Gold World News Flash |

- Bitcoin Absorbing Wealth From Precious Metals?

- Paul Craig Roberts – US Corruption & World Interference Failing

- Fashion Catches Up to Investment Demand for Gold Jewelry

- $1,000 For One Ounce of Silver? …Don’t Laugh! — Andy Hoffman

- The Weekend Vigilante – Freedom, Bitcoin and China

- The "Anti-Widowmaker" Trade: Get Paid To Wait For The Japanese House Of Card To Collapse

- China’s Debt Binge & Buying Spree Is About to Burst!

- China Literally Buying Gold By The Ton

- Russell Napier: "We Are On The Eve Of A Deflationary Shock "

- Guest Post: Economic Prosperity Ahead Or A Train A Comin'

- 1974 Enders To Kissinger: "We Should Look Hard At Substantial Sales & Raid The Gold Market Once And For All"

- Paul Craig Roberts - US Corruption & World Interference Failing

- Filling the China Cabinet With Gold

- Market Monitor – November 30th

- What's The Difference Between Markets & Reality? About 22% YTD

- Gold & Silver: “You have stayed for the pain, will you not stay for the gain?”

- This Inflation Is Supposed To Be GOOD For Japanese Workers?

- Comex Registered Gold Inventory Levels - 65 Potential Claims Per Ounce

- Comex Registered Gold Inventory Levels - 65 Potential Claims Per Ounce

- Ukraine President Explains Relations With Russia Using Body Language, While Local Violence Escalates

- This Past Week in Gold

- Gold And Silver - Reverse Bubble. Huge Rally When Broken. Note Bitcoin Results

- Silver and Gold as Currency Commodities

- Are Bitcoin's Better Than Gold? Crypto-Future of Trillion Dollar Digital Trading & Exchange?

- Gold And Silver Reverse Bubble. Huge Rally When Broken. Note Bitcoin

- Gold Investors Weekly Review – November 29th

- Gold Outlook – Love Trade And Fear Trade Likely To Return

- Junior Gold Stocks Rabbit Hole

| Bitcoin Absorbing Wealth From Precious Metals? Posted: 01 Dec 2013 12:00 AM PST from Trillion Dollar Silver: |

| Paul Craig Roberts – US Corruption & World Interference Failing Posted: 30 Nov 2013 11:30 PM PST from KingWorldNews:

I think the pricing of gold would then just move to the physical market. We see the demand for (physical) gold continues to rise. The reason we haven't seen the rising price, despite the rising demand, is the price is fixed in the paper gold market. |

| Fashion Catches Up to Investment Demand for Gold Jewelry Posted: 30 Nov 2013 10:00 PM PST from Wealth Cycles:

Of course, there are exceptions to every rule: if one were able to purchase gold jewelry at near the spot of the gold it contained, and if the quality of the gold it contained were guaranteed, then the value of gold jewelry as an investment would be sound. Fortunately, that type of gold jewelry investment product is now available. Even more serendipitously, the fashion world has recently embraced the chunky gold chain as the "now" jewelry statement. |

| $1,000 For One Ounce of Silver? …Don’t Laugh! — Andy Hoffman Posted: 30 Nov 2013 09:55 PM PST

Andy Hoffman from Miles Franklin joins us to for a clarion call about the true, real world value of PHYSICAL SILVER. With the market value of all available Bitcoins now more than $5 BILLION, compared to around $21 Billion for all investable PHYSICAL silver, Andy says “What we’re seeing is a speculative mania.” Andy reminds us that the Chinese are fed up, and have now publicly drawn a line in the sand AGAINST the US Dollar, “The Chinese just made this incredible announcement that they no longer want to accumulate currency reserves. That is probably the most bullish thing I have heard for precious metals in my twelve years of watching this.” “The Chinese have $3.6 TRILLION of currency reserves and they want OUT. There’s only $100 billion of gold mined in a single year, worldwide. And $15 Billion of silver. The point is that gold and silver are way undervalued compared to the amount of buying that’s going to be coming into them.” Back to Bitcoin, I ask Andy, if $1,000 USD is possible for a single Bitcoin, what is one ounce of physical silver really worth? Andy says, “Alternative currencies are a viable concept… but Bitcoin doesn’t have intrinsic value, whereas silver for instance is the second most used commodity on earth, in fact three quarters of ALL production is used for things other than investment.” As for concrete value for an ounce of physical silver, Hoffman’s take is this: “My long standing price target, if it weren’t rigged, I would say it should be $1,000 – $4,000 an ounce right now. And that’s simply using the math of how much money the government SAYS has been printed and how much gold they SAY they have in reserve. And of course they have printed a lot more than they say and they have a lot less gold than they say.” |

| The Weekend Vigilante – Freedom, Bitcoin and China Posted: 30 Nov 2013 08:00 PM PST by Jeff Berwick, Dollar Vigilante:

I am still here, but not for long, as I leave to Mexico City on Sunday night for a Monday interview by satellite with Max Keiser, then off to Miami for one night and then on to St. Kitts for the Liberty Forum conference on the beach with Peter Schiff, Doug Casey and many other greats to help to free some slaves. As I wrote last weekend, I barely feel like I know my own family as they change so much during my sometimes month-long sojourns. This didn´t improve much even though I was here for an entire week this time around. I saw my wife for perhaps a total of a few hours, but it wasn’t entirely my fault. |

| The "Anti-Widowmaker" Trade: Get Paid To Wait For The Japanese House Of Card To Collapse Posted: 30 Nov 2013 07:46 PM PST

- Harley Bassman, Credit Suisse That Japan's economy is doomed (as best seen in this chart), as are its government bonds, is unquestionable. There is simply no way the country, faced with an inescapable demographic collapse...

...can crawl its back to viability without imploding in an eventual deflationary singularity, from which, however, courtesy of the BOJ's epic printathon, it may eventually inflate away its debt, but not before crucifying its currency, and the living standards of its population. In other words, there is no realistic escape. This is not news. The problem is that for many - especially the Japanese experts - this has not been news for years and years, yet anyone and everyone who has so far bet on the collapse of the Japanese house of cards, has lost money if not gone bankrupt due to the negative carry or the time decay of any short options. Hence the name: the "widow-maker" trade. There may, however, be a loophole for all those who, correctly, know that the end of the line for Japan is just a matter of time. The trade in question is described by the "convexity maven" - Credit Suisse's Harley Bassman: The Trade Taking a "short position" in either Japanese interest rates or their currency is a fundamentally sound idea; however it may take three to seven years for the "Macro-profits" to be fully realized. Over that time, a short position will demand a cost, either in the terms of the negative carry of a spot position or the time decay of a short-dated option. Additionally, since it is unlikely you will enter the trade at the extreme, there could be some mark-to-market vibrations that may breach your risk limits. To the rescue is the strange circumstance of a widening USD vs. JPY Rate differential in conjunction with a flattening Volatility Term Surface. Below is a table of mid-market values for Par Strike USD call // JPY put options with expiries from one-year to ten-years. The critical observation is that a five-year option costs more than a ten-year option; thus the weird dynamic of owning an option with (effectively) positive "theta": You are paid to own an option ! This is neither financial "magic" nor an "option special"; these are all plain vanilla options than can be priced using Bloomberg's OVDV screen. Rather, it is merely the interesting mathematical paradox between the Rate process which is Linear and the Time process which is Logarithmic. In a nutshell, net interest income is linear to time so two years of coupon payments are twice the size as a single year's value. In contrast, an option's price increases with the square root of time, so a two-year option is only 1.4 times greater in price than a one-year option.

The easy execution of this idea is just to buy a ten-year call option and put it away for five years: Strike = 100; Price ~~ Customer pays 7.375% The more interesting trade might be to execute a five-year vs. ten-year calendar: Sell five-year vs. Buy ten-year, Strikes = 100; Client receives 0.50% Summary 1) The maximum loss for an out-right purchase is limited to the fee paid; The lesson from so many of the great Macro Investments Themes is that it sometimes takes the "fullness of time" to realize the largest profits. Unfortunately, the current environment has less patience to tolerate investment costs, as such a "Positive Carry" long option position should be quite interesting. The Japanese financial situation will normalize at some point; being "paid to wait" for the first five years solves the thorny problem of trying to time that date. |

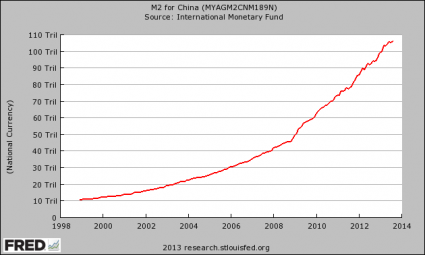

| China’s Debt Binge & Buying Spree Is About to Burst! Posted: 30 Nov 2013 05:21 PM PST When it comes to reckless money creation, China is the king. Over the past five years So says Michael Snyder (theeconomiccollapseblog.com) in edited excerpts from his original article* entitled China Is On A Debt Binge And A Buying Spree Unlike Anything The World Has Ever Seen Before. [The following is presented by Lorimer Wilson, editor of www.FinancialArticleSummariesToday.com and www.munKNEE.com and the FREE Market Intelligence Report newsletter (sample here – register here). The excerpts may have been edited ([ ]), abridged (…) and/or reformatted (some sub-titles and bold/italics emphases) for the sake of clarity and brevity to ensure a fast and easy read. This paragraph must be included in any article re-posting to avoid copyright infringement.]Snyder goes on to say in further edited excerpts: Chinese bank assets have grown from about 9 trillion dollars to more than 24 trillion dollars. In just five years:

I was curious to see what all of this debt creation was doing to the money supply in China. So I looked it up, and I discovered that M2 in China has grown by about 1000% since 1999… What has China been doing with all of that money? [China is Buying Up the World – Big Time! Take a Look and China's Foreign Investment Spending ($443 Billion) by Country] Well, they have been on a buying spree unlike anything the world has ever seen before:

Unfortunately for the Chinese, it appears that the unsustainable credit bubble that they have created is starting to burst. According to Bloomberg, the amount of bad loans that the five largest banks in China wrote off during the first half of this year was three times larger than last year…and Goldman Sachs is projecting that China may be facing 3 trillion dollars in credit losses as this bubble implodes… The Chinese are trying to get this debt spiral under control by tightening the money supply. That may sound wise, but the truth is that it is going to create a substantial credit crunch and the entire globe will end up sharing in the pain… [Indeed, it] could ultimately be a much bigger story than whether or not the Fed decides to “taper” or not. It has been the Chinese that have been the greatest source of fresh liquidity since the last financial crisis, and now it appears that source of liquidity is tightening up so as the flow of “hot money” out of China starts to slow down, what is that going to mean for the rest of the planet and when you consider this in conjunction with the fact that China has just announced that it is going to stop stockpiling U.S. dollars, [China's Reining In of U.S. Treasury Purchases Will Precipitate U.S. Dollar Collapse] it becomes clear that we have reached a major turning point in the financial world. 2014 is shaping up to be a very interesting year, and nobody is quite sure what is going to happen next. [Editor's Note: The author's views and conclusions in the above article are unaltered and no personal comments have been included to maintain the integrity of the original post. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.]*http://theeconomiccollapseblog.com/archives/china-is-on-a-debt-binge-and-a-buying-spree-unlike-anything-the-world-has-ever-seen-before (Copyright © 2013 The Economic Collapse) Related Articles: 1. China is Buying Up the World – Big Time! Take a Look

China is buying up the world – big time! Take a look. It’s all shown here in one map. Read More » 2. China's Foreign Investment Spending ($443 Billion) by Country The Heritage Foundation just put out a report full of charts and infographics highlighting "key economic and political indicators for Asia." Here is one to watch – China's foreign investment spending in other countries. Take a look! 3. China's Reining In of U.S. Treasury Purchases Will Precipitate U.S. Dollar Collapse

The People's Bank of China is reported by Bloomberg to have said that it will rein in dollar purchases as the country no longer benefits from increases in its foreign-currency holdings…What implications will this have? I believe that we’ll see the start of a U.S. dollar collapse. Here’s why Read More » 4. China Converting U.S. Dollar Debt Holdings Into Gold At Accelerating Rate

China, Russia and other nations are exiting their dollar-denominated holdings in favor of gold. This action should put pressure on the dollar and U.S. treasuries, pushing not only central banks, but mainstream investors towards the safety of precious metals and other tangible assets that cannot be defaulted on. There will be a rush out of dollars and into assets with no counter-party risk, it is just a matter of how soon it happens. Read More » The post China’s Debt Binge & Buying Spree Is About to Burst! appeared first on munKNEE dot.com. |

| China Literally Buying Gold By The Ton Posted: 30 Nov 2013 04:46 PM PST China Literally Buying Gold By The Ton ~ David Morgan : [[ This is a content summary only. Visit http://www.GoldSilverNewsBlog.com or http://www.newsbooze.com or http://www.figanews.com for full links, other content, and more! ]] |

| Russell Napier: "We Are On The Eve Of A Deflationary Shock " Posted: 30 Nov 2013 02:26 PM PST In the aftermath of Ray Dalio's conversion to an inflationista earlier this year (even if he has since once again been pushing a deflationary agenda when he once again went long Treasurys in late September as Zero Hedge reported previously), which promptly got such permanent deflationists as David Rosenberg to change their multi-year tune, it seemed as if there was nobody left in the deflationary camp. Which, implicitly meant Bernanke was winning as the world's expectations for a return to inflation were rising (remember: hyperinflation has nothing to do with inflation per se, and everything to do with loss of confidence in a currency, even if formerly a reserve), and also meant the Fed would need to do less to further its reflationary agenda. Alas, as the Taper Tantrum and the shock upon its subsequent withdrawal showed, not to mention the recent outright disinflation in Europe, any rumors that the Fed was back in control were wildly exagerated, and here we find ourselves, entering the last month of 2013 with loud speculation that not only will the BOJ increase its own QE but the ECB itself will have no choice but to join the QE party (even as the Fed may or may not taper although it is increasingly looking likely that with an economy this late in the cycle, Yellen will simply forego tapering altogether, and may even navigate Bernanke's chopper) in order to stoke even more inflation as the current amount was, surprise, insufficient. We ignore all discussion of what such a reckless action would mean for the credibility of fiat, although we remind readers that right now both the US and Japan monetize 70% of their gross bond issuance, and thus deficit. So with everyone expecting deflation to have been conquered early in 2013, only for events to once again show that neither is it conquered, nor are central banks in charge despite having a collective balance sheet of over $10 trillion, we have once again gotten a demonstration of Bob Farrell's rule #9: " When all the experts and forecasts agree – something else is going to happen." And yet, that is not exactly true: not all "experts" think the Fed has won the fight, and the deflation has been conquered (what the Fed's response to even more deflation will be is a separate topic altogether, but it is not rocket surgery to assume "more of the same" until one day the Fed breaks the dollar itself). CLSA's Russell Napier has just written perhaps the most vocal pro-deflation piece we have read in a long time. It is titled, appropriately enough, "An ill wind." Selected extracts from CLSA's Russell Napier:

* * * We wonder how long before the lack of controlled (that being the key word) inflation will the recent inflationary converts throw in the towel again and once again start pounding the deflationary drum. Actually, in retrospect, we couldn't care less. The bigger question, as has been the case from Day 1 of QE, is how long until the disproportionate response to even more deflation will the Fed react, as it always does, with even moar stimulus, until it finally does just enough to force consensus to finally begin doubting the viability of the current reserve currency under the mentorship of the Marriner Eccles monetary mandarins. Because as we never tire, no monetary system (or nation, or civilization for that matter) has ever ceased to exist due to hyperdeflation - the cause has always been the response of the ruling class to said deflation. |

| Guest Post: Economic Prosperity Ahead Or A Train A Comin' Posted: 30 Nov 2013 01:25 PM PST Originally posted at Monty Pelerin's World blog, Whether the light at the end of the economic tunnel represents sunshine or an on-coming train depends on whom you ask. I am of the opinion that it is a train a comin'. Economic matters cannot get better until we hit bottom and rebuild from the ashes. That need not be except government policies drive us there. Government, especially the current one, has incented people to not work by providing overly long and generous benefits. Society has an obligation to take care of its less fortunate, but it does not have an obligation to encourage people to join that group and then make it comfortable enough that they have little incentive or ability to leave. The dole should not be a safety net, not a career choice! One political party in particular has interest in seeing dependency grow. It forms a substantial part of their support and power. The creation of more dependents is the creation of more voters and more electoral success. No society can grow or recover when government deliberately undermines the need to work. That path leads to poverty and destruction. Printing money is no substitute for effort. It does not create things or wealth. The myth of Keynesian economics is not the answer to a society that declines in labor force participation and has fewer productive people supporting more dependents. Incentives at the individual level must be changed in order to make work more desirable and attractive than welfare. A society whose workforce is in decline is one that can pretend to live at former levels only by consuming the wealth and capital created by previous generations. This behavior is equivalent to the man who used to make $250,000 per year in a job and now is unemployed. To save face, he continues to live as if he is still earning at his previous rate. He achieves this short-run living style only by consuming the capital that he built up from years of hard work. At some point, he runs out of capital and must live as a pauper (or the modern equivalent of one). Our economy and government both behave like this formerly rich man. Both are consuming the seed corn in order to maintain the appearance of well-being. Politicians will continue this behavior until the music stops. Hopefully when that happens there is enough left of society and freedom to allow a rejuvenation. Many believe that government and its partner the Federal Reserve are wise and strong enough to avoid this crash. If printing money and spending money were a solution, there would be no poverty anywhere in the world. Even the poorest country has a government and can afford a printing press. Thus far there has been no collapse. However, that is equivalent to the man who jumps off the Empire State building and is heard to say as he flashes by the fortieth floor: "So far, so good." His fate was sealed when he jumped. Similarly, so is our economy's. Economics has its own gravity. It is as powerful and immutable as that of physics. "So far so good" is not acceptable for an economy. There has been no economic recovery since one was falsely declared in June of 2009. The distortions and mis-allocations imposed on the economy for the last several decades are cumulative and have finally reached that stage where they can no longer be covered up. The myth of a recovery is getting harder to maintain. A complete cleansing of the mal-investments, distorted incentives and regulatory burdens must occur before a true recovery can take place. Can the economy flutter around is some kind of air pocket at the fortieth floor for a year or even several before resuming its destiny with terra firma? Perhaps, but it cannot fly without wings and these have been removed by regulatory interference and economic interventions over the course of decades. They can re-grow, but not before a complete and total cleansing. A major crash is coming. The dot.com bubble and the housing bubble were not crashes, at least as I imagine a crash. They were the beginnings of corrections that were aborted by government economic intervention. The country survived these two major bubbles, but only at the cost of making the next one bigger. Government did not save us from these two events. They created them and by deferring their correction assured the next one would be bigger and more painful. The video below shows a train moving down a track. It struck me as a reasonable metaphor for our economy. The train represents market forces, slow but powerful. The train does not appear threatening. But, like markets, it represents a massive force. That the video is in slow motion exaggerates the surprise and the force. Government may believe it is in control of the economy, but it is not. It may think it is influencing and controlling outcomes. To some degree it is and has. However the forces that have built up over decades of these interventions cannot, at some point, be controlled. The mismatch between Ben Bernanke, Barack Obama, the Federal establishment and all their dollars and regulations is about to be run over by the train that represents decades of suppressed market forces. No government is a match for hundreds of millions of citizens who are represented by markets. Suppressing markets is suppressing the will of citizens. At some point markets dig in their heals and say enough. Then government is helpless. |

| Posted: 30 Nov 2013 11:57 AM PST Four years ago we exposed what appeared to be a 'smoking gun' of the Fed's willingness to manipulate the price of gold. Then Fed-chair Burns noted the equivalency of gold and money, and furthermore pointed out that if the Fed does not control this core relationship, it would "easily frustrate our efforts to control world liquidity." Through a "secret understanding in writing with the Bundesbank that Germany will not buy gold," the cloak-and-dagger CB negotiations were exposed as far back as 1975. Recently, we exposed Paul Volcker's fears of "PetroGold" and the importance of the US remaining "masters of gold." Today, via a transcript of then Secretary of State Kissinger's 1974 meeting we see how clearly they understood that demonetizing gold was a critical strategy to maintaining a dominant power position in the world, and "raiding the gold market once and for all."

... On June 3, 1975, Fed Chairman Arthur Burns, sent a "Memorandum For The President" to Gerald Ford, which among others CC:ed Secretary of State Henry Kissinger and future Fed Chairman Alan Greenspan, discussing gold, and specifically its fair value, a topic whose prominence, despite former president Nixon's actions, had only managed to grow in the four short years since the abandonment of the gold standard in 1971. In a nutshell Burns' entire argument revolves around the equivalency of gold and money, and furthermore points out that if the Fed does not control this core relationship, it would "easily frustrate our efforts to control world liquidity" but also "dangerously prejudge the shape of the future monetary system." Furthermore, the memo goes on to highlight the extensive level of gold price manipulation by central banks even after the gold standard has been formally abolished. The problem with accounting for gold at fair market value: the risk of massive liquidity creation, which in those long-gone days of 1975 "could result in the addition of up to $150 billion to the nominal value of countries' reserves." One only wonders what would happen today if gold was allowed to attain its fair price status. And the threat, according to Burns: "liquidity creation of such extraordinary magnitude would seriously endanger, perhaps even frustrate, out efforts and those of other prudent nations to get inflation under reasonable control." Aside from the gratuitous observation that even 34 years ago it was painfully obvious how "massive" liquidity could and would result in runaway inflation and the Fed actually cared about this potential danger, what highlights the hypocrisy of the Fed is that when it comes to drowning the world in excess pieces of paper, only the United States should have the right to do so. ... Lastly, the memo presents a useful snapshot into the cloak-and-dagger, and highly nebulous world of CB negotiations and gold price manipulation:

Volcker's 1974 "PetroGold" concerns... First, here is what the S intentions vis-a-vis gold truly are when stripped away of all rhetoric:

In other words: gold can not be allowed to dominated a "durable, stable system", and a rising gold price would cripple the reserve currency du jour: well known by most, but always better to see it admitted in official Top Secret correspondence.

Specifically, this is among the top secret paragraphs said on a cold night in March 1968:

And Now Kissinger's 1974 Transcript... Via Mike Krieger's Liberty Blitzkrieg blog, The following excerpts are from a transcript of a 1974 meeting held by the then Secretary of State Henry Kissinger and his staff. This particular meeting was held on April 25, and focused on an European Commission Proposal to revalue their gold assets. What follows is an incredible insight into the minds of powerful American leaders scheming to maintain power and show other nations their place. What is most significant is how clearly they understood that demonetizing gold was a critical strategy to maintaining a dominant power position in the world. So to those who continue to say that “gold doesn’t matter” because it hasn’t been used as an official asset in the monetary system for decades, I say give me a break. In fact, the reality of gold having been largely demonetized makes it an even greater threat going forward if the U.S. does not have all the gold it claims to, and other nations have more than they admit to. Thanks to In Gold We Trust for bringing this to my attention. Choice excerpts are provided below, and breaks in the conversation are denoted with an “…” Enjoy. Secondly, Mr. Secretary, it does present an opportunity though—and we should try to negotiate for this—to move towards a demonetization of gold, to begin to get gold moving out of the system. Secretary Kissinger: But how do you do that? Mr. Enders: Well, there are several ways. One way is we could say to them that they would accept this kind of arrangement, provided that the gold were channelled out through an international agency—either in the IMF or a special pool—and sold into the market, so there would be gradual increases. Secretary Kissinger: But the French would never go for this. Mr. Enders: We can have a counter-proposal. There’s a further proposal—and that is that the IMF begin selling its gold—which is now 7 billion—to the world market, and we should try to negotiate that. That would begin the demonetization of gold. Secretary Kissinger: Why are we so eager to get gold out of the system? Mr. Enders: We were eager to get it out of the system—get started—because it’s a typical balancing of either forward or back. If this proposal goes back, it will go back into the centerpiece system. Secretary Kissinger: But why is it against our interests? I understand the argument that it’s against our interest that the Europeans take a unilateral decision contrary to our policy. Why is it against our interest to have gold in the system? Mr. Enders: It’s against our interest to have gold in the system because for it to remain there it would result in it being evaluated periodically. Although we have still some substantial gold holdings—about 11 billion—a larger part of the official gold in the world is concentrated in Western Europe. This gives them the dominant position in world reserves and the dominant means of creating reserves. We’ve been trying to get away from that into a system in which we can control— … Mr. Enders: Yes. But in order for them to do it anyway, they would have to be in violation of important articles of the IMF. So this would not be a total departure. (Laughter.) But there would be reluctance on the part of some Europeans to do this. We could also make it less interesting for them by beginning to sell our own gold in the market, and this would put pressure on them. Mr. Maw: Why wouldn’t that fit if we start to sell our own gold at a price? Secretary Kissinger: But how the hell could this happen without our knowing about it ahead of time? Mr. Hartman: We’ve had consultations on it ahead of time. Several of them have come to ask us to express our views. And I think the reason they’re coming now to ask about it is because they know we have a generally negative view. Mr. Enders: So I think we should try to break it, I think, as a first position—unless they’re willing to assign some form of demonetizing arrangement. Secretary Kissinger: But, first of all, that’s impossible for the French. Mr. Enders: Well, it’s impossible for the French under the Pompidou Government. Would it be necessarily under a future French Government? We should test that. Secretary Kissinger: If they have gold to settle current accounts, we’ll be faced, sooner or later, with the same proposition again. Then others will be asked to join this settlement thing. Isn’t this what they’re doing? Mr. Enders: It seems to me, Mr. Secretary, that we should try—not rule out, a priori, a demonetizing scenario, because we can both gain by this. That liberates gold at a higher price. We have gold, and some of the Europeans have gold. Our interests join theirs. This would be helpful; and it would also, on the other hand, gradually remove this dominant position that the Europeans have had in economic terms. … Mr. Rush: Well, I think probably I do. The question is: Suppose they go ahead on their own anyway. What then? Secretary Kissinger: We’ll bust them. Mr. Enders: I think we should look very hard then, Ken, at very substantial sales of gold—U.S. gold on the market—to raid the gold market once and for all. Mr. Rush: I’m not sure we could do it. Secretary Kissinger: If they go ahead on their own against our position on something that we consider central to our interests, we’ve got to show them that that they can’t get away with it. Hopefully, we should have the right position. But we just cannot let them get away with these unilateral steps all the time. Full transcript here.

|

| Paul Craig Roberts - US Corruption & World Interference Failing Posted: 30 Nov 2013 11:39 AM PST  Today a former US Treasury Official warned King World News that US corruption and global interference is failing. He also discussed the desperate situation the US now faces and what this means for the gold market. Below is what Dr. Paul Craig Roberts had to say in part II of this powerful interview series. Today a former US Treasury Official warned King World News that US corruption and global interference is failing. He also discussed the desperate situation the US now faces and what this means for the gold market. Below is what Dr. Paul Craig Roberts had to say in part II of this powerful interview series.This posting includes an audio/video/photo media file: Download Now |

| Filling the China Cabinet With Gold Posted: 30 Nov 2013 11:00 AM PST Nichols on Gold |

| Market Monitor – November 30th Posted: 30 Nov 2013 10:58 AM PST Top Market Stories For November 30th, 2013: China Gives Thanks For Cheap Gold - John Rubino Smuggled gold has its own price in India - Mineweb I Wish I Were Smarter - GoldSeek The HUI Has Penetrated Its June Lows, Gold and Silver To Follow - 321 Gold China’s gold imports jump to 2nd highest on record in October - Reuters [...] |

| What's The Difference Between Markets & Reality? About 22% YTD Posted: 30 Nov 2013 10:41 AM PST Faith, hope, and confidence are the 3 key factors driving stocks at this point with fundamentals lagging an awkward 4th place. Faith in the perpetual central bank put (and bad news is thus good news); Hope that repeating the same 'experiment' following its previous failures will work this time; and confidence that the old normal is re-attainable (no matter how many times we kick the can). Year-to-date, S&P 500 earnings are up around 7% (and the trajectory is declining); accordingly, as we noted previously, confidence is ultimately responsible for levitating nominal stock prices through multiple expansion.. and is responsible for the rest of the market's gains. With confidence now fading (according to most surveys) investors will not be willing to pay increasing multiples unless they are confident that the future streams of earnings are sustainable and forecastable...

The S&P 500's return year-to-date - between Fundamentals and markets...

(h/t @Not_Jim_Cramer)

But, it's all about confidence... investors will not be willing to pay increasing multiples unless they are confident that the future streams of earnings are sustainable and forecastable... And simply put, the current levels of Consumer Sentiment need to almost double for the US equity market tp approach historical multiple valuation levels...

And remember - as we noted here - its the 80% that consume and the 80% are not benefitting from the wealth effect (much to the chagrin of the Fed).

So next time your "manager" or investment advisor proclaims stocks are cheap compared to historical peak levels, perhaps its worth asking him with "risk" priced into the market at almost all-time lows,

Where is the next doubling of Sentiment coming from? Especially in light of the collapse in economic confidence we are seeing recently. |

| Gold & Silver: “You have stayed for the pain, will you not stay for the gain?” Posted: 30 Nov 2013 10:27 AM PST You don't need to be a Ph. D. to realize this current oversold situation in gold and So says Dudley Pierce Baker (commonstockwarrants.com) in edited excerpts from his original article* entitled I Wish I Were Smarter. [The following is presented by Lorimer Wilson, editor of www.FinancialArticleSummariesToday.com and www.munKNEE.com and the FREE Market Intelligence Report newsletter (sample here – register here). The excerpts may have been edited ([ ]), abridged (…) and/or reformatted (some sub-titles and bold/italics emphases) for the sake of clarity and brevity to ensure a fast and easy read. This paragraph must be included in any article re-posting to avoid copyright infringement.]Baker goes on to say in further edited excerpts: …Some of the brightest minds in the natural resource sector discussed this timing issue at the recent Metals & Minerals Conference in San Francisco.

No one knows, (and no one will know until well after the bottom is in place and we can look back in our rear view mirror with clarity…[so] what is the average investor to do, if anything and when? … [I believe] we are near a low in gold and resource shares and, over the next few years, fortunes will be made by those investors staying the course and remaining committed to this investment sector. As Rick Rule says, "you have stayed for the pain, will you not stay for the gain?"Precious Metals: Don't Want To Play Anymore? Many good companies are selling for below or very near their cash value. While this is unthinkable in a bull market, at this particular time it is not difficult to find companies with lots of cash in the bank selling at ridiculously low prices. Now I may not be the smartest guy on the block but I can recognize opportunities and it is definitely time for investors to be positioning themselves for the next big uptrend, which could begin at anytime. Gold Stocks: Likelihood of Making Breathtaking Returns Has Never Been Greater! Here's Why Should you be nervous? Of course, everyone is nervous, because 'we' don't' know if there is further downside risk. So perhaps you will want to tip toe into the waters and keep some cash for later, hedge your bets so to speak. While an aggressive investor might say, 'the hell with it, I am going all-in'. I could show you some charts, but you already know how bad it is. This is the worst of times for the resource shares over the last decade or so. Charts would only make you cry to see the destruction of wealth in this sector. Noonan: Charts Say NO End In Sight for Decline In Gold & Silver Prices My suggestion is to focus your attention on:

The balance of 2013 could be very interesting as tax loss selling season in upon us. Funds will probably also be selling to clear out their weakest positions before year-end as well as to meet redemptions by their shareholders. Thus investors have until the first of the year to complete their due diligence on selected companies… While I still wish I were smarter, I am not. However, I will use the approaches above to find new opportunities and alternative investment strategies and to be in the best position possible heading into the first of the year. [Editor's Note: The author's views and conclusions in the above article are unaltered and no personal comments have been included to maintain the integrity of the original post. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.]*http://juniorminingnews.com/?p=3576 Related Articles: 1. Gold Stocks: Likelihood of Making Breathtaking Returns Has Never Been Greater! Here's Why  We all think the price of gold, the metal, is depressed and is about equal to the total cost of production but when one compares the price of precious metals mining companies to the price of gold bullion, their prices are at historical lows. It seems that the mining shares can only go in one direction…up…but when and by how much? This article suggests it presents the greatest opportunity in 30 years. Look at the charts! Absolutely unbelievable. Read More » 2. Noonan: Charts Say NO End In Sight for Decline In Gold & Silver Prices No matter what the latest "news" development is for PMs that paints a rosy picture, those in the fundamentalist camp are looking through rose-colored glasses to expect change in the near future. The charts for gold & silver continue to tell a more accurate story that belie all known fundamentals, and the charts shown here depict a market in decline with no apparent end in sight. Read More » 3. Expect Gold to (Only) Drop to $1,150 by Mid-2014! Here's Why  The gold price will likely decline to $1,150 next spring but should find enough buyer support from physical buyers and jewellery makers to prevent a fall below $1,000. Read More » 4. Sustained Rise in Gold Price Likely – Here's Why  Many events moved the market this month which are all very bullish for gold. In addition, gold's leading indicator is currently at a major low area all of which strongly reinforce the likelihood of an upcoming sustained rise. Let us explain. Read More » 5. 12 Reasons Why Gold Should Bounce Sharply Higher in 2014  Is it time to throw in the towel? Is the bull market in precious metals really over? I don’t think so because my analyses suggest that nearly all of the fundamental factors that have been driving the gold price higher in the past decade have only strengthened in the past two years. Now that the correction has most likely run its course, I expect gold to rebound into the close of the year and bounce sharply higher in 2014. Here are the 12 reasons why. Read More » Other Articles by Dudley Baker: 1. Precious Metals: Don't Want To Play Anymore?

We suspect that many precious metals investors are saying, "We don't want to play anymore!" and our reply is, "You mean you want to quit right now? Right at the bottom of this cycle? You must be crazy – and that is crazy with a capital C!" True, this is a very challenging market environment for resource shares, but we know what the ultimate outcome will be: higher share prices. The only question is "when" and our opinion is that we are very close in time (within days or a week or two at most) of being able to say that the lows are behind us. Let me explain. Words: 785 Read More » …Even in these challenging times there have been many great winners in the natural resource sector. I have been fortunate, lucky or smart to have racked up some nice gains through the years. I have been consistently picking winners, big winners, monster winners for years – a string of 10 years of 500% plus winners and more, sometimes much more, year after year – …[so] my message to you is simple: follow me! Your only question should be “Which of my current positions will be the next big winners?” Words: 804; Table: 1 Read More » 3. My Rules for Successful Investing In Stock Warrants Very few investors know about the potential benefits via the additional leverage that warrants can offer but they are substantial if you follow the 4 rules I present in the article below. Words: 766 Read More » 4. Here's How Best to Deploy $5-10,000 in the Gold & Silver Junior Mining Sector $5,000 to $10,000 may not go far in buying the top companies on the NYSE or the Toronto Stock Exchange, but in the junior mining sector, you will be amazed what you can accomplish. You can actually buy thousands and thousands of shares. Yes, these are 'penny stocks' but the challenge is to uncover those companies which have the potential to perform well in the coming months. The risk is incredibly high but so is the potential reward. [Let me explain.] Words: 538 Read More » The post Gold & Silver: "You have stayed for the pain, will you not stay for the gain?" appeared first on munKNEE dot.com. |

| This Inflation Is Supposed To Be GOOD For Japanese Workers? Posted: 30 Nov 2013 09:59 AM PST Wolf Richter www.testosteronepit.com www.amazon.com/author/wolfrichter Japan's new economic religion, lovingly dubbed Abenomics, relies mostly on a money-printing binge that monetizes the entire government deficit plus a chunk of its public debt, month after month. Printing yourself out of trouble and to wealth works every time. For the elite. This is a lesson learned from the Fed. But how are workers and consumers faring? And by implication the real economy? We keep getting juicy morsels of data on this phenomenon. Abenomics is accomplishing its two major goals – watering down the yen and stirring up inflation – pretty well. Over the last 12 months, the yen has been devalued by 20% against the dollar that the Fed is trying to devalue as well. So this is quite a feat! It's been devalued by 28% against the euro. And inflation is heating up. The consumer price index, released today, rose 0.1% in October and is now up 1.1% for the 12-month period. Less "imputed rent," inflation rose 1.4% year over year. Service prices were up 0.4%, but goods prices jumped 1.9%. At this rate, Abenomics will have no problems meeting or exceeding by March, 2015, its "2% price stability" target, as the Bank of Japan has come to call it with bitter cynicism. What isn't happening: wage increases! The Japanese Statistics Bureau just reported incomes and expenditures of households with two or more persons. This is by far the largest category of households in Japan. Due to the cost of housing in large urban areas – and due to remnants of tradition – a large number of singles live with their parents. This category is further divided into "workers' households," "no occupation" households, and "other" households. Incomes of the all-important "workers' households" rose a measly 0.1% from a year ago to ¥482,684. In nominal terms. But adjusted for inflation – yes, here is where the benefits of Abenomics are kicking in – incomes fell 1.3%. Disposable incomes fell 1.4%. The details were ugly: "Current income" (salaries and wages) dropped 1.2% and "temporary bonuses" plunged 19.5%. Income from self-employment and piecework plummeted 20.8%. So these strung-out workers' households whose belts are being tightened by Abenomics and whose real incomes are being whittled away by inflation, how can they spend more to perk up the economy? Turns out, they don't. Spending rose a scant 0.4% in nominal terms from a year ago – but adjusted for inflation, spending fell 1.0%. And this despite rampant frontloading of big-ticket purchases. The consumption-tax hike from 5% to 8%, to take effect on April 1, is motivating households to buy big-ticket items now and save 3%. It has turned into a frenzy. Durable goods purchases, the primary target of frontloading, jumped 40.4% in October from a year ago. While it's goosing the economy now, it will create a hole starting next spring. Japan has been through this before. When the consumption tax hike from 3% to 5% was passed in 1996, Japanese consumers went out on a buying binge of big-ticket items to avoid paying the extra 2% in taxes, and the economy boomed. The hangover came around April 1, 1997, when the tax hike became effective. The economy skittered into a recession that lasted a year and a half. Now Japanese households are frontloading to avoid an additional 3% in consumption tax. The hangover next year is going to be painful. But frontloading of a few big-ticket items is hitting day-to-day expenditures. These households spent 1.8% less on non-durable goods and 2.0% less on services, compared to prior year. Hence, the drop of 1% in overall spending by these households, despite their splurging on a few big items. This is the benefit of inflation without compensation! A process that ever so slowly hollows out the middle class and pushes the lower classes deeper in the quagmire. It's hurting workers and consumers. It's constraining the real economy. Yet, holders of assets that the central bank inflates into the stratosphere benefit. Japan isn't the only country that is practicing this large-scale redistribution of wealth from workers to holders of inflated assets. Abenomics is following the playbook of the Fed. But it's pushing it further to the extreme. The dogfight over Japan's biggest problem, its gargantuan government deficit, entered its annual ritual of leaks and pressure tactics that usually lead to a pre-Christmas draft budget with an even bigger deficit. But this time, it's different. Very different. Read..... Japan Is Used To Natural Disasters, But This One Is Man-Made |

| Comex Registered Gold Inventory Levels - 65 Potential Claims Per Ounce Posted: 30 Nov 2013 09:07 AM PST |

| Comex Registered Gold Inventory Levels - 65 Potential Claims Per Ounce Posted: 30 Nov 2013 09:07 AM PST |

| Ukraine President Explains Relations With Russia Using Body Language, While Local Violence Escalates Posted: 30 Nov 2013 08:00 AM PST A week ago Europe was furious, and Putin once again glorious, after Europe's "bread basket", the Ukraine, under president Yanukovich decided to terminate its pro-European stance, and instead in a very symbolic shift, chose Moscow as its future trading partner hub. "This is a disappointment not just for the EU but, we believe, for the people of Ukraine," EU foreign policy chief Catherine Ashton said in a statement. Yanukovich said he had declined to sign the EU pact as the cost of upgrading the economy to meet EU standards was too great and that economic dialogue with Russia, Ukraine's former Soviet master, would be revived. Today, tensions in the Ukraine finally spilled over when following the break up of a pro-Europe protest by local police, the opposition announced it would call a countrywide general strike to force the resignation of president Viktor Yanukovich.

For jailed former Prime Minister Yulia Tymoshenko this is just the political spark that might escalate and get her out of prison.

Even the boxers (and potential future presidents)chimed in:

Things will likely get worse before they get better:

Of course, now that Putin has found his opening and the current Ukraine regime is instrumental in his plan of recreating the old USSR sphere of influence, this time with Gazpromia's resource monopoly, so hated by Europe, the opposition's work may be cut out for them. For the clearest explanation of just why it will be next to impossible to shake the Kremlin off, watch the following silent Euronews clip showing Yanukovich's body language explanation to Angela on just where his country's relations with Russia currently stand. |

| Posted: 30 Nov 2013 06:41 AM PST Summary: Long term - on major sell signal since Mar 2012. Short term - on sell signals. Gold sector cycle - down as of 11/08. Read More... |

| Gold And Silver - Reverse Bubble. Huge Rally When Broken. Note Bitcoin Results Posted: 30 Nov 2013 06:12 AM PST Gold and silver are in reverse bubbles, if you will, where price has been both severely distorted and suppressed by central banks, the visible tools of the otherwise hidden moneychangers, those on the top of the population pyramid who want ... Read More... |

| Silver and Gold as Currency Commodities Posted: 30 Nov 2013 05:00 AM PST Jeffrey Lewis |

| Are Bitcoin's Better Than Gold? Crypto-Future of Trillion Dollar Digital Trading & Exchange? Posted: 30 Nov 2013 03:20 AM PST The price of one Bitcoin -- a mathematically designed digital crypto-currency -- is now within a stone's throw of the price of a troy ounce of gold at more than USD 1,200 per unit. That marks a gain of over 5,000% from the USD 20 level at which Bitcoin was trading at the start of this year. At that time, not many businesses accepted the digital coins as actual currency. Since then, the currency has seen a boom that rivals the dotcom bubble of the 1990s. |

| Gold And Silver Reverse Bubble. Huge Rally When Broken. Note Bitcoin Posted: 30 Nov 2013 03:14 AM PST Gold and silver are in reverse bubbles, if you will, where price has been both severely distorted and suppressed by central banks, the visible tools of the otherwise hidden moneychangers, those on the top of the population pyramid who want to control and enslave the entire world in a totalitarian state of existence. Ironically, the best and only hope for the [not so] free world comes from China and Russia. It is a twisted world in which we live. |

| Gold Investors Weekly Review – November 29th Posted: 30 Nov 2013 02:58 AM PST In his weekly market review, Frank Holmes of the USFunds.com nicely summarizes for gold investors this week's strengths, weaknesses, opportunities and threats in the gold market. The price of the yellow metal went lower after two consecutive weeks of gains. Gold closed the week at $1,251.39 which is $7.76 per ounce lower (0.62%). The NYSE Arca Gold Miners Index fell 0.31% on the week. This was the gold investors review of past week. Gold Market StrengthsChina's net imports of gold from Hong Kong climbed to the second-highest level on record in October as jewelers and retailers bought the metal to build up inventories ahead of a peak-demand season at the end of the year. A total net purchase of 131 tonnes in the month, nearly 20 percent above the 111 tonnes in September, is only slightly lower than the record of 136 tonnes of net imports registered in March 2013. The appetite for gold from China has proved to be both remarkable and persistent. The much touted ETF liquidations that helped bring gold prices down to the $1,200 level have been absorbed entirely by China. Gold refineries in Switzerland have been busy converting the 400-ounce bullion bars, typically owned by ETFs, into one kilogram bars preferred by Chinese jewelry makers and gold investors. The world's largest listed jewelry chain, which is Chow Tai Fook Jewellery Group Ltd., forecasted steady growth for the rest of the fiscal year after first-half profits almost doubled on a surge in Chinese demand for gold. Net income rose to HK$3.5 billion and was above the average estimate of HK$2.98 billion from five analysts compiled by Bloomberg. Not surprisingly, Tiffany & Co., the world's second-largest jewelry retailer, delivered blowout earnings this week, mostly due to international growth, where the Asia Pacific region had sales growth of 27 percent. Investors should remember that roughly 50 percent of the global demand for gold is fueled by the "Love Trade," and evidenced by the success of these two retailers. Gold Market WeaknessesGross speculative short positions on the COMEX have doubled in the past three weeks to 82,842 contracts. According to David Rosenberg of Gluskin Sheff, this is only the fifth time that this has happened in the past decade, which as a strong contrarian indicator sets up the gold market for a nice countertrend rally. The biggest factor weighing on the market is a resumption of selling by ETFs. ETF holdings stabilized during the summer, but have since resumed, with investors having liquidated 1 million ounces over the past month, with 600,000 ounces of that coming over the past week. The renewed decline in ETF holdings suggests that weak hands haven't completely exited the market. Gold Market OpportunitiesAccording to Dr. Martin Murenbeeld, Dundee's Chief Economist, if we were to summarize gold market developments for 2013 to date the first concept that would come to mind would be that of a great rotation out of debt and into equity. What has actually happened is a great rotation out of gold and into equity instead. The chart below compares the gold price and the S&P500, showing that the correlation between the two is about as negative as it has ever been. The most curious part is that gold has declined in the face of exponential growth of global liquidity. The negative correlation of gold is much higher with the S&P 500, than with the U.S. dollar for example, which suggests the S&P 500 is driving the gold complex. The chart shows that gold is now -2.4 standard deviations below the S&P 500, an oversold level that on purely statistical terms, has to trigger a correction in the near to medium term.

Throughout this year, the Indian government increased import duties on gold and silver three times in a bid to protect the currency from a widening current account deficit. The All India Gems and Jewellery Federation has finally stepped up and appealed to the government to roll back the import duty from 15 percent to 5 percent. The abrupt and arbitrary rulings are threatening jewelers by making it very difficult to access the much needed gold and silver. The import curbs force jewelers to pay a record $200 per ounce premium over the London price from next month to obtain supplies, according to the All India Gems & Jewellery Trade Federation. The premium is currently at near record $120-$130 an ounce. As a result, Mumbai-based Tara Jewels said that it will close some of its less profitable gold-led stores to adapt to the current regulatory environment. Gold Market ThreatsThe daily gold fix in London, the benchmark used by miners, jewelers and central banks to trade the yellow metal, is being scrutinized amid speculation there could be superior knowledge by those involved in the fixing. Tradition calls for five banks to meet, from a few minutes to an hour, to set the price of gold twice a day. However, unnamed traders who have been involved in the process, as well as other dealers and economists argue that knowledge gleaned from the calls could potentially give traders an unfair advantage in the market. Although there is no concrete evidence of wrongdoing, both academics and economists concur in that the system is outdated and vulnerable to abuse, especially considering gold trading is a $20 trillion market. Goldman Sachs is set to swap $1.68 billion in cash with the Venezuelan central bank, to be backed by $1.85 billion of the nation's gold reserves. The terms of the loan dictate the South American government will pay 7.5 percent plus three month LIBOR over seven years, with Goldman Sachs holding the gold in a margin account. Speculation has been rampant after some details of the story were leaked to the press, with some analysts calling the transaction a classic, non-transparent emerging market transaction where deduction is necessary to guesstimate where the story is going. In our view, the gold provided by Venezuela to Goldman Sachs will create another source upon which the bank can write and sell massive paper gold bets on, increasing the already speculative paper gold market, and continuing to disturb the well-earned reputation of physical gold. |

| Gold Outlook – Love Trade And Fear Trade Likely To Return Posted: 30 Nov 2013 02:42 AM PST This is a guest post from Frank Holmes from USFunds.com. I recently returned from India, a nation where an incredible 600 million people are under the age of 25. That's nearly double the entire population of the U.S.! What's amazing about that figure is that, unlike the 1970s when India had no global footprint, today's generation is increasingly gaining access to the Internet. Social networking platforms are seeing an incredible growth trajectory in India, as one of the fastest growing markets. In fact, by 2016, the country is set to be Facebook's largest population in the world, according to the BBC. While Forbes India reports that there are only 137 million users in India, with the growing population and rising wealth, we expect this number to grow substantially. I believe this connectivity changes the growth pattern for commodities. Like I told Kitco's Daniela Cambone at the Metals & Minerals Investment Conference in San Francisco, this population carries on its love of gold. Mineweb reports that about 1 million couples will marry this wedding season, with around 33,000 weddings taking place on November 19 alone. Gold traditionally accompanies these events, and a typical gift is "a pendant, earrings or a ring, weighing 5-10 grams depending on financial circumstances. Parents of the bride generally give heavier items like a necklace or bangles weighing 50 grams or more," according to Mineweb. Still, to help manage expectations, investors should anticipate a short-term headwind for the precious metal as India's GDP per capita has stalled. The World Bank estimated India to grow 6.1 percent this year, but lowered its forecast to 4.7 percent due to a slowdown in manufacturing and investment. The long-term picture looks positive though. While India grew at 4.8 percent in the third quarter, the finance ministry is confident the country can return to its "high-growth plan." It projects the economy to pick up, accelerating to around 6 percent in the next fiscal year and about 8 percent in another two years, says TheWall Street Journal.

As we explain in our Special Gold Report on the Fear Trade, one of its strongest drivers is real interest rates, which is when the inflationary rate of return is greater than the current interest rate. Our model tells us that a real interest rate of more than 2 percent is typically bearish for gold. Still, the real rate is not very close to the 2-percent tipping point. As of the end of November, the 5-year Treasury yield is 1.31 percent while inflation is at 1 percent. Investors end up with a slightly positive return of 0.31 percent.

With onerous regulations continuing to slow down the flow of money, I believe the government will need to keep its printing presses warm, eventually reigniting the Fear Trade. Keep in mind that real rates are not positive in every country. As I will be showing in my presentation at the Mines and Money conference in London, U.K. investors are still losing money after inflation. The 5-year gilt yield is at 1.51 percent, but inflation is at 2.2 percent, resulting in a negative real rate of return.

|

| Junior Gold Stocks Rabbit Hole Posted: 29 Nov 2013 08:52 AM PST Lewis Carroll’s Alice in Wonderland is a timeless tale that chronicles the journey of a young girl into a psychedelic fantasy land. This tale is one that turns logic upside down, and takes us into a bizarre world that defies reality. To get to this world Alice falls down a precarious rabbit hole, perhaps the same one that has swallowed the junior gold stocks. The juniors have seen so much carnage lately that investors have completely disregarded their sector. And this disregard has sent them down a proverbial rabbit hole, into a world that is bizarre and illogical to say the least. Though these stocks certainly don’t have much support with gold prices so weak lately, popular consensus that their sector is dead is pure fantasy. |

If the dollar loses its role as the world currency, and if the exchange rate falls, I think that hampers the ability of the Federal Reserve and the bullion banks to sell naked shorts, or to control the gold price by dumping all of these naked shorts in the gold futures market.

If the dollar loses its role as the world currency, and if the exchange rate falls, I think that hampers the ability of the Federal Reserve and the bullion banks to sell naked shorts, or to control the gold price by dumping all of these naked shorts in the gold futures market. Gold jewelry is not generally considered an appropriate investment mainstay, due to the fact that the buyer typically pays a high premium over the price of the gold for the workmanship that goes into transforming gold into jewelry, and because the quality of the gold in jewelry varies widely from piece to piece.

Gold jewelry is not generally considered an appropriate investment mainstay, due to the fact that the buyer typically pays a high premium over the price of the gold for the workmanship that goes into transforming gold into jewelry, and because the quality of the gold in jewelry varies widely from piece to piece.

Hello from Acapulco Bay,

Hello from Acapulco Bay,

| You are subscribed to email updates from Save Your ASSets First To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment