Gold World News Flash |

- GDP - A Grossly Defective Product

- New Evidence Links Voting Machines And Clinton Foundation

- Let Crude Crash: US Oil Producers Are Hedging At Levels Not Seen Since 2007

- Full Speech: Donald Trump Rally in Springfield, OH 10/27/16

- DAILY NEWS BRIEF: VOTE RIGGING DOWN in TEXAS (and ALL US) & FIGHT to SAVE GLOBALISM

- DEUTSCHE BANK ON THE BRINK OF COLLAPSE ! Tough Times Ahead

- Hillary Clinton’s Helicopter Moneyman

- Election Is Everything But Over! - Hannity (FULL SHOW 10/26/2016)

- Jack The Ripper Declassified

- Gold Daily and Silver Weekly Charts - Capped Again at 1270 - Election Speculation

- Waking up in Hillary Clinton’s America

- BREAKING: CLINTON ‘FIXER’ GOES PUBLIC, CONNECTS HILLARY TO BRUTAL HOMICIDES

- URGENT: THOUSANDS OF AMERICANS TAKE A STAND AGAINST SOROS’ RIGGED ELECTION FOR HILLARY CLINTON

- Michael Moore In TrumpLand: The Last President of the United States

- Egon von Greyerz: Except in dollars, gold is near the 2011 highs

- Last chance to purchase GATA conference video discs and WSJ ad posters

- Alasdair Macleod: The vexed question of the dollar

- The vexed question of the dollar

- Must Watch!! Hillary Clinton tried to ban this video

- Donald Trump Has Won The 2016 Presidential Election

- Anonymous - Humanity's Now Is The Time

- Gold Chart of the Day

- The Dark Wave of Brexit Uncertainty

- This Is What Gold Does In A Currency Crisis, Brexit Edition

- “Chindia†Buying Gold on Dips, 20% Corrections Are “Non Eventsâ€

- Breaking News And Best Of The Web

- New PEA for Seabridge's KSM Is a Game-Changer

- Santacruz Silver Mining: The Market Still Doesn't Get It!

- Recommended Reading: 'When Money Dies: The Nightmare of the Weimar Collapse'

| GDP - A Grossly Defective Product Posted: 28 Oct 2016 12:30 AM PDT Submitted by Lance Roberts via RealInvestmentAdvice.com, GDP – The ProblemPaul Wallace recently penned for Reuters an interesting article entitled: “GDP Is A Grossly Defective Product.” In the article he states:

He is absolutely correct. Now, for all of you playing the home version of “Nail That GDP Number,” it was in 2013 the BEA decided that the economy was not growing fast enough and “tweaked” the GDP calculation and added in “intellectual property.” Those adjustments boosted GDP by some $500 million. There are inherent problems when you begin to adjust the “math” to “goal seek” a specific outcome. For example, the problem with adding “intellectual property” is that the cost of a new cancer drug treatment, a Hollywood movie or a new hit song is already included in the value of product brought to market. In other words, since production is what drives economic growth, that value is captured in the quarterly analysis of business investment, spending, etc. Furthermore, how does the BEA value “intellectual property” accurately and fairly across all industries and products? Some products like a cancer treatment have a much different “value” than a song. However, since those tweaks did not boost the economic growth rate as much as was hoped, the BEA went further in 2015 to adjust the calculation once again. To wit:

I am not a conspiracy theorist by any stretch. However, something strikes me as very odd about the frequency of adjusting the calculation to obtain better outcomes. The Federal Reserve understands, as we push into the eighth year of the current economic expansion, that we are likely closer to the next recession than not. The problem is the Fed has remained stuck at the zero bound for interest rates for far too long.

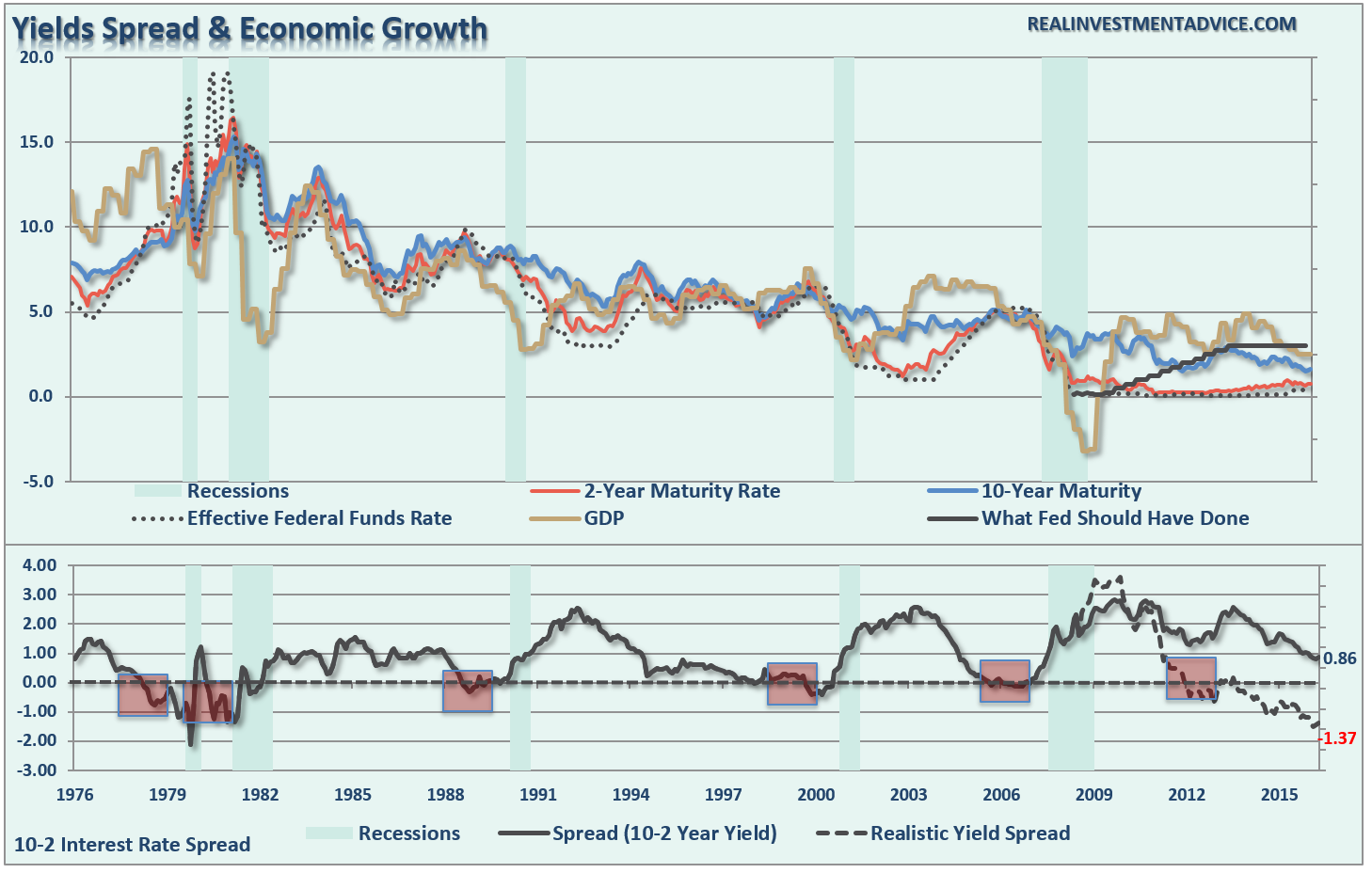

While QE programs have NOT been effective at creating organic economic growth, they were effective at boosting asset prices and providing an illusory wealth effect. This would have provided cover for the Federal Reserve to raise interest rates off of the zero bound giving them access to a more effective monetary policy tool in the future. The chart below shows the trajectory of rate increases the Fed should have undertaken given the support the expansion of their balance sheet would have provided.

Of course, the offset of using the liquidity push to raise rates and normalization of monetary policy early on would have limited asset price inflation to about one-half of its previous advance. Certainly not nearly as much fun for Wall Street. But alas, the Fed failed to use the recalculated and adjusted economic numbers, massive liquidity flows and rising asset prices to reload their policy tools. After two years of promises to hike rates in the face of stronger economic growth, each attempt has been consistently met with “weaker than expected” economic data. As we approach the end of the year, the Fed is once again determined to raise interest rates. However, is economic growth strengthening enough to support the hike? We can look at some alternative measures of the economy to answer that question.

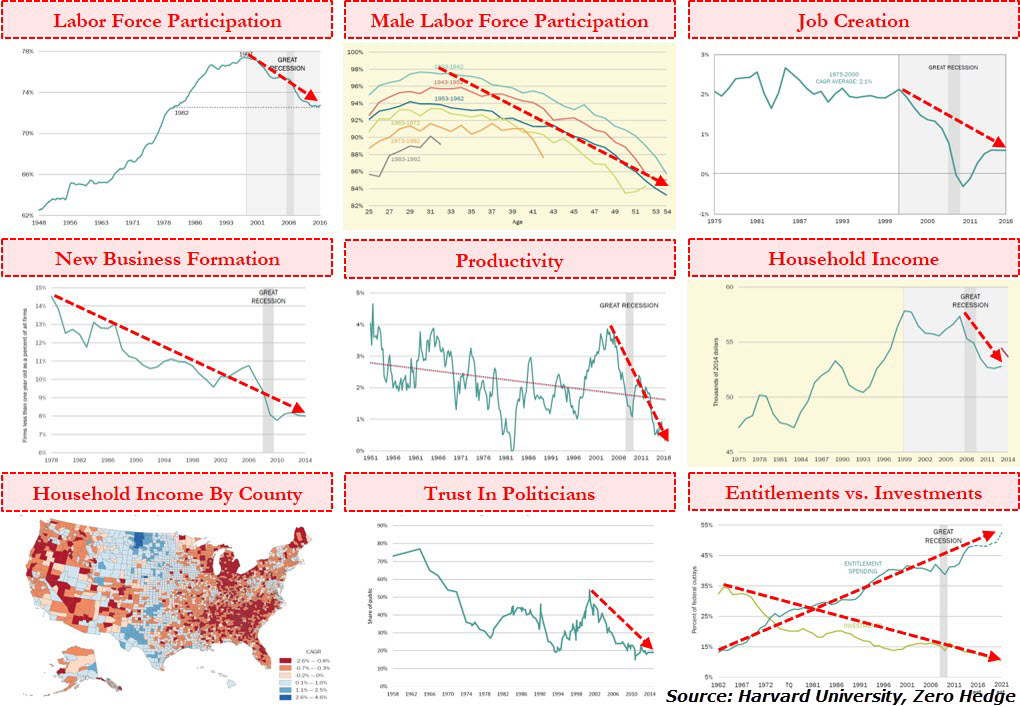

Alternative Measures Of Economic GrowthWhile the BEA is suggesting that it is simply “residual adjustments” lingering in the inventory and production-related data, that does not really explain the economic weakness in other areas of the economy. The chart collection below is from a recent Harvard study entitled “Problems Unsolved and a Nation Divided” which came to a couple of key conclusions (via ZeroHedge)

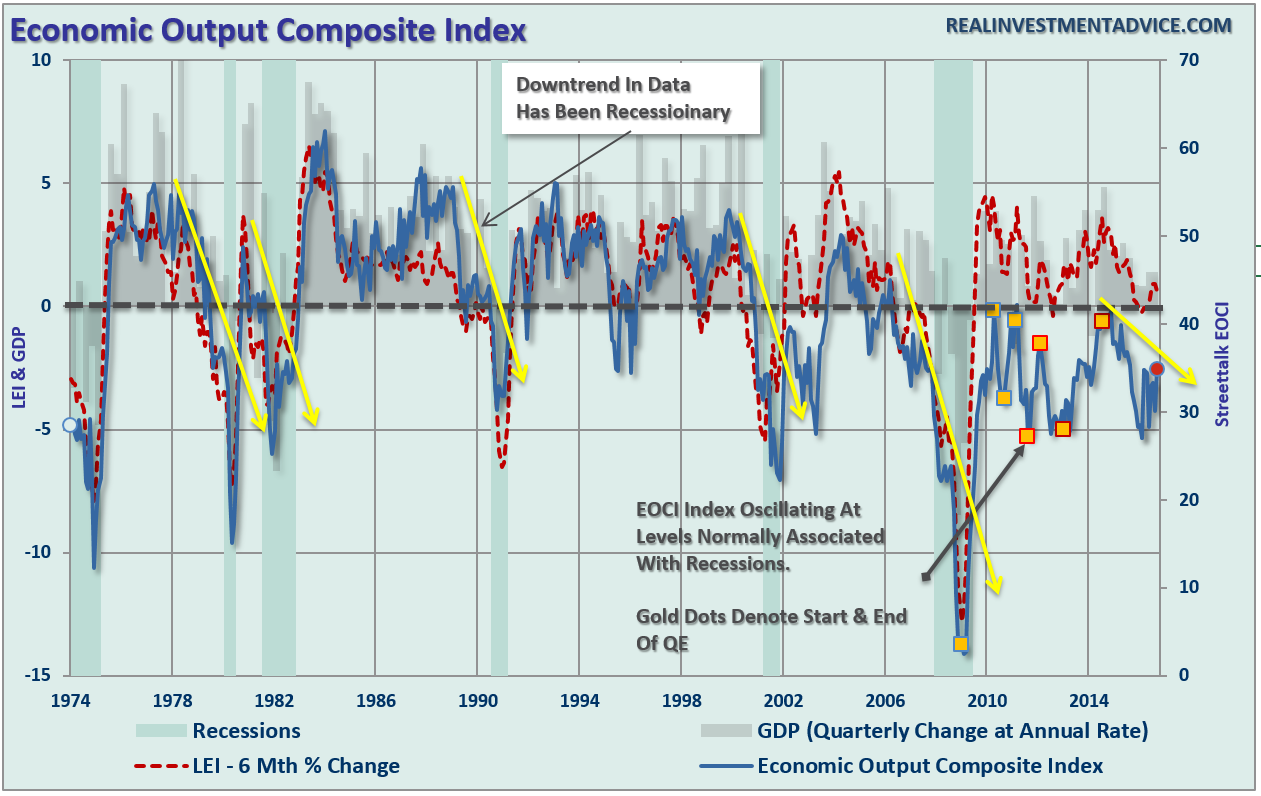

However, most importantly, the following chart is the best overall indicator of economic activity in the domestic economy. The Economic Output Composite Index (EOCI) is a compilation of broad economic inputs from manufacturing to small business to leading economic indicators. (read more on construction here)

Importantly, all of these indicators confirm that economic weakness is pervasive across a broad swath of the economy, and weakness in GDP growth in Q1 was likely more than just a “statistical anomaly.” Furthermore, despite the recent bounce in some of the economic data, it is important to note the entire complex of indicators still operate at levels more normally associated with weak economic environments versus expansionary ones. But it is here, as suggested above, that the Federal Reserve finds itself trapped. The Federal Reserve needs stronger economic growth to justify raising interest rates. After all, the reason the Fed tightens monetary policy to is SLOW economic growth to mitigate the potential of surging inflationary pressures. The problem currently, is that the Fed is discussing raising interest rates into an environment of low growth and inflation. So, what has happened historically when the Fed has raised interest rates in such an environment?

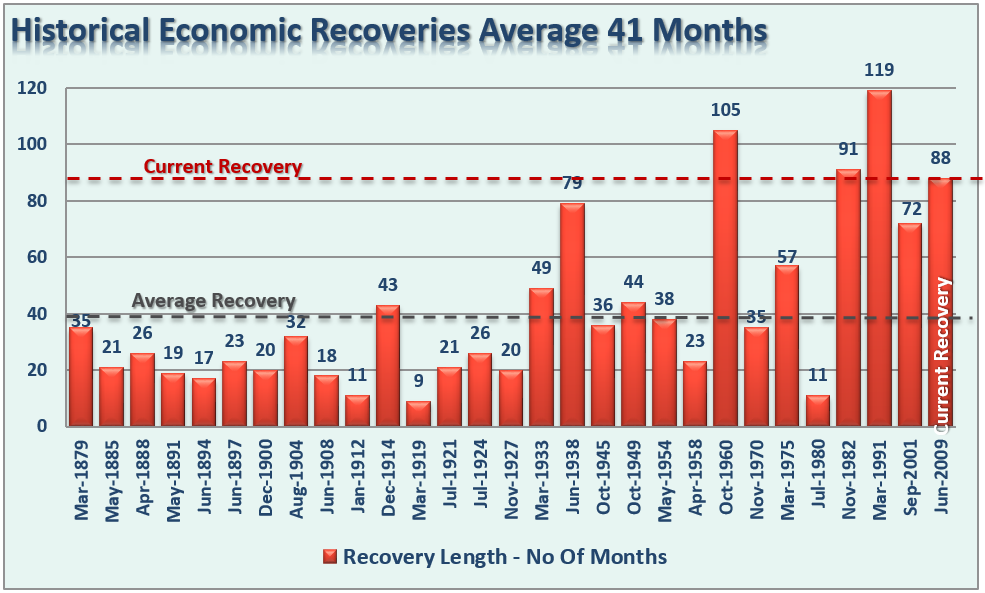

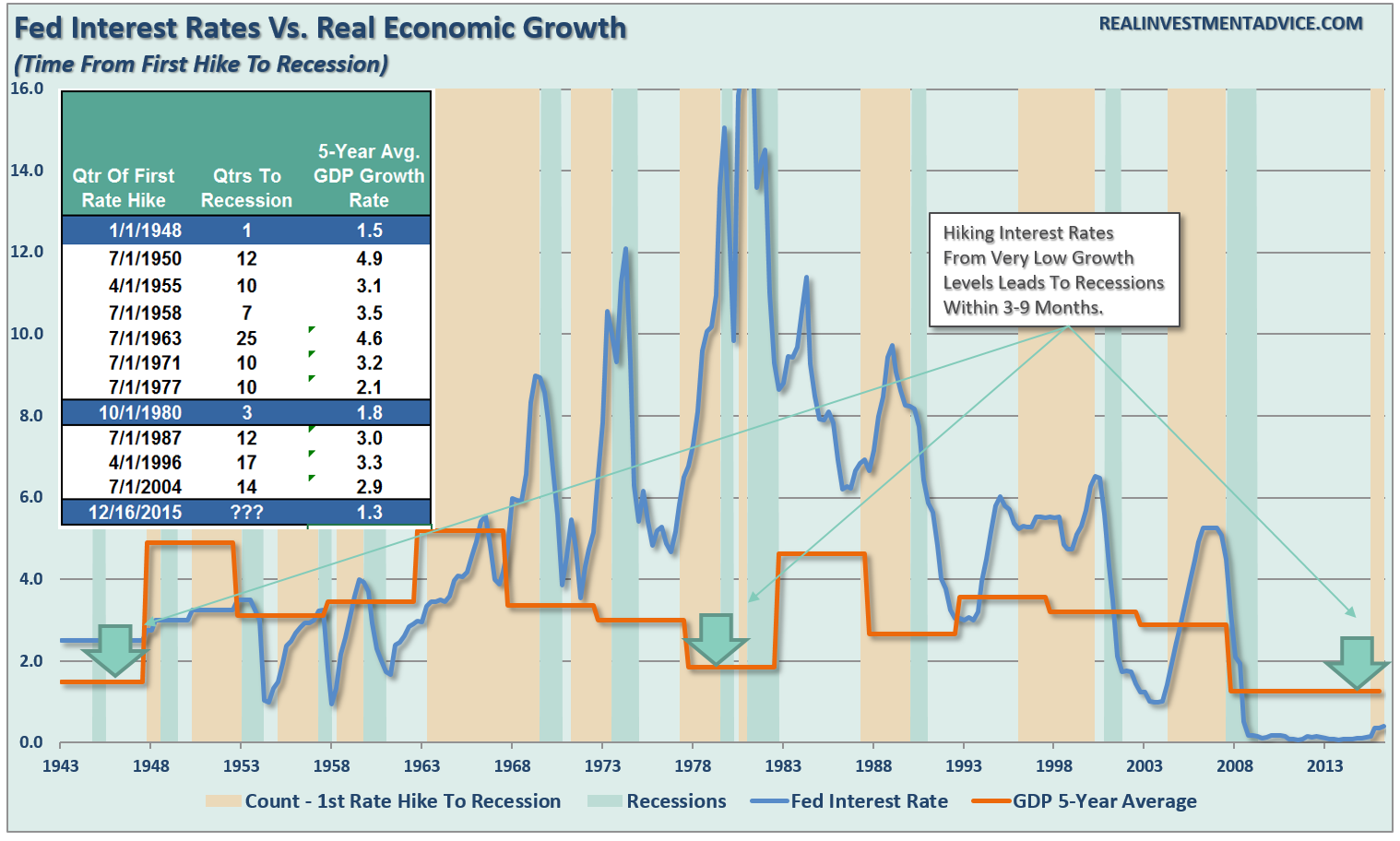

Interest Rates Versus Economic GrowthCurrently, employment and wage growth is extremely weak, 1-in-4 Americans are on Government subsidies, and the majority of American’s are living paycheck-to-paycheck. This is why Central Banks, globally, are aggressively monetizing debt to keep growth from stalling out. However, currently, many analysts and economist have increased the odds of the Fed hiking rates in December. The belief is that economic growth can continue to accelerate despite tighter monetary policy. The problem is most of the analysis overlooks the level of economic growth at the beginning of interest rate hikes. The Federal Reserve uses monetary policy tools to slow economic growth and ease inflationary pressures by tightening monetary supply. For the last eight years, the Federal Reserve has flooded the financial system to boost asset prices in hopes of spurring economic growth and inflation. As stated, outside of inflated asset prices, there is little evidence of real economic growth as witnessed by an average annual GDP growth rate of just 1.3% since 2008, which is the lowest in history….ever. The chart and table below compares real, inflation-adjusted, GDP to Federal Reserve interest rate levels. The gold vertical bars denote the quarter of the first rate hike to the beginning of the next rate decrease or onset of a recession.

If I look at the underlying data, which dates back to 1943, and calculate both the average and median for the entire span, I find:

However, note the GREEN arrows. There have only been TWO previous points in history where real economic growth was below 2% at the time of the first quarterly rate hike – 1948 and 1980. In 1948, the recession occurred ONE-quarter later and THREE-quarters following the first hike in 1980.The importance of this reflects the point made previously, the Federal Reserve lifts interest rates to slow economic growth and quell inflationary pressures. There is currently little evidence of inflationary pressures outside of financial asset prices and spiraling rent and health care costs. Therefore, rather than lifting rates when average real economic growth was at 3%, the Fed is now considering further rates hikes with growth at less than half that rate. Think about it this way. If it has historically taken 11 quarters to fall from an economic growth rate of 3% into recession, then it will take just 1/3rd of that time at a rate of 1%, or 3-4 quarters. This is historically consistent with previous economic cycles, as shown in the table to the left. This suggests there is much less wiggle room between the first rate hike, and the next recession, than currently believed. But then again, if you can just keep changing the data calculation to goal seek a better economic picture, then surely that is enough. Right? Might want to ask those 100 million on government welfare what they think. Just some things I am thinking about.

|

| New Evidence Links Voting Machines And Clinton Foundation Posted: 27 Oct 2016 08:45 PM PDT Submitted by Stefanie MacWilliams via PlanetFreeWill.com, Could these connections be enough to implicate the Clinton Foundation in the alleged early vote rigging in Texas? As usual, the internet has come through as the ultimate watchdog while the supposed safeguards of our democracy have failed. A Gab user by the name “Special Prosecutor Will Logan” has found some stunning information. Note: as Gab is a members only site, you’ll have to join to see his actual posts, but we included all pertinent information in the article.

According to OpenSecrets, the company who provided the alleged glitching voting machines is a subsidiary of The McCarthy Group. The McCarthy group is a major donor to the Clinton Foundation – apparently donating 200,000 dollars in 2007 – when it was the largest owner of United States voting machines. Or perhaps the 200,000 dollars went to paying Bill Clinton for speeches? Either way, it doesn’t look good. But there’s more. As the same user notes in this post, Dominion Voting Systems and The Clinton Foundation did a 2.25 million dollar charity initiative in developing nations together called the DELIAN Project. According to the project’s own website:

Of course, this is all speculation, and we are not making any claims of illegal activity by the Clinton Foundation. However, it presents a very troubling conflict of interest. Most Americans would certainly agree that voting machines should have zero connection to presidential candidates and their foundations. Consider the implications further abroad, as well. Could this DELIAN Project be designed to influence elections in developing nations? It can certainly be argued that electronic voting machines do not in fact provide an “improved electoral process” or provide “safer elections” Again, this is speculation. But we will be keeping an eye on this story if and when more information becomes available. |

| Let Crude Crash: US Oil Producers Are Hedging At Levels Not Seen Since 2007 Posted: 27 Oct 2016 06:58 PM PDT As warned here one month ago after the farcical OPEC meeting in Algiers, the cartel's latest jawboning ploy to keep prices artificially higher - if only for one more month - is fast falling apart. Just a few hours ago, Bloomberg reporter Daniel Kruger penned the following assessment of the situation:

That oil's upside is capped at this point is clear; in fact as both Goldman and Citi have warned, unless OPEC can come to a definitive and auditable agreement - no just another verbal can kicking - in which the member states, by which we mean almost entirely Saudi Arabia as most of the marginal producers are exempt or want to be, immediately curtail production, oil will promptly crash to $40 or below. But an even more amusing twist is that a plunge in oil prices may be just what US shale producers are waiting for. The reason for that is that while OPEC has been busy desperately jawboning oil higher, US producers have been thinking of the inevitable next step, oil's upcoming reacquaintance with gravity. As a result, as the EIA reports, the amount of WTI short positions held be producers and merchants is just shy of a decade high. According to a recent EIA report, short positions in West Texas Intermediate (WTI) crude oil futures contracts held by producers or merchants totaled more than 540,000 contracts as of October 11, 2016, the most since 2007, according to data from the U.S. Commodity Futures Trading Commission (CFTC). Banks have tightened lending standards for some energy companies as crude oil prices declined throughout 2014 and 2015, and some banks require producers to hedge against future price risk as a condition for lending.

Short positions of WTI futures increased at a faster pace than futures contracts of Brent (an international crude oil benchmark) since summer 2016, suggesting U.S. producers are able to drill for oil profitably in the $50 per barrel range. In the Crude Oil Markets Review section of the October Short-Term Energy Outlook (STEO), the U.S. Energy Information Administration (EIA) discusses an increase in U.S. onshore producers' capital expenditures that is contributing to rising drilling activity, which EIA projects will lead to an increase in U.S. onshore production by the second quarter of 2017.

* * * Which closes the circle of irony: almost exactly two years ago, Saudi Arabia set off a sequence of events with which it hoped to crush US shale producers and its high cost OPEC competitors. It succeeded partially and briefly, however now the remaining US shale companies are more efficient, restructured, have less debt, a far lower all-in cost of production; and - best of all - they will all make a killing the next time oil plunges, as it will once OPEC's hollow gambit is exposed. Meanwhile, the last shred of OPEC credibility will be crushed, the truly high cost oil exporters within OPEC will suffer sovereign defaults and social unrest, as will Saudi Arabia. The good news for Riyadh is that at least it got a $17.5 billion in fresh cash from a bunch of idiots who will never get repaid. We are curious just how long that cash will last the country which burned through $98 billion just last year, before the threat of social unrest and financial system collapse returns? Two months? Three? |

| Full Speech: Donald Trump Rally in Springfield, OH 10/27/16 Posted: 27 Oct 2016 05:30 PM PDT Thursday, October 27, 2016: Live stream coverage of the Donald J. Trump for President rally in Springfield, OH at the Champion Center Expo at 1:00 PM ET. LIVE Stream: Donald Trump Rally in Springfield, OH The Financial Armageddon Economic Collapse Blog tracks trends and forecasts ,... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| DAILY NEWS BRIEF: VOTE RIGGING DOWN in TEXAS (and ALL US) & FIGHT to SAVE GLOBALISM Posted: 27 Oct 2016 05:00 PM PDT DAILY NEWS BRIEF: VOTE RIGGING DOWN in TEXAS (and ALL US) & FIGHT to SAVE GLOBALISM The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many more [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| DEUTSCHE BANK ON THE BRINK OF COLLAPSE ! Tough Times Ahead Posted: 27 Oct 2016 04:00 PM PDT Bad news could spark a sell-off contagion that could lead to another global financial meltdown and a bail out by Angela Merkel's government despite her opposition to German state intervention.Analysts are warning that ultra high frequency trades triggered by machines could lead to a perfect... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| Hillary Clinton’s Helicopter Moneyman Posted: 27 Oct 2016 02:02 PM PDT This post Hillary Clinton’s Helicopter Moneyman appeared first on Daily Reckoning. You can see a nasty maneuver developing aboard the Hillary train that may end up being too clever by half. At least we can hope… I'm referring to the ill-disguised plan circulating among her policy inner circle to hand Janet Yellen a gold watch early so she can be swapped out for Helicopter Moneyman Larry Summers at the Fed. My response: Please, Hillary, bring it on! For one thing, whatever is left of the GOP congressional majority after Nov. 8 would have a field day with Larry Summers’ confirmation hearings. The man is one of the great jackasses of American public life — whose record of offending people and groups is Trumpian in scale. But the jackass part is actually his views on the supposed elixir of government debt. In the face of a $20 trillion public debt and what even the Congressional Budget Office (CBO) says will be another $10 trillion of red ink based on built-in policy over the next decade, Summers' “moar” debt proposition is so asinine that it is likely to incite even the fiscally irresponsible Senate GOP into a fit of outrage. We now have official confirmation that the federal deficit rose by 35% in 2016, to $589 billion. That’s bad enough in itself. But what’s worse is that it came at the end of an 87-month-old business cycle expansion when the budget should be balanced or in surplus. And in any event, it was a ringing announcement that the phony trend toward a lower annual deficit is now in the rearview mirror. Moreover, the actual public debt outstanding surged $1.7 trillion during the last two years, and will therefore coast past the $20 trillion mark soon after Inauguration Day. What’s remarkable about that awful milestone is that it's nearly double the $10.6 trillion level where the public debt stood in January 2009. That’s right. Barack Obama and the GOP Congress printed nearly as much debt in eight years as had the first 43 U.S. presidents during the preceding 240 years! But Professor Summers thinks what ails the U.S. economy has been insufficient rations of fiscal largess from Washington. You can’t make this stuff up. Here’s his latest emission of economic jabberwocky: [The] primary responsibility for addressing secular stagnation should rest with fiscal policy. An expansionary fiscal policy can reduce national savings, raise neutral real interest rates and stimulate growth… Other structural policies that would promote demand include steps to accelerate investments in renewable technologies that could replace fossil fuels and measures to raise the share of total income going to those with a high propensity to consume… Let’s see. The public debt was about $5 trillion at the turn of the century. So why didn’t that $15 trillion, or 4X gain, in barely a decade and a half crush the “secular stagnation” problem in its tracks? Apparently, the good professor thinks economic growth petered out anyway for lack of effort in the Imperial City. With a few more wars, even more expansive Obamacare and more prodigious emissions from the domestic pork barrels, we could have had a $30 trillion expansion of the public debt that has already been gifted to future generations. Whether that would have done the trick, Professor Summers never says. His ready answer is always that stimulus failed because it wasn’t big enough. He's dead wrong. It is rooted in the Keynesian proposition that we can borrow our way to prosperity. We can't. Summers and his fellow Keynesian swindlers will claim this is a brand-new scheme of “helicopter economics” under which the Fed’s prodigious outpouring of new money will go to the people rather than Wall Street. This will purportedly be achieved by huge increases in the nation’s already monumental public debt to fund spending increases and tax cuts, which would then be monetized dollar for dollar by the Fed. Folks, that’s not a new idea. It’s as old as the hills, and it's called monetary fraud. Regards, David Stockman Ed. Note: The most entertaining and informative 15-minute read of your day. That describes the free daily email edition of The Daily Reckoning. It breaks down the complex worlds of finance, politics and culture to bring you cutting-edge analysis of the day's most important events. In a way you're sure to find entertaining… even (ahem) risqué at times. Click here now to sign up for FREE. The post Hillary Clinton’s Helicopter Moneyman appeared first on Daily Reckoning. |

| Election Is Everything But Over! - Hannity (FULL SHOW 10/26/2016) Posted: 27 Oct 2016 02:00 PM PDT Hannity doesn't believe the liberal media and neither should you! Newt Gingrich stops by to discuss the latest revelations in the race between Donald Trump and Crooked Hillary Clinton. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists ,... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| Posted: 27 Oct 2016 01:30 PM PDT Who really was Jack The Ripper? Learn all that's worth knowing about the infamous serial killer. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| Gold Daily and Silver Weekly Charts - Capped Again at 1270 - Election Speculation Posted: 27 Oct 2016 01:23 PM PDT |

| Waking up in Hillary Clinton’s America Posted: 27 Oct 2016 12:53 PM PDT This post Waking up in Hillary Clinton's America appeared first on Daily Reckoning. This post first appeared on TomDispatch.com As this endless election limps toward its last days, while spiraling into a bizarre duel over vote-rigging accusations, a deep sigh is undoubtedly in order. The entire process has been an emotionally draining, frustration-inducing, rage-inflaming spectacle of repellent form over shallow substance. For many, the third debate evoked fatigue. More worrying, there was again no discussion of how to prevent another financial crisis, an ominous possibility in the next presidency, whether Donald Trump or Hillary Clinton enters the Oval Office — given that nothing fundamental has been altered when it comes to Wall Street's practices and predation. At the heart of American political consciousness right now lies a soul-crushing reality for millions of distraught Americans: the choices for president couldn't be feebler or more disappointing. On the one hand, we have a petulant, vocabulary-challenged man-boar of a billionaire, who hasn't paid his taxes, has regularly left those supporting him holding the bag, and seems like a ludicrous composite of every bad trait in every bad date any woman has ever had. On the other hand, we're offered a walking photo-op for and well-paid speechmaker to Wall-Street CEOs, a one-woman money-raising machine from the 1% of the 1%, who, despite a folksiness that couldn't look more rehearsed, has methodically outplayed her opponent. With less than two weeks to go before E-day — despite the Trumptilian upheaval of the last year — the high probability of a Clinton win means the establishment remains intact. When we awaken on November 9th, it will undoubtedly be dawn in Hillary Clinton's America and that potentially means four years of an economic dystopia that will (as would Donald Trump's version of the same) leave many Americans rightfully anxious about their economic futures. None of the three presidential debates suggested that either candidate would have the ability (or desire) to confront Wall Street from the Oval Office. In the second and third debates, in case you missed them, Hillary didn't even mention the Glass-Steagall Act, too big to fail, or Wall Street. While in the first debate, the subject of Wall Street only came up after she disparaged the tax policies of "Trumped-up, trickle down economics" (or, as I like to call it, the Trumpledown economics of giving tax and financial benefits to the rich and to corporations). In this election, Hillary has crafted her talking points regarding the causes of the last financial crisis as weapons against Trump, but they hardly begin to tell the real story of what happened to the American economy. The meltdown of 2007-2008 was not mainly due to "tax policies that slashed taxes on the wealthy" or a "failure to invest in the middle class," two subjects she has repeatedly highlighted to slam the Republicans and their candidate. It was a byproduct of the destruction of the regulations that opened the way for a too-big-to-fail framework to thrive. Under the presidency of Bill Clinton, Glass-Steagall, the Depression-era act that once separated people's bank deposits and loans from any kind of risky bets or other similar actions in which banks might engage, was repealed under the Financial Modernization Act of 1999. In addition, the Commodity Futures Modernization Act was passed, which allowed Wall Street to concoct devastating unregulated side bets on what became the subprime crisis. Given that the people involved with those choices are still around and some are still advising (or in the case of one former president living with) Hillary Clinton, it's reasonable to imagine that, in January 2017, she'll launch the third term of Bill Clinton when it comes to financial policy, banks, and the economy. Only now, the stakes are even higher, the banks larger, and their impunity still remarkably unchallenged. Consider President Obama's current treasury secretary, Jack Lew. It was Hillary who hit the Clinton Rolodex to bring him back to Washington. Lew first entered Bill Clinton's White House in 1993 as special assistant to the president. Between his stints working for Clinton and Obama, he made his way into the private sector and eventually to Wall Street — as so many of his predecessors had done and successors would do. He scored a leadership role with Citigroup during the time that Bill Clinton's former Treasury Secretary (and former Goldman Sachs co-Chairman) Robert Rubin was on its board of directors. In 2009, Hillary selected him to be her deputy secretary of state. Lew is hardly the only example of the busy revolving door to power that led from the Clinton administration to the Obama administration via Wall Street (or activities connected to it). Bill Clinton's Treasury Under Secretary for International Affairs, Timothy Geithner worked with Robert Rubin, later championed Wall Street as president and CEO of the New York Federal Reserve while Hillary was senator from New York (representing Wall Street), and then became Obama's first treasury secretary while Hillary was secretary of state. One possible contender for treasury secretary in a new Clinton administration would be Bill Clinton's Under Secretary of Domestic Finance and Obama's Commodity Futures Trading Commission chairman, Gary Gensler (who was — I'm sure you won't be shocked — a Goldman Sachs partner before entering public service). These, then, are typical inhabitants of the Clinton inner circle and of the political-financial corridors of power. Their thinking, like Hillary's, meshes well with support for the status quo in the banking system, even if, like her, they are willing on occasion to admonish it for its "mistakes." This thru-line of personnel in and out of Clinton World is dangerous for most of the rest of us, because behind all the "talking heads" and genuinely amusing Saturday Night Live skits about this bizarre election lie certain crucial issues that will have to be dealt with: decisions about climate change, foreign wars, student-loan unaffordability, rising income inequality, declining social mobility, and, yes, the threat of another financial crisis. And keep in mind that such a future economic meltdown isn't an absurdly long-shot possibility. Earlier this year, the Federal Reserve, the nation's main bank regulator, and the Federal Deposit Insurance Corporation, the government entity that insures our bank deposits, collectively noted that seven of our biggest eight banks — Citigroup was the exception — still have inadequate emergency plans in the event of another financial crisis. Exploring a Two-Faced WorldPoliticians regularly act one way publicly and another privately, as Hillary was "outed" for doing by WikiLeaks via its document dump from Clinton campaign manager John Podesta's hacked email account. Such realities should be treated as neither shockers nor smoking guns. Everybody postures. Everybody lies. Everybody's two-faced in certain aspects of their lives. Politicians just make a career out of it. What's problematic about Hillary's public and private positions in the economic sphere, at least, isn't their two-facedness but how of a piece they are. Yes, she warned the bankers to "cut it out! Quit foreclosing on homes! Quit engaging in these kinds of speculative behaviors!" — but that was no demonstration of strength in relation to the big banks. Her comments revealed no real understanding of their precise role in exacerbating a fixable subprime loan calamity and global financial crisis, nor did her finger-wagging mean anything to Wall Street. Keep in mind that, during the build-up to that crisis, as banks took advantage of looser regulations, she collected more than $7 million from the securities and investment industry for her New York Senate runs ($18 million during her career). In her first Senate campaign,Citigroup was her top contributor. The four Wall-Street-based banks (JPMorgan Chase, Citigroup, Goldman Sachs, and Morgan Stanley) all feature among her top 10 career contributors. As a senator, she didn't introduce any bills aimed at reforming or regulating Wall Street. During the lead-up to the financial crisis of 2007-2008, she did introduce five (out of 140) bills relating to the housing crisis, but they all died before making it through a Senate committee. So did a bill she sponsored to curtail corporate executive compensation. Though she has publicly called for a reduction in hedge-fund tax breaks (known as "closing the carried interest loophole"), including at the second debate, she never signed on to the bill that would have done so (one that Obama co-sponsored in 2007). Perhaps her most important gesture of support for Wall Street was her vote in favor of the $700 billion 2008 bank bailout bill. (Bernie Sanders opposed it.) After her secretary of state stint, she returned to the scene of banking crimes. Many times. As we know, she was also paid exceedingly well for it. Friendship with the Clintons doesn't come cheap. As she said in October 2013, while speaking at a Goldman Sachs AIMS Alternative Investments' Symposium, "running for office in our country takes a lot of money, and candidates have to go out and raise it. New York is probably the leading site for contributions for fundraising for candidates on both sides of the aisle." Between 2013 and 2015, she gave 12 speeches to Wall Street banks, private equity firms, and other financial corporations, reaping a whopping $2,935,000 for them. In her 2016 presidential run, the securities and investment sector (aka Wall Street) has contributed the most of any industry to PACs supporting Hillary: $56.4 million. Yes, everybody needs to make a buck or a few million of them. This is America after all, but Hillary was a political figure paid by the same banks routinely getting slapped with criminal settlements by the Department of Justice. In addition, the Clinton Foundation counted as generous donors all four of the major Wall Street-based mega-banks. She was voracious when it came to such money and tone-deaf when it came to the irony of it all. Glass-Steagall and Bernie SandersOne of the more illuminating aspects of the Podesta emails was a series of communications that took place in the fall of 2015. That's when Bernie Sanders was gaining traction for, among other things, his calls to break up the big banks and resurrect the Glass-Steagall Act of 1933. The Clinton administration's dismantling of that act in 1999 had freed the big banks to use their depositors' money as collateral for risky bets in the real estate market and elsewhere, and so allowed them to become ever more engorged with questionable securities. On December 7, 2015, with her campaign well underway and worried about the Sanders challenge, the Clinton camp debuted a key Hillary op-ed, "How I'd Rein in Wall Street," in the New York Times. This followed two months of emails and internal debate within her campaign over whether supporting the return of Glass-Steagall was politically palatable for her and whether not supporting it would antagonize Senator Elizabeth Warren. In the end, though Glass-Steagall was mentioned in passing in her op-ed, she chose not to e |

| BREAKING: CLINTON ‘FIXER’ GOES PUBLIC, CONNECTS HILLARY TO BRUTAL HOMICIDES Posted: 27 Oct 2016 12:30 PM PDT The Conservative Tribune reports, The man whom Hillary Clinton and her husband, ex-President Bill Clinton, hired to cover up some of their dirtiest schemes has come forward to explain some of the worst secrets about the couple. The Financial Armageddon Economic Collapse Blog... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| URGENT: THOUSANDS OF AMERICANS TAKE A STAND AGAINST SOROS’ RIGGED ELECTION FOR HILLARY CLINTON Posted: 27 Oct 2016 12:00 PM PDT The Conservative Tribune reports, conservatives have launched a White House petition demanding that voting machines allegedly owned by liberal billionaire George Soros be removed from all polling stations. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts ,... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| Michael Moore In TrumpLand: The Last President of the United States Posted: 27 Oct 2016 11:30 AM PDT Here's the REAL ending to Mike's ANTI-Trump rant that was cut out by Trump supporters. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many more [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| Egon von Greyerz: Except in dollars, gold is near the 2011 highs Posted: 27 Oct 2016 10:43 AM PDT 12:45p CT Thursday, October 27, 2016 Dear Friend of GATA and Gold: Swiss gold fund manager Egon von Greyerz writes that while gold lately has not been doing well in U.S. dollar terms, in terms of other currencies it has being doing very well indeed, even spectacularly. Von Greyerz's analysis is headlined "Gold Is Near the 2011 Highs" and it's posted at the Gold Switzerland internet site here: https://goldswitzerland.com/gold-is-near-the-2011-highs/ CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT We Are Amid the Biggest Financial Bubble in History; With GoldCore you can own allocated -- and most importantly -- segregated coins and bars in Switzerland, Singapore, and Hong Kong. Switzerland, Singapore, and Hong Kong remain extremely safe jurisdictions for storing bullion. Avoid exchange-traded funds and digital gold providers where you are a price taker. Ensure that you are outright legal owner of your bullion. If you do not own segregated bullion that you can visit, inspect, and take delivery of, you are exposed. Crucial guides to storage in Singapore and Switzerland can be read here: http://info.goldcore.com/essential-guide-to-storing-gold-in-singapore http://info.goldcore.com/essential-guide-to-storing-gold-in-switzerland GoldCore does not report transactions to any authority. Safety, privacy, and confidentiality are paramount when we are entrusted with storage of our clients' precious metals. Email the GoldCore team at info@goldcore.com or call our trading desk: UK: +44(0)203-086-9200. U.S.: +1-302-635-1160. International: +353(0)1-632-5010. Visit us at: http://www.goldcore.com Help GATA by purchasing DVDs of GATA's London conference in August 2011 or GATA's Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: |

| Last chance to purchase GATA conference video discs and WSJ ad posters Posted: 27 Oct 2016 10:28 AM PDT 12:30p CT Thursday, October 27, 2016 Dear Friend of GATA and Gold: Video discs of GATA's 2005 conference in the Yukon and 2011 conference in London and posters of GATA's January 31, 2008, full-page advertisement in The Wall Street Journal will be available for purchase only until the end of this month. If you don't have one of each, please consider helping us clear the inventory. The video discs can be purchased here: http://www.goldrush21.com/order.html The posters can be purchased here: CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT 13.4 Trillion Reasons Why New BMG Silver BullionFund Company Announcement TORONTO, Ontario -- Bullion Management Group Inc., a Canadian pioneer in precious metals investing, has expanded its line of bullion funds with the launch of BMG Silver BullionFund. The new fund invests exclusively in physical silver bullion. It is designed for investors seeking to add silver to their precious metals investments that offer long-term security and potential capital growth. BMG Silver BullionFund is an open-end mutual fund trust that can be purchased and redeemed daily at net asset value and is eligible for TFSA, RRSP, and RESP investments. Nick Barisheff, president and CEO of BMG, believes that there are several important reasons why investors looking for a safe haven are adding bullion to their portfolios. He observes that $13.4 trillion of government bonds worldwide now offer yields below zero. ... For the remainder of the announcement: http://bmgbullion.com/13-4-trillion-reasons-new-bmg-silver-bullionfund-m... Help GATA by purchasing DVDs of GATA's London conference in August 2011 or GATA's Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: |

| Alasdair Macleod: The vexed question of the dollar Posted: 27 Oct 2016 10:13 AM PDT 12:15p CT Thursday, October 27, 2016 Dear Friend of GATA and Gold: GoldMoney research director Alasdair Macleod writes today that China is controlling both interest rates and gold prices and likely already has enough gold to hedge its dollar exposure in its huge foreign exchange reserves. Macleod's analysis is headlined "The Vexed Question of the Dollar" and it's posted at GoldMoney here: https://wealth.goldmoney.com/research/goldmoney-insights/the-vexed-quest... CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT Sandspring Resources Commences 2016 Exploration Campaign Company Announcement Sandspring Resources Ltd. (TSX VENTURE:SSP, US OTC: SSPXF) is pleased to announce commencement of the 2016 exploration campaign at its Toroparu Gold Project in Guyana, South America. In 2015 the company completed a 3,700-meter diamond drilling program on the promising Sona Hill Prospect, located 5 kilometers southeast of the main Toroparu deposit. Sona Hill is the easternmost gold anomaly in a cluster of 10 gold features located within a 20-by-7-kilometer hydrothermal alteration halo around Toroparu. Drilling at Sona Hill in 2012 and in 2015 intercepted high-grade mineralization in both saprolite and bedrock, and confirmed the continuity and grade potential of the Sona Hill mineralization. For the remainder of the announcement and highlights of the 2015 drill program: https://finance.yahoo.com/news/sandspring-resources-commences-2016-explo... Help GATA by purchasing DVDs of GATA's London conference in August 2011 or GATA's Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or by purchasing a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: |

| The vexed question of the dollar Posted: 27 Oct 2016 10:02 AM PDT Finance and Eco. |

| Must Watch!! Hillary Clinton tried to ban this video Posted: 27 Oct 2016 09:30 AM PDT Hillary Clinton's Strange Behavior: WHAT IS GOING ON? Shocking Video clinton works like a demon bill clinton faints 911 memorial bizarre interview hillary clinton president presidential race 2016 2017 The Financial Armageddon Economic Collapse Blog tracks trends and forecasts ,... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| Donald Trump Has Won The 2016 Presidential Election Posted: 27 Oct 2016 09:07 AM PDT In this special report Alex Jones goes over how Donald Trump has already won and the Democrats are pulling every dirty trick to try and steal the election from him. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free... [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| Anonymous - Humanity's Now Is The Time Posted: 27 Oct 2016 08:44 AM PDT Trump is climbing up on the polls , Send Hillary to colonize the Sun. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many more [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| Posted: 27 Oct 2016 08:26 AM PDT The first retest of the 200 DMA is the second best buying opportunity in a new bull market. |

| The Dark Wave of Brexit Uncertainty Posted: 27 Oct 2016 07:49 AM PDT This post The Dark Wave of Brexit Uncertainty appeared first on Daily Reckoning. The UK voted to part ways with the EU in June. Since then Brexit uncertainty has left the UK's market in disarray as the pound sterling's fallen 18% since the referendum. While what happens in the UK might seem like "just something across the pond," the coming months of Brexit negotiations could impact your money, investments and global trade. The Bank for International Settlement (BIS) and the International Monetary Fund (IMF) have identified banks that are "systemically important" to the world economy. Under those same principles, the United Kingdom is a systemically important country for financial markets. What happens in the UK matters worldwide. Why the UK MattersThe IMF's World Economic Outlook report noted, "the Brexit vote implies a substantial increase in economic, political, and institutional uncertainty, which is projected to have negative macroeconomic consequences." The organization has since reduced its global forecast for 2017 by 0.1 percentage point, down to 3.4 percent. The IMF also reduced Britain's 2016 GDP forecast to 1.9%. The UK is the second largest economy in the EU system (for now anyways). According to the World Bank's GDP index for 2015 the UK holds the fifth largest economy in the world. To see a systemically important world economy make such a move will have real repercussions. While the EU project continues to develop from its Euro currency introduction in 1999, the UK remained resistant to adopting the currency as its own. As a country of separated status, the pound sterling remained the modus operandi of the British Isles. But it was still highly connected to mainland Europe's economy. In 2015, 44% of the UK's goods and services were exported to the EU, while 53% of UK imports came from the EU. Since the leave vote, areas ranging from travel to business investment options have come into question. As the French mathematician Blaise Pascal once said, "It is not certain that everything is uncertain." Pascal very well could have changed his approach after the Brexit debacle. Brexit UncertaintyThis type of uncertainty has left the private sector in disarray. The chief executive of Morgan Stanley, Robert Rooney, said that regardless of the emotional hits from Brexit, "it really isn't terribly complicated. If we are outside the EU and we do not have what would be a stable and long-term assured commitment that we would have access to the single market, then we will have to do a lot of things that we do today from London somewhere inside the EU 27." Even Goldman Sachs is considering dipping out in the wake of the UK "leave" vote. In an August regulatory filing Goldman indicated that the Brexit decision "may adversely affect the manner in which we operate certain of our businesses in the European Union and could require us to restructure certain of our operations." If financial institutions leaving the UK is bad, industrial sectors trending toward leaving might be an even heavier blow. Nissan has claimed that it is now going to review and, potentially, reconsider its future industrial investments in the UK after much uncertainty following Brexit aftermath. This was the first major multinational company to announce that it was reviewing its future operations following the Brexit negotiations. Expectations would suggest that this will not be the last major business to consider such options within the uncertain climate. As stories like these continue under a wave of uncertainty, international markets could be under threat. This wave could also take a huge hit with other EU states. The impact on multinational companies, because of grey clouds from Brexit, will impact how the U.S economy operates. The globalization efforts that have been set in motion will mean that negative economic consequences are on the table. French President Hollande did not mince words saying, "There must be a threat, there must be a risk, there must be a price, otherwise we will be in negotiations that will not end well and, inevitably, will have economic and human consequences." Jim Rickards predicted such a harsh rhetoric all the way back in July. While standing at the London Eye after the vote Rickards said, "The EU is likely to take a punitive approach to the Brexit negotiations. This will be done as "an example to the rest" in order to head off other nationalist movements that want to quit the EU."

Policy Makers Meet, No Actions TakenSimilar to Hillary Clinton's Wall Street notes that were leaked out, the newly appointed British Prime Minister, Theresa May saw her own statements to Goldman Sachs let out. The leak reveals that she disclosed her private concerns about the business sector fleeing the country following Brexit negations and the impact on the private sector and what it might mean. She spoke in an hour long session at Goldman's London offices in May. While there she said on the UK leaving the EU that, "I think the economic arguments are clear." The Prime Minister went on to note that "I think being part of a 500-million trading bloc is significant for us. I think, as I was saying to you a little earlier, that one of the issues is that a lot of people will invest here in the UK because it is the UK in Europe." Since then, the European Council met in October but neglected to formally address the any Brexit negotiations at all. This coming after an informal Council meeting in September in which only vague promises on European "unity" were made. Given the fallout from the Brexit vote and the misjudgments by so many, what is worse is that now markets, business investors and private sector growth is being left in the dark. The lack of strategy from leadership in the UK and the EU appears to be at an all time low. The leader of the Labour Party, Member of Parliament Jeremy Corbyn blasted the lack of action saying, “Brexit was apparently about taking back control but the devolved governments don’t know the plan, businesses don’t know the plan, Parliament doesn’t know the plan." Markets often follow leadership. But to find the real story you have to follow the trends. Top trend following expert, Michael Covel wrote, "Brexit was the signal that the global financial system is a toxic cesspool. But here's the thing: It might not be the catalyst to send the global economy into a tailspin." Covel believes that while the British vote from the EU was harsh, there is still more "exits" to come. This is why the uncertainty and speculation around the UK will have a violent impact with the global economy. The U.S, EU and BrexitTo put it simply, the impact of the Brexit and the uncertainty around its exit strategy is complex. While the immediate shock of the Brexit vote hit U.S markets, things have since then calmed. Though the U.S economy might not have as much to lose as the EU, the outcomes of negotiation over Brexit and how business and trade operate will be important to watch for years to come. The U.S economic bond with the EU is the largest and most complex worldwide. The transatlantic connections have an estimated $2.7 billion per day in generated goods and services through trade flows. This relationship goes even further with an estimated 6.8 million jobs that stem through transatlantic investment relations. In a recent Wall Street Journal (WSJ) survey of economists, polling found that "60% thought financial activities would suffer…" The journal noted that the risk of increased uncertainty in the UK exit strategy could hit significant speed bumps if the "UK's departure from the EU is drawn out with unfavorable economic terms," said Lewis Alexander, chief U.S. economist of the investment bank Nomura.

So what does that mean for U.S in particular? Unlike other more "parasitic" trade flows, the U.S has a services trade surplus of $50.6 billion with the EU (2014). These trade connections between the U.S and EU are not only vital to a large section of global trade flows, they are strategic building surplus markets. These factors provide room for economic stability and investments globally. Generating a newly demanded relationship that is divergent from the previous three decades between the UK and the EU will not be a walk in the park. It seems the one area that most can agree on is that the two year exit mandate under the current EU treaty is just not feasible. The prospect of two years (plus) of negotiations, poignant rhetoric and clouds of unpredictability is something that cannot easily be afforded. Especially in the current global economic state. Leaving the EU market might be a harder sell for markets and have a harsher impact on the global markets than had once been expected. As Jim Rickards posted in the Daily Reckoning in the immediate aftermath of the Brexit vote, "Above all, these trends mean uncertainty. Markets have ways to price risk on a probabilistic basis, but markets have no way to price uncertainty where almost anything can happen. In these situations, markets go to the safest of safe havens and that means cash, U.S. Treasuries, and gold." Expect these markets to take greater precaution for the months, if not years to come. Regards, Craig Wilson, @craig_wilson7 Ed. Note: Sign up for a FREE subscription to The Daily Reckoning, and you'll receive regular insights for specific profit opportunities. By taking advantage now, you're ensuring that you'll be set up for updates and issues in the future. It's FREE. The post The Dark Wave of Brexit Uncertainty appeared first on Daily Reckoning. |

| This Is What Gold Does In A Currency Crisis, Brexit Edition Posted: 27 Oct 2016 03:53 AM PDT In June the UK shocked the world – or at least the world’s elites – by voting to pull out of the European Union. Economists predicted disaster, EU leaders threatened pain for British exporters and tourists, and the media settled in to watch the UK shrivel and die. Four months later, the appropriate response is a yawn rather than a scream. |

| “Chindia†Buying Gold on Dips, 20% Corrections Are “Non Events†Posted: 27 Oct 2016 03:04 AM PDT Mike Gleason (Money Metals Exchange): Frank, it's good to have you back on. Congratulations on another well-deserved award and thanks for joining us again today. Frank Holmes (U.S. Global Investors): Well, thank you for that recognition, but I want to make sure that your listeners know that portfolio manager Ralph Aldis is also key in that whole thought process and director of research and oversees the gold funds with myself. He's a geologist. He has a master’s in mineral economics, a master’s in geology. I like to tease him he has more degrees than a thermometer. |

| Breaking News And Best Of The Web Posted: 27 Oct 2016 02:37 AM PDT Deluge of earnings this week, with Apple starting things on a down note. The dollar is rising and so is inflation. Corporate debt and earnings becoming major near-term risks. China’s mortgage bubble is the biggest ever. US auto sales start to fall. Major cyber attack hits US east coast. Clinton way up in polls after […] The post Breaking News And Best Of The Web appeared first on DollarCollapse.com. |

| New PEA for Seabridge's KSM Is a Game-Changer Posted: 27 Oct 2016 01:00 AM PDT Calling the new preliminary economic assessment for Seabridge Gold Inc.'s (SEA:TSX; SA:NYSE.MKT) KSM "a big improvement for a unique massive Au-Cu project," Paradigm Capital believes the company will continue to build value for investors. |

| Santacruz Silver Mining: The Market Still Doesn't Get It! Posted: 27 Oct 2016 01:00 AM PDT Ben Kramer-Miller, chief analyst at miningWEALTH, notes that Santacruz Silver Mining has been a top pick since March, and while shares have risen ~70%, he still believes there is substantial upside... Visit the aureport.com for more information and for a free newsletter |

| Recommended Reading: 'When Money Dies: The Nightmare of the Weimar Collapse' Posted: 27 Oct 2016 01:00 AM PDT Precious metals expert Michael Ballanger discusses his favorite investing books and reviews the landscape for gold and the U.S. dollar between now and the end of the year. |

Mainland Europe will continue to feel this concentrated uncertainty. The

Mainland Europe will continue to feel this concentrated uncertainty. The | You are subscribed to email updates from Save Your ASSets First. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment