground to describe his method in his 1989 letter to shareholders…

If you buy a stock at a sufficiently low price, there will usually be some hiccup in the fortunes of the business that gives you a chance to unload at a decent profit, even though the long-term performance of the business may be terrible. I call this the “cigar butt” approach to investing. A cigar butt found on the street that has only one puff left in it may not offer much of a smoke, but the “bargain purchase” will make that puff all profit.

However… all too often, this approach caused him lots of problems, especially as his operations grew in size and he began taking control of companies. After that point, his strategy proved to be far too cumbersome and risky. Selling the assets became difficult or even impossible. Again and again, he found himself “trapped” with low-quality assets that he couldn’t sell for any price.

Working with investors over the past 20 years, I’ve seen lots of people make huge mistakes buying expensive stocks, whether it was the Internet darlings of the late 1990s, real estate stocks in 2007, or today’s social-media stocks (which will crash soon enough).

It’s not difficult to learn why this happened and how to avoid expensive stocks… You just don’t buy anything that is wildly popular, a newly minted initial public offering (IPO), or trading at 50 times earnings. But learning how to avoid big investment mistakes in cheap stocks is a lot more difficult, as Buffett’s track record demonstrates. In many cases, these opportunities seem the safest… which is why they can be particularly deadly.

Let’s start with the big one…

In 1962, Buffett began buying shares in a beaten-down former industrial powerhouse called Berkshire Hathaway. The company, which once was among the largest businesses in New England, had been in decline since the end of World War II. Cheaper, non-union labor in the South and a slew of new innovations made the company’s mills obsolete.

By the time Buffett took control in 1964, the company’s previous nine years of operations saw revenues of more than $500 million… but an aggregate loss of $10 million. The business was no longer competitive in the market. Management responded by closing down mills, selling assets, and generating cash for its balance sheet. The result was a company with far greater assets on its books ($22 million) than its share price… and a lot of cash. This attracted the attention of the Graham-and-Dodd deep-value crowd, including Buffett.

Buffett figured he could buy the stock safely because sooner or later, Berkshire Hathaway’s then-CEO (Seabury Stanton), whose family had owned and run the business for decades, would try to buy it back from him. That’s exactly what happened. In 1964, Buffett negotiated with Stanton to tender (sell) his shares back to the company. They verbally agreed on a price: $11.50 per share. But when the formal tender offer was published, the asking price was reduced by one-eighth of a point – to only 11 and three-eighths. What happened next was a disaster. As Buffett told CNBC…

If that letter had come through with 11 and a half, I would have tendered my stock. But this made me mad. So I went out and started buying the stock, and I bought control of the company and fired Mr. Stanton…

Buffett was now saddled with a failing textile maker. To escape the industry’s grim economics, he began to invest the company’s cash flows in businesses with better prospects. The first thing he bought was insurance company National Indemnity in 1967.

As you likely know, Buffett would continue to use Berkshire Hathaway as his main investment vehicle. He bought stakes in other high-quality businesses like insurance firm Geico, credit-card company American Express, soft-drink empire Coca-Cola, and dozens more. It was these investment decisions that have made him and his fellow shareholders roughly 20% a year since 1965.

But the situation raises an interesting question: Why didn’t Buffett simply borrow (or raise from investors) the capital he needed to buy the insurance companies and the other blue-chip stocks? Why did he fool around with Berkshire at all? Putting all of these great assets into Berkshire was a horrible mistake, because Berkshire continued to require a lot of capital. Says Buffett…

Berkshire Hathaway was carrying this anchor, all these textile assets… And for 20 years, I fought the textile business before I gave up. Instead of putting that money into the textile business originally, if we just started out with the insurance company, Berkshire would be worth twice as much as it is now – That was a $200 billion mistake.

Buffett got “trapped” owning a lousy business. He even doubled down on his bet by buying Waumbec Mills (another New England textile company) and merging it with Berkshire. In investment circles, this situation is known as a “value trap.” Plenty of great investors have seen their careers ruined because they took an oversized position in a stock that looked really cheap, but was actually worth a lot less than its balance sheet suggested.

Here’s the key concept to grasp: It didn’t matter how much money Buffett could afford to put into Berkshire. It didn’t matter what Berkshire management decided to try next. The economics of its entire industry were being decimated by low-cost competition. More than 250 different textile firms went bankrupt between 1980 and 1985.

As a result, every dollar Buffett put into Berkshire’s textile business was going to be a dollar lost – as Buffett found out when he tried to liquidate Berkshire’s assets at an auction held in early 1986, which he described in a shareholder letter soon after…

The equipment sold took up 750,000 square feet of factory space and was eminently usable. It originally cost us about $13 million… The equipment could have been purchased new for perhaps $30 to $50 million. Gross proceeds from our sale of this equipment came to $162,122… Relatively modern looms found no takers at $50. We finally sold them for scrap at $26 each, a sum less than removal costs

Buffett made at least three separate errors of this same kind…

In 1966, shortly after buying Berkshire, he partnered with Charlie Munger to buy the failing Baltimore department store Hochschild Kohn. They managed to sell it in 1969 and get back what they paid for it. They got lucky.

In 1993, much later in Buffett’s career, he bought Maine shoemaker Dexter Shoe, paying $433 million worth of Berkshire Hathaway shares. Buffett already owned HH Brown (another shoemaker) and knew Dexter was in trouble because of foreign competition… just like his original textile investments. Buffett says the Dexter deal ended up costing Berkshire $3.5 billion by the time he finally liquidated in 2001. As Buffett told Reuters news service in 2008, “Dexter is the worst deal that I’ve made.”

Buffett isn’t the only person who makes these mistakes. I’ve watched several great money managers make similar (and even bigger) mistakes, buying huge positions on stocks with marginal underlying businesses, where the company’s fundamentals are obviously in terminal decline. A few famous examples…

Bill Miller at Legg Mason’s Value Trust – once one of the largest and most respected mutual funds – bought 32 million shares of film manufacturer Kodak in 2000 and 2001, paying around $41 per share, long after the introduction of digital cameras. He held shares until 2011 – long after digital cameras were ubiquitous in cell phones. His fund lost more than $500 million.

O. Mason Hawkins, one of the most respected senior value-investment managers in the U.S. and founder of the Longleaf Value fund, began buying shares of carmaker General Motors in 1999 at $65 per share. He eventually held 44 million shares. This was after more than 30 consecutive years of declines in GM’s global market share and decades of losses in the car business. Plus, the company was being forced to maintain a “jobs bank” where it paid thousands of employees who didn’t work.

Hawkins held shares until August 2008, when it traded around $12 per share. On the eve of the global financial crisis, he took the proceeds of his GM share sale and invested in the company’s Series B convertible bonds, at one point owning one-third of the entire issue. These bonds were sold days before GM filed for bankruptcy at less than 20 cents on the dollar.

Bruce Berkowitz – once named one of investment-research company Morningstar’s money managers of the decade from 2000 to 2010 – began buying shares of retailer Sears Holdings in 2005 at more than $100 per share. As the company has closed locations and starved its stores of badly needed capital improvements, Berkowitz has added millions of shares to his position, mostly at prices above $100 per share. Now, with the company borrowing money from shareholders to avoid bankruptcy, he’s still buying. Berkowitz bought more than 3 million shares in the first quarter of 2014, at prices above $40. Today, the stock is trading around $27.

Writing in his 1989 shareholder letter, Buffett commented specifically on why these “value traps” usually don’t work out…

1. In a difficult business, no sooner is one problem solved than another surfaces – never is there just one cockroach in the kitchen.

2. Second, any initial advantage you secure [by buying at a very low price] will be quickly eroded by the low return that the business earns. Time is the friend of the wonderful business, the enemy of the mediocre.

3. Good jockeys will do well on good horses, but not on broken-down nags. When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.

How can you use these lessons in your own investing? Buffett says just to stick with the stuff that’s easy: “In both business and investments, it is usually far more profitable to simply stick with the easy and obvious than it is to resolve the difficult.”

That’s a lesson I should have remembered before I thought I could help turn Devon Energy around. Shares have now fallen more than 20% since I wrote my letter in July asking management to sell its oil-sands project before the price of oil fell, due to massive increases in supply. (We’ve “unlocked” a copy of the issue here.)

Here are a few good rules of thumb.

First, use a little common sense. Before you buy your next deep-value stock, ask yourself if it’s likely to turn out as well over the long term (10 years) as doing something “easy and obvious.”

Right now, you can buy shares of blue-chip consumer-products company Apple (AAPL) for around 10 times annual cash earnings. That’s reasonable for a well-managed company that has great brands (plenty of goodwill), and holds $180 billion in cash. Plus, activist investor Carl Icahn says Apple is worth twice as much as its share price is trading for today. One thing is for sure… a lot of people will still use iPhones, iMacs, and iPads a decade from now. They will continue to use Apple TV and iTunes to view, store, and manage their digital content.

That deep-value stock you’re thinking about buying might turn around. It might make you a lot of money. But is it really morelikely to outperform Apple over the next decade? I wouldn’t bet on it. Why do what’s hard when you can simply do what’s easy and obvious?

Second, learn to avoid – at all costs – any publicly traded company whose revenues have not increased over the last five years. If a business can’t grow over five years, there’s probably a good and obvious reason why… one that’s not going to change after you buy the stock.

Third, beware of companies writing off goodwill. “Goodwill” is the capitalized value of a company’s intangible assets – like its brands, customer base, and the relationships it uses to distribute its products. Goodwill is a critical asset, but it’s hard to measure. When goodwill is growing, it’s usually far more valuable than what’s represented on the balance sheet. But when goodwill is in decline, the opposite is often true.

The public’s relationship with brands is fickle. Sears at one time had a brand so strong that store openings were a triumph for local politicians and developers. Having a Sears in your town meant you were a “real place.” Today, having a Sears at your mall is a sign of doom. It means your retail center is most likely dangerous and deserted. What was once the company’s greatest asset – its strong reputation for merchandising and service – is now a significant liability.

The 12 companies listed below are not currently short-sell recommendations at Stansberry Research. But I suspect that they are “value traps.” These companies look cheap… but they are far more likely to cost investors huge money over the next few years than they are to turn into profitable investments. We will keep an eye on them for you and check in with these stocks from time to time. (Full disclosure: One of my analysts disagrees with me on one stock, Real Networks. He very well could be right.)

We’re being hit with a double-whammy: Wages are under deflationary pressure, and almost everything else is exposed to inflationary pressure.

As correspondent Mark G. observed in Globalization = Permanent Instability, it’s impossible to understand inflation and deflation now except in a global context.

Now that prices for commodities such as oil and grain are set on the global market, local surpluses don’t push prices down. If North America has record harvests of grain, on a national basis we’d expect prices to fall as local supply exceeds local demand.

But since grain is tradable, i.e. it can be shipped to other markets where demand and thus prices are much higher, the price in North America reflects supply and demand everywhere on the planet, not just in North America.

If we put ourselves in the shoes of a farmer or grain wholesaler, this is a boon: why sell your product for 1X locally, when it fetches 2X in other countries? You’d be crazy not to put it on a boat and get double the price elsewhere.

As the share of the economy exposed to digitization increases, so does the share of work that can be done anywhere on the planet. When work is digitized, it is effectively commoditized, meaning that it no longer matters who performs the work or where they live.

If people in countries with low wages can perform the work, why on Earth would you pay double to have high-wage people do the work? It makes no sense. Taking advantage of the differences in local pay scales is called labor arbitrage, as the employer is trading on (i.e. arbitraging) two sets of prices.

It’s not just labor that can be arbitraged: currency, interest rates, risk, environmental regulations, commodities–huge swaths of the global economy can be arbitraged.

The basic idea of the global carry trade is to borrow money cheaply in a currency that’s weakening and use the money to buy low-risk, high-yield assets in currencies that are gaining in relative value.

It’s a slam dunk arbitrage: not only does the trader earn an essentially free return (borrowing yen at 1%, for example, converting the yen to dollars and buying Treasury bonds paying 3%), but there is a bonus yield on the dollar strengthening against the yen: a two-fer return.

Global labor is in over-supply–one reason why wages in the U.S. have been declining in real terms, i.e. when inflation is factored in. The better description is purchasing power: how much can your paycheck buy?

Here is a chart reflecting the decline in purchasing power of U.S. earnings since 2006:

Courtesy of David Stockman, here is a chart of inflation (i.e. loss of purchasing power) since 2000:

Whatever isn’t tradable can skyrocket in cost because, well, it can–since there’s little competition in healthcare and school districts, both of which operate as quasi-monopolies, school administrators can skim $600,000 a year: Fired school leaders get big payouts:

A former Union City, CA superintendent took home more than $600,000 last year, making her the top earner on a new online database tracking salary and benefit information for California public school employees.

Since healthcare is only tradable at the margins, for example, medical tourism, where Americans travel abroad to take advantage of treatments that are 20% the cost of the same care in the U.S., healthcare costs can rise 500% when measured as a percentage of wages devoted to healthcare:

Note that this doesn’t mean that healthcare costs rose along with wages–it means a larger share of our earnings is going to healthcare than ever before. Other than a brief period in the 1990s when productivity gains drove wages higher, healthcare costs have risen faster than earnings every decade. The consequence is simple: the more of our earnings that go to healthcare, the less there is for savings, investments and other spending.

In a way, we’re being hit with a double-whammy: whatever can’t be traded, such as the local school district and hospital, can charge outrageous fees and pay insiders outrageous sums for gross incompetence, while whatever can be traded can go up in price based on demand and currency fluctuations elsewhere.

Meanwhile, as labor is in over-supply virtually everywhere, wages are declining when measured in purchasing power. Wages are under deflationary pressure, and almost everything else is exposed to inflationary pressure. No wonder we feel poorer: most of us are poorer.

The greenback, as illustrated by the USDX, has managed to poke through the chart resistance level at 87 in today's session. The overnight, surprise action by the Bank of Japan, has given currency traders a strong reason to hammer the Yen lower and they are doing exactly that.

The Euro is holding a bit better and is only down some .7% compared to the 2.5+% beating that the yen is taking, but both majors are down against the Dollar and that has enabled the greenback to finally better that tough chart level noted.

Essentially what we have is a currency, that was trading in a very broad range for the last two years that broke out of that range to the upside in September. The reason for the breakout was simple - investors and traders are convinced that is any of the Western industrialized nations ( and I am including Japan in this group ) was going to move higher on the interest rate front, it would be the US.

This is in spite of the clear statements by the Fed that they intend to keep interest rates low for a "considerable time".

The issue however is very clear - the ECB and the Bank of Japan were NOT going to move higher on rates. Neither was Canada or Australia, not with the price of commodities moving lower. In effect, the Dollar wins by default when it comes to the currency of choice for investors and traders in such an environment.

After the upside breakout on the chart, the Dollar has spent the last month consolidating its gains building a base from which to launch the next move higher. That appears to have finally taken place today with the BOJ move the catalyst.

At this point, a weekly CLOSE above 87, sets up a likely run at 89. As long as the Dollar is exhibiting such strength, gold has little chance of halting its slide lower.

I can add another comment to this... grain traders who are oblivious to these movements in the critical currency markets and are happily chasing grain and bean prices higher, are going to experience a lesson in global markets very soon that they will not forget.

With crusher margins at levels not seen in two months, and at levels which by any historical standard of comparison, are incredibly profitable, they will crush as many beans as they can get their hands upon and do it as fast as they possibly can. At some point, the supposed meal shortage is going to become a meal glut.

We are in a bottom for sure. How long will it last is anybody's guess- but silver stackers need not worry. This is only a question of how much fiat can you raise in order to purchase hard core, hold in your hands bullion to hold for a couple of years through the greatest worldwide total […]

Colorado and Oregon could soon become the first states in the nation to pass ballot initiatives mandating the labeling of food products containing genetically modified organisms. Earlier this year, Vermont became the first state to approve GMO labeling through the legislative process, but the decision is now being challenged in the courts. Leading corporations opposing […]

Stocks globally surged, while gold fell sharply today despite renewed irrational exuberance on hopes that the Bank of Japan's vastly increasing money printing will fill some of the gaps left by the apparent end of Federal Reserve bond buying.

We have been chronicling with some detail the regular weekly Commitment of Traders reports for some time in many of the markets that I choose to comment upon. In those comments, I have noted the positioning of some the LARGE speculative forces as being on the LONG SIDE of gold.

Here is a graphic of the condition ( or better - what WAS the condition ) of all those SPECULATIVE longs in the market.

Note the HUGE NUMBER: It currently stands at 241,792 if you include option positioning.

By the way, just for comparison's sake, the total number of SPECULATIVE SHORTS in the gold market is a trifling 134,381. As you can see, speculators have continued to be stubbornly long in the gold market despite the deteriorating chart pattern and despite the deteriorating fundamentals for gold. By the latter, I am speaking primarily of the surging US Dollar and the fact that commodity prices in general are falling right along with the TIPS spread which is indicating the sentiment that inflation is of no concern at this moment.

Here is the point in all this... an examination of the chart shows that approximately 55,000 of those new long positions put on in gold near the $1200 are all completely underwater. That is where this selling is coming from. Once the TRIPLE BOTTOM at $1180 failed ( remember the old trading adage that, "TRIPLE BOTTOMS RARELY HOLD" ), the sell stops were activated and out they came.

Bears have been licking their chops to get to those for some time now. Today, they got them. With that level being the last line of defense in the sand for the gold bulls, speculative forces are going to be aggressive in going after gold from the short side now, just like they had begun doing in the silver market for some time. The carnage might just be getting started.

Interestingly enough, at the moment I am typing these comments, gold is down 2.96% compared to the HUI being down 5.42%. Guess what - that HUI-gold ratio that I have been charting, noting that it has reached levels last seen 14 years ago in the year 2000, is still falling lower. Gold is therefore either going to continue to move lower or the HUI Is going to have to move higher. Gold is overvalued, even after its fall today, compared to the mining universe.

Either that, or as I said yesterday, many mining companies are finished.

In the first half of our new interview with Alasdair Macleod we discuss the November 30th Swiss gold referendum and what it might mean for the Bankster's central banking Ponzi scheme. We also discuss Majestic Silver CEO Keith Neumeyer's move to withhold physical silver sales – and his idea to form an OPEC-like mining cartel to […]

From Dr. Steve Sjuggerud, editor, True Wealth Systems:

Our company just performed an internal “audit” of our track records…

I didn’t know what the results would be.

After hundreds of hours invested, the audit team at Stansberry Research announced the results…

Two things stand out:

We delivered big gains for our readers… My True Wealth Systems letter has delivered a 27% compound annualized gain (since inception through the end of 2013).

We did it with more losers than you might think… Our “winning percentage” was only 44.4%.

I am proud of our performance so far… The overall result is excellent.

What is more interesting to me is how we got there. These two little facts tell the story:

The median gain on our winners was 43.7%.

The median loss on our losers was -6.8%.

That is how you make money.

What this shows is this: You don’t need to be right 100% of the time, or even 80% of the time…

What you need to do is simple: You need to make your winners bigger than your losers.

“Winning percentage” is not an important number to me… The important number is the dollar value on your portfolio statement. Is your portfolio value going up? A lot? Then good!

If your portfolio value is up – by a lot – then should it matter to you how you got there? What if you only “got it right” one out of three times? It shouldn’t matter.

I am happy being WRONG two out of three times – if my typical winner is 43.7% and my typical loser is negative 6.8%. I will take those “loser” odds any day.

So how do you end up with 43.7%-gain winners and 6.8%-loss losers? The most important thing you do is you cut your losses early. You use trailing stops. Also, you let your winners run.

Most individual investors that I know do exactly the opposite of this… They let their small losses turn into bigger ones, by waiting for them to recover.

Also, most investors take a small profit, never letting their winners fully bloom. Right now, in True Wealth Systems, we are sitting on a 270% profit in a position we recommended in 2012.

Are you willing to continue holding a position that you have a 270% profit in?

If not, you need to change your mindset… Here’s the correct mindset:

I am willing to concede many small battles… to win the war.

This isn’t war… this is investing. You NEED to be willing to have some casualties, in order to grow your portfolio.

You need to be willing to admit you might be wrong – probably more than half the time – in order to make the most money.

This is not rocket science. It’s basic math. If your losers are small, and your winners are big, you will do well. And you can do well even if you have twice as many losers as winners.

So please, change your mindset.

Don’t think you have to be right every time. Think about keeping your losers small, and allowing your winners to soar.

Then, maybe, you can end up with a compound annual gain of 27%-plus, like we achieved (through 2013, according to our audit) in True Wealth Systems.

P.S. The success we’ve had in True Wealth Systems isn’t just about cutting losses and letting winners run. It’s also about the complex computer systems we spent nearly $1 million building with the help of my friend and colleague Dr. Richard Smith. On top of that, we’ve found a new and exciting way to invest in the markets. Find out for yourself right here.

A bond market reversal will ultimately be the salvation of the gold price but not today. The yellow metal is under attack.

In today’s ‘Bart Chart,’ Bloomberg’s Mark Barton takes a look at gold as it pertains to the dollar, rising equities and tame inflation. He speaks on Bloomberg Television's ‘Countdown’…

The ‘trend is your friend’, until an epic reversal occurs… The Last Coin in the Silver Shield Banksters Collection: End of the Line- On a Long Enough Timeline, the Survival Rate Drops to Zero! Submitted by ETP: When events "happen," they happen in a directed way by the elite's mainstream media outlets. […]

Stocks globally surged, while gold fell sharply today despite renewed irrational exuberance on hopes that the Bank of Japan's vastly increasing money printing will fill some of the gaps left by the apparent end of Federal Reserve bond buying.

The BOJ decided to increase the pace at which it expands base money to a whopping 80 trillion yen ($726 billion) per year. Previously, the BOJ targeted an annual increase of 60 to 70 trillion yen.

The BOJ sailed into deeper uncharted monetary territory with the announcement that they would triple annual purchases of exchange-traded funds (ETFs) and Japanese real-estate investment trusts (REITS) to 3 trillion yen and 90 billion yen respectively.

The Nikkei surged 5% in minutes to a seven year high after the Bank of Japan decision, while gold fell.

These unprecedented monetary events remind us of the old English mapmakers who used to write on uncharted territories on their maps – "Here be Dragons".

The BOJ claimed the surprise action was due to concerns that a decline in oil prices would weigh on consumer prices and delay a shift in sentiment away from deflation.

BOJ Governor Haruhiko Kuroda portrayed the decision as a preemptive strike to the 'lost decade' economy, rather than an admission that his plan to reflate the long moribund economy has so far failed.

The prime reason for the extraordinary monetary policies is likely that the Japanese economy remains very weak and risks tipping over into a depression. Bankruptcies more than doubled to 214 in the first nine months of 2014 compared with the same period a year ago. Japan has introduced quantitative easing to stimulate the economy and to spur inflation. But it may backfire and lead to stagflation and in a worst case scenario a German 'Weimar' style hyperinflation.

The yen’s real effective exchange rate has dropped to its lowest level since 1982. With Japan easing likely to deepen, the yen may fall to an unprecedented level. Though the fall of the yen may promote exports – energy, food and raw material costs will rise, especially imports.

There has been much cheer leading of the Fed's announcement that QE is over this week. We have doubts whether this will be the case and believe that a new round of QE and deepening currency wars is inevitable.

The Fed is very unlikely to start actually withdrawing its stimulus, so its balance sheet will remain elevated and a source of risk. The Fed's 6 years of QE saw its balance sheet soar to $4.5 trillion. As one monetary expert insider and expert put it to me in an email overnight:

"Just think, the Fed’s balance sheet was $140 billion, comprised of short term T Bills, in 1980 and that was thought to be runaway expansionism." Most analysts are ignoring the fact that the Fed has leveraged itself to nearly 80 to 1 and is effectively insolvent. A mere 1.25% drop in the value of its assets will wipe out its capital base. A few other inconvenient truths being ignored by markets and market participants for now are the fact that: *The U.S. Total Debt to GDP ratio today is 340% and rising *The U.S. National Debt continues to rise and will surpass $18 trillion in the coming weeks *U.S. Unfunded Liabilities are estimated to be between $100 trillion and $200 trillion One of the dire consequences that many of us warned would result from global currency debasement was the creation of new and large asset bubbles. This is coming to pass.

The other dire consequences that many of us saw flowing from QE and global currency debasement – a sharp fall in the value of fiat currencies and hyperinflation – have not come to pass.

However, history shows that stagflation and hyperinflation can be slow in developing but then can occur very rapidly.

Once the inflation genie is out of the bottle – it is nigh impossible to contain as was seen throughout the western world in the stagflation of the 1970s and has been in inflationary events throughout history.

Given the current weakness what should gold owners do? Gold, in the short term, looks prone to further weakness. We could see gold test lows of $1,156 which is a 61.8% retracement of the move from the October 2008 low to the all-time high at $1,921. If clients are worried about their gold position and have short term commitments there are a number of ways to manage downside risk, which may be of interest, please call our office to discuss further..

See Essential Guide to Storing Gold and Silver In Switzerland here

MARKET UPDATE Today's AM fix was USD 1,173.25, EUR 933.45 and GBP 733.47 per ounce. Yesterday's AM fix was USD 1,205.75, EUR 958.09 and GBP 753.59 per ounce. Gold fell $12.50 or 1.03% to $1,198.90 per ounce yesterday and silver slid $0.58 or 3.4% to $16.49 per ounce.

Bullion for immediate delivery lost as much as 2.6% to $1,167.49, the lowest since July 2010 and looked vulnerable to further falls to $1,100/oz.

Gold in U.S. Dollars – 5 Days (Thomson Reuters)

Silver slid as much as 3% to $16.00 an ounce, the lowest since February 2010. Platinum fell 0.9% to $1,239.75 an ounce. Interestingly, palladium bucked the trend and rose 0.5% to $790 an ounce, after a six days of gains.

Gold fell below $1,200 an ounce as equities and bonds surged – even bonds from Italy to Portugal climbed.

Gold in U.S. Dollars – 10 Years (Thomson Reuters)

Gold is heading for a decline of 4.4% this week, the most since September 2013. The metal is also set for the first consecutive monthly loss in 2014. Silver is set for a fourth monthly decline that's the worst run since June 2013. An ounce of gold bought as much as 73.3154 ounces of silver today, the most since April 2009.

If the mooted end of QE in the U.S. is bearish for gold and silver, then it is also equally bearish if not more so for overvalued stock and bond markets. Yet, those markets saw far less volatile trading and many stock markets are back at multi month highs or indeed all time record highs.

The sharp move lower today took place in illiquid Asian markets, soon after the BOJ announcement of the extraordinary new money printing experiment in Japan. This news in itself should have seen gold bounce higher as it is very gold bullish. Instead, gold plummeted lower.

The move lower this week also took place against a backdrop of very high global coin and bar demand in recent weeks which would ordinarily have led to higher prices. It also comes at a time of heightened geopolitical and economic concerns and the emergence of the Ebola virus. Not to mention, the bullish "Save Our Swiss Gold" initiative which will continue for the next four weeks.

As we wrote yesterday, the sudden sharp selling of precious metals this week despite robust demand could be another example of manipulation. Central banks want equities and bonds higher and precious metals lower. The counter intuitive trading action has hallmarks of continuing manipulation of the gold and silver futures market.

Prudent money will continue to dollar cost average into coins and bars on price weakness.

Get Breaking News and Updates on the Gold Market Here

Radomski said that RSI indicator is not oversold, so gold can very well fall further. How low can gold go initially? At least to the previous October low or perhaps a bit more lower.

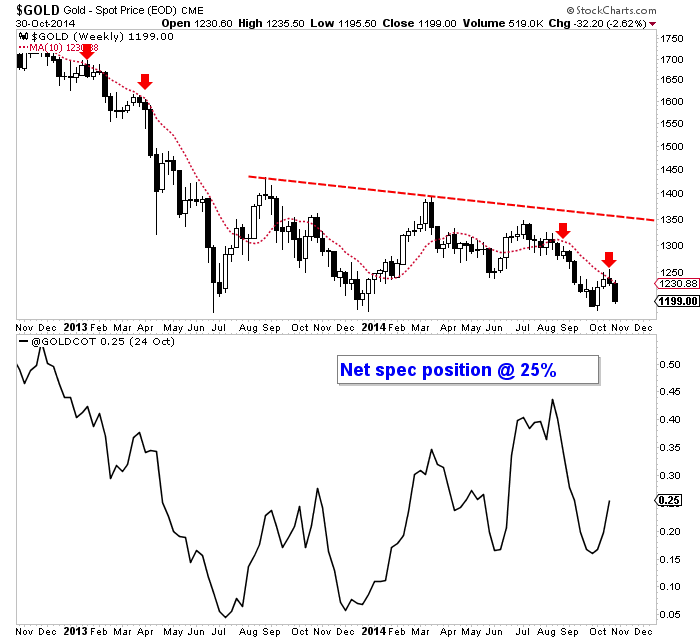

Last week we argued that the underperformance of the gold miners during Gold's rebound was a bad sign. Since then the miners have plunged to new lows while Gold appears to be at the doorstep of a major breakdown below $1180. It shouldn't be a surprise as it would simply be following the miners and Silver. The current bear market is getting very long in the tooth but it is not yet over. We see more losses ahead before a potential lifetime buying opportunity.

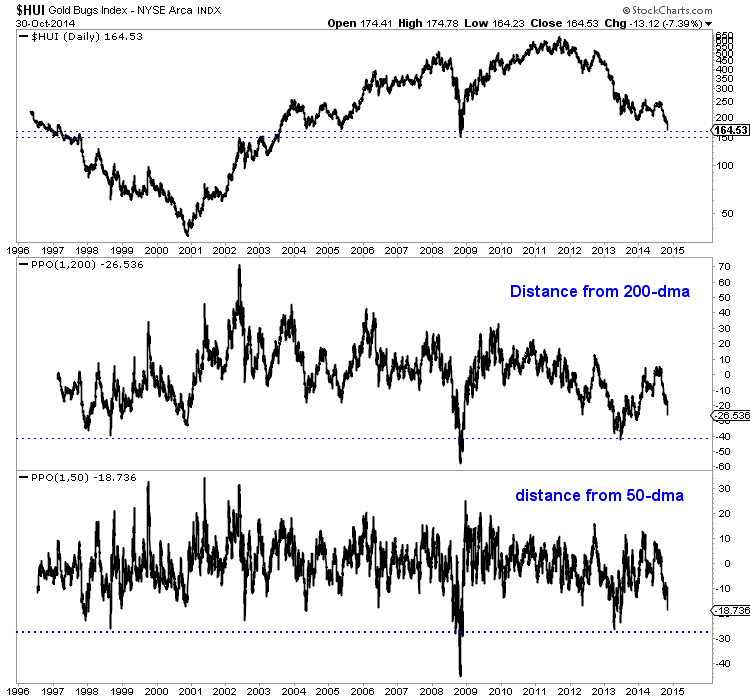

The HUI Gold Bugs Index is obviously very oversold but its not yet at strong support. It closed Thursday at 164 but should fall another 9% to support at 150. Currently the HUI is 26% below its 200-day exponential moving average and 19% below its 50-day moving average. The chart argues that those figures need to reach 40% and 27% before we deem the oversold condition extreme. If the HUI trades below 150 then it would mark an 11-year low. That is extreme!

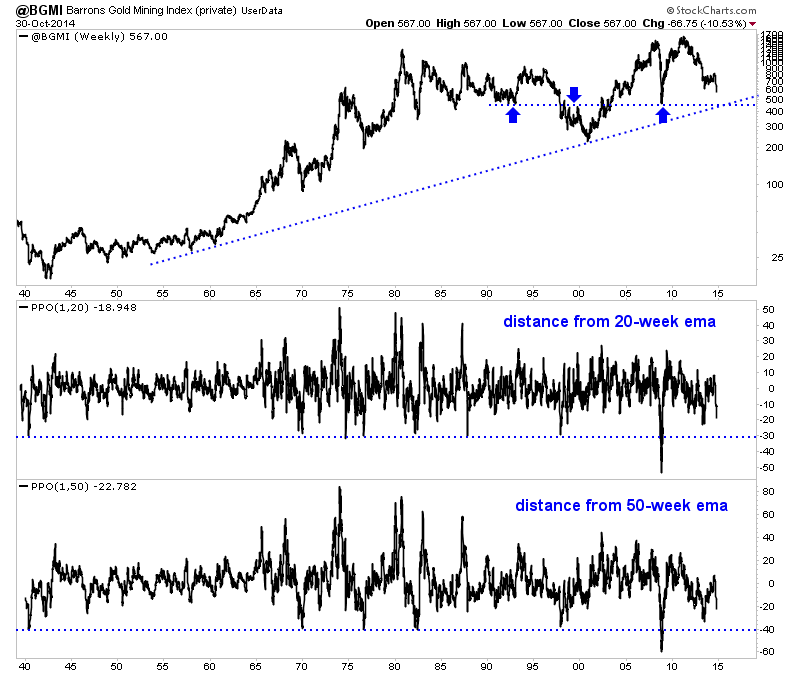

Nick Laird of ShareLynx provided me data from the Barron’s Gold Mining Index (BGMI) which I uploaded to stockcharts.com. This index dates back to 1938 and allows for greater historical perspective. Data is updated weekly so I had to estimate the current price. The HUI, XAU and GDX are all down 10% or 11% on the week so I calculated a 10.5% loss on the week which is a price of 567. Lateral support, which dates back to the early 1990s as well as trendline support that dates back 50 years provide a strong confluence of support in the mid 400s. That is roughly 20% downside.

Another reason to expect more downside is Gold hasn't even broken $1180 yet, though it may have by the time you read this. The price action has been textbook bearish. Gold failed to rally up to trendline resistance in the summer and then it declined in nine of twelve weeks. It rebounded for two weeks but quickly reversed at the 10-week moving average which is sloping down sharply. Also, the net speculative position in Gold as of a week ago was 25% of open interest. There are a fair amount of longs left to capitulate. Gold's downside support targets are $1080, $1040 and $1000.

We've been warning for several weeks of the near-term downside potential in precious metals. It is being realized but that does not mean its over. The miners plunged to new lows in recent days yet they are likely to move lower before a major turn. Our work above suggests a minimum of 9% downside potential and as much as 20%. Meanwhile, Gold could fall another 15% to strong support at $1000. Opportunities are coming but they are not here yet. We want to see Gold and gold stocks decline further so that they become extremely oversold as they reach major support levels. That is the combination that could produce a lifetime buying opportunity in the weeks or months ahead.Consider learning more about our premium service including a report on our top 5 stocks to buy at the coming bottom.

"Silver price is now back to where it was in the first quarter of 2010"

¤ Yesterday In Gold & Silver

The gold price wasn't allowed to do much in early Far East trading on their Thursday---and developed a negative bias around 1 p.m. Hong Kong time---and by the time JPMorgan et al were through, with the low tick coming at 11:30 a.m. EDT, they had gold down around fifteen bucks from it's Thursday close. It recovered a few dollars off that low by noon, but then chopped sideways for the remainder of New York trading session.

The high and low tick were recorded as $1,216.50 and $1,195.50 in the December contract.

Gold closed yesterday at $1,198.80 spot, down $12.80 from Thursday's close. Net volume was very high at 195,000 contracts.

The silver price didn't do much in Far East trading up until shortly before 2 p.m. Hong Kong time. At that point the HFT boyz and their algorithms showed up---and the rest, was they say, was history. The low tick was in at 11:15 a.m. EDT---and from there it bounced off that low a few times before rallying a bit. After 12:30 p.m., the price chopped sideways in a tight range until the 5:15 p.m. EDT close of electronic trading.

The high and low in silver were reported as $17.205 and $16.33 in the December contract, which was an intraday move of a hair over 5 percent.

Silver finished the Thursday session at $16.46 spot, down 63 cents from Thursday's close. That's a new low price for silver going back to March of 2010. Net volume was a whopping 74,000 contracts.

Platinum also ran into the same not-for-profit seller shortly before 2 p.m. in Hong Kong. It's low came minutes before 12 o'clock noon in New York. It rallied a few bucks from there before trading flat for the remainder of the Thursday session. Platinum was closed down 17 bucks.

The palladium price got smacked twice yesterday. The first time was at the New York open at 6 p.m. on Wednesday evening---and the second time was at the London p.m. gold fix on Thursday. Like platinum, JPMorgan et al set the low of the day just minutes before noon EDI---and the price didn't do much after that. Palladium was closed down 16 dollars on the day.

The dollar index closed at 85.99 late on Wednesday afternoon in New York---and then took three steps up to its 86.41 high tick, which came shortly after London opened on their Thursday. From there it quietly sold back to the 86.00 mark by 12:20 p.m. EDT. It gained some back by 2 p.m.---and then traded sideways into the close. The index finished the Thursday session at 86.18---up 19 basis points on the day.

Once again the gold shares got crushed, as the HUI closed lower by 7.44%---the biggest one-day decline that I can remember---and I can remember quite a lot. The HUI is down almost 12 percent in the last two trading days.

The silver equities fared better, but that's only a relative term in this situation, as Nick Laird's Intraday Silver Sentiment Index got hammered for another 5.65 percent.

The CME Daily Delivery Report for Day 1 of the November delivery month showed that 2 gold and 44 silver contracts were posted for delivery on Monday. In silver, the only short/issuer was Jefferies---and R.J. O'Brien and Canada's Scotiabank stopped 25 and 18 contracts respectively. The link to yesterday's Issuers and Stoppers Report is here.

As I said in yesterday's missive, barring any surprises, the November delivery month will be a yawner---and it's certainly lived up to its advanced billing.

The CME Preliminary Report for the Thursday trading session showed that November open interest declined by 207 contracts and now sits at only 67 contracts left---minus the two in the previous paragraph. In silver, the November open interest is now down to 164 contracts, minus the 44 posted for delivery tomorrow that were mentioned above.

There was another withdrawal from GLD yesterday, as an authorized participant took out 38,449 troy ounces and, once again, there was no change in SLV.

Since there were no withdrawals or additions to SLV during the reporting week, which ended on Wednesday, there was no report from Joshua Gibbons yesterday.

For the second day in a row, there was no sales report from the U.S. Mint.

I'll certainly be interested if they update their sales report for today, which is the last business day of the month. If they don't, the sales report for Monday should be quite something, as the mint has now gotten into the practice of withholding sales at the end of the month if it pushes silver eagles sales for the current month, too high.

There was no gold received at the Comex-approved depositories on Wednesday, but 96,450.000 troy ounces were shipped out---and that amount is precisely 3,000 kilobars, probably heading to China. The link to that activity is here.

It was a very quiet day in silver, as nothing was received---and only 7,060 troy ounces were shipped out.

Nick Laird surprised me with the latest withdrawal from the Shanghai Gold Exchange for the week ending October 24. It was another very chunky amount, as 59.684 tonnes were reported withdrawn---and here's Nick's most excellent chart.

Once again I don't have a lot of stories for you today---but there are several in here that fall into the absolute must read category so I hope you can make time for them.

¤ Critical Reads

Q.E. central bankers deserve a medal for saving society

The final word on quantitative easing will have to wait for historians. As the US Federal Reserve winds down QE3 we can at least conclude that the experiment was a huge success for those countries that acted quickly and with decisive force.

Yet that is not the ultimate test. The sophisticated critique - to be distinguished from hyperinflation warnings and "hard money" bluster - is that QE contaminated the rest of the world in complicated ways and may have stored up a greater crisis for the future.

What we can conclude is that extreme QE enabled the US to weather the most drastic fiscal tightening since demobilisation after the Korean War, without falling back into recession. Much the same was true for Britain.

The Fed's $3.7 trillion of bond purchases did not drive up debt ratios, as often claimed. It reduced them.

Ambrose is a paid whore/mouthpiece for the 'establishment'---and will print whatever he's told to print. This should be kept in mind should you read this commentary posted on The Telegraph's Internet site at 9:00 p.m. GMT on Thursday evening. I thank Roy Stephens for his first offering in today's column.

The $75 trillion shadow hanging over the world

Global shadow banking assets rose to a record $75 trillion (£46.5 trillion) last year, new analysis shows.

The value of risky investment products, mortgage-backed securities and other non-bank entities increased by $5 trillion to $75 trillion in 2013, according to the Financial Stability Board (FSB).

Shadow banking, which is not constrained by bank regulation, now represents about 25pc of total financial assets - or roughly half of the global banking system. It is also equivalent to 120pc of global gross domestic product (GDP).

The FSB, which monitors and makes recommendations on financial stability issues, said that while non-bank lending complemented traditional channels by expanding access to credit, data inconsistencies together with the size of the system meant closer monitoring was warranted.

This commentary is also from The Telegraph. It was posted there at 4:01 p.m. GMT on their Friday afternoon---and I thank South African reader B.V. for sharing it with us.

Prosecutors Suspect Repeat Offenses on Wall Street

It would be the Wall Street equivalent of a parole violation: Just two years after avoiding prosecution for a variety of crimes, some of the world’s biggest banks are suspected of having broken their promises to behave.

A mixture of new issues and lingering problems could violate earlier settlements that imposed new practices and fines on the banks but stopped short of criminal charges, according to lawyers briefed on the cases. Prosecutors are exploring whether to strengthen the earlier deals, the lawyers said, or scrap them altogether and force the banks to plead guilty to a crime.

That effort, unfolding separately from a number of well-known investigations into Wall Street, has ensnared several giant banks and consulting firms that until now were thought to be in the clear.

As I and others have been saying for years, unless they start throwing people in jail---Wall Street and their bankster friends aren't going to change their behaviour. This essay appeared on The New York Times website at 3:56 p.m. EDT on Thursday---and I thank Phil Barlett for sending it along.

Russian lawmaker asks Nobel Committee to strip Obama of Peace Prize

A representative of the populist LDPR nationalist party claims in an official letter that the US President should be blamed for thousands of innocent people’s deaths and therefore cannot keep his 2009 Nobel Peace Prize.

“More and more international experts are calling Obama’s presidency dark times. The reason for that is the brutal policy that he is conducting all over the world, like Napoleon or Hitler had done before. But I want to warn Obama so that he pays more attention to history and understands that he can end up like Hitler,” MP Roman Khudyakov said in an interview with Izvestia daily.

The politician added that under Obama the United States participated in the “dirty war” in the Middle East, financed the armed conflict in Ukraine and violated international law by torturing suspected terrorists. All this makes the US President complicit in the violent deaths of several thousand innocent civilians and such a person cannot remain the holder of the Nobel Peace Prize, Khudyakov said.

I wholeheartedly agree, as he should never have been awarded the Peace Prize in the first place. This news item was posted on the Russia Today website at 9:50 a.m. Moscow time on their Thursday morning, which was 1:50 a.m. EDT. It's the second contribution of the day from Roy Stephens.

France denies warship delivery, as Russian bombers skirt E.U. airspace

France's controversial warship deal with Russia is hitting the headlines again, with a cacophony of statements and denials after a Russian minister published a French invitation to the hand-over ceremony.

Russian deputy prime minister Dmitry Rogozin on Wednesday (29 October) published a letter on his Twitter page by the French constructor of Mistral warships, supposedly inviting Russian authorities to the ceremony in St. Nazaire on 14 November.

He tweeted that the Russian state-owned arms company Rosoboronexport was invited for the delivery of one ship and for next steps on construction of the second one in the contract.

But a spokesperson of the constructor (DCNS) said a few hours later that the Mistral delivery has not yet been confirmed.

This news story, filed from Brussels, showed up on the euobserver.com Internet site at 9:56 a.m. Europe time yesterday morning---and it's also courtesy of Roy Stephens.

France on alert after mystery drones spotted over nuclear plants

France has launched an investigation into unidentified drones that have been spotted over nuclear plants operated by state-owned utility EDF, its interior minister said on Thursday.

Seven nuclear plants across the country were flown over by drones between Oct. 5 and Oct. 20, an EDF spokeswoman said, without any impact on the plants’ safety or functioning.

“There’s a judicial investigation under way, measures are being taken to know what these drones are and neutralise them,” Interior Minister Bernard Cazeneuve told France Info radio on Thursday, without specifying the measures.

The drone sightings may renew concerns about the safety of nuclear plants in France, the world’s most nuclear-reliant country with 58 reactors on 19 sites operated by EDF.

This news item appeared on the france24.com Internet site yesterday sometime---and it's the second offering of the day from reader B.V.

Has the E.U. lost the ability to enact sanctions?

The E.U. has had a rotten time trying to punch its weight on the international scene. Internal disagreements and treaty limitations mean it is little wonder that it is known as an economic giant but a political dwarf.

With the U.S. increasingly urging the E.U. to share the burden of keeping world order, the Union is finding out that the main mischief-maker is not some stubborn member state but one of its own institutions - the European Court of Justice.

The E.U.'s highest court has been busy unravelling the foreign agenda of the Union – by consistently overturning sanctions enacted by Brussels.

In its most recent ruling on 16 October, the court struck down anti-terrorism sanctions imposed on the Tamil Tigers in 2006, citing that the council’s decision to place the group on a list of terrorist organisations had been based on "imputations derived from the press and the Internet".

This euobserver.com story, filed from Brussels, put in an appearance on their website at 9:28 a.m. Europe time on their Thursday morning. The offerings from Roy just keep on coming.

Russia Agrees to Terms With Ukraine Over Gas Supply

Russia agreed to terms for restoring natural-gas exports to Ukraine, laying the groundwork to prevent residents going without heat as temperatures drop.

The gas negotiations, brokered by the European Union, came as pro-Russian rebels stepped up attacks on Kiev government forces. European leaders said they hoped the deal would help improve ties between the two countries.

“This breakthrough will not only make sure that Ukraine will have sufficient heating in the dead of the winter,” European Energy Commissioner Guenther Oettinger said at a news conference in Brussels last night. “It is also a contribution to the de-escalation between Russia and Ukraine.”

This Bloomberg article, co-filed from Kiev and Brussels, appeared on their Internet site at 7:32 p.m. Denver time on Thursday evening.

Vladimir Putin is the Leader of the Moral World — Paul Craig Roberts

Vladimir Putin’s remarks at the 11th meeting of the Valdai International Discussion Club are worth more than a link in my latest column. These are the remarks of a humanitarian political leader, the like of which the world has not seen in my lifetime. Compare Putin to the corrupt war criminal in the White House or to his puppets in office in Germany, UK, France, Japan, Canada, Australia, and you will see the difference between a criminal clique and a leader striving for a humane and livable world in which the interests of all peoples are respected.

In a sane Western society, Putin’s statements would have been reproduced in full and discussions organized with remarks from experts such as Stephen F. Cohen. Choruses of approval would have been heard on television and read in the print media. But, of course, nothing like this is possible in a country whose rulers claim that it is the “exceptional” and “indispensable” country with an extra-legal right to hegemony over the world. As far as Washington and its prostitute media, named “presstitutes” by the trends specialist Gerald Celente, are concerned, no country counts except Washington. “You are with us or against us,” which means “you are our vassals or our enemies.” This means that Washington has declared Russia, China, India, Brazil and other parts of South America, Iran, and South Africa to be enemies.

This is a big chunk of the world for a bankrupt country, hated by its vassal populations and many of its own subjects, that has not won a war since it defeated tiny Japan in 1945 by using nuclear weapons, the only use of such terrible weapons in world history.

No one can read Putin’s remarks without concluding that Putin is the leader of the world.

I'd been saving Putin's incredible Sochi speech for my Saturday column, but current events have forced my hand---and here it is in now. It's a long read, but an absolute must read, especially those who are serious students of the New Great Game. It was posted on Paul's website on Sunday and, not surprisingly, it's courtesy of Roy Stephens.

Putin to Western Elites: Play-Time is Over

Most people in the English-speaking parts of the world missed Putin's speech at the Valdai conference

First things first, Chinese gold demand is still very strong and it’s in a uptrend since July.

Apologies for my late reporting on the latest SGE withdrawals numbers – which are the best benchmark for Chinese gold demand. I was trying to figure out some details on gold trade rules between the mainland and the Shanghai Free Trade Zone. I still haven’t got confirmation, so will get back to it.

Chinese wholesale gold demand is at least 1541 metric tonnes year to date (inc. week 42 – until October 17). Shanghai Gold Exchange (SGE) withdrawals, as disclosed by the Chinese SGE reports, were 52 tonnes in week 42 and according to my estimates China has approximately net imported 991 tonnes year to date.

Perhaps the ones with a sharp eye noticed the title of this post claims Chinese gold demand is 1541 tonnes year to date, but in the chart above we read total SGE withdrawals stand at 1547 tonnes year to date. Do SGE withdrawals still equal Chinese wholesale gold demand? Not anymore, sadly.

This gold-related story is definitely worth reading---and it was posted on the Singapore website bullionstar.com yesterday sometime. I found it embedded in a GATA release.

How exactly is it possible that China acquired 10,000 metric tons of Gold since 2011? 2015 Silver Perth Kookaburras 25th Anniversary Limited Edition! Submitted by Chris Hamilton: Since August '11 to August of '14, China has decreased its holdings of US Treasury debt by <-$9> Billion (according to the most recent […]

This is an excerpt from the daily StockCharts.com newsletter to premium subscribers, which offers daily a detailed market analysis (recommended service).

The end of QE is bullish for the Dollar. Note that the Fed has ended QE and the European Central Bank (ECB) is threatening QE. This is Dollar bullish and Euro bearish. The US Dollar ETF (UUP) held its support zone and surged to affirm support at 22.60. The Euro Index ($XEU) held resistance and plunged below 127.

Gold gave us a little preview of the Fed policy statement by breaking down last week. This break held as GLD consolidated in the 118 area. GLD continued lower after the Fed announced the long awaited end to quantitative easing, which is Dollar bullish and bullion bearish. I will not move key resistance to 119.

The end of QE3 is official. What does this mean for markets and metals? The short answer: deflation ahead. The longer answer: almost all asset prices are about to come down (sharply) except the U.S. Dollar.

As we all know, the end of QE1 and QE2 resulted in volatility and unstable stock markets. The end of QE3 will most likely result in a short term extension of the bull run in stocks, after which volatility will start increasing and prices will come down systemetically. We believe that our call of early this year, when we predicted that 2014 Will Be The Year Of The Super Crash, will unfortunately come true. A crash is not an event but a process. Although we do not expect a full crash between now and December 31st of this year; we rather believe that the start of a very severe correction of at least 25% is imminent.

What does this imply for precious metals? First, the ongoing collapse of the gold miners does not bode well. The miners lead the metals in both directions. Unfortunately for gold bulls, the miners are now in the lead, which suggests that metals will follow their decline.

The following chart shows the performance of miners and metals since early June. Note how much lower miners and silver are trading since early September.

The strengthening U.S. Dollar will continue to put enormous pressure on gold and silver. We sense that it will result in a phase of capitulation. If there is one "good" thing about capitulation, it is that all sellers will get exhausted on (much) lower prices, leaving the marketplace with no sellers. Capitulation are rare events but, when they tend to progress very fast.

What would happen in such a scenario? In a matter of two weeks, prices could come down another 30% followed by a spike up. It would fit with the idea that stocks would rise a bit higher and then start coming down, resulting in money starting to flow towards the deeply oversold precious metals miners.

On top, in the physical market, if the Swiss gold referendum on November 30th would result in a "yes" vote, then we would have the first country after more than 4 decades returning to a gold standard. Additionally, in line with the gold rush of 2013 in Asia, (much) lower gold prices could probably make the physical market explode.

How likely is this scenario? Our belief is that it has a probability of 50%.

Longer term, we think that the Fed is underestimating deflation and that they will launch another "money printing" program in 2015 to push back deflation. Chances are high that it will feed inflation expectations which is beneficial for precious metals. The only question, in our view, is "when" not "if." That should become the driver for precious metals longer term.

No comments:

Post a Comment