Gold World News Flash |

- Q3 GDP Is A Head Fake

- As CNYJPY Jumps To QE2 Levels, What Odds Are Markets Implying Of A China Hard Landing?

- How BIG is the U.S. Debt?

- Please Welcome The Latest Currency Peg

- Silver Market Update

- Central Banks Top Up Gold Reserves

- A Very Interesting CoT

- Let Them Eat Cake: 10 Examples Of How The Elite Are Savagely Mocking The Poor

- BaNZai7 HaLLOWeeN KiCK OFF: QuoTH THe RaVeN, DEBTS NO MORE!

- Is Gold Over Or Undervalued? How About The EFSF (Europe = Fastow, Skilling & Fuld)

- This Past Week in Gold

- Gold Market Update

- MF Global Hires Two Bankruptcy Legal Advisors As Chapter 11 Looms

- The Big Mac Index: Is Your Country?s Currency Over or Under-Valued Compared to USD?

- Stock World Weekly: Europhoria

- "When Money Dies" Author Adam Fergusson And James Turk Discuss (Hyper)Inflation In The Past, In The Present And In The Future

- Oktoberfest: When The Music (Money) Stops Playing (Flowing)…

- The "Dumb Money" Refuses To Play Along: China State Media Says It Won't Rescue Europe

- Gold and hyperinflation

- Dollar Breakdown Triggers Stock Markets Risk Rally, It's All About the 3's

- Gold and Silver News 10/29/2011 EU Debt Deal

| Posted: 30 Oct 2011 06:06 PM PDT This article originally appeared on the Daily Capitalist. The news on the latest GDP report said "recession fears recede." Now, a few days later, it's "red flags." So which is it? I think it is still "red flags." But then we have most of mainstream economists/analysts who disagree with us. The difference is that they have been mostly wrong and we have been mostly right. There are several things to understand about gross domestic product before analyzing the numbers: 1. Spending Isn't Everything One is GDP measures spending in the economy as an indicator of what the entire U.S. economy is doing. In other words it is concerned only with demand and consumption of goods, not with the production of goods. As a statistic it tells you nothing about how all those goods got there. This is an interesting topic going way back in Austrian theory economics and which distinguishes it from other economic theories. We Austrians are more concerned with what individuals are doing not some aggregate "national" output that economists make up. It's complicated. (This article makes it easy.) But think about this: if the Fed injects more dollars into the economy it will show up as increased final demand/consumption and boost GDP. Since printing more money doesn't create wealth, that doesn't tell us much about our economic health (e.g., spending boomed during the Weimar Republic and in Zimbabwe). Since we Austrians are, if nothing else, realists, we understand that everyone pays attention to GDP, including the Fed, so we pay attention to it as well. 2. This Report Will Be "Revised" So assuming GDP is important to follow, the next thing to understand about this Q3 report is "a". "a" is the letter attached to this report and means "advance estimate". These GDP reports are revised as better data comes in, so next we will get the "second estimate" and then the "third (final) estimate." More often than not these reports have been revised downward lately more than upward. 3. They Fudge The Deflator Lastly these numbers are what are called "real", or inflation-adjusted numbers. This gives rise to the question of what is the actual rate of price inflation. They don't use the CPI ratio put out by the Census Bureau. They use what is called a "chained" price deflator from the GDP report which means they take prices as they were in 2005 and figure how much they have gone up since then. Then they adjust the gross spending numbers by this ("deflator"). This is good for the government because it is lower than what we believe to be the actual price inflation rate and makes GDP look better than it really is. Let's face it, 2005 isn't very long ago and if you go back farther in time this inflation indicator would make GDP look worse. Why not 1995 or 1985 or 1975? Also, they keep changing their calculation methodologies. My preferred price inflation source is Shadowstats which uses methodologies the government used in 1990 or from 1980. Their 1980 chart is showing price inflation at about 12%. The BEA (which puts out the GDP report) is using a 2.5% rate of price inflation. In other words, if you adjusted current GDP by the 1980 deflator GDP would be in the negative. And, if that were the case, which I believe it is, we would be seeing flat to declining growth and high unemployment, which we are. The Q3 Report GDP was up 2.5% for Q3 2011. This is almost double the Q2 report (1.3%). Spending by businesses centered on equipment, especially computer and software related goods (up 17.4%). Consumer spending was up (2.4%) and auto sales were healthy. Durable goods were up 4.1% and fixed investment (nonresidential) was up 16.3% (vs. 10.3 Q2). Negative signs were that inventories have been increasing. Another very negative indicator was real disposable personal income (-1.7%), which confirms that income/wages are going backwards. Another negative trend was that the personal savings rate declined one full percentage point to 4.1% from 5.1%. While the report suggests that cutting back in state and local government spending is a negative, we need to see this as a positive in economic terms. A look at the BEA's report on Personal Income and Outlays for September shows that real disposable personal income (i.e., inflation adjusted) decreased 0.1% in September (vs. -0.4% in August). And real personal consumption outlays (spending) increased 0.5% (vs. a decrease of 0.1% in August). This mirrors the Q3 GDP report. The fact that auto sales are up is a positive, but much of this is related to pent-up demand, "improving availability of product, lower pricing and this year's late-starting model-year-end clearance activity. But pricing still has not fully returned to normal and there are still inventory shortages. This suggests there may be a small upside to near-term sales."

Remember that most people in America are fully employed (about 84% of the workforce) and they are buying cars because of dealer incentives and the availability of desirable models. This may be analogous to Cash for Clunkers, where future demand was pulled into the present and when the incentives were gone, sales dived. A better indicator of economic health is the fact that people have cut back on driving because of higher gas prices. Business spending is also up, but other data suggests that companies are replacing equipment in order to create efficiencies in operations, but they are not hiring because of a lack of demand. What does all this tell us? It tells us that consumers are spending by almost the same amount that they are drawing down savings (savings down $116.2 billion from prior month, yet personal outlays were up $133.1 billion). These are rough statistics to be sure—we would need to see the Fed's Flow of Funds report when it comes out to get more accurate data. But it illustrates the reality that since people are earning less and spending more, the money must come from somewhere and that somewhere is savings. This is not healthy. In an economic recovery we would be seeing wages grow and consumption increase. That is not happening:

What is really happening is that consumers are being squeezed and spending is modest and declining; this is the trend:

When you see economists exultant about a minor blip in spending you can be assured that they are high on hopium. We fervently hope that the economy would recover, but for that to occur the Fed needs to raise interest rates and wind down excess reserves. Then real savings would increase, and ultimately as capital is accumulated, production would increase, debt loads would be reduced at the personal level, housing would bottom and start to turn around, banks would resolve their balance sheets, and employment would increase. But that isn't the likely case. All the attention on GDP—demand and consumption—is misplaced. This quarter's report is a false signal, a head fake if you will, that is an artifact of two rounds of quantitative easing (QE), which cannot be sustained when you have wages declining and debt loads still historically high. In my article, "Winners and Losers: The New Economy", I pointed out that the top 5% of earners account for 37% of all consumer spending and it they who are supporting consumer spending. It is our opinion that the über rich have been the main beneficiaries of QE and that it hasn't "trickled down" to the middle income earners. As the Fed's fiat money is distributed throughout the economy it has been causing prices to rise, perhaps modestly, but then QE is not a very efficient way to inflate. It hasn't created real wealth and has been rewarding financial players rather than producers. Without another round of QE we should see a continued economic decline and then a gradual recovery as outlined two paragraphs above. Because of all of the government interference in the recovery process, this will take some time. The probable scenario in the near term is that the financial markets will decline, corporate profits will flatten or decline, exports will decline because of a worldwide slowdown and a rise in the dollar, unemployment will remain high, and prices will continue to rise. That certainly doesn't add up to an increase in future real economic growth. That will alarm the Street, the Obama Administration, and the Fed and we can expect another round of quantitative easing, continued ZIRP, higher prices, and calls for more fiscal stimulus. This will kick off another round of market euphoria, a further decline in the formation of real capital required to fuel a new recovery, more price inflation, continued high unemployment, and economic stagnation. The further implications of these events will be spelled out in another article coming soon.

|

| As CNYJPY Jumps To QE2 Levels, What Odds Are Markets Implying Of A China Hard Landing? Posted: 30 Oct 2011 06:04 PM PDT With tonight's multi-year record CNY fixing and trillions being flushed at maintaining an arbitrary JPY line in the sand, it seems appropriate to re-consider how to hedge a China hard landing and what probabilities various asset classes are assigning to it occurring. While many are pointing to what seems an entirely capricious level of 79.20 JPY to the USD as the 'new normal' being defended, we were curious at the strange coincidence that the CNYJPY cross implied by tonight's CNY fixing and the 79.2 JPY was exactly the average CNYJPY level during the QE2 period. It seems the Japanese are hedging their tail-risk against the Chinese and a recent note by Morgan Stanley points to how various asset class traders might consider hedging their own version of a hard-landing scenario and notably they agree with us that China sovereign CDS remains among the 'best' hedge.

Morgan Stanley recently published a series of well-considered articles on 'The China Hedge' as part of their cross-asset-research. It seems with the G-20 meeting and increasingly unilateral behavior cracking the Nash equilibrium at its margins and as usual - first one to migrate, wins. For clarity, MS defines a hard-landing as:

From the MS note:

Aussie rates are the clear winner (and we have liked Aussia bank credit over corporates for a while also as a systemic slow-down trade). And as far as the best hedges (from a risk-reward-cost perspective):

And specifically the pros and cons of the four most efficient hedges:

The considerable compression in China CDS recently (combined with the rise in DTCC exposure) offers both an increasingly liquid and 'cheaper' hedge than at any time in the last couple of months and while CNY Puts (FX) make sense, there remains considerable concern with regard the jumpy-nature of the NDFs. ITRX Asia is perhaps the most basis-heavy hedge but by far the most liquid - particularly given the perspective that credit will be the first thing to be withdrawn. Of course, with tonight's actions, it is hard to say whether currency wars are escalating or this is some odd agreement among every one but the USA to ebb towards a gold standard to avoid an inevitable money printing endgame? Of course, the modest rise tonight in China CDS, bounce in gold, and 1% drop in ES suggest risk is off for now and perhaps grabbing some affordable hedges is in order.

|

| Posted: 30 Oct 2011 04:25 PM PDT [Ed Note: This is just one of the many reasons we recommend buying physical silver and gold.] And sadly gang, it's probably worse than $65 Trillion. Boston University economist Laurence Kotlikoff says U.S. government debt is actually $200-trillion – 840 per cent of current GDP. You can read about the $200-Trillion Debt Which Cannot Be Named HERE.

|

| Please Welcome The Latest Currency Peg Posted: 30 Oct 2011 03:32 PM PDT For the last 45 minutes, USDJPY has been unable to shake loose of 79.2 by more than a pip or two. Following the SNB and their efforts with EURCHF, which as far as we recall is technically pegged at 1.20, is Azumi now pushing another of our freely floating foreign exchange currencies to a peg, as he soaks up any and all USDJPY offers under 79.20? Gold is down a little (in its knee-jerk response to USD strength reflecting off the JPY intervention) but one has to wonder if slowly but surely we are being reverted to the 'rigidity' of a gold standard? Lastly, we eagerly await to hear the justification for this unilateral defection by a G-X member 5 days ahead of the G-20 meeting in Cannes this Friday.

It is also worth noting that ES just dropped below Friday's lows as JPY crosses become useless carry-drivers (for the first time in many weeks/months). Chart: Bloomberg

|

| Posted: 30 Oct 2011 02:53 PM PDT by Clive Maund via SilverSeek.com:

On its 4-month chart we can see how silver has broken out above the resistance at the upper boundary of its base area, and has advanced towards the higher more concentrated zone of resistance towards the lower boundary of the range of trading between July and September where a lot of trapped and traumatised traders are waiting for the chance to "get out even", hence the resistance in this zone.

|

| Central Banks Top Up Gold Reserves Posted: 30 Oct 2011 02:47 PM PDT Central banks have used gold's recent plunge to top up their holdings of the precious metal. by Garry White, and Emma Rowley, Telegraph.co.uk:

Bolivia, Kazakhstan, Tajikistan and Thailand spent a collective $1.52bn (£942m) buying 26.7 tons of gold. However, the Mexican central bank was a seller, reducing its holding by 0.1 ton, according to data compiled by Bloomberg. Thailand's gold reserves rose 11pc to 152.41 tons and Bolivia's bullion reserves increased 17pc to 49.34 tons. Bolivia increased its holdings by 5pc to tons and Tajikistan's bullion stockpile increased 26pc to 4.74 tons. Over the past 20 years, central banks have been reducing their holdings of the precious metal, but concerns about paper money and global debt has turned them into net buyers. Also, the gold price has increased every year for the past 11 years. The price is up 23pc in the year to date, closing at $1,743.75 an ounce on Friday.

|

| Posted: 30 Oct 2011 02:44 PM PDT from TFMetalsReport.com:

First, the data. For the period 10/18 – 10/25, the Dec11 silver contract rose over $1, from a little under $32 to a little over $33. Not bad, I'm sure we'd all take that $1/week into infinity. But, as is often the case, there's more here than meets the eye. Namely, a significant effort by The Evil Empire to paint a false picture of silver market price action post the historic CFTC position limit ruling. Below is an hourly chart of silver. Clearly, this can be marginalized as Turd choosing to see what Turd wants to see but, for me, the chart speaks volumes. When combined with the CoT data, the picture comes into sharp focus. Read More @ TFMetalsReport.com

|

| Let Them Eat Cake: 10 Examples Of How The Elite Are Savagely Mocking The Poor Posted: 30 Oct 2011 02:43 PM PDT from The Economic Collapse Blog:

There is absolutely nothing wrong with working hard and making a lot of money, but there is something wrong with being completely arrogant and smug about it. Today, many among the elite are savagely mocking the poor, and that is a huge mistake. You shouldn't kick people when they are down. There are tens of millions of Americans that are deeply frustrated about losing their homes, losing their jobs or barely being able to survive in this economy. These frustrations have been one of the primary reasons for the rise of the Tea Party movement and the rise of the Occupy Wall Street movement. What these movements have in common is that people in both movements are sick and tired of the status quo and they want something to be done about our broken system. There are huge numbers of families out there right now that have just about reached the end of their ropes. Instead of showing compassion, many of the ultra-wealthy have decided that it is funny to mock the poor and those that are suffering. So how are all of these protesters going to respond to the "let them eat cake" attitude of the Wall Street elite? The protesters are being told that nothing that they can do will change anything and that they should be grateful for what Wall Street and the ultra-wealthy have done for them. They are essentially being told that they should just shut up and go home. So will we see these protest movements become discouraged and die down, or will the patronizing attitudes of so many among the elite just inflame them even further? Read More @ TheEconomicCollapseBlog.com

|

| BaNZai7 HaLLOWeeN KiCK OFF: QuoTH THe RaVeN, DEBTS NO MORE! Posted: 30 Oct 2011 02:14 PM PDT

THE RAVEN (Debts No More) (Edgar Allen Poe, The Raven) WilliamBanzai7 |

| Is Gold Over Or Undervalued? How About The EFSF (Europe = Fastow, Skilling & Fuld) Posted: 30 Oct 2011 01:26 PM PDT From Sean Corrigan In an opinion piece of our own, instigated by the gentlemen at Gold Money, we were asked how we work out whether gold is over or undervalued at any given minute. What a question at the best of times, much less now! What we came up with was the following, something which encapsulates a theme about which we have written much of late:?

And that pretty much sums up our commentary on the EFSF—the ''Excruciating Folly of Suspending Finality' or 'Endorsing Falsity to Succour the Few', or perhaps just 'Europe = Fastow, Skilling & Fuld'. Its agreement has ignited a rally—at that, one which could technically unwind much of the preceding rout, unless some renewed problem surfaces from among the many, murky lacuna in the details of how this Archimedean earth?mover will actually be knitted together; not least among them the suggestion that such a nakedly cynical attempt to frustrate the existential purpose of the CDS market might render its whole, multi?trillion edifice unstable and so force a widespread rebalancing of holdings across the physical bond market. To the extent that the deal does succeed in heading off an immediate meltdown, some removal of risk premia seems entirely justified, but that is not to say that Europe's problems are at an end, nor that the global economy does not now hover parlously between a stalling recovery and a renewed slump. Notable, too, is that fact that this month's stock index rally has been equally strongly felt in the KOSPI as in the DAX and in the TWSE as in the CAC, as the underweight institutionals and the 80% of hedge funds said to be under water scramble to take advantage of a rising tide with scant regard for which boat they are actually clambering aboard. Adding to the optimism (the jaundiced among us might say, the pessimism) that no bank in Europe is about to close its doors, is the hope that the Chinese authorities are on the verge of issuing one of their heaven?shaking decrees and so will restore the profitability of business there at a stroke, by relaxing their grip on official monetary policy. Since we all know just how swimmingly such steps have worked out in our own countries, in the aftermath of a dramatic episode of pervasive commodity and property speculation, we can immediately cast all cares aside the minute that the omniscient Communist Party issues a diktat to the effect that it will be adopting the success?garlanded procedures of Bernanke, King, et al. Sarcasm aside, the hoo?hah has been blown up over the declaration by Premier Wen that policy should be 'fine?tuned' and that banks should henceforth be more responsive to the needs of struggling small businesses—an exhortation which has predictably been parlayed up into a signal that the PBoC is about to cut reserve ratios ? and possibly interest rates— before year end. This comes despite Wen's continued insistence that the fight against inflation is still the number one priority. It also ignores the fact that while the policy banks may be encouraged to ration out their credit quotas a little more evenly in future, this potential liberalisation will go hand?in?hand with steps being already taken to crack down on the grey market for loans which is those same small firms' main lifeline at present. It also overlooks the fact that many SMEs told those conducting a recent survey of the sector that their main worry was not the availability of credit, but the inexorable rise in their cost base in a land where the increase in commodity prices has been second only to the ascent of wage rates in dampening their chances of achieving profitability. Nor does it pay much heed to the fact that people waking up to the idea that property prices may not just rise by 10?20% a year, but may fall 40?50% in an afternoon, might not be too impressed if SHIBOR trades 25bps lower in the near future. Never mind. In that old retailing maxim, it's not the steak that sells, it's the sizzle. If the story of an imminent Great Wall of Chinese liquidity being unleashed reinforces the desperate need to see asset prices higher, so be it, but those riding what might turn out to be a thoroughly misplaced interpretation of events should at least keep their stop?loss discipline while they ride the updraft higher.

|

| Posted: 30 Oct 2011 12:39 PM PDT Summary: Long term - on major buy signal. Short term - on buy signals. Buy signals in all of the ETFs, waiting for set ups. Read More...

|

| Posted: 30 Oct 2011 12:36 PM PDT Needless to say, the news that Europe is set to wholeheartedly embrace the economic principles of the likes of Alan Greenspan and Ben Bernanke and refill the punch bowl with a gusto set the markets ablaze. Markets love inflation, hate deflation ... Read More...

|

| MF Global Hires Two Bankruptcy Legal Advisors As Chapter 11 Looms Posted: 30 Oct 2011 10:35 AM PDT

The deadline to submit a bankruptcy filing to the Southern District of New York is around midnight, which probably explains why even as MF Global is proceeding at a feverish pace to sell parts or all of it to what appear increasingly skittish investors (who, like China will likely wait until the stalking horse auction to show their bids), it has, as the WSJ has just reported, hired bankruptcy and restructuring lawyers in the face of Weil Gotshal, best known for collecting hundreds of millions in hourly legal fees for its work on the Lehman bankruptcy case, as well as Skadden Arps. It appears that the sale process has not gone quite as well as hoped for, and now the company is bracing for the worst with just under 6 hours left to iron out a going concern solution. Per the WSJ: "MF Global Holdings Ltd., the troubled securities firm, has hired bankruptcy and restructuring lawyers, said people familiar with the matter, as it races to sell all or part of its broker-dealer in an effort to survive. MF Global, whose shares have plummeted amid investor concerns over its exposure to European government debt, has hired law firms Skadden, Arps, Slate, Meagher & Flom and Weil, Gotshal & Manges to prepare potential restructuring options, the people said. A bankruptcy filing or other restructuring transaction remains an option for MF Global should it be unable to get a sale done, one of the people said." Why two restructuring legal counsels? "Skadden joins restructuring and deal bankers at Evercore Partners advising MF Global. Other Skadden lawyers that don't specialize in restructuring are also advising the investment firm. Weil, meanwhile, would represent MF Global's U.K. subsidiary should it need to pursue some kind of formal restructuring proceeding overseas, a separate person familiar with the matter said. In addition, Sullivan & Cromwell's restructuring practice has also joined the fray advising MF Global, people familiar with the matter said. Non-restructuring lawyers at Sullivan are also working on the situation." And here comes, naturally, the hedge: "The hiring of restructuring advisers doesn't mean MF Global will necessarily seek bankruptcy protection. Such advisers work on a range of transactions, including raising new debt or equity or trying to find other out-of-court solutions to a company's woes. Still, a federal bankruptcy court could provide a venue for a potential sale of MF Global's assets. MF Global has been focused on trying to find buyers without resorting to bankruptcy." And while we, and most likely everyone else in the world, wishes Jon Corzine all the best, just in case all the best does not happen, we are confident there will be numerous reporters around the main entrance of Southern District of New York at 1 Bowling Green where the bankruptcy petition still has to be handed in physically should all else fail. Well, not all else: Corzine will have succeeded in handing over the firm he has headed for just about two years to Goldman Sachs on a bankruptcy, read 35 cents on the dollar, platter.

|

| The Big Mac Index: Is Your Country?s Currency Over or Under-Valued Compared to USD? Posted: 30 Oct 2011 10:14 AM PDT The Economist's Big Mac index is a fun guide to whether currencies are at their "correct" level. It is based on the theory of purchasing-power parity (PPP), the notion that in the long run exchange rates should move towards the rate that would equalise the prices of a basket of goods and services around the world. [As such, take a look at the chart below to see just how expensive a Big Mac is in your country (raw and adjusted for GDP per person)*and therefore, by inference, the extent to which your country's currency is over- or under-valued compared to the U.S. dollar.] Words: 421 So reports The Economist online ([url]www.economist.com[/url]) in edited excerpts from an article* which Lorimer Wilson, editor of www.munKNEE.com (Your Key to Making Money!), has further edited ([ ]), abridged (…) and reformatted below for the sake of clarity and brevity to ensure a fast and easy read. The author's views and conclusions are unaltered and no personal comments have been included to ma...

|

| Stock World Weekly: Europhoria Posted: 30 Oct 2011 08:17 AM PDT

Stock World Weekly: Europhoria

Excerpt from Europhoria, the week ahead section: The markets enjoyed this week's eurozone announcement, with its expansion of the EFSF, the 50% "haircut" for Greek bondholders, and the recapitalization of European banks. But the Europhoria was not universal, and many remain skeptical. For a well-done glimpse into the inner-workings of the eurozone's latest plan, watch this Xtranormal cartoon. Zero Hedge's take: "While it is not the bears doing the explaining in this latest all too realistic summary of the European non-bailout, it is the next best thing." We agree; we cannot find a better way to communicate the pure confusion. One obvious problem is the political and financial fallout from the "voluntary" 50% haircuts being agreed to by Greek bondholders. Now that Greek bondholders have been shorn, what will keep Italy, Spain and Portugal from asking for the same deal to help them out of their debt obligations? German Chancellor Merkel is already warning against this. She declared, "In Europe, it must be prevented that others come seeking a haircut." It is possible that the finance ministers of the eurozone have accomplished nothing more than to prevent fiscal contagion by exchanging it for a pandemic of debt forgiveness, as nation after nation lines up to ask their creditors to similarly accept 50% haircuts or perhaps even more. If these bondholder haircuts are deemed "voluntary," then their credit default swap (CDS) insurance won't pay out, because the event would not be considered a default. How this strategy will play out remains unknown. Jennifer Lee of BMO Capital Markets surmised,"Enthusiasm, so evident yesterday with the huge market rallies seen around the world, appears to have taken a backseat to the question 'How on Earth is all of this going to work?' The details, or the implementation of the grand plan, will be extremely difficult to carry out."(Indexes in idle mode: Stock rally fed by Europe deal slows) Lee Adler of the Wall Street Examiner closely follows the Federal Reserve and Treasury markets. He recently wrote to subscribers,"Investors sold Treasuries and bought stocks this week. The Treasury market took some heat due to a big slug of new supply, and a continuing buyers' strike by foreign central banks (FCBs). $48 billion in new Treasury supply settles on Monday. It's not clear whether there was enough liquidation of Treasuries last week to cover the bill. I suspect not, given that it looked like all of the cash was dumped right into equities. The dealers may still have a ton of Treasury inventory to get rid of, especially the 7 year note auctioned at the peak of the carnage on Thursday. "FCBs are in a short term cyclical upturn in their buying pattern, but this turn comes from an unprecedented level of weakness and the numbers coming off the low are pathetic, and still deeply negative. If this is the up phase, I can't wait to see the next down phase. It will be ugly. But we probably will not have to deal with that for at least another 6 or 8 weeks if typical timing holds for this buying cycle. "On the other hand, unless the FCBs step up to the plate much more than they have in the past couple of weeks, either the Treasury market will collapse, or the stock market rally will fizzle, or both. We're not there yet, but if these trends continue, make no mistake, the balance will tip. For the time being, the theme of one market rallying at the expense of the other can continue, but that's a limited term proposition. Once the FCBs go into their next normal retrenchment period, probably around the turn of the year, the situation should deteriorate. The rise in yields will become intolerable, and stock investors will probably start liquidating as a result. At that point, the Fed would be forced to step in to attempt to stave off financial collapse." (The Treasury Market Will Collapse) Summarizing his outlook for next week, Phil wrote, "We take a series of BALANCED trades – SELLING as much premium as we can so that time (theta decay) is always on our side. We take our profits off the table and, when we have to, we take our losses. However, we try to adjust the losing sides of our positions with the expectation that the markets will remain in a trading range and make the occasional reversals. We continue to play that range while the Big Chart is below the +10% lines. We will get MORE bearish as we move higher but we BALANCE our trades. Our bearish expectations are based on possible Yentervention by the BOJ, negative analysis of the EFSF over the weekend, and LACK of additional stimulus by the US, China and Japan to match the strong but Globally inadequate EU contribution." JW Jones's of OptionsTradingSignals shared his perspective with us. "In addition to the unknown factors impacting the European 'solution' next week the Federal Reserve will have their regular FOMC meeting and statement. There has been a lot of chatter regarding the potential for QE III to come out of this meeting. While I could be wrong, initiating QE III right after the Operation Twist announcement would lead many to believe that Operation Twist was a failure. "With interest rates at or near all time lows and the recent rally we have seen in the stock market, it does not make sense that QE III would be initiated during this meeting. It is possible that if QE III is not announced the U.S. Dollar could rally and put pressure on risk assets such as the S&P 500 in the short to intermediate term. If this sequence of events played out, a correction would be likely." Our trade ideas this week are from Phil's White Christmas virtual portfolio. One is to buy the SCO November $45/48 bull call spread, currently at $1.10. SCO ($44.94) is the ProShares UltraShort Crude Oil ETF which corresponds to 200% of the inverse of the daily performance of the Dow Jones-UPS Crude Oil Sub-Index. The premise behind this trade idea is that the price of oil has gone up a too quickly and is due for a pullback. Other ideas from the WCP are as follows (note: many bullish trades that worked were taken off the table, leaving those that didn't work - the bearish trades):

Click on this link for a free trial to Stock World Weekly.

|

| Posted: 30 Oct 2011 06:51 AM PDT

When it comes to discussing monetary history, and specifically what happens when it all goes horribly wrong, there are two must read tomes: one is "The Dying of Money" by Jens Parsson (pdf link) and the other one is "When Money Dies" (pdf link) by Adam Fergusson. Today, we are lucky to bring to you a must watch interview between James Turk of the GoldMoney Foundation and the author of the former, Adam Fergusson. They discuss the fateful decisions that led to hyperinflation in post-First World War Germany, and how central bankers as well as ordinary members of the public today would be well advised to heed this warning from history. Fergusson discusses how the hyperinflation affected different groups in German society in different ways – with debtors benefiting and huge numbers of middle-class savers wiped out. Riots, corruption and political extremism were just some of the malignancies encouraged by the hyperinflation. He points out that those who held hard currencies as well as people who held tangible assets like gold and silver were in-large part protected from the worst economic consequences of the hyperinflation. In his words: "gold remained at all times in Germany the measure of what was important to them." James and Adam discuss whether or not today there is any way for governments in the developed world to repay their huge debts. Both men conclude that inflation is the only politically viable method of repudiating these unmanageable obligations. Fergusson highlights the importance of velocity and the demand for money in determining whether or not inflation turns into hyperinflation – though points out that this tipping point can take a surprisingly long-time to arrive; in Germany, people kept confidence with the rapidly devaluing mark throughout the First World War, despite clear signs that the country was heading for a currency crisis. Fergusson thinks that we are heading for high inflation in many countries, but is doubtful that Weimar Germany's nightmare currency collapse can be replicated in a sophisticated modern economy. He concludes with a quote from Jean-Claude Juncker, prime minister of Luxembourg, who recently commented with respect of the sovereign debt crisis: "we all know what has to be done; what we don't know is how to get re-elected once we done it."

|

| Oktoberfest: When The Music (Money) Stops Playing (Flowing)… Posted: 30 Oct 2011 06:27 AM PDT Last week, the markets rallied sharply on news that banks were willing to take a 50% haircut on their Greek Bond holdings.

These kind of stimulus packages are like alcohol for the stock markets . They are fun and they make everything look better than it really is… The only problem is that if you get too much of it (alcohol) in a short time, the next day you will probably have a very bad hangover. The same is true with stock markets: when they rally too much over a too short time frame, the hangover will soon follow. In an article I posted on September 11th, I wrote the following: Let's start off with a chart of the German DAX index. While price makes lower lows, the RSI sets higher lows on a daily basis.

On August 12th, I posted the following chart of the dutch AEX index (for subscribers only) with the blue line being my expectations:

An updated version of this chart was posted on October 24th (for subsribers only): We can see that price (and thus also the Moving Averages) acted almost EXACTLY as forecasted. Following this sharp rise in stock markets over the past few weeks, prices are looking overbought in the short term, and price has now reached the 200EMA. When we look at the following chart, we can see that this 200EMA has often been an important level during both Bull AND Bear markets. Price was very stretched below the 200EMA a couple of weeks ago, and has tested this level last week. It might rise slightly above this 200EMA in order to attract as many bulls as possible, but so far, it looks like this is just a massive bear market rally (which we forecasted). Potential targets would be 320-335 points for the AEX.

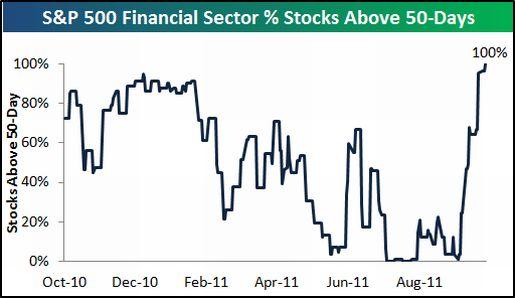

Bespoke Investment Group notes:

Bespoke also shows that 100% of the stocks in the Financial sector are trading above their respective 50-day moving averages… The financial stocks rallied big time, so everything is good now? I don't think so. When we look at the Ted spread (which is the difference between the interest rates on interbank loans and on short-term U.S. Government Debt), we can see that the tensions between the banks are growing, as the TED spread is reaching a 16-month high:

Gold rallied sharply as well last week, moving away from the green support line in the chart below:

As a result, the HUI index also rallied substantially.

Based on the chart above, we think the Mining stocks need to correct a bit along with the equity markets. However, gold looks set to test the all-time highs, so when/if we get a correction in gold mining stocks, it wil likely be a mild one… Conclusion: A couple of weeks ago, when everybody was looking for Financial Armageddon, we turned very bullish. Today, everybody is in a party mood, but we are leaving the party. When the music stops playing, everybody will rush for the exits, sometimes causing accidents. It's better to leave a bit too early and maybe miss the last song of the night (rally), than to leave too late and rush for the exits. There will be plenty of parties over the next couple of years.

|

| The "Dumb Money" Refuses To Play Along: China State Media Says It Won't Rescue Europe Posted: 30 Oct 2011 04:56 AM PDT

A few days ago China telegraphed it refuses to continue to be seen as the world's rescuer and the dumbest money in the room. Many assumed China was only kidding: after all how would China let its biggest export partner flounder? And furthermore, all China does is provide vendor financing, right? Well, as it turns out, wrong, because to China the current state of Europe is far from the terminal crisis Europe is trying to make it appear. This is happening even as a thoroughly desperate and grovelling Europe, kneepads armed and ready, has said via the EFSF's Regling that it will even consider issuing Yuan-denominated bonds. Alas, China is less than impressed. As AFP reports, "China's state media Sunday warned that the country will not be a "savior" to Europe, as President Hu Jintao left for an official visit to the region including a G20 summit. Hu's visit has raised hopes that cash-rich China might make a firm commitment to the European bailout fund, but in a commentary, the official Xinhua news agency said Europe must address its own financial woes. "China can neither take up the role as a savior to the Europeans, nor provide a 'cure' for the European malaise. "Obviously, it is up to the European countries themselves to tackle their financial problems," it said, adding that China could only do so "within its capacity to help as a friend." A friend, who at this point is quite sensible, and realizes far better deals are to be had down the line if one merely waits. That said, we are certain China is not the only one out there with an instant notification pending the second Santorini, Ibiza or the Isle of Capri hits E-bay. More:

The bold says it all. And for those to whom it is still confusing:

So, about that magical European box full of promises and quite empty of money...

|

| Posted: 30 Oct 2011 12:45 AM PDT Historian Adam Fergusson discusses his cult-classic history of the Weimar hyperinflation, When Money Dies, with James Turk from the GoldMoney Foundation. In this video they discuss how speculators, ...

|

| Dollar Breakdown Triggers Stock Markets Risk Rally, It's All About the 3's Posted: 29 Oct 2011 09:45 PM PDT Dollar Breakdown Triggers Stock Markets Risk Rally, It's All About the 3's Last week I wrote about the key support that needed to hold for the DX at 76.50, the rest is history, but it's clearly obvious with the strength that we saw towards the middle of the week in risk markets, you saw a significant breach of that support, which suggests that all we saw is a 3 wave rally.

|

| Gold and Silver News 10/29/2011 EU Debt Deal Posted: 29 Oct 2011 06:58 AM PDT EU Debt Deal, Eliminating USD, US Mint Sales of Gold and Silver Eagles

|

Last week the weight of the evidence suggested that silver was late in a base building process, and our judgement that this was the case was vindicated by subsequent action, when it broke out upside from the intermediate base pattern during the week in response to the inflation positive news out of Europe. This is discussed in some detail in the Gold market update, but suffice it to say here that Europe has decided that it will attempt to print its way out of trouble, just like the US, which is great news for holders of inflation hedges like gold and silver.

Last week the weight of the evidence suggested that silver was late in a base building process, and our judgement that this was the case was vindicated by subsequent action, when it broke out upside from the intermediate base pattern during the week in response to the inflation positive news out of Europe. This is discussed in some detail in the Gold market update, but suffice it to say here that Europe has decided that it will attempt to print its way out of trouble, just like the US, which is great news for holders of inflation hedges like gold and silver.

{kind=link}

| You are subscribed to email updates from Save Your ASSets First To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment