Gold World News Flash |

- Saudi Financial Crisis “Could Leave Oil at $25″ as Contractors Face Being Paid in IOUs

- Gold Price Closed at $1252.90 Down $1.80 or -0.14%

- TRUTH BOMB: The Saudis Turn On The Neocons, “The U.S. Blew Up World Trade Center To Create War On Terror”

- Hedge Funds Are Betting Record Amounts on Meltdown of Australian Banks and Housing Bubble

- Shortage Or No Shortage? Renowned Silver Expert David Morgan Presents the Data

- Who Is Right Between Oil And Other Commodities: One Hedge Fund's Opinion

- How Will America Trade With WORTHLESS DOLLARS & NO GOLD? — Bill Holter

- The Fed's Loss Of Credibility Is Real: This Is What It Looks Like

- The CME Admits Futures Trading Was Rigged Under Old System

- Wheelbarrow Economics

- We're In The Eye Of A Global Financial Hurricane

- Banks must defend Libor lawsuits after judges warn of impact

- Gold is having an unusual rising correction, Turk tells KWN

- Four Events in April Set the Stage for the Rest of 2016

- Are Investors Idiots?

- Gold Daily and Silver Weekly Charts - Option Expiry on the Comex - History Lesson

- Donald Trump on Brexit

- #Brexit: #ProjectFear is Ridiculous

- Tomorrow the Eurozone Determines Greece’s Fate

- The Zionist Subversion of Western Civilization [Part 1]

- How the Fed Is Fooling You Again

- END TIMES ALERT -- Something Strange is Happening Worldwide!

- Agenda 21 Alert -- Germany's Bayer Makes Offer to Buy Monsanto for $62 Billion

- Can The British Pound Turn Around?

- Why Aren't Venezuelan Interest Rates Going Negative Like in Europe?

- Time to Hedge Gold and Silver Positions

- Gold - The Next Top Performing Asset to 2020 & Beyond

- Did AMAT Chirp? Implications for the Economy and Gold

- ZAR Gold Price Signals A September 2001-Type Event In The Financial Markets

- How to Take Advantage of Multi-Week Correction in Gold and Silver

- How the US Dollar Influences Oil Prices

| Saudi Financial Crisis “Could Leave Oil at $25″ as Contractors Face Being Paid in IOUs Posted: 23 May 2016 10:30 PM PDT by Ambrose Evans-Pritchard, The Telegraph:

Three-month interbank offered rates in Riyadh have suddenly begun to spiral upwards, reaching the highest since the Lehman crisis in 2008. Reports that the Saudi government is to pay contractors with tradable IOUs show how acute the situation is becoming. The debt-crippled bin Laden group is laying off 50,000 construction workers as austerity bites in earnest. Societe Generale's currency team has advised clients to short the Saudi riyal, betting that the country will be forced to ditch its long-standing dollar peg, a move that could set off a cut-throat battle for global share in the oil markets. Francisco Blanch, from Bank of America, said a rupture of the peg is this year's number one "black swan event" and would cause oil prices to collapse to $25 a barrel. Saudi Arabia's foreign reserves are still falling by $10bn (£6.9bn) a month, despite a switch to bond sales and syndicated loans to help plug the huge budget deficit. The country's remaining reserves of $582bn are in theory ample – if they are really liquid – but that is not the immediate issue. The problem for the Saudi central bank (SAMA) is that reserve depletion automatically tightens monetary policy. Bank deposits are contracting. So is the M2 money supply. Domestic bond sales do not help because they crowd out Saudi Arabia's wafer-thin capital markets and squeeze liquidity. Riyadh now plans a global bond issue. While crude prices have rallied 80pc to almost $50 a barrel since mid-February, this has not yet been enough to ease Saudi Arabia's financial crunch. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold Price Closed at $1252.90 Down $1.80 or -0.14% Posted: 23 May 2016 10:29 PM PDT

I reckon I couldn't have picked a better day to play hooky than last Friday, as very little transpired. As usual, that scurvy tapeworm, the US dollar index, lies at the knot of the riddle (to mix a couple of disgusting metaphors). Chart's here, http://schrts.co/dIXAR3 Last Wednesday the Dollar index traded up through its 50 DMA, then Thursday penetrated the downtrend line from February -- and stopped. Jes' balked like a flop eared mule. And has been stuck there ever since, too lily-livered to bust through 95.50 resistance. What's the big deal? Just this, markets that break through resistance & downtrend lines tend to show at least some life & enthusiasm, reaching into the new territory. Even with the Fed sending out OLs (Official Liars) to jawbone up the dollar with more empty threats of raising their discount rate in June, dollar index can't advance. Now this may not be permanent, it may be passing, but it sure ain't no way to start a rally. Looks weak & sickly as a runt pig. Japanese yen benefited from trade balance news today and rose 0.78% to 91.53. This leaves the yen broken down from a bearish rising wedge, but bouncing off its 50 DMA. Euro lost 0.04% to $1.1218. Lift up your eyes to the horizon! Y'all realize that we are watching a currency centrifuge in slow motion, right? The huge overindebtedness is whirling currencies & economies around faster and faster until they are shaken to pieces. Mercy, don't be one of those who can't believe an inevitable outcome because it's not yet before your eyes. The default will come, & with it transglobal agony. Facebook won't save you, nor Amazon. Not even Netflicks. Stocks are breaking down through the neckline of a head & shoulders top. http://schrts.co/Q6KUW0 Like busy fire ants beneath the surface, I suspect the Nice Government Men of the Plunge Protection team and sweating themselves to dehydration trying to keep stocks up. Dow gained -- get out your magnifying glass -- 2.09 (0.01%) to 17,503.03, but other indices lost millimeters. S&P500 shaved off 2.79 (0.14%) to 2,049.53. Dow in Gold & Dow in silver are correcting the first little leg down of their unfolding plunge. DiS is here, http://schrts.co/Q6KUW0 Dow in Gold here, http://schrts.co/8Sv0tc Gold lost $1.30 today to settle on Comex at $1,251.10. Silver subtracted 10.9¢ to 1641¢. Both have skidded to a halt after last week's break, at least temporarily. Gold chart can be found here, http://schrts.co/rXkzy8 My suspected targets are the bottom of the present uptrending range, which would be a very shallow correction indeed, and the $1,208 - $1,190 area. Below that a Freddie Kruger correction would cut to the 200 DMA ($1,161). The height of that triangle gold formed in May (blue dashed line) projects a decline to $1,200 or $1,190. Volume is rising slightly as it falls. Silver's chart is here, http://schrts.co/ztbfs7 Most likely targets are 1600¢ and the 200 day moving average, now at 1618¢. As for gold, indicators point down for silver but it's taking its time to work lower. I am anxious to see how Commitments of Traders reports have changed when they come out this week. I keep thinking this will be a shallow correction, but the market may slap my jaws. Don't mess with Czechs. On 23 May 1618 in Prague began the 30 Years War when Czech protestants tossed three Habsburg governors out a window -- the Defenestration of Prague. It was NOT a first story window, and this was not the first time the Czechs had removed offensive officials by defenestration. They killed seven city council members that way in 1419. Now all you squeamish modern folks will wince at the thought of pitching offending officials out the window. However, think about it. Think how it would improve the manners of those defenestrated, and how respectful it would render the rest, the not-yet-defenestrated. Might work better than a recall election, and certainly more permanently. Aurum et argentum comparenda sunt -- -- Gold and silver must be bought. - Franklin Sanders, The Moneychanger The-MoneyChanger.com © 2016, The Moneychanger. May not be republished in any form, including electronically, without our express permission. To avoid confusion, please remember that the comments above have a very short time horizon. Always invest with the primary trend. Gold's primary trend is up, targeting at least $3,130.00; silver's primary is up targeting 16:1 gold/silver ratio or $195.66; stocks' primary trend is down, targeting Dow under 2,900 and worth only one ounce of gold or 18 ounces of silver. US $ and US$-denominated assets, primary trend down; real estate bubble has burst, primary trend down. WARNING AND DISCLAIMER. Be advised and warned: Do NOT use these commentaries to trade futures contracts. I don't intend them for that or write them with that short term trading outlook. I write them for long-term investors in physical metals. Take them as entertainment, but not as a timing service for futures. NOR do I recommend investing in gold or silver Exchange Trade Funds (ETFs). Those are NOT physical metal and I fear one day one or another may go up in smoke. Unless you can breathe smoke, stay away. Call me paranoid, but the surviving rabbit is wary of traps. NOR do I recommend trading futures options or other leveraged paper gold and silver products. These are not for the inexperienced. NOR do I recommend buying gold and silver on margin or with debt. What DO I recommend? Physical gold and silver coins and bars in your own hands. One final warning: NEVER insert a 747 Jumbo Jet up your nose. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 23 May 2016 09:27 PM PDT by SGT, SGT Report.com:

It has been 14 years, 8 months, and 12 days since the Neocon Zionist monsters in the United States along with their partners in the crime, the Saudis and Israeli Mossad orchestrated the 9/11 false flag operation that murdered nearly 3,000 innocents. Just a few smoking guns of their heinous crimes include the free fall collapse of world trade center building 7, the statistical impossibility of the BBC reporting about it 25 minutes too early and Lucky Larry’s multi-billion dollar insurance payout for “acts of terror.” The litany of evidence of the NWO’s dastardly deeds on 9/11 has been documented, catalogued and readied for trials. The true culprits have been identified. And if you want the exact names and details there is no better video to watch than this one: 9/11 Conspiracy Solved: Names, Connections and Details Exposed What remains is for these evil men to be brought to justice and tried for their crimes against American law, the Constitution and humanity. We have long hoped that the day would come when these sinister evil doers would start turning on each other and the truth would begin spilling out. Enter the 28 pages and the Saudis. Reportedly, the classified 28 pages of the 9/11 report implicate the Saudis for at least helping to fund the terror attacks, but those 28 pages conveniently make no mention of Israeli involvement in the planning and execution of the attacks that day. The dancing Mossad agents who were arrested, sent back to Israel after ten weeks and who then admitted on Israeli TV, “We were there to document the event“. No mention of them.

The decision has been made to throw the Saudis under the bus for the event that has been up to this point, been blamed solely on Muslims. But the official 9/11 fable is now in the process of collapsing like a house of cards, and that house of cards is now coming down as fast as WTC-7. In my interview with Harley Schlanger on May 20th we discussed this in some detail. I told Harley, “all of this is being orchestrated to throw Saudi Arabia under the bus, whilst never mentioning Israel.” Harley’s response could not have been more prescient.

The 9/11 truth research community has the goods on these people. We KNOW what really happened and who is really responsible. But what we have needed is for these rats to turn on each other on a global stage. And today it began. The Saudis have just dropped the biggest truth bomb since Putin exposed the Pentagon’s bogus war on Isis in Syria. Breitbart reported today: Saudi Press: U.S. Blew Up World Trade Center To Create 'War On Terror The Saudi press is still furious over the U.S. Senate'sunanimous vote approving a bill that allows the families of 9/11 victims to sue Saudi Arabia. This time, the London-based Al-Hayat daily has claimed that the U.S. planned the attacks on the World Trade Center in order to create a global war on terror.The article, written by Saudi legal expert Katib al-Shammari and translated by MEMRI, claims that American threats to expose documents that prove Saudi involvement in the attacks are part of a long-standing U.S. policy that he calls "victory by means of archives." Al-Shammari claims that the U.S. chooses to keep some cards close to its chest in order to use them at a later date. One example is choosing not to invade Iraq in the 1990s and keeping its leader, Saddam Hussein, alive to use as "a bargaining chip" against other Gulf States. Only once Shi'ism threatened to sweep the region did America act to get rid of Hussein "since they no longer saw him as an ace up their sleeve." He claims that the 9/11 attacks were another such card, enabling the U.S. to blame whoever suited its needs at a particular time; first it blamed Al-Qaeda and the Taliban, then Saddam Hussein's regime in Iraq, and now Saudi Arabia.

The intention of the attacks, writes al-Shammari in his conspiracy article, was to create "an obscure enemy – terrorism – which became what American presidents blamed for all their mistakes" and that would provide justification for any "dirty operation" in other countries. ————— You can read the rest at Breitbart by clicking here. But today, Monday, May 23rd is a day for all of those who care about TRUTH to remember. The rats are fleeing the sinking ship of lies. Let the trials of the real perpetrators of the 9/11 horrors begin. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Hedge Funds Are Betting Record Amounts on Meltdown of Australian Banks and Housing Bubble Posted: 23 May 2016 09:00 PM PDT by Wolf Richter, Wolf Street:

It has been called the "widow maker trade," based on how short sellers have been dealt with over the past few years. The fundamentals have been inviting: Australia has been in a fully blooming housing bubble. Households are the most indebted in the world, based on debt to disposable income. To maintain the housing bubble, the central bank slashed interest rates to record lows (1.75%). The government wants to keep the bubble going for as long as possible. So regulators close their eyes, according to media reports, to questionable or even illegal lending practices. Home prices, after soaring for years, are clearly unsustainable. But just because it's a bubble doesn't mean it has to implode on schedule. It will implode, as all bubbles do, but on its own time. If short sellers get the timing wrong, they'll get run over by market euphoria. Hence, "widow maker trade" for betting against the housing bubble by shorting the banks. The biggest four banks in Australia are special creatures. Total assets of Commonwealth Bank of Australia (CBA), Australia & New Zealand Banking Group (ANZ), Westpac Banking Corp (WBC), and National Australia Bank (NAB) amount to 220% of Australia's GDP! The assets (mostly outstanding loans) of the big four Australian banks have skyrocketed. For example, in 1999, CBA's assets amounted to 14% of GDP. That was already high, for just one bank! By the end of 2014, they reached 51% of GDP. How's that possible? A housing bubble with sharp price gains funded by ever larger mortgages extended by ever blinder loan officers. If these four banks topple, as we noted almost a year ago, they can sink the entire Australian economy. These banks are powder kegs. The housing bubble is already toast in a number of smaller cities, particularly those tied to the mining bust. It's starting to wobble in other areas. So hedge funds have redoubled their bets. Short positions on the big four Australian banks have soared 50% this year to over 9 billion Australian dollars (US$6.49 billion), and are up 350% since 2014, according to the Wall Street Journal – "the highest level since regulators began compiling data six years ago."

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shortage Or No Shortage? Renowned Silver Expert David Morgan Presents the Data Posted: 23 May 2016 08:30 PM PDT from The Morgan Report: | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Who Is Right Between Oil And Other Commodities: One Hedge Fund's Opinion Posted: 23 May 2016 08:22 PM PDT From Francesco Filia of Fasanara Capital So far in May, base metals and Oil decoupled markedly (chart attached below). While the Oil price kept rising and moved closer to 50$, base metals fell off a cliff and descended below March lows. We believe that Oil is the errant outlier, helped by deep but temporary supply outages in Canada and Nigeria and all-time record speculative flows, and is more likely to catch down to other commodities going forward rather than the other way round. We look at Oil gyrations as short-term heavy volatility, within a long-term downward trend.

On the other hand, weakness in commodities is consistent with fundamentals:

As such, at present, we find the price action so far in May to come in confirmation of our underlying thesis, thus expect more weakness in commodities from here, and Oil to eventually give in. * * * Extract from our latest Outlook 1. Strong US Dollar Factor: The weak Dollar is the major factor propelling the reflation sentiment in the market – EMs and Commodities greeted it with enthusiasm. However, it seems to us more a story of appreciating Yen and Eur out of the failed attempts by the Boj and the ECB to reflate their economies, as markets doubt their capacity at negative rates. It is not the typical weak Dollar out of increasing US current account deficit and increasing spending / imports, positive for the world and inflation. We expect the USD to have another leg up in the months ahead. A stronger Dollar alone has the potential to revive January-type fears over Oil, CNH, EMs, leading to a risk off of global assets, including the S&P. We see drivers of USD strength as follows: a. The FED took the steam off the Dollar by moving its expected path of tightening in 2016 from 4 hikes to 2 hikes only. The FED may become more dovish than that, but the market already discounts that. Of the 2 rate hikes planned, a tiny 20% is priced in at present. Not much headwind for the USD is left from FED's communication. At the other end of the equation, after recent fails, the BoJ first and then the ECB will go back at it, trying again to reflate their stagnant economies, with the debasement of JPY and EUR either a working tool or a side effect. b. A contracting current account deficit and budget deficit in the US will help strengthen the US Dollar. Recent trade balance numbers showed an unexpected marked improvement. The propensity to take on more debt for households and businesses may well be on a declining path. Savings rate for lower income brackets may rise as uncertainties loom large, the cost of retirement has gone up on zero rates environment, together with growing healthcare and education costs. Corporates desire for leverage, buybacks and M&As, may also deflate somewhat, as short rate rise, leverage ratios are now high (the median credit rating for S&P companies is now BB and declining, for a median net debt/ebitda above 3), regulation changes (inversion trades), pricing power is weak, excess capacity abounds. The public sector should fill the gap, but that is unlikely to happen in an election year. You can't increase deficit if you do not take on more debt. If borrowing declines, the deficit declines, the US Dollar rallies. c. Most likely, the relative performance of the US economy will continue to outclass growth in EMs, Europe and Japan. Technology is a huge plus for the US economy, their lead likely to outlast any speed-bump due to elections. 2. China factor: In the first quarter of 2016, it only managed to keep GDP in shape by means of monumental 1trn$ credit expansion (a whopping 10% of GDP in one quarter); unsustainable pace, and clearly a Pyrrhic victory. Unsurprisingly, you cannot borrow 10% of GDP per quarter for long without a currency adjustment, whether desired or not. And generally, what is the point in selling reserves to defend the peg, thus doing monetary tightening, when you seek so desperately monetary expansion. China's slowdown will continue affecting commodities markets front and center, metals in primis. China has grown to become the world's largest purchaser of aluminum, iron ore, zinc, nickel and copper, asking every year for more than double the needs o the US, Europe and Japan altogether. Incidentally, moreover, the speculative flows that determined massive volatility in RMB equity markets earlier on and possibly boosted propensity to currency outflows, are now to be seen in the commodity market. Not only then China buys a lot of metals, but speculative flows multiply those flows a few times over. Anecdotally, twice in the last few months, trading volumes in Iron Ore on the Dallan Commodities Exchange exceeded total China's 2015 imports (950m tonnes), in a single day. Rebar trading volumes exceeded Iron Ore, across 100 million trading accounts. Authorities rushed to curb speculation through higher fees and more margin requirements, but we have seen how effective they were last time around. An epic unwind may loom large (Read). Base Metals vs. Brent In May, there has been a clear divergence between Oil and other commodities. We believe that Oil is the errant outlier, helped by deep but temporary supply outages in Canada and Nigeria, and is more likely to catch down to other commodities going forward rather than the other way round. We look at Oil gyrations as short-term heavy volatility, within a long-term downward trend.

Speculative flows on Oil at all-time record highs NYMEX Crude Oil Light Sweet Non-Commercial Long Contracts/Futures Only at all-time highs

Iron Ore Futures Iron Ore has recently broken below March lows, falling by almost 30% this month. More weakness may be expected in the following weeks.

Rebar Futures Similarly to Iron Ore, Rebar lost more than 30% in the last month.

US Crude Oil Production US Crude Oil Production is slowing but not falling off a cliff (differently than what most market participants seem to believe).

DOE Crude Oil Total Inventories Crude Oil inventories remain close to historical highs (despite 60+ defaults in the US energy sector alone this year).

US Interest Rate Implied Probabilities A 32% hike probability is now priced in for the June meeting, from just 4% last week.

US 2yr Treasuries' yield 2yr US yields are currently close to a major resistance.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| How Will America Trade With WORTHLESS DOLLARS & NO GOLD? — Bill Holter Posted: 23 May 2016 07:48 PM PDT Dear CIGAs, (Courtesy of SGTreport.com) Bill Holter from JS Mineset is back to help us document the collapse for the fourth week of May, 2016. And as physical gold and silver moves East and intothe strong hands of more than a billion Chinese, and as foreign banks publicly settle global trade in the Yuan, Bill... Read more » The post How Will America Trade With WORTHLESS DOLLARS & NO GOLD? — Bill Holter appeared first on Jim Sinclair's Mineset. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Fed's Loss Of Credibility Is Real: This Is What It Looks Like Posted: 23 May 2016 07:15 PM PDT Asset markets aren't prepared for a hawkish Fed. As Bloomberg's Richard Breslow notes Fed speakers have even taken to the Sunday talk shows to beat the rate-rise drum as economics is morphing into punditry. They’re going to raise rates because they can, are independent, apolitical and can’t be bullied by foreigners. The numbers notwithstanding...

Simply put, as BofAML warns, a lack of credibility constrains Fed effectiveness drastically as they have "cried hawk" one too many times...

Therefore, as Breslow concludes, if the Fed plans to preemptively tighten, many investors will be caught massively off side doing the central bank’s bidding. Unless the Fed immediately starts intoning the mantra of “gradualism” in every speech.

If the Fed wants to rack up a success, they should let the economy continue to improve. Raising rates when they aren’t sure risks being a “Mission Accomplished” moment. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| The CME Admits Futures Trading Was Rigged Under Old System Posted: 23 May 2016 07:02 PM PDT Ask any trader what they believe to be the hallmark feature of any "rigged market" and the most frequent response(in addition to flagrant crime of the type supposedly demonstrated every day by Deutsche Bank and which should not exist in a regulated market) will be an institutionally bifurcated and legitimized playing field, one in which those who can afford faster, bigger, more effective data pipes, collocated servers and response times - and thus riskless trades - outperform everyone else who may or may not know that the market is legally rigged against them. Think of it as baseball game for those who take steroids vs a 'roid free game, only here the steroids are perfectly legal for those who can afford them. Or like a casino where the house, or in this case the HFTs, always win. However, as it turned out, the vast majority of the public had no idea that a small subset of the market was juicing, despite our constant reports on the topic since 2009, until the arrival of Michael Lewis' book Flash Boys, which explained the secret sauce that made all those HFT prop shops into unbeatable "trading titans": frontrunning. That's really all one had to know about the mystical inner working of the modern market. All Reg NMS did was legitimize and legalize frontrunning at a massive scale for those who could afford (and hide) it, all the while the technology race ran in the background making it increasingly more expensive to stay at the top: fiber optics, microwaves, lasers, FPGAs, PCI-Express and so on. And, as we have also discovered in recent years especially since the advent of IEX, for many exchanges providing a two-tiered marketplace was the lifeblood of the business model: the bulk of the revenues for "exchanges" such as BATS and Nasdaq would come from selling non-HFT retail and institutional orderflow to HFT clients. Since the HFTs made far more than the invested cost in permitting such perfectly legal frontrunning, they were happy, the exchanges were happy too as they betrayed only those clients who didn't pay up the "extra fee", and only the true outsiders lost. And any time they complained how rigged the system was against them, the HFTs would scream that "they provide liquidity" as they are the real modern-day market makers. Except that's not true: the only time HFTs provide liquidity it when it is not needed. When liquidity is truly scarce and required in the market, such as on days like the May 2010 flash crash, or August 2015... they disappear. Meanwhile, nothing changes, because the regulators are just as corrupt as the exchanges and the HFTs, and their role is not to bring transparency to a broken, manipulated market, but to keep retail investors in the dark about just how rigged everything is. It appears that the CME was doing just that as well. According to Bloomberg, the CME Group - the world's largest exchange operator - just completed an "upgrade" traders said would eliminate a shortcoming that gave some participants an advantage. Under the old system, data connections that linked customers to CME - where key products like Treasury futures and contracts tied to the Standard & Poor's 500 Index trade - had noticeably different speeds, opening up the potential for gaming, according to traders and other experts. Those who knew how to gain faster access could increase their odds of being first in line to trade. The new design supposedly stamps that out. Oh, so it was a design glitch that allowed those who "knew" how to frontrun everyone else to do so. That's the first time we have heard of the particular excuse. Usually the scapegoat is a "glitch", only in this case the CME didn't even bother. "It's an excellent step forward," said Matthew Andresen, co-owner of Headlands Technologies LLC, a quantitative trading firm. "The new architecture is flat and fair, a great improvement," said Andresen, whose knowledge of market infrastructure goes back to the 1990s, when he worked for electronic trading pioneer Island ECN. But, wait... if it is an "excellent step" that some traders can no longer frontrun other traders on the CME, why is it not a "poor step" that virtually every other exchange still enables precisely this kind of tiered marketplace, which is neither flat nor fair? Actually, scratch that: that's precisely what IEX is trying to resolve. The reaction? An exchange which explicitly profits from providing a two-tiered market and charging an arm and a leg for those who can afford it (and thus frontrun everyone else) namely the Nasdaq, has threatened to sue the SEC if it permits IEX to become a full-fledged stock exchange. As Bloomberg adds, the situation involving CME's data connections highlights a fresh set of difficulties ensuring a level playing field in the era of light-speed markets, in which even the smallest bits of a second matter. The race to shave off milliseconds has spurred efforts to carve through mountains, span continents with microwave networks and prompted a backlash championed by the likes of IEX Group Inc., the upstart stock market that delays trading to impose fairness. Unlike some of today's state of the art means of being faster than everyone else, frontrunning orderflow on the CME was more of a "brute force" mechanism: CME customers are allotted data connections to the exchange. Some have more, some have less. Given that their speeds varied noticeably under the old architecture, the more lines a trading firm had, the better odds it could find a faster one. Trading firms with a lot of links had the chance to fish around for the fastest way to get trades done. Other firms that didn't have as many connections or the computer programming resources to test around and find the quickest, most efficient way in were at the mercy of the connections they had. "The performance could vary widely" with data connections under the former CME architecture, Andresen said. By which he meant that those who could afford to pay much more than everyone else, would also be able to frontrun almost everyone else. But no more. The new system "is an important innovation that will set a new standard for fair and efficient access to the futures markets," said Benjamin Blander, managing member of Radix Trading, a Chicago-based trading firm. CME declined to comment on claims the old system was unfair, Bloomberg adds. "We are continuously enhancing our infrastructure in order to provide the latest and best technology architecture for our clients," said Michael Shore, a spokesman for CME. CME has been installing the new architecture since February. The last group of futures and options became available on the new system last week, according to CME. Traders aren't required to switch over to the new system and can keep trading the old way if they want. This isn't the first time CME revamped its systems to stamp out an imperfection. Before an upgrade more than two years ago, traders were notified that their own orders were completed before everyone else found out, potentially giving initiators of transactions time to buy or sell on other exchanges with knowledge of their executions. We expect more violations of "accidentally" rigged markets to be uncovered in time, both on the CME and elsewhere, although we wonder at this time does it even matter: besides central banks trading with other central banks (especially courtesy of the CME's own Central Bank Incentive Program), does anyone else even bother? If judging by the total collapse in trading volumes over the past decade in virtually every product class, the answer is clear. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 23 May 2016 06:50 PM PDT Submitted by Jeff Thomas via InternationalMan.com, In 2014, we published an article entitled “Watch the Movie Before It Is Filmed.” In that article, I described the situation in Venezuela at that time. The effects of fifteen years of collectivism were threatening to collapse the economy. The government was reacting by printing bolivares (Venezuelan currency) on a large scale—a knee-jerk solution that has been utilized by over twenty other countries in the last century—always with the same outcome: hyperinflation, resulting in economic collapse. At the time, I recommended to readers that they “watch the movie” as it was being played out in Venezuela, as it would offer them insight into what was on the way in their own country, should they reside in Europe or North America. The pattern followed by Venezuela is roughly the same as for the other jurisdictions; Venezuela is just a bit more advanced in the progression. Therefore, what we are observing in Venezuela is likely to be played out in other countries that have made the same mistake of taking on more debt than they can ever pay back. As predicted, Venezuela is now well along with regard to hyperinflation. The traditional definition of “inflation” is “the increase of the amount of money in circulation.” Today, we think of inflation as an increase in the cost of goods, but this is merely a predictable by-product of inflation. If the amount of money increases, the cost of goods will always rise to meet it. Therefore, the issuance of large amounts of paper money has only a very temporary positive effect. Ultimately, it creates an increase in the price of goods and services, which, in turn, calls for further printing. In 1922, Germany was up to its eyes in debt, to the point that it was beyond repayment. The government, in attempting to overcome the dire poverty that had developed, decided to print more paper banknotes. The printing didn’t (and couldn’t) solve the problem, so they printed more. Then more again. They kept up the printing, until, by the autumn of 1922, the reichsmark was worth so little that new bills were being delivered to the banks in boxcars. A story of the time describes a man bringing a wheelbarrow of reichsmarks to a baker to buy a loaf of bread. Whilst in the shop, making the deal with the baker, he was robbed—the wheelbarrow full of money that he had left out on the sidewalk had been stolen. The thief dumped the reichsmarks on the pavement and made off with the wheelbarrow.

Above, we see a photo from the time—a wheelbarrow full of reichsmarks. Next to it, we see a photo from present-day Venezuela—a wheelbarrow full of bolivares. So, are the leaders of Venezuela learning from the mistakes of other countries that have followed this pattern? Far from it. Recently, they took delivery of over five billion banknotes—enough to fill three dozen 747 cargo planes. At the same time, Venezuela is selling off its gold in order to pay for the new currency and other debts. Venezuela will soon run out of real money to pay for the fiat money, and that will bring the charade to a disastrous end. The reader may say to himself, “When will people learn?” Sadly, they don’t. Incredibly, when the reichsmark collapsed in 1923, no one blamed the excessive printing. In fact, many people felt that if only the printing had continued just a bit longer, everything might have been all right. What we can take away from this is that what happened in Weimar Germany in 1922–1923 is happening now in Venezuela in 2016. (And has happened in some twenty other countries over the last hundred years, most recently in Argentina in 2000 and in Zimbabwe in 2008.) The same will occur in Europe and America in the fairly near future. That’s not a “Chicken Little” overreaction; it’s a virtual certainty. The same economic errors always bring the same catastrophic results. Ben Bernanke, just two years prior to being named head of the Federal Reserve, assured an audience that the Fed would react to any deflationary trend by printing as many currency notes as necessary. This was no idle threat. Remember, the owners of the Fed profit heavily from the hidden tax of inflation, but lose money if there is deflation. That assures us that, with the present unsustainable level of U.S. national debt (nominally, some nineteen trillion dollars, but actually some hundred trillion dollars, including unfunded liabilities), a collapse in the dollar is a given. And, of course, the severity of the crash is always commensurate with the level of the debt, which promises us that, since this debt load is by far the greatest the world has ever seen, the crash will be the greatest the world has ever seen. Those who have studied the histories of countries after they’ve experienced a hyperinflationary collapse will be aware of what’s headed their way, if they reside in Europe or North America. Those who have not undertaken such a study might choose instead to watch the movie—to observe what happens in Venezuela as its hyperinflation plays out and learn what their own fate might be. Our predicted outcome, which may have seemed hypothetical in 2014, is now right around the corner in Venezuela. This will be of value to the reader who watches as the collapse occurs, then observes what follows. The events that unfold will be essentially the events that will unfold in Europe and North America when their respective collapses occur. This “movie” is not meant to be entertainment at the expense of others’ suffering; watching it is a way to forewarn oneself as to what’s coming to those countries that are irrevocably on the same path, but have not yet reached the same point. By watching, the reader may be forewarned as to how to prepare himself so that, whilst his country may be headed toward economic collapse, he may take action to assure that the impact to himself, his family and his investments are diminished. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

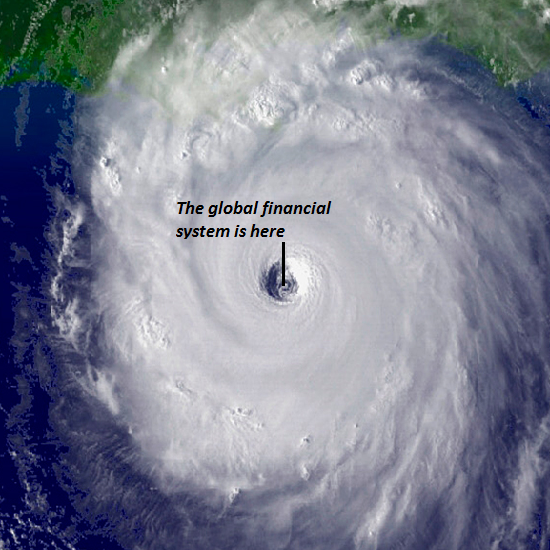

| We're In The Eye Of A Global Financial Hurricane Posted: 23 May 2016 06:46 PM PDT Submitted by Charles Hugh-Smith via OfTwoMinds blog, The only "growth" we're experiencing are the financial cancers of systemic risk and financialization's soaring wealth/income inequality. The Keynesian gods have failed, and as a result we're in the eye of a global financial hurricane.

The Keynesian god of growth has failed. The Keynesian god of borrowing from the future to fund today's consumption has failed. The Keynesian god of monetary stimulus / financialization has failed. Every major central bank and state worships these Keynesian idols: 1. Growth. (Never mind the cost or what kind of growth--all growth is good, even the financial equivalent of aggressive cancer). 2. Borrowing from the future to fund today's keg party, worthless college diploma, particle board bookcase, stock buy-back, etc. (oops, I mean "investment")--a.k.a. deficit spending which is a polite way of saying this unsavory truth: stealing from our children and grandchildren to fund our lifestyles today. 3. Monetary stimulus / financialization. If private investment sags (because there are few attractive investments at today's nosebleed valuations and few attractive investments in a global economy burdened with massive over-production and over-capacity), drop interest rates to zero (or below zero) to "stimulate" new borrowing... for whatever: global carry trades, bat guano derivatives, etc. Here is my definition of Financialization: Financialization is the mass commodification of debt and debt-based financial instruments collaterized by previously low-risk assets, a pyramiding of risk and speculative gains that is only possible in a massive expansion of low-cost credit and leverage. That is a mouthful, so let's break it into bite-sized chunks. Home mortgages are a good example of how financialization increases financial profits by jacking up risk and distributing it to suckers who don't recognize the potential for staggering losses. In the good old days, home mortgages were safe and dull: banks and savings and loans institutions issued the mortgages and kept the loans on their books, earning a stable return for the 30 years of the mortgage's term. Then the financialization machine revolutionized the home mortgage business to increase profits. The first step was to generate entire new types of mortgages with higher profit margins than conventional mortgages. These included no-down payment mortgages (liar loans), no-interest-for-the-first-few-years mortgages, adjustable-rate mortgages, home equity lines of credit, and so on. This broadening of options (and risks) greatly expanded the pool of people who qualified for a mortgage. In the old days, only those with sterling credit qualified for a home mortgage. In the financialized realm, almost anyone with a pulse could qualify for an exotic mortgage. The interest rate, risk and profit margins were all much higher for the originators. What's not to like? Well, the risk of default is a problem. Defaults trigger losses. Financialization's solution: package the risk in safe-looking securities and offload the risk onto suckers and marks. Securitizing mortgages enabled loan originators to skim the origination fees and profits up front and then offload the risk of default and loss onto buyers of the mortgage securities. Securitization was tailor-made for hiding risk deep inside apparently low-risk pools of mortgages and rigging the tranches to maximize profits for the packagers at the expense of the unwary buyers, who bought high-risk securities under the false premise that they were "safe home mortgages." Financialization-- which can only expand to dominate an economy if it is supported by a central bank bent on expanding credit--has two inevitable and highly toxic consequences: -- Risk seeps into every nook and cranny of the financial system, greatly increasing the odds of a systemic domino reaction in financial meltdowns. This is precisely what we saw in the 2008-09 Global Financial Meltdown (GFM): supposedly "contained" subprime mortgages toppled dominoes left and right, bringing the entire risk-saturated system to its knees. -- Extraordinary wealth and income inequality, as those closest to the central bank money/credit spigots can scoop up income-producing assets first at much lower costs than Mom and Pop Main Street investors. The rising anger of the masses left behind by the central bank / financialization wealth harvesting machine is the direct result of Keynesian monetary stimulus that rewards debt-based speculative gambles by those closest to the cheap-credit spigots. As I explain in my book Why Our Status Quo Failed and Is Beyond Reform, the only possible output of central bank monetary stimulus is financialization, and the only possible output of financialization is unprecedented wealth and income inequality. The global financial system is in the eye of an unprecedented hurricane. While central bankers are congratulating themselves on their god-like mastery of Nature, and secretly praying to the idols of the Keynesian Cargo Cult every night, the inevitable consequence of borrowing from the future, the obsession with "growth" at any cost and financialization /monetary stimulus, a.k.a. the rich get richer thanks to central banks is systemic collapse. Don't fall for the mainstream media and politicos' shuck-and-jive that all is well and "growth" will return any day now. The only "growth" we're experiencing are the financial cancers of systemic risk and financialization's soaring wealth/income inequality. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Banks must defend Libor lawsuits after judges warn of impact Posted: 23 May 2016 05:49 PM PDT By Bob Van Voris Sixteen of the world's largest banks, including JPMorgan Chase & Co. and Citigroup Inc., must face antitrust lawsuits accusing them of hurting investors who bought securities tied to Libor by rigging an interest-rate benchmark, a ruling that an appeals court warned could devastate them. The appellate judges reversed a lower-court ruling on one issue -- whether the investors had adequately claimed in their complaints to have been harmed -- while sending the cases back for the judge to consider another issue: whether the plaintiffs are the proper parties to sue, in part because their claims, if successful, provide for triple damages that could overwhelm the banks. "Requiring the banks to pay treble damages to every plaintiff who ended up on the wrong side of an independent Libor‐denominated derivative swap would, if appellants' allegations were proved at trial, not only bankrupt 16 of the world's most important financial institutions, but also vastly extend the potential scope of antitrust liability in myriad markets where derivative instruments have proliferated," the U.S. Court of Appeals in New York said in the ruling. Bank of America Corp., HSBC Holdings Plc, Barclays Plc, Credit Suisse Group AG, Deutsche Bank AG, Royal Bank of Canada, and Royal Bank of Scotland Group Plc are also among the banks sued in Manhattan. ... ... For the remainder of the report: http://www.bloomberg.com/news/articles/2016-05-23/banks-are-ordered-by-c... ADVERTISEMENT We Are Amid the Biggest Financial Bubble in History; With GoldCore you can own allocated -- and most importantly -- segregated coins and bars in Switzerland, Singapore, and Hong Kong. Switzerland, Singapore, and Hong Kong remain extremely safe jurisdictions for storing bullion. Avoid exchange-traded funds and digital gold providers where you are a price taker. Ensure that you are outright legal owner of your bullion. If you do not own segregated bullion that you can visit, inspect, and take delivery of, you are exposed. Crucial guides to storage in Singapore and Switzerland can be read here: http://info.goldcore.com/essential-guide-to-storing-gold-in-singapore http://info.goldcore.com/essential-guide-to-storing-gold-in-switzerland GoldCore does not report transactions to any authority. Safety, privacy, and confidentiality are paramount when we are entrusted with storage of our clients' precious metals. Email the GoldCore team at info@goldcore.com or call our trading desk: UK: +44(0)203-086-9200. U.S.: +1-302-635-1160. International: +353(0)1-632-5010. Visit us at: http://www.goldcore.com Support GATA by purchasing recordings of the proceedings of the 2014 New Orleans Investment Conference: https://jeffersoncompanies.com/landing/2014-av-powell Or by purchasing DVDs of GATA's London conference in August 2011 or GATA's Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold is having an unusual rising correction, Turk tells KWN Posted: 23 May 2016 03:50 PM PDT 6:49p ET Monday, May 23, 2016 Dear Friend of GATA and Gold: GoldMoney founder and GATA consultant James Turk tells King World News today that gold is going through an unusual rising correction. Either many buyers are awfully eager to buy the dips, Turk says, or investors fear that something nasty is imminent for the world financial system and figure that gold is necessary insurance. An excerpt from Turk's interview is posted at KWN here: http://kingworldnews.com/james-turk-this-is-why-gold-is-headed-much-high... CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT Free Storage with BullionStar in Singapore Until 2016 Bullion Star is a Singapore-registered company with a one-stop bullion shop, showroom, and vault at 45 New Bridge Road in Singapore. Bullion Star's solution for storing bullion in Singapore is called My Vault Storage. With My Vault Storage you can store bullion in Bullion Star's bullion vault, which is integrated with Bullion Star's shop and showroom, making it a convenient one-stop-shop for precious metals in Singapore. Customers can buy, store, sell, or request physical withdrawal of their bullion through My Vault Storage® online around the clock. Storage is FREE until 2016 and will have the most competitive rates in the industry thereafter. For more information, please visit Bullion Star here: Support GATA by purchasing DVDs of GATA's London conference in August 2011 or GATA's Dawson City conference in August 2006: http://www.goldrush21.com/order.html Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit: | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Four Events in April Set the Stage for the Rest of 2016 Posted: 23 May 2016 01:49 PM PDT This post Four Events in April Set the Stage for the Rest of 2016 appeared first on Daily Reckoning. [Editorial Note: The following was excerpted and edited from the Trends Journal. Click here for more information.] Before we head for summer and the endlessly looming, overcovered fall election, let's consider the desperate measures the four most powerful central banks have taken this year. Each has pushed its artisanal money policies to the limit, keeping markets, banks and (in their minds only) economies afloat through artificial manipulation, stimulation and value fabrication. This year's central bank interventions have exhibited more bipolarity than ever before. Speeches indicate one view one minute, another the next. What is said publicly for global consumption and privately for national intake varies. Infighting is escalating within the hallowed walls at monetary policy meetings. The Federal Reserve is trying to keep it all together, but cracks in the facade of the stability it is selling are growing wider and appearing with greater frequency. Volatility can be contained intermittently, not forever. This phase began when the Fed raised rates a smidge at the end of 2015. They then backtracked after realizing they couldn't control the Armageddon that would ensue in the event of an actual tightening policy. Following an 18% stock market drop in the Standard & Poor's 500 from Dec. 16 through Feb. 11 and a dismal January, Chairwoman Janet Yellen equivocated. Global economies, she maintained, remained too weak (like that was new). The other three central banks quickly fell into line, offering rate reductions, bond purchasing programs and required reserve reductions for national banks. The result? By April 18, the Dow Jones had risen above 18,000 points for the first time since July 2015. Since mid-February, the S&P 500 leapt 15%. China got big points in the business press for showing 6.9% annual GDP growth for 2015, even though it was the worst result in 25 years. (That's still impressive relative to other emerging countries. China is doing better than people think: Its government and central bank pockets are deep.) European Central Bank head Mario Draghi (aka "Super Mario") unleashed an overdrive monthly buying spree, expanding the ECB's quantitative easing program 33% (from 60 billion to 80 billion euros per month) and inviting corporate bonds into the tent. The Bank of Japan followed the ECB into negative interest rate territory and, like the ECB, began expressing the bizarre view that negative interest rates will do what zero rates couldn't. When all was said, but not done, a few new and more desperate themes poked above the parapet of the three major non-Fed central banks. Monetary policy is great, but it's not enough. Fiscal policy must follow. To me, this signals the last act of the Artisanal Money Show has begun. The blame game will take us to final curtain. Fade to black. How long can this show go on? Will global financial systems crack and liquidity die? Or will the Fed and its cohorts keep it going as the little people get sucked into a false sense of security — until it all comes crumbling down? I think the latter; the issue, as always, is timing. The bases are loaded with QE and ZIRP and NIRP. Will the Fed hit it out of the park before things come crashing down? Will pinch hitters from the other three teams do the deed? Or will the game be rained out — and we do it all over again tomorrow? Stakes are high, because the beginning of this year showed what happens if just one player, one major central bank, doesn't do its part. What's ahead for the rest of 2016? The answer lies partly in two back-to-back events that took place in Washington (naturally) in April. The first was a last-minute, nonpublic, no-transcripts-disclosed meeting between Yellen and President Obama. There was no mention of the meeting on the Fed's website's "All Press Releases" section. The announcement of the 3 p.m. Monday meeting at the Oval Office was made by the White House on Sunday night. (Vice President Joe Biden also was scheduled to attend.) The second event was a joint press release two days later from the Federal Reserve and the Federal Deposit Insurance Corp. It effectively indicated that seven of the eight systemically important ("too big to fail") U.S. banks would need another HUGE bailout (as opposed to the cheap money that lubricates them now) in a crisis. Let's dig a little deeper. This story starts on April 11th… Janet Yellen attended an unscheduled "secret" meeting with Obama at the White House. The markets and business media launched into overdrive speculation mode as to what it could mean. The Fed offered no explanation. The White House posted a vague morsel, claiming the encounter was (bold mine):

None of that sounds like something that can't be discussed on the phone — or through email or even text message — except the passage in italics, which is a complete lie. Here the plot thickens. The most recent byproduct of the extensive coddling of the banking system has morphed into a political tool for extending the Clinton-Obama-Clinton administrations. Two days later… On April 13, the FDIC and Fed noted that five of eight "systemically important" US banks had failed to deliver adequate 2015 (and legally required as per the Dodd-Frank Act) living wills — or "resolutions" in the event of another financial crisis. The Board of Governors of the Federal Reserve System and FDIC jointly determined that: "Each of the 2015 resolution plans of Bank of America, Bank of New York Mellon, JPMorgan Chase, State Street, and Wells Fargo was not credible or would not facilitate an orderly resolution under the U.S. Bankruptcy Code, the statutory standard established in the Dodd-Frank Wall Street Reform and Consumer Protection Act." They gave these five firms until Oct. 1, 2016 to address their "deficiencies." But, they have until 1 July 2017 to file another living will. (Perhaps that will occur by the time Trump submits his audited tax returns; who knows?) But more likely, they will be given a clean bill of health in October into the general election to complete the fantasy of the Fed and Obama administration fixing the crisis, economy, Wall Street and the universe. The agencies also identified weaknesses in the 2015 resolution plans of Goldman Sachs and Morgan Stanley. The FDIC determined Goldman Sachs' plan "was not credible or would not facilitate an orderly resolution." The Fed concurred for Morgan Stanley's plan. If you're keeping score, that's seven of the eight banks that could re-crater the economy. Who's left? Both agencies identified shortcomings for Citigroup to address. Yet, they gave the firm — at which Bill Clinton's Treasury secretary, Robert Rubin, had a plum position in the buildup to the 2008 crisis, as did Obama's current Treasury secretary (and deputy secretary for Hillary Clinton when she was secretary of state), Jack Lew — the only thumbs up. Citigroup. That's what they're going with. We're screwed. TREND FORECAST: The Fed won't raise rates in June because it can't afford the possible political repercussions domestically and internationally. Banks will magically appear healthy in October around earnings time. Volatility will increase as the election approaches due to bets on what the Fed will do and because nothing's truly fixed. Again. Then, The Day After That… Meanwhile, in China. After the G20 Finance Ministers and Central Bank Governors Meeting April 14 and 15 in Washington, the People's Bank of China issued this public statement:

China isn't thrilled with playing backup to the Fed's monetary-policy initiatives, being joined at the hip to the Fed or being chastised for considering concerns of its own economy over the needs of the US. It never has been. As such, the bank added:

China will continue to have debt and leverage problems, but will keep the Yuan stable against the dollar to avoid dealing with US complaints of "manipulation" and will talk its markets up when it can. And Then, a Week After That… Back in Tokyo, Haruhiko Kuroda, governor of the BOJ, has been saying the Bank of Japan, submitted his Semiannual Report on Currency and Monetary Control on April 20. Kuroda accentuated the falsehood of economic recovery being based on negative rates. "Japan's economy has continued its moderate recovery trend." (The Bank of Japan has been saying the economy is "recovering at a moderate pace" since 2009.) Taking the Fed and ECB's side, he stuck it to China a bit, adding:

Kuroda confirmed that his bank's "Quantitative and Qualitative Monetary Easing With a Negative Interest Rate" policy would continue, "in combination with continued large-scale purchases of Japanese government bonds," known as JGBs. He added that the BOJ "will not hesitate to take additional easing measures in terms of three dimensions — quantity, quality and the interest rate" if necessary. The Bank of Japan will do what it says, keeping rates negative and buying JGBs, which should depress the yen from its recent elevation against the dollar in the near future. The Result? Central Bank Dissension Will Grow… Finger-pointing between central bankers and their governments, and internal dissension, will grow… In Europe, Germany Finance Minister Wolfgang Schäuble has been the main critic of the ECB's and Draghi's "flexible" monetary policy. Angela Merkel has been politically cautious on this issue, noting it is legitimate for Germans to discuss interest rates and effects on German society, but "that shouldn't be confused with interference in the independent policy of the ECB, which I support." Playing both sides is not a sign of confidence in the ECB, but insecurity about her own political future. As Schäuble publicly expresses concerns about Draghi's god complex, Draghi is fighting back. On March 17, he held a private meeting in Brussels at which he conveyed to European Union leaders that the ECB has "no alternative" to its recent rate cuts and monetary-policy decisions. To the press, he covered his ass and stuck it to Schäuble, saying, "I made clear that even though monetary policy has been really the only policy driving the recovery in the last few years, it cannot address some basic structural weaknesses of the eurozone economy." Europe is a hot mess. The banks of Portugal and Italy, in particular, are on life support. Trading desks are figuring out how to trade the other side of the ECB's corporate bond-buying program, which could mean a London-Whale-type scenario, where corporate bond spreads do the opposite and widen dramatically. At the Fed, there will be more grumbling, as Yellen keeps finding new reasons to keep the current policy. When the Federal Open Market Committee released its March 16 statement about keeping rates where they were, only Fed member Esther L. George was against the decision. The following week, Yellen faced more internal opposition. Four of the 17 members (including George) openly disagreed with her dovish strategy. Undaunted, at a March 29 speech at the Economic Club of New York, Yellen announced that for the next few months, the Fed's strategy would be to pursue only gradual increases in federal fund rates, showing a dovish perspective. That was two weeks before the Obama meeting. The meeting and timing signaled the beginning of the end of coordinated central-bank policy. But for now, we remain in play. I have said that at the most, the Fed would raise rates by 50 basis points this year in, at the most, two 25-basis-point increments. But given the election situation and volatility accentuation of other central-bank leaders, I now think we're looking at only one 25 basis-point move this year at the most. This means the US stock market will trade in a volatile range until the election. Regards, Nomi Prins [Editorial Note: The following was excerpted and edited from the Trends Journal. Click here for more information.] The post Four Events in April Set the Stage for the Rest of 2016 appeared first on Daily Reckoning. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 23 May 2016 01:30 PM PDT This post Are Investors Idiots? appeared first on Daily Reckoning. BALTIMORE, Maryland – "It's easy to criticize," the President of the University of Vermont seemed to be looking in our direction. "But cynicism doesn't help build a better world." It's the season for weddings and graduations. We had one of each this past weekend… a wedding in Delaware and then a graduation in Vermont. Both brought tears. Fraud and FoolishnessThe wedding took place on an old Dupont estate that has been converted into a country club. Elizabeth's goddaughter, a beautiful redhead, got married to a handsome and charming young black man. This cross-race marriage would have been shocking in the Maryland of our youth. On Saturday, it seemed perfectly natural. Times change. We couldn't stay for the drinking and dancing, however. Our youngest son was to graduate from the University of Vermont on Sunday; we had to hit the road.

The ceremony in Burlington was our fifth one. Saint John's College… Davis and Elkins… Boston University… University of Virginia… We've been to "commencement" celebrations at them all. And all were full of fun, fraud, and foolishness. The University of Vermont was a standout in all three ways… But we'll come back to that tomorrow… Let's at least begin the week "on message." The Diary is about money. Today, we'll stick to the subject. Black-and-Blue Crash Alert FlagOld friend Mark Hulbert has done some research on the likelihood of a crash in the stock market. Writing in Barron's, he points out that the risk… or, more properly, the incidence… of crashes, historically, has been very small:

Whoa! Are investors idiots, or what? Maybe not. Your editor is among those who happily over-estimate the risk of a crash. He expected one in 1998… and again in 1999… and when it came in 2000, he was as surprised as anyone. Then, prices went up again. And again, he raised the old black-and-blue Crash Alert flag. In 2005… in 2006… in 2007… finally, in 2008, he got what he expected. And now that the market has recovered again… he expects another one. Investors and TurkeysStatistically, as Mark points out, the likelihood of a crash coming on any given day is small. But that is a little like telling a turkey not to worry because the likelihood of Thanksgiving is only 1 out of 365. Eventually, all turkeys and all investors get whacked. And, generally, the longer a market goes without a correction, the more it needs one. Besides, there is something a little fishy about these numbers. In the last 20 years, there were the aforementioned sell-offs in the stock market – one in 2000, heavily concentrated in the Nasdaq… and the other across the board in 2008. But people don't think of investing in terms of avoiding the specific day of crash. Investors don't really care if a crash happens on a Wednesday or a Thursday. If they think a crash will happen any time within six months, they usually want to stay out of the market… realizing that they can't time these sorts of things with any precision. So if we look at it in these terms… there were 40 six-month periods in the last 20 years. And crashes happened in two of them… or one in 20. If investors truly believed that the odds of a crash were 28 times higher than one in 20, they would have believed that there would be a crash EVERY SIX MONTHS. And they would have been out of stocks all the time. It's Like Russian RouletteAlso, the statistics Mark cites do not really gauge the "risk" of a crash. They speak only to the frequency. Imagine the drunken imbecile who puts a bullet into a revolver, spins the chamber, and puts the gun to his temple. "There's only one chance in six that this will kill me," he says. Statistically, he is right. The odds are in his favor. But what a bad bet! The true measure of risk involves more than just statistical probability. The frequency needs to be multiplied by the gravity in order to get the true picture. The typical investor is in his 50s. If the next stock crash is followed by a big bounce… like the other two crashes in the last 20 years… he will be glad he paid no attention to our warnings and just kept his money in stocks. But what if the stock market crash of 2016 is more like the crash of '29… or the bear market of '66? He could have to wait 20 years to break even. Or if it is like the crash that happened in Japan in 1990, he'll still be waiting in 2042. Regards, Bill Bonner P.S. Another dollar crisis is coming. It's not a question of if, but when. And gold could soar to record levels when it strikes. If you own gold beforehand, you can preserve – and grow – your wealth. That's why we've produced a FREE special report called The 5 Best Ways to Own Gold. Don't buy any gold until you read it. We'll send you your report when you sign up for the free daily email edition of The Daily Reckoning. Every day you'll get an independent, penetrating and irreverent perspective on the worlds of finance and politics. And most importantly, how they fit together. Click here now to sign up for FREE and claim your special report. The post Are Investors Idiots? appeared first on Daily Reckoning. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gold Daily and Silver Weekly Charts - Option Expiry on the Comex - History Lesson Posted: 23 May 2016 01:15 PM PDT | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 23 May 2016 11:38 AM PDT Donald Trump on UK Brexit and the special relationship between Britain and America. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many more [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| #Brexit: #ProjectFear is Ridiculous Posted: 23 May 2016 11:00 AM PDT The arguments against #Brexit have reached unbelievable levels of hysteria. The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many more [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Tomorrow the Eurozone Determines Greece’s Fate Posted: 23 May 2016 10:02 AM PDT This post Tomorrow the Eurozone Determines Greece’s Fate appeared first on Daily Reckoning. And now… today's Pfennig for your thoughts… Good day, and a marvelous Monday to you. Well, have you felt the BIG SHIFT? I sure did, and am still scratching my balding head and wondering where did this BIG SHIFT in sentiment by the Fed toward a rate hike in June come from? But it’s there for sure. And to just enforce that the BIG Shift (BS) pun intended, the Fed will send at least six more speakers out this week to talk, including Fed Chair, Janet Yellen, who speaks on Friday. There really isn’t a plethora of economic data on the docket this week, so these speakers will carry the ball for the resurgent dollar. In fact, I don’t think we’ll see any “real economic” data until Thursday when Durable Goods/ Capital Goods Orders print. That’s very fortunate for the Fed speakers in my opinion, as they won’t have to be looking over their shoulder for a weak economic report that just printed while they talk about hiking rates in June. The dollar has turned down the heart on the burner to simmer this morning. You can tell that the dollar still has the upper hand, but for the most part, the currencies are trading in the same clothes as Friday, which means that the dollar is softer as a whole. Yes, there are some currencies getting the snot knocked out of them, and some currencies that are carving out gains, but for the most part, it’s a day of calm, so far. Remember a couple of weeks ago, when I told you that May 24th was the next day to watch regarding Greece and the Eurozone Finance Ministers. And guess what? Tomorrow is May 24th! It’s here already! It appears that everyone is playing nicely in the sandbox, as the Greek Parliament easily approved the measures that creditors required of them, and now it appears that a euro 10 billion in program funds will be issued to Greece, which, get this, will allow them to pay their debt that’s due next week to the Eurozone. Did you follow that? The Eurozone will give Greece the money they need to pay the Eurozone back. Why didn’t they just give them an extension on the amount due? Ahhh, because Greece doesn’t have the money to pay back the loans whether you have it due this week, next week or next year, or the next five years for that matter! I won’t say never, because miracles do happen. Speaking of the Eurozone the euro is still holding the 1.12 handle by the skin of its teeth, but could see a bump coming this week when their latest PMI’s (manufacturing indexes) print. The recent prints by month have looked steady Eddie for the Eurozone, and another steady Eddie print or even a bump higher in the index would sure underpin the euro for this week. The Japanese yen is bit stronger this morning as their latest Trade Balance printed last night, and believe it or don’t but their Trade Balance returned to a Surplus! The April Trade Surplus was yen 824 billion, which beat the expectations of yen 755 billion. I think what this Surplus hides is the fact that import trends continue to drop in Japan. And that’s not a good thing for the domestic economy. Yes, I always say a surplus is a good thing, and it is. But you’ve got to look around the corner here to find that there are unintended consequences with this Trade Surplus for Japan, and that is, no domestic demand. The Bank of Canada (BOC) will meet on Wednesday this week. I don’t expect any rate movements from the BOC on Wednesday, but I’ll bet a dollar to a Krispy Kreme that BOC Gov. Poloz will find the time to mention the strength of the Canadian dollar/loonie. The loonie, even though it has backed off recent highs is still two-cents above where it was at the last BOC meeting, and they were hemming and hawing about it then. So, look for Poloz to say something that could weaken the loonie this week. But remember, it’s only words. Loonie traders have to remember that sticks and stones my break their bones, but words should never hurt them! The price of oil is sniffing around $48 this morning, as it is trading at $47.88. It sure looks like to me that oil is hell bent and whiskey bound to reach $50 this summer. I was reading some research on the price of oil this weekend, and found a trader that has tied the performance of the oil price to the yield of the 2-year Treasury. So, if you believe the BS/Big Shift change, and that rates in the U.S. are going higher, then Treasury yields will go higher too, and if this relationship remains intact, then we could see the oil price reach $50, as I talked about here. Those sure were some powerful statements last Friday about household debt levels here in the U.S. weren’t they? You know, the economists have all been chastising the Fed for not hiking rates because the Fed was too concerned with global problems. The economists said that the Fed needed to just hike rates and be done with it. But what about these debt problems? Did you see that high percentage of people, no matter what salary range they were in, would struggle to make a $1,000 payment on something that came up? OMG! Wouldn’t it behoove the Fed to pay attention to these things? Household debt levels are so high, and guess what the credit card companies are going to do with a rate hike? Gold is flat this morning at $1,252.00. The shiny metal sure has had the stuffing kicked out of it in May. The month of May has been gold’s kryptonite. It will be interesting to see if gold can get back on the rally tracks in June. I somewhat think that it’s going to be a tough row to hoe for gold in June. First of all we have a plethora of things going on around the world including a Fed Rate meeting. But wait! What am I saying here? I completely forgot what I told Joseph and Chris last week in our monthly meeting, when I asked them the question (knowing the answer of course) “what has gold done since the Fed last hiked rates?” And of course we all knew that gold had not let the rate hike interfere with its rally. So, maybe, of course we never know, but maybe gold can pull that rabbit out of its hat again in June! The U.S. Data Cupboard is in need of data, but will scratch around and find the Flash PMI’s for May to print today. And the Fed speakers on the docket today are James Bullard, and John Williams, who’s been speaking a lot lately, and Patrick Harker. So, a trio of Fed speakers today, will all sing from the same song sheet and talk about the virtues of a rate hike in June, as the BS/Big Shift gets in motion. I found this on Bloomberg this morning. And I’m hoping it’s not going to come to fruition, as the old “risk on/risk off” trading drove me absolutely crazy! So, here’s the snippet from the report:

Chuck again.. Well, I’ve said all I need to say about risk on/risk off. I sure hope it goes away, and was just a false dawn. That’s it for today. I hope you have a marvelous Monday and be good to yourself! Regards, Chuck Butler P.S. Have you thought about investing in gold but don't know the best way to do it? Then you need to see the FREE special report we've produced called The 5 Best Ways to Own Gold. It answers all the questions you have. We'll send you your report immediately when you sign up for the free daily email edition of The Daily Reckoning. It combines hard-hitting information with charm and wit to bring you a unique perspective on the world. Click here now to sign up for FREE and claim your special report. The post Tomorrow the Eurozone Determines Greece’s Fate appeared first on Daily Reckoning. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Zionist Subversion of Western Civilization [Part 1] Posted: 23 May 2016 09:05 AM PDT "Whoever controls the media controls the mind" The Financial Armageddon Economic Collapse Blog tracks trends and forecasts , futurists , visionaries , free investigative journalists , researchers , Whistelblowers , truthers and many more [[ This is a content summary only. Visit http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| How the Fed Is Fooling You Again Posted: 23 May 2016 09:03 AM PDT This post How the Fed Is Fooling You Again appeared first on Daily Reckoning. Last week, Janet Yellen's flunkies rattled Wall Street by talking up an interest rate hike in June… Richmond Fed President Jeffrey Lacker told the Washington Post that the chance of a June rate hike was "pretty strong." And New York Fed President William Dudley said a June rate hike is a "reasonable expectation" based on the economy's strength. So, is Mao Yellen really going to turn off the easy money spigot that's been keeping stocks at all-time highs and Wall Street bankers flush with cash? Well, there's one easy way to tell. And it has nothing to do with what Yellen's PR agents at the Fed are pumping… The Only Data That MattersJanet Yellen loves to portray herself as a modern day Detective Joe Friday from the classic TV show "Dragnet"… Just the facts, ma'am! She dresses up as a no-nonsense public servant driven only by objective data. And under her leadership, she's constantly spinning that the Fed has never been more "data dependent." Yellen's fair-minded Fed is supposedly not influenced by the short-term gyrations of the S&P 500 Index. It only relies on "clean" domestic data on labor markets, inflation and economic growth to determine U.S. monetary policy. And when that data says it's time to adjust rates, that's what the Fed does. Except when it doesn't. You see, it's true that Yellen's Fed is data dependent. But it's mostly dependent on one piece of data. And that's the performance of the stock market. Here's a prime example… The Fed BlinkedIn December 2015, the Fed raised interest rates for the first time in six years. And it indicated more increases were on the way… The Fed said four rate hikes would happen in the coming year if core U.S. inflation went higher than 1.6% and unemployment hit 4.7% by the end of 2016. So what happened? Well, inflation had already hit the Fed's target before its March 2016 meeting. And unemployment was also well on its way to the 4.7% year-end target. In other words, the data had only made a stronger case for higher rates. So why did the Fed leave rates unchanged in March? Well, the S&P 500 collapsed more than 10% from the beginning of 2016 to mid-February. "Buy and hold" investors panicked at the thought of their easy money going bye-bye. They had already seen the collapse of Chinese stocks and oil, but the S&P plummeting caused a "Code Red." And the Fed blinked. It put rate increases on hold despite enormous economic data indicating it was time for a rate hike. And like clockwork, the S&P immediately rallied. That, ladies and gentlemen, is not following the data. That's engineering the data. Proceed With CautionKeep this "process" in mind the next time Yellen pretends her next move will be based on noble economic principles or "data only" models. Sure, the Fed says it pays attention to inflation and economic stats. But its one guiding principle since March 2009 is to levitate the S&P at any cost. And how could that not be the truth? Take a look at this chart. Fed interventions are perfectly correlated with stocks going to the moon.