Gold World News Flash |

- Rick Rule - Physical Supply Shortages in Silver

- 11 Reasons Why the Gold Bubble Will Burst

- Jim?s Mailbox

- U.S. Dollar Update aka Geithner Is Full Of Sh!t

- John Embry - Gold & Silver Commercial Signal Failure

- Lunch With the Treasury Secretary

- Grandich Client Oromin Explorations – Going for “World Class” Gold in West Africa

- Jim's Mailbox

- Wall Street Journal joins brokers in trying to talk investors out of gold

- As Expected, Goldman FX Closes EURCHF At Loss To Clients, Profit To Zero Hedge Readers

- Weekly Recap, And Upcoming Calendar - Here Are The Main Events To Look For

- Weekend SPX, Dollar, Oil and Gold Analysis

- Honest Money Gold and Silver Report: Market Wrap Week Ending 10/22/10

- Correcting

- Lawrence White on Austrian Economics, Free-Banking and Real Bills

- Gene Arensberg: Big commercial shorts not piling on in gold and silver

- Turning Points

- Gold, Silver, and Mining Stocks Pause

- International Forecaster October 2010 (#7) - Gold, Silver, Economy + More

- Gold at Foothills of a Mania

- Don't Fear the Euro

- Has Gold Fallen Far Enough? Not Necessarily.

- Has Gold Fallen Far Enough? Not Necessarily

- COT Flash - October 24, 2010

- Client newsletter release tomorrow

- Bank ‘Reform’ Makes All Oligarchs Permanently Too-Big-To-Fail

- Profit, Policy and Propaganda

- Risk in Everything, Including Gold

- "Good Time" to Buy Gold

- Who Will Defend the US Dollar?

- US Commercial Real Estate: "A Mess"

- Fake Money, Real Silver

- Default or Hyperinflation: The US’s Only Two Options

- G20 forswears currency, trade wars but sniping starts right up again

- Goldman: The Fed Needs To Print $4 Trillion In New Money

- War On?

- Gold and the Great Depression; the Great Myth

- Indonesia is On Fire

- Gold's in a Mini-Mania, Not a Bubble

- The G20 Meeting of Finance Ministers. Success, Failure, or Irrelevant?

- Guaranteed Hyperinflation: Expect Another Big Year for Precious Metals

- QE2 Is About Assets, Not Banks

| Rick Rule - Physical Supply Shortages in Silver Posted: 24 Oct 2010 09:23 PM PDT With gold and silver correcting, King World News interviewed one of the great minds in the resource world, Rick Rule. Rick is one of the most level-headed individuals in the business, so what he said about silver was shocking,"We are seeing huge inflows into physical silver, and that may create a shortfall of available physical silver." He also mentioned, "Silver strip and silver coin demand continues very, very strong as well."

|

| 11 Reasons Why the Gold Bubble Will Burst Posted: 24 Oct 2010 06:17 PM PDT James Altucher submits: I first wrote about gold in early July at WSJ.com. I took a lot of heat then but the jury is still out. In fact, since July 9, stocks and gold have performed almost exactly the same. But with stocks trading at record low multiples over earnings (versus bond yields) and with gold at an all time high I can think of 11 straightforward reasons why the Gold Bubble is going to burst and stocks are the primary place one should put their money.

Complete Story »

|

| Posted: 24 Oct 2010 05:51 PM PDT View the original post at jsmineset.com... October 24, 2010 06:51 PM The Strong Follow Capital Flows While Weak Follow Fear CIGA Eric The strong continue to recognize and follow strength while the weak are dismantled from the trend by disinformation and fear. The break of the 2009 swing low suggests an acceleration of the out performance of gold stocks relative to equities. This likely acceleration is illustrated by the green arrows in the chart below. U.S. Large Cap Stocks Capital Appreciation Index (LCSCAI); S&P 500 to S&P Gold Ratio (GPM)*: * S&P Gold from 1945, Barron’s Gold Stock Index from 1939-1945, Homestake Mining: More… Silver’s Footprint of Control CIGA Eric The normal footprint of control by ‘connected money’ is revealed by the combination of opposite arrows. That is, selling strength (green up and red down) and buying weakness (red down and green up). This footprint of control was first broken by lat...

|

| U.S. Dollar Update aka Geithner Is Full Of Sh!t Posted: 24 Oct 2010 05:49 PM PDT The USDX appears to have resumed it's descent tonight on the heels of the G20 meeting. In reference to my last post about the dollar, I said that from a "chart perspective" the dollar was oversold and could go through a corrective bounce that might take it back up to the 80-81 level. At the same time, I said that if it failed to trade back up to its resistance at 80 and rolled over again that it would be very bearish. Here are updated weakly and daily daily charts of the spot dollar price as of this evening:   (click on charts to enlarge) The charts are pretty much self-explanatory. I leave it to each reader to draw their own conclusions about where they think the dollar is headed next. I will say that it has become a source of extreme comedic relief watching Geithner prostitute his stupidity every time he's on the world stage pontificating about U.S. policy support of a strong currency. It's clear from the action in gold and silver tonight that the gold hoarding countries of the world are laughing at him along with me, as the price of these monetary metals has shown solid resilience in the face of the attempted price takedown last week by the bullion banks. The big bullion accumulators do not really seem to care about the gold-bashing rhetoric flooding from the U.S. media. Given the rapid decline in sentiment indicators at the end of last week, it would appear gold and silver could continue their rapid ascent up the proverbial "wall of worry." I'm not willing to go out on a limb and proclaim that the pullback in the bullion market is over. However, judging from the action in both the SPX and bullion futures tonight, it would appear that the U.S. financial and economic system is starting to assume "Weimar-esque" characteristics. Avete oro? This is an excellent article which was linked in Friday's "Midas" report at http://www.lemetropolecafe.com/. I have never read this guy before, but it is an insightful commentary on the dynamic of the current bullion market: FinanceAndEconomics.org

This posting includes an audio/video/photo media file: Download Now |

| John Embry - Gold & Silver Commercial Signal Failure Posted: 24 Oct 2010 04:30 PM PDT  John Embry, Chief Investment Strategist for Sprott Asset Management, believes the long awaited commercial signal failure in gold and silver may be at hand: "...demonstrated by an explosion in open interest on the Comex as the usual suspects shorted aggressively in an attempt to mitigate the relentless buying that was occurring. This, I suspect, will result in either another correction, which should be short and shallow, or more probably, the long-awaited commercial signal failure in which the shorts are overrun and forced to cover in a rising market." John Embry, Chief Investment Strategist for Sprott Asset Management, believes the long awaited commercial signal failure in gold and silver may be at hand: "...demonstrated by an explosion in open interest on the Comex as the usual suspects shorted aggressively in an attempt to mitigate the relentless buying that was occurring. This, I suspect, will result in either another correction, which should be short and shallow, or more probably, the long-awaited commercial signal failure in which the shorts are overrun and forced to cover in a rising market."

This posting includes an audio/video/photo media file: Download Now |

| Lunch With the Treasury Secretary Posted: 24 Oct 2010 03:59 PM PDT

When I wake up at 4:30 am each morning to check the overnight markets and review the opening salvo of incoming emails, I often have trouble focusing my eyes in my groggy state. So I had to blink twice when the first message in my inbox politely inquired if I had time to meet the Secretary of the Treasury in Palo Alto for lunch that day, apologizing for the short notice. Tim Geithner was in San Francisco for a day to meet with a small group of venture capitalists and other business leaders. It was a short stop in his way to the G-20 meeting on finance ministers in Seoul, South Korea. I can’t say who else was invited. Suffice it to say that I was the only one without an NYSE or NASDAQ listing. When I greeted lithe, athletic, but diminutive Treasury Secretary, I could see the six secret service agents in the room visibly tense up. At 6’4” I towered over him, but he shook my hand firmly. At 49, he is one of the youngest Treasury Secretaries on record. He is also the first one who surfs, so I if he had stowed his board on Air Force One so he could shoot “Steamer Lane” in nearby Santa Cruz after the meeting. He laughed, confessing that he rode the waves in a less than adequate fashion. Geithner succinctly laid out the administration’s position on a wide range of financial and economic issues. The economy is now healing, has been growing for 18 months, but conditions were still very tough, especially if you were in construction, real estate, or small banks. Private sector investment grew of 20% in H1, but then slowed down to 10% in H2. Exports are strong. The economy is undergoing some difficult, but necessary changes. The crisis was caused by excessive debt levels, the adjustment of which is now mostly behind us. The savings rate has soared from below 0% before the crisis to 4%-6% today. The debt burden is falling. Still, further measures are required. Geithner thrilled his audience by proposing a permanent investment tax credit for domestic R & D. On top of that, he wants to add a one year tax credit for capital investment. It was music to the ears of those present, who were primarily engaged in the business of starting new companies. He would also eliminate tax preferences that encouraged companies to build plants overseas. At the very least, the playing field should be level. Stepped up spending on infrastructure is a big priority, which has suffered from decades of neglect and under investment. The US is not a country with unlimited resources, and this is where the taxpayer gets the highest return on money spent. He also highlighted the urgency to extend tax cuts for the bottom 98% of the working population. The country entered the crisis with an unsustainable fiscal situation, and this would help address that. Geithner says that the US would not engage in a debasement of its currency. It is very important that our counterparties believe that we will fulfill our long term obligations. The US benefits from the dollar being used as a reserve currency, and there will be no non dollar reserve currency in our lifetimes. The Dodd-Frank bill was an essential reform, as a huge financial industry had grown up outside the existing rules. Banks needed bigger shock absorbers. Governments do a very bad job at picking industries to protect, which only supports the weak at the expense of consumers. Geithner said that by any measure, the Chinese Yuan was undervalued, and that was unfair to all of the country’s trading partners. Although this was enabling China to reap short term benefits, long term it meant that the US was setting its monetary policy. A flexible exchange rate would give China economic independence and soften the impact of imported inflation. When asked what exchange rate he would be happy with, he would only say “HIGHER”. Geithner has devoted much of his life to public service. He spent his childhood abroad while his father was a micro finance administrator for the Ford Foundation, growing up in Zimbabwe, Indonesia, and India, and finally graduating from high school in Bangkok. He did his undergrad at Dartmouth, and obtained a master’s in Asian studies at Johns Hopkins, where he gained fluency in Chinese and Japanese. I first met Tim myself two decades ago, when he was a low level Treasury attaché at the Tokyo embassy who spoke the local language flawlessly. The embassy then was mostly staffed with plodding civil servants plodding towards an early retirement. Tim, who spoke the local language flawlessly, was the brightest bulb in a fairly dark closet. When I departed meetings at the Ministry of Finance and the Bank of Japan, I passed him on the way in. I dare say the order would be reversed today. After that, his rise was meteoric, from Undersecretary of the Treasury for International Affairs, to President of the New York Fed, to his current gig. Geithner put on quite the performance. No matter what the question, he was able to caste it in the context of its historical background, the lead up over the past two decades, the current policy response, and parallels with other major and minor countries. We jumped from the Japanese stagnation, to the Swedish banking crisis in the early nineties, to Indonesia’s explosion of hyperinflation in the sixties, to the Mexican debt crisis, all within a minute. His canned answers to standard question rolled effortlessly off his tongue, while original problems delivered an intensity of thought one rarely sees. Before he left, I pulled out all the cash in my wallet and pointed out to Geithner that while I had bills signed by previous Treasury Secretaries Larry Summers, Paul O’Neil, and Robert Rubin, I lacked one with his illegible scrawl. Did he have any which he could exchange with me? He sheepishly admitted that while such bills existed, they we being held back from circulation until the Treasury’s existing stockpile of Hank Paulson bills ran out, in order to deliver taxpayers good value for money. I would only see his bills once the economy recovers and the growth of M1 starts to accelerate. That is truly an answer one would expect from the 75th Treasury Secretary. To see the data, charts, and graphs that support this research piece, as well as more iconoclastic and out-of-consensus analysis, please visit me at www.madhedgefundtrader.com . There, you will find the conventional wisdom mercilessly flailed and tortured daily, and my last two years of research reports available for free. You can also listen to me on Hedge Fund Radio by clicking on “This Week on Hedge Fund Radio” in the upper right corner of my home page.

|

| Grandich Client Oromin Explorations – Going for “World Class” Gold in West Africa Posted: 24 Oct 2010 03:40 PM PDT The following is automatically syndicated from Grandich's blog. You can view the original post here. Stay up to date on his model portfolio! October 24, 2010 07:35 PM The global search for 'world-class' gold deposits has transformed West Africa into one of the fastest growing gold production and exploration area in the world, thanks to the efforts of visionary companies such as Oromin Explorations Ltd. West African gold production has increased by 53% over the past decade and the region continues to generate multi-million-ounce gold discoveries at a time when similar discoveries are declining in more mature mining districts, notably in the Americas and Australia. Oromin may not have the highest profile or market valuation of the rapidly growing list of West Africa gold explorers — having focused more on drilling programs than self-promotion — yet has achieved a track record of success that warrants serious attention from industry and investors. *Within the past five years, the com...

|

| Posted: 24 Oct 2010 02:51 PM PDT The Strong Follow Capital Flows While Weak Follow Fear The strong continue to recognize and follow strength while the weak are dismantled from the trend by disinformation and fear. The break of the 2009 swing low suggests an acceleration of the out performance of gold stocks relative to equities. This likely acceleration is illustrated by the green arrows in the chart below. U.S. Large Cap Stocks Capital Appreciation Index (LCSCAI); S&P 500 to S&P Gold Ratio (GPM)*:

Silver's Footprint of Control The normal footprint of control by 'connected money' is revealed by the combination of opposite arrows. That is, selling strength (green up and red down) and buying weakness (red down and green up). This footprint of control was first broken by late 2005 – early 2006. Connect money began buying strength rather than selling weakness. The introduction of the silver ETF (SLV) in April 2006 and Buffett's coincidental decision to sell his silver holdings (largely assumed to seed or front the paper silver ETF) provided material redirection of physical demand towards paper. The normal footprint of control had resumed by the fall of 2006. The footprint of control, similar to 05-06, is once again showing signs of strain. Connected money is uncharacteristically buying rather than selling strength to contain the advance. Could this second and even-more powerful surge in demand for physical demand finally overwhelm the controlling mechanism of the paper market? It's likely that something material is going on here. Silver London P.M Fixed and the Commercial Traders COT Futures and Options Stochastic Weighted Average of Net Long As A % of Open Interest:

|

| Wall Street Journal joins brokers in trying to talk investors out of gold Posted: 24 Oct 2010 01:00 PM PDT Advisers Try to Tame Investors' Appetite for Gold By Ian Salisbury http://online.wsj.com/article/SB1000142405270230435410457556841049510600... As individual investors hop on the gold bandwagon, financial advisers are finding themselves in an all-too-familiar role: that of mom and dad slapping hands away from the cookie jar. The precious metal has enjoyed a long run-up, gaining about 25% in the past year and consistently making headlines with records pushing ever higher. Also fueling the buying binge is a number of big-name investors like Paulson & Co.'s John Paulson. Gold prices stood at $1,324.40 a troy ounce Friday. Such price spikes and high-profile bullishness often create a ticklish situation for advisers: They think about selling just as clients want to buy. "I am not a gold bug, but I have a couple of clients that have just insisted," said Jim Heitman, a financial planner in Alta Loma, Calif. "Even as they objectively recognize the threat of a bubble, they just don't seem to care." ... Dispatch continues below ... ADVERTISEMENT Prophecy Resource Goes Into Production A commission appointed by Mongolia's Ministry of Mineral Resources and Energy has conducted the final permit inspection at Prophecy Resource Corp.'s Ulaan Ovoo mine site and has instructed the company to begin coal production. Prophecy Resource (TSX.V: PCY) has begun production of its first 10,000 tonnes of coal as a trial run of supply to be taken by rail to electric power stations in Darkhan and Erdenet, Mongolia's second and third largest cities after the capital, Ulaanbaatar. The company is the second-ever Canadian mining company to get a permit to mine in Mongolia and start production there. For the company's complete announcement, please visit: http://www.prophecyresource.com/news_2010_oct14.php Mr. Heitman says he sometimes uses commodity-sensitive stock funds such as PowerShares Dynamic Basic Materials Sector ETF but doesn't like making direct bets on a single commodity like gold. To clients who walk in the door craving gold, he makes two arguments. For one, long-term gold prices merely keep pace with inflation, and investors should concentrate instead on their broader goals like what kind of income they would like to generate. For those that won't be swayed, he points toward SPDR Gold Trust, but he keeps the exchange-traded fund at no more than 5% of their overall portfolios. Trying to talk clients out of hot investments is nothing new for financial advisers. In some ways, advisers say, the gold boom is easier to deal with than past spikes like the Internet-stock bubble in the late 1990s. The Internet bubble proved to be the cap on a 20-year bull market that had many investors feeling invincible. After the dot-com blowup and the market crash that rocked Wall Street in 2008, few are feeling that way. George Middleton, a financial adviser in Vancouver, Wash., says the current fascination with gold began in 2009, spurred in part by desire for a safe harbor. As the price of gold has climbed steadily, investors have remained interested, if not always for the same reasons. While many of his clients own iShares Gold Trust, he has been selling small lots to keep the metal from becoming too big a part of their portfolios. Clients "check to make sure they own it; then they ask should I buy more?" Mr. Middleton said. "The answer is usually 'No.'" Financial adviser Bob Kargenian, in Orange, Calif., has gone a step further and begun to sell. For instance, for his moderately aggressive clients, he has cut exposure to Van Eck International Investors Gold Fund, a mutual fund that focuses on gold miners, to about 1.8% of investment portfolios from about 3.5% at the end of September. Investors have hired him to protect them from their own worst instincts, he explains, particularly in situations like this. "If clients start calling us up and saying, 'We want to see gold,' that is like the kiss of death," he joked, noting the general public's tendency to arrive at good investment ideas too late. "It's like seeing it on the cover of Time magazine." Join GATA here: New Orleans Investment Conference * * * Support GATA by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Or a video disc of GATA's 2005 Gold Rush 21 conference in the Yukon: * * * Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit:

|

| As Expected, Goldman FX Closes EURCHF At Loss To Clients, Profit To Zero Hedge Readers Posted: 24 Oct 2010 01:00 PM PDT

On the 19th of October, we told readers that Goldman is pitching a short EURCHF trade; and that, as a result, it is time to go long. Back then we said: "Like every other time Goldman says to do something, the prudent thing to do is the opposite. Of course, this means more weakness for gold, as the Swiss Franc is simply the safest equivalent of gold in the monetary realm. Oh well - if better cost bases are to be had, than so be it." We were pretty much spot on, as usual, vis-a-vis our evaluation of Goldman involvement (and gold has indeed presented a better cost basis). Since then, the EURCHF has ploughed straight up, and gold has plunged. Just relased: Goldman has closed the EURCHF trade, after the 1.36 limit was hit. End result to clients - loss of 1.4%. End result to those who took our slightly jaded view on things: profit of 1.4%. We also suggest readers take profit on our "profit" limit being hit. From Goldman:

And here is how the EURCHF fared since the 19th:

|

| Weekly Recap, And Upcoming Calendar - Here Are The Main Events To Look For Posted: 24 Oct 2010 12:48 PM PDT

Week in Review – Markets on a Soul Searching Mood From Goldman Sachs

|

| Weekend SPX, Dollar, Oil and Gold Analysis Posted: 24 Oct 2010 12:36 PM PDT Last week was volatile thanks to China raising their interest rates a quarter basis point. This rate hike caused the Dollar to spike in value which in turn forced equities and metals to sell off sharply. This one day event caused equities ... Read More...

|

| Honest Money Gold and Silver Report: Market Wrap Week Ending 10/22/10 Posted: 24 Oct 2010 12:22 PM PDT Most markets are keying off the dollar. Since June, the dollar has fallen precipitously, from a high of 88.78, to the recent low of 76.14, a loss of over 14%. This has placed a strong bid under stocks, commodities, and precious metals ... Read More...

|

| Posted: 24 Oct 2010 12:21 PM PDT [U]www.preciousmetalstockreview.com October 23, 2010[/U] The G20 meetings this weekend seem to have ended as they began. The two heavyweights are China and the US. The US says that China must let it’s currency appreciate since they have such a large external surplus. But why should China let it’s currency rise? They didn’t create all these dollars that in turn are forcing other currencies to fall in value, nor did they directly force the US to incur such a deficit. The fact is the US has already massive and still growing unfunded liabilities that it simply cannot fund in any way shape or form except by devaluing the home currency which unfortunately at the time was the major global unit of trade. Got physical Gold and Silver yet? Metals review Gold slid 2.96% this past week and began it’s much needed correction. Gold was trading with more and more volatility recently and it was simply too diffi...

|

| Lawrence White on Austrian Economics, Free-Banking and Real Bills Posted: 24 Oct 2010 12:12 PM PDT Sunday, October 24, 2010 – with Ron Holland Dr. Lawrence White The Daily Bell is pleased to present an exclusive interview with Lawrence White (left). Introduction: Lawrence H. White is a professor of economics at George Mason University. Prior to position at George Mason, he was the F. A. Hayek Professor of Economic History in the Department of Economics, University of Missouri-St. Louis. He has been a visiting professor at the Queen's School of Management and Economics, Queen's University of Belfast, and a visiting scholar at the Federal Reserve Bank of Atlanta. Professor White is the author of The Theory of Monetary Institutions (Blackwell, 1999), Free Banking in Britain (2nd ed., IEA, 1995), and Competition and Currency (NYU Press, 1989). He is the editor of several works, including The History of Gold and Silver (3 vols., Pickering and Chatto, 2000), The Crisis in American Banking (NYU Press, 1993), African Finance: Research and Reform (ICS Press...

|

| Gene Arensberg: Big commercial shorts not piling on in gold and silver Posted: 24 Oct 2010 12:01 PM PDT 8p ET Sunday, October 24, 2010 Dear Friend of GATA and Gold (and Silver): A flash from Gene Arensberg's "Got Gold Report" tonight finds it remarkable that the big commercial shorts were responsible for a declining share of the open interest in the gold and silver futures markets this week, suggesting that they were not at all confident of lower prices. Arensberg's report is headlined "COT Flash October 24" and you can find it here: http://library.constantcontact.com/doc205/1103244937002/doc/4AX4VRa4KlbM... CHRIS POWELL, Secretary/Treasurer ADVERTISEMENT Prophecy Resource Goes Into Production A commission appointed by Mongolia's Ministry of Mineral Resources and Energy has conducted the final permit inspection at Prophecy Resource Corp.'s Ulaan Ovoo mine site and has instructed the company to begin coal production. Prophecy Resource (TSX.V: PCY) has begun production of its first 10,000 tonnes of coal as a trial run of supply to be taken by rail to electric power stations in Darkhan and Erdenet, Mongolia's second and third largest cities after the capital, Ulaanbaatar. The company is the second-ever Canadian mining company to get a permit to mine in Mongolia and start production there. For the company's complete announcement, please visit: http://www.prophecyresource.com/news_2010_oct14.php Join GATA here: New Orleans Investment Conference * * * Support GATA by purchasing a colorful GATA T-shirt: Or a colorful poster of GATA's full-page ad in The Wall Street Journal on January 31, 2009: http://gata.org/node/wallstreetjournal Or a video disc of GATA's 2005 Gold Rush 21 conference in the Yukon: * * * Help keep GATA going GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at: To contribute to GATA, please visit:

|

| Posted: 24 Oct 2010 11:43 AM PDT There is continued evidence that we are approaching a short-term top, but confirmation will come only when the current uptrend line is broken and the SPX decline below 1160. GLD has entered a period of consolidation ... Read More...

|

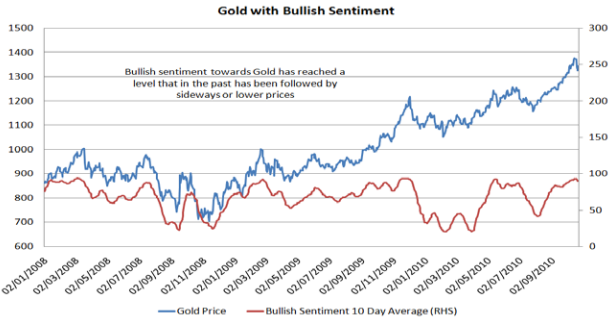

| Gold, Silver, and Mining Stocks Pause Posted: 24 Oct 2010 11:30 AM PDT Here's a chart from the current issue of the investment newsletter at Iacono Research. It's been quite a ride for gold, silver, and mining stocks in recent months, their future direction now uncertain as the world waits to see what Ben Bernanke and the crew at the Federal Reserve do in ten days after the most highly anticipated Fed meeting in quite some time.

Full Disclosure: Long gold, silver, and mining stocks

|

| International Forecaster October 2010 (#7) - Gold, Silver, Economy + More Posted: 24 Oct 2010 11:16 AM PDT The foreclosure crisis has set its sights on MERS, the Mortgage Electronic Registration Systems, which files almost all of the foreclosure actions in behalf of lenders. The problem never anticipated by lenders is that the company has no legal standing to do such things. In addition they broke the law by not requiring a notarized document of transfer of title signed by the seller and buyer.

|

| Posted: 24 Oct 2010 11:12 AM PDT The connotation of "foothills" is a perfect way of stating precisely where we are at in the collapse of the US Dollar based global financial system and the return of the king, gold, as money. It is perfect because while we are certainly seeing a movement towards a mania, with gold hitting fresh all-time highs in US Dollar terms on almost a daily basis throughout September and much of October, we are still far from reaching the top of the mountain.

|

| Posted: 24 Oct 2010 11:04 AM PDT When the euro hit a low of $1.1917 against the US dollar on June 7th, 2010, the airwaves crackled with assertions that the European common currency, beset by Greek debt problems and intra-union discord, was destined to trade at parity with the greenback. They were wrong.

|

| Has Gold Fallen Far Enough? Not Necessarily. Posted: 24 Oct 2010 11:01 AM PDT We've heard a lot about the currency war, but next thing you know they'll be calling it the McCurrency War. If we needed any proof that the Chinese yuan is 40 per cent undervalued, we finally got it from the Economist. The magazine's famous Big Mac Index compares the prices of a Big Mac in various countries making exchange rate theory more easily digestible.

|

| Has Gold Fallen Far Enough? Not Necessarily Posted: 24 Oct 2010 10:52 AM PDT We've heard a lot about the currency war, but next thing you know they'll be calling it the McCurrency War. If we needed any proof that the Chinese yuan is 40 per cent undervalued, we finally got it from the Economist. Read More...

|

| Posted: 24 Oct 2010 08:56 AM PDT As we expected, gold pulled back this week and so did silver. However, the action in the CFTC commitments of traders reports is not exactly what we expected to see at this point in the pullback.

|

| Client newsletter release tomorrow Posted: 24 Oct 2010 07:51 AM PDT Tomorrow we release the November issue of USAGOLD News, Commentary & Analysis. The lead article this month is Pete Grant's annual comparative investment survey. You will not be surprised at what tops the list in the five and ten year studies, but what tops the list for the past year might make you feel a bit light-headed. (Gold finished a close second.) In "Gold in the time of currency wars" find out how the developing currency war might develop as a "war of attrition" in which "all sides are 'bled white'" and gold ends up the primary beneficiary. Also, this month's "Nuggets" section includes our take on the former Treasury undersecretary Ted Truman's proposal to sell the national gold reserve — Truman's Folly sounds a lot like Gordon Brown's Folly. We also talk about why the helium pumped into Wall Street's balloon might suddenly go flat. WE INVITE YOU TO SUBSCRIBE by going here. There is a no-hassle sign-up box in the upper left corner. Typically between 15,000 and 30,000 read our monthly take on gold market happenings, and we think this month's issue will be particularly relevant to our regular clientele and newcomers alike. Best of all. . . . .It's still FREE of charge.

|

| Bank ‘Reform’ Makes All Oligarchs Permanently Too-Big-To-Fail Posted: 24 Oct 2010 07:50 AM PDT By Jeff Nielson, Bullion Bulls Canada The Obama regime must feel like a jilted-lover, as Wall Street has chosen to expend the vast majority of their politician-buying dollars buying Republicans in the next election. After all, the Democrats have demonstrated that they can serve the bankers at least as faithfully and unreservedly as the Bush regime did before them. The crowning achievement of the Obama regime in serving its masters is the so-called "bank reform" in the Dodd-Frank bill – arguably created by the Democrats' two most dedicated banker-servants (outside Obama, himself). The goals for this so-called "bank reform" were numerous and explicit. There was supposed to be "regulation" of the derivatives market. There was supposed to be both the authority and the practical means of shutting-down the too-big-to-fail Oligarchs. There was supposed to be greater "oversight" (as in more than zero). There was supposed to be an end to reckless, bankster risk-taking. And overall, markets in general and the financial sector in particular were supposed to be made more stable (i.e. protected from reckless, bankster gambling). None of those goals has even remotely been accomplished. Indeed, it is arguable that the Obama regime (and Dodd and Frank in particular) actually managed to make things worse in every respect. No one has been watching both the bankers and the farce of bank "reform" closer than Gretchen Morgenson of the New York Times. In a detailed piece titled "Count on Sequels to TARP", Morgenson explains the Democrats' most-important failure – in the derivatives market. The "clearinghouse" which was created in the new legislation does virtually nothing to either regulate derivatives, nor to make them more transparent. Indeed, all it really accomplishes is to increase "liquidity" for the bankers – which always translates into the banksters simply ratcheting-up their leverage even further. As if this wasn't bad enough, instead of merely having the implicit backing of the U.S. government in back-stopping the reckless gambling of the Oligarchs, an explicit government guarantee has been created for this "clearinghouse". In other words, all the clearinghouse actually accomplishes is to create an explicit, unlimited "tap" of government funds – directly from the printing-press of the Federal Reserve and/or the coffers of the Treasury Department. Having "guaranteed" (and nationalized) the entire U.S. mortgage market, having provided a (literally) infinite "guarantee" on Fannie and Freddie's endless losses, the U.S. government is now explicitly backing the $1.5 quadrillion derivatives market – which is more than twenty times larger than the entire, global economy. The Obama regime (and their apologists) will disingenuously point to the "resolution authority" that was created in the so-called reforms. It is obviously totally meaningless. Governments could pass the "resolution authority" to end poverty, hunger, violence, or even to fly to another galaxy. Creating the authority to do something is irrelevant when there could never be a practical means of exercising such authority. Specifically, in every meaningful way, the Obama regime has made the Wall Street Oligarchs even more "too big to fail". To begin with, all of the Oligarchs (except AIG) are much bigger than before – having not merely been allowed to cannibalize many of their former brethren, but receiving $trillions in government hand-outs/guarantees/loans (mostly from Republicans) to facilitate their rapid expansion. Those funds provided to Wall Street were explicitly given in return for the Oligarchs' pledge to increase lending in the U.S. economy. The Oligarchs did the exact opposite – greatly reducing their lending, and spending all the money on buying-up other bank assets and increasing their reckless gambling – with the derivatives market having roughly doubled in size since the Wall Street-induced "financial crisis" began. So, the Oligarchs are much, much bigger. They have doubled their reckless gambling, and now the U.S. government is explicitly backing their private casino: the derivatives market. What this means is that in the next systemic crisis created by Oligarch-greed, the argument which will be advanced (by both Republicans and Democrats) is not that the Oligarchs have to be saved because they are "too big to fail". Even for the apathetic sheep of the American electorate, this would be too great an outrage. No, in the future, unlimited and infinite funding of the banksters' gambling will be provided by the U.S. government because with the U.S. now "guaranteeing" an amount which exceeds twenty times global GDP, it is the solvency of the United States, itself which is now directly on the line in each-and-every future crisis created by these bankers. More articles from Bullion Bulls Canada….

|

| Posted: 24 Oct 2010 07:50 AM PDT By Jeff Nielson, Bullion Bulls Canada Roughly a year ago, I wrote a two-part feature on the U.S. housing sector. I explained how this entire economic catastrophe was a massive, deliberate scheme on the part of the Wall Street Oligarchs. I pointed out how these fraud-factories methodically created the largest Ponzi-schemes in human history – so that they could scam all their victims (i.e. investors) on the way up, and steal tens of millions of homes from their other victims (U.S. homeowners) on the way down. The articles received little attention. Given that this massive, bankster fraud is now totally out into the open, I'm assuming that there will be a larger and more interested audience when I illustrate this again – armed with the benefit of hindsight. The first point to make to readers is with respect to mortgage securitization, as without this key element of their scheme, the Ponzi-schemes Wall Street could have generated would have only been (relatively) nickel-and-dime fraud – like Bernie Madoff. With mortgage securitization, the banksters were able to erect a $1+ quadrillion mountain of fraud (roughly equal to 2,500 "Bernie Madoffs"). Typically, U.S. banks had previously been allowed to leverage themselves by an average of roughly 10:1. In other words, every time a dollar was deposited with them, they would lend-out (or "invest") ten dollars (invented "out of thin air"). While this is a reckless amount of leverage (and money-creation) to allow into any system which is supposed to remain "stable", it did not represent a systemic threat to the entire financial sector. Then the banksters went to work. First, they convinced their weak-minded servants in the U.S. government that mortgage securitization was "a good thing", which (supposedly) would reduce overall risk in the system – by spreading debt across a larger number of "players" in the market. In fact, the banksters never intended to reduce risk, but rather their plan all along was to dramatically ratchet-up leverage. In other words, instead of simply spreading-out the same amount of debt amongst more entities (which would have reduced risk) they used all the chumps they lured into their schemes as a means of piling-up much more debt – with everyone leveraged-to-the-max. However, the banksters were just getting started. The leverage being created via mortgage securitization was much more dangerous than anything which had ever previously been allowed to exist in any financial system – because not only was the total amount of debt much greater, but it was all interconnected. In the event of a crisis, banks and investors would be nothing more than debt-dominoes – where the failure of one resulted in the failure of all. To pacify so-called "regulators", the banksters pretended that they were "insuring" all of this debt, which (they claimed) would eliminate any and all "systemic risk". The pretend-insurance they created is called a "credit default swap". These are the most-leveraged financial products ever invented in the history of human commerce. A handful of Wall Street Oligarchs (with only $billions in operating capital) claimed to be insuring $60 trillion of the banksters' other scams – an amount equal to total, global GDP. Through the combination of mortgage securitization and credit default swaps, the Wall Street Oligarchs – instead of "reducing risk" (i.e. leverage) – had tripled their leverage, to an average of 30:1 (across the entire U.S. financial system). By itself, this ridiculous level of leverage screams out "Ponzi scheme", but that was literally only half the picture. To create all of this reckless leverage in their Ponzi-schemes, Wall Street had to round-up enough chumps to borrow all of the paper they were creating out of thin air. The problem: real wages for the average American had already been falling steadily for thirty years. Americans were barely able to cope with the level of debt they held before these scams were commenced – meaning they weren't creditworthy enough to justify lending-out one dime more (let alone trillions of dollars). The Oligarchs had a "plan" for that, too: they simply tore-up all lending standards across the entire U.S. financial system. The servant-regulators – and most-notably, New York Fed President Tim Geithner – did nothing. This alone was the greatest regulatory failure in human history. Geithner's "punishment" for serving the banks, instead of the American people? He was promoted to Treasury Secretary, where instead of simply being told to go for a very long nap, he was now given the "privilege" of writing blank-cheques for his Masters. With no lending standards (and no regulators), U.S. financial institutions lent-out three times as much money to the same group of people (Americans), despite the fact they knew it would never be possible for that debt to be repaid. Trillions of dollars of fraudulent mortgages were written-up, which were 100% guaranteed to fail. More articles from Bullion Bulls Canada….

|

| Risk in Everything, Including Gold Posted: 24 Oct 2010 07:50 AM PDT Bullion Vault The market, I mean. Which market, you may ask? Increasingly, it doesn't matter. The zag of the gold market has come to look very much like the stock market's zig. Over the past month, the correlation between the S&P 500 and gold has shot up 60 percentage points. The fact that the coefficient is now at 38% should tell you that it's gone from a risk-neutralizing negative value to a tag-along positive. The turnaround, too, followed a near-vertical trajectory. Not that this hasn't happened before. Over the past two years, the correlation coefficient has dropped with equal velocity, but not risen. There ought to be more than just academic interest in the heightening of the correlation coefficient. From a portfolio standpoint, it lessens gold's utility; in other words, the metal's hedge value diminishes. A persistently positive correlation makes gold less attractive to institutional money managers and hedge funds. There's yet another worrisome risk metric. The rising cost of gold puts. Complacency about gold's unbridled price rise has been replaced by caution as traders seek insurance from bullion's downside volatility.

|

| "Good Time" to Buy Gold Posted: 24 Oct 2010 07:50 AM PDT Bullion Vault While I'm much more focused on buying cheap Gold Mining assets in my Gold Stock Analyst advisory, I know "newbies" want the comfort of a single indicator to forecast gold's future before they climb on board. I've studied the gold market for over 30 years. I've seen it boom and I've seen it bust. And my work says the "Real Interest Rate" is the best forecasting tool for looking at the big picture in gold. Right now, this indicator is saying it's still a good idea to Buy Gold. The Real Interest Rate is the risk-free return on money, adjusted for inflation. It's what you can earn on your cash in the bank. I determine the Real Interest Rate by subtracting the Consumer Price Index (CPI) from the three-month Treasury yield. CPI is the government's gauge of inflation…or how much purchasing power your cash is losing per year. The three-month Treasury yield is the benchmark yield folks can get on their cash at the bank. And when the result of subtracting the CPI rate from the three-month Treasury yield is positive, gold is flat (middle area in chart below). Remember, gold pays no interest. If money in the bank is paying a good interest rate, holding cash is more attractive than holding gold. As you can see from the lower right-hand corner of the chart, we are still in an era of negative Real Interest Rates. At the current 1.1% CPI and a typical 0.1% money market yield, $100 at the start of the year will have only $99 in purchasing power at the end. I see a negative Real Interest Rate condition for the next several years…as the Fed will be unable to raise interest rates due to the high US unemployment rate. And even when the Fed begins raising rates, if it lags the CPI increases as it did in the 1970s, Gold Prices will still move higher. Yes, gold has enjoyed a big run in the past few months. But the Fed is committed to keeping interest rates low for years. So gold has years more to run, I believe…and so do Gold Mining stocks.

|

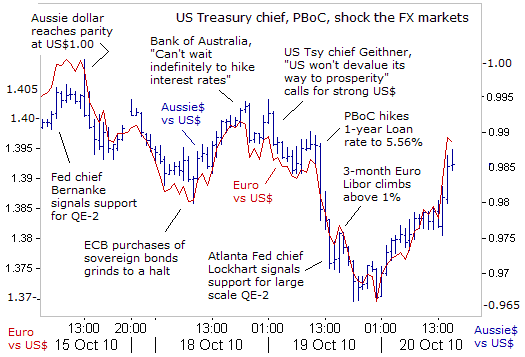

| Who Will Defend the US Dollar? Posted: 24 Oct 2010 07:50 AM PDT Bullion Vault

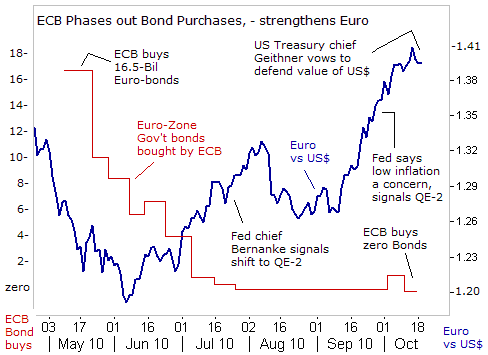

HOW SHOULD traders interpret the latest remarks by US Treasury chief Timothy Geithner, who shocked the currency markets on October 18th, citing his determination to defend the value of the US Dollar? asks Gary Dorsch, editor of Global Money Trends. Geithner was asked in a question and answer forum…

Geithner surprised his audience with a passionate defense of the US Dollar.

Yet just a few days earlier, during a much-anticipated speech on October 15th, Fed chief Ben "Bubbles" Bernanke broadly hinted that he favored an early resumption of "quantitative easing" (QEII), knocking the US Dollar into a tailspin.

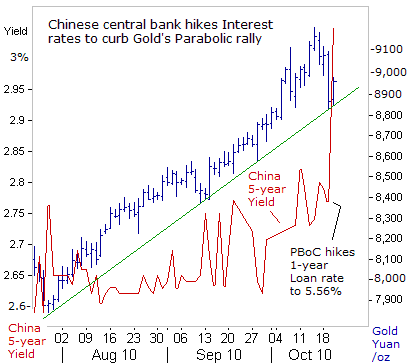

Bernanke took the highly unusual step of making it clear that the Fed's policy going forward would be to raise the rate of inflation to 2% by means of massive money printing. The Fed chairman tried to brainwash the American public into believing that QEII will significantly bring down the jobless rate. Bernanke's support for QEII helped the Dow Jones Industrials index to soar above 11,100…despite further losses in US payrolls and a jump in the under-employment (U-6) jobless rate to 17.1%. The US Dollar also fell to parity with the Canadian Dollar, and hit new all-time lows against the Swiss Franc, and a 15-year low against Japan's Yen. Brazil's Real, Chile's Peso, the Korean Won, and the Indian Rupee rose versus the US Dollar, while Gold Bullion hit a new record high and commodities such as crude oil, copper, corn, cotton, cattle, soybeans, platinum, palladium, rubber, and silver all continued their upward spiral. After Geithner's remarks, the Euro quickly found resistance at $1.400, and began to sink to $1.3935 within a few minutes. The Aussie Dollar dropped 0.80¢ to 98.50¢, before getting blasted again, a few hours later, after China's central bank shocked the markets, by lifting its one-year loan rate a quarter-point to 5.56%, its first rate hike in 3-years, knocking industrial commodities lower. The Aussie plummeted towards 96.50¢ a few hours later, before regaining its footing. The Euro's slide came to a halt at $1.3700, where sidelined buyers emerged. However, 24-hours later, the impact of Geithner's remarks and China's surprise rate hike, had already dissipated into thin air. The Aussie Dollar – a symbol of risk taking – rebounded strongly to 98.75¢, and the Euro recovered to $1.3950. The US Dollar skidded to ¥81, despite threats by the Bank of Japan a few hours earlier to expand its own version of QEIII, beyond the ¥5 trillion of Japanese government bond-buying pledged earlier. Once again, traders resumed their betting on "Bubbles" Bernanke, and a massive tidal wave of QEII, starting after the Fed's next meeting on Nov. 3rd, that would trump the efforts of other central banks to prevent the US Dollar's downfall. A few hours later, Geithner stepped-up his verbal rhetoric, by telling the Wall Street Journal, on October 20th, there's no need for the US Dollar to sink further against the Euro and the Yen, saying these currencies are "roughly in alignment" now. He emphasized that the US Treasury isn't trying to devalue the US Dollar, echoing comments he made in Palo Alto, California. Geithner appeared to offer a secret gentleman's agreement with Beijing, to stop the currency war, if the pace of the Chinese Yuan's appreciation against the US Dollar since September is sustained, to correct its undervaluation.

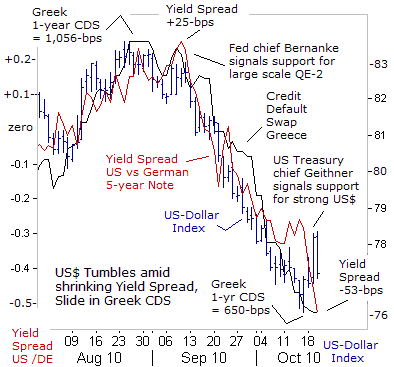

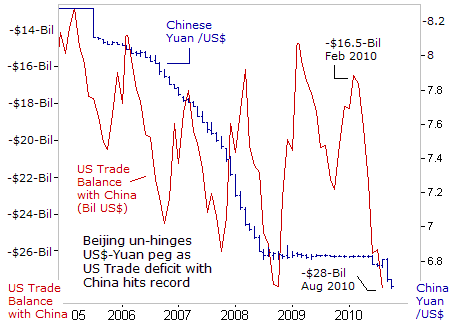

But traders can expect greater volatility and turbulence in exchange rates, with the Group-of-20 nations moving towards the brink of a currency and trade war that is being driven by high unemployment in the United States. President Barack Obama is under heavy pressure from leading Democrats, to declare China a currency manipulator, and to agree to stiff tariffs against Chinese imports. The Fed has meantime engineered the devaluation of the US Dollar, by issuing a steady drumbeat of threats to unleash QEII, upon the world money markets. Bond dealers reckon the Fed could print a minimum of $500 billion in the months ahead, or it might decide to monetize the entire US-budget deficit for this fiscal year, projected at $1.2 trillion. Also greasing the skids under the US Dollar has been the steady slide of US Treasury yields compared to German bund yields. In early September, the US Treasury's 5-year note yielded 25-basis points more than German 5-year yields. Today, the US-Treasury's 5-year note yields 53-bps less. The US Dollar's allure as a "safe haven" currency has also crumbled, as tensions surrounding the Greek bond market continue to subside. Credit default swap (CDS's) rates, measuring the odds that Athens would default on its debts, have dropped in half over the past four months, to around 650-basis points today. Tokyo denounced Beijing for bidding up the Yen by increasing its purchases of Japanese government notes. And since Beijing scrapped a 23-month-old peg to the Dollar on June 19th, and said it would let the Yuan resume a managed "dirty" float, the Yuan has appreciated 2.8% against the US Dollar, but weakened 10% against the Euro.

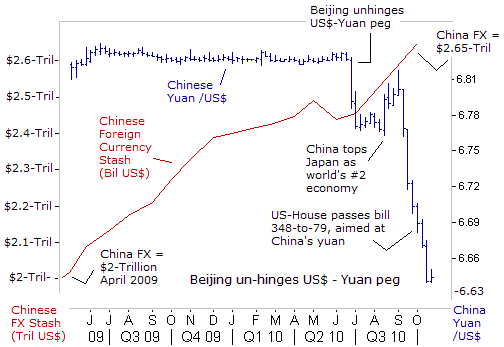

US lawmakers and President Obama have seized upon America's widening trade deficit, which reached $49.7 billion in June 2010, to take aim against the Chinese Yuan. Over the last 12 months, the US-trade deficit with China reached $257 billion, and is running 21% above the pace from a year earlier. The deficit with China as a share of America's balance of payments is now over 40%, compared to just 20% in 2001. Year-to-date imports from China are $229 billion, while exports are only $55.8 billion, leaving the ratio of imports to exports at 4.9. The average for all nations' imports-to-exports with the United States is a ratio of 1.6. Beijing intervenes regularly in its foreign exchange market to rig the value of the Yuan, and it's acquired a massive $2.65 trillion in foreign exchange reserves, while keeping the Chinese Yuan undervalued by 40% against the US Dollar, on a trade-weighted basis. Democrats and Republicans in the US Congress aren't willing to wait for Beijing to revalue the Yuan at a snail's pace over the next several years. In Hong Kong, the 12-month Yuan forward contract is trading at 6.4425 per Dollar, indicating that traders figure that Beijing would only allow the Yuan to rise by a paltry 3.2% rise against the Dollar over the next 12-months. In the past, the Senate has pushed for tariffs of 25% on Chinese imports. "There is no question that China manipulates its currency in order to subsidize Chinese exports," said Republican Senator Richard Shelby of Alabama.

On October 16th, Treasury chief Geithner backed away from a showdown with Beijing over the value of the Yuan, by delaying a much-anticipated decision on whether to label China as a currency manipulator until after the Group-of-20 summit on November 11th.

Geithner said on October 18th, that the delay in the currency report was…

Bank of England Mervyn King warned that the prospect of a trade war over global imbalances could spark a 1930s-style economic collapse:

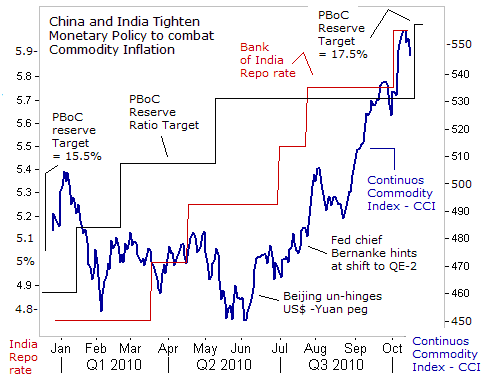

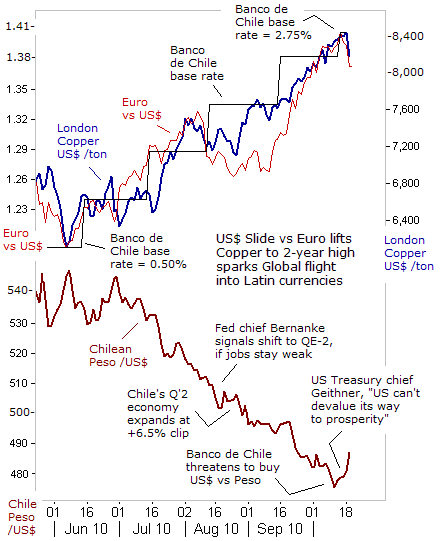

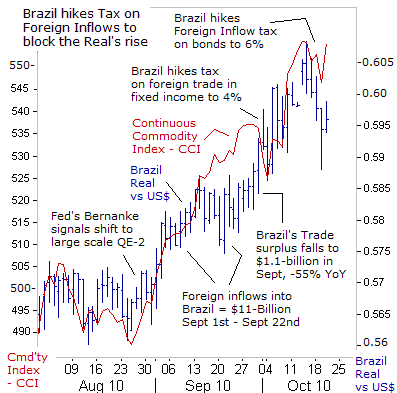

A stronger Yuan is in China's best interest, since it can be utilized to shield the world's biggest buyer of commodities from the sting of sharply higher import prices. But it also acts to push prices higher. Since Beijing un-hinged the tightly pegged Dollar-Yuan peg, and the Fed began sending signals about unleashing of QEII, the Continuous Commodity Index (CCI) – an equally weighted index of 17 different commodity futures, has rallied by 23% to its highest level in two-years. Coffee, cotton, corn, cattle, gold, silver, platinum, soybeans, and wheat have been the stellar performers, with crude oil lagging behind. Other key industrial commodities not included in the index which have skyrocketed are tin, rubber, nickel, and palladium. Efforts by Fed to weaken the US Dollar by threatening to unleash QEII have led to sharply higher commodity prices, and is pushing-up China's inflation rate to 3.5% per year. There's also bubbles brewing in Chinese property prices and renewed interest in Shanghai red-chips. Against this backdrop, the Fed and the US Treasury have exerted considerable pressure on Beijing to allow the Yuan to rise. The People's Bank of China (PBoC) finds it difficult to lift interest rates to combat inflation, because a widening in the Chinese yield spread over US Treasuries would only suck in more "hot-money" into the Chinese Yuan. The rate hike follow on the heels of the PBoC's decision to lift reserve requirements by half-point to 17.5% at six Chinese banks last week, draining CNY200 billion out of the Shanghai money markets. Commodity traders are beginning to wonder if Beijing has just started to roll-out a longer-term tightening campaign. The Reserve Bank of India (RBI) has also been forced to tighten its monetary policy to fend off commodity inspired inflation, by lifting its repo rate on five occasions this year to 6%. India's wholesale prices are 8.5% higher than a year ago, and inflation is far above the RBI's perceived tolerance level of around 5%, keeping the inflation-adjusted interest rate stuck in negative territory. India's economy is now on track to grow at 8.5% this year, lagging only China's stellar growth, so the RBI could be forced to hike its repo rate several more times if commodities continue to spiral higher on the magic carpet ride of the Bernanke's QEII. Amongst resource producers, Chile is among a number of emerging economies, including Brazil, India, Thailand, Korea, and South Africa, whose currencies have risen sharply against both the US Dollar and the Dollar-linked Yuan. These currencies are rising from an influx of foreign capital seeking higher returns than are available in the UK, Japan and the US, where interest rates are hovering near zero-percent. Capital is flooding into emerging markets and could lead to excessive exchange-rate moves, asset bubbles and financial instability, warned IMF chief Dominique Strauss-Kahn on October 18th. Many of these emerging countries are intervening repeatedly in the currency markets to hold down the value of their currency against the US Dollar, and – by default – the Chinese Yuan.

Traders are pouring vast sums of capital into the emerging stock markets, forcing-up the exchange rate of emerging currencies and inflating asset bubbles. Chile posted economic growth of 6.5% in the second quarter, helped by inflated copper prices, which are linked to a staggering 40% of the country's total economic output. Banco-de-Chile chief Jose De Gregorio is now utilizing the direction of copper as a real-time indicator to gauge the forward momentum of the local economy. In sync with higher copper prices, Chile's central bank has also guided its overnight loan rate higher, by 225-basis points to 2.75% last week. In turn, the steady increase in Chile's interest rates has widened the gap with US Treasuries, and has attracted foreign capital – putting more upward pressure on the Chilean Peso. Chile's finance chief Felipe Larrain says:

Brazil's ministry of finance (MoF) is also locked in a bitter struggle with traders over the value of its currency – the Real – in a battle that requires unorthodox techniques. The MoF is desperately trying to halt the appreciation of the real, which has more than doubled in value against the US Dollar since President Lula da Silva took office in 2003. Brazil and its currency are now the darlings of foreign investors. Yet what was once seen as a blessing has become a curse. From January until August, Brazil's trade surplus was whittled down to $11.6 billion, or 41% less than in the same period a year earlier. Finance chief Guido Mantega warned he'll take whatever measures are necessary to keep the real from further eroding Brazil's trade surplus. The Bank of Brazil has resorted to multiple interventions in the currency market to prevent the Real from climbing higher. Brazil's foreign exchange stash now exceeds $250 billion, with $165 billion parked in US Treasuries it's bought to try and buoy the US Dollar. However, the combination of Brazil's robust economy and the world's highest interest rate at 10.75%, has made the real an irresistible target for foreign traders, at a time when Japanese and US bonds are saturated with excess liquidity and ultra-low yields. Brazil should begin to reap bigger trade surpluses in the months ahead, as the latest upward thrust in global commodity prices filters into its economy. Currency dealers are tracking commodity prices, lifting the Real briefly above 60-US¢ last week. Finance chief Mantega says Brazil is engaged in a "currency war" with Bernanke's Fed, and has "a lot of ammunition" such as boosting taxes on foreign investment in Brazilian fixed income. Mantega criticized the Fed for "considering more quantitative easing. It won't reactivate the US-economy, but it will weaken the US Dollar." On October 18th, Brazil hiked taxes on foreign investment in fixed-income bonds to 6%, and also closed a loophole that allows speculators to avoid the tax on margin deposits for transactions in futures markets. The higher taxes will only affect new flows of money into the bond market, not deposits already in Brazil. "This currency war needs to be deactivated," Mantega said. China's central bank (PBoC) surprised traders on October 19th, with its first hike in bank deposit rates in three years, reflecting its concern about rising asset prices and stubbornly high inflation. The PBoC guided 1-year bank deposit rates higher by 25-basis points, to 2.50%, and triggered a 3% drop in the Shanghai gold market. Once a consensus has been forged in Beijing to raise or cut rates, past experience shows that the PBoC moves in a series of adjustments. To date, the PBoC has relied on slowing down bank lending and lifting banks' reserve requirements to keep the growth of the M2 money supply from boiling over. Still, China's Treasury yields rates are too low for an economy that's growing at a 10% clip. The real rate of interest on China's Treasury notes is buried in negative territory – yielding less than the official 3.6% rate of inflation. Negative interest rates are whetting the appetite of Chinese traders in gold, silver, and base metals. The Shanghai stock index, a laggard this year, has jumped 16% in the past nine trading days, led by banks and commodity related companies. Li Daokui, an adviser to the People's Bank of China, said on October 19th:

However, gold traders and speculators in Shanghai red-chips disagree. The amount of cash sitting in China's bank deposits increased by CNY1 trillion ($156 billion) in September, to CNY30 trillion, and could lend plenty of firepower for the Shanghai gold market. On October 20th, China's central bank continued to exert upward pressure on short-term Treasury yields, by draining CNY145 billion ($21.8 billion) from the Shanghai money markets through 91-day reverse repos. The PBOC also mopped-up CNY50 billion by selling one-year T-bills. But There's other channels that can keep the gold market buoyant. The Value Gold ETF is expected to be launched on the Hong Kong Stock Exchange in early November, with the underlying physical gold held at Hong Kong's Precious Metals Depository. The Gold ETF could attract a whole new wave of wealthy investors to the yellow metal, since the Hong Kong Monetary Authority pegs its overnight loan rate at a miniscule 0.50% in order to keep the HK-Dollar fixed to the US currency. Having bought €16.5 billion of Greek, Irish, and Portuguese bonds in the second week of May, the ECB's purchases of bonds slowed to a trickle by early August, winding down its sterilized QE scheme at €63.5 billion. The three-month Euro Libor rate climbed above 1% th

|

| US Commercial Real Estate: "A Mess" Posted: 24 Oct 2010 07:50 AM PDT Bullion Vault FOLLOWING the real estate debacle of the 1980s, Andy Miller co-founded SevoMiller, Inc. in 1990, writes David Galland of Casey Research. The company provided workout services for major financial institutions throughout the United States, and also began buying and developing apartments, retail and office properties. From its founding to the present, the company's acquisitions totaled over 30,000 apartment units, several million square feet of retail space, and numerous office projects throughout the country, including the states of Colorado, Arizona, California, Nevada, Illinois, Texas, Louisiana, Indiana, Oklahoma, Georgia, and Florida. Employing over 500 people, SevoMiller also built, managed, marketed, leased, and sold commercial real estate for many institutions and third-party owners across the country. Clients included General Electric Credit, SunAmerica, and Huntington Bank, as well as many defunct banks, savings and loans, and private equity groups. In 1994, Andy and Dave Frishman co-founded Realty Funding Group, a mortgage and finance company that has acted as a mortgage broker and mortgage banker for numerous commercial real estate projects across the US RFG has provided financing for over $1 billion of commercial real estate. In 1998, Andy founded Rapid Funding, a commercial and residential hard-money lender that has loaned in excess of $200 million for land developments, shopping centers, office buildings, and construction loans on condominium buildings. In addition to sourcing and servicing real estate loans, Rapid Funding also handled its own workouts and sales. Each of these companies founded or co-founded by Andy now operates as part of the Miller Frishman Group. Here, I speak to Andy Miller on behalf of The Casey Report, where readers seek big profits from big trends… David Galland: Given the importance of real estate to the economy, it's not surprising that we get a lot of questions about the sector. What's the buzz in the industry? Andy Miller: Talking about single family, as opposed to commercial real estate, the most visible news story is what happens with the "robo signing" scandal and the foreclosure moratorium. The short answer is that we don't know the full implications yet. A lot will depend on how inclusive this becomes in terms of which lenders will also adopt this moratorium, in how many states, and for how long? All those questions have yet to be answered, but as a generic comment, I'll say this; if what happens results in a concerted effort to impede or stop or delay foreclosures throughout the country, it's going to have a very, very big impact. It's going to have an impact in some ways that are obvious, and some ways that aren't so obvious. We believe there are roughly 8 million loans now in some stage of default or foreclosure. If those 8 million loans are impeded, if the time that it takes to foreclose is extended, or if state attorney generals won't let lenders start foreclosures, that will have serious repercussions. Paradoxically, because it will reduce the number of foreclosures and short-sales coming to market, one of the things you may see is the home market improve slightly over the next three to five months. That may seem like a blessing to the politicians as it will certainly staunch some of the negative news headlines out there around foreclosures, but it doesn't do you any good because ultimately the price paid for the short-term abatement in the news cycle could be high. DG: Okay, so that's a plus for the political optics of the situation, but what about the flipside? Andy Miller: Well, for starters you have to ask what impact this will have in the mid to long term on the ability to sell mortgage-backed securities into the marketplace? If you're an investor or institution that's already loaded up on a bunch of mortgage-backed securities and your master servicers or your special servicers are saying, "We're really stuck in this mire right now where we can't foreclose or address our defaults," how much more of this paper are you going to want to buy? I don't think very much. Now, the truth is that the Fed is buying a lot of these things, but at some point in time, it is going to need to divest itself of the trillions of Dollars of mortgage-backed securities, and who's going to want to buy those, and at what yields? I mean, if you know that with the swipe of a pen, an attorney general can impose a moratorium or somehow prohibit you from doing foreclosures, that has to have dire implications for the future of mortgage-backed securities. DG: Then there's the moral hazard. Andy Miller: Absolutely. If you're a hard-working person who has stayed current on your mortgage even at some hardship to yourself, and your neighbor who's been living in his home for 12 or 15 months without making payments comes over to the barbecue on Saturday afternoon and tells you, "Oh by the way, my foreclosure has been blocked. It looks like I get to live here another 12 or 18 months scot-free," does that encourage anybody else to do the same? It's very hard to know, David, but it doesn't do the market any good. As you know, it's my contention that the only thing that's going to fix this situation is to let the free market deal with the issues so that prices can settle at their own level. All these machinations to manipulate foreclosures and/or prices and/or interest rates are only exacerbating the already bad consequences for the home market. DG: What should concern investors in all of this? Andy Miller: Frankly, we can't know yet. There are too many variables still unsettled. What I would advise is that everybody should be acutely aware of what's happening right now, and once we really know how much time this is going to take and what lenders are most involved, only then will we be able to interpret how bad this is going to be and what the risks are. But right now it's unknown. It just doesn't look very good. DG: What about commercial real estate? Andy Miller: In contrast with the residential housing market, on the commercial side everybody has the giggles. I've never seen anything like it. It's a real paradox, because there's a very active commercial market right now with all kinds of money entering the market and paying ridiculously high prices for assets, and it is almost as if the crisis never happened. In some cases, meaning some states and some product types, we are actually seeing commercial real estate prices at about what they were in '07. DG: These are people looking to deploy their cash into tangible, productive assets? Andy Miller: Yes. There's a lot of institutional money on the sidelines earning no yield that is increasingly being deployed. A lot of this hot money has found its way into commercial real estate. There are very few individual buyers out there that are actually laying out their own money to buy product – this is mostly institutional money, which means the buyers are using other people's money to chase product, and we see that acutely. DG: So these institutional money managers are often given time limits during which they have to deploy the money they are entrusted with, or return it to the investors. And so the buying can become fairly indiscriminate. Do these chickens come home to roost at some point? Andy Miller: Yes, absolutely. David, the commercial business is a mess. The fundamentals are not improving. We've talked about this before, but just to reiterate, you have to start by asking, what constitutes a recovery in commercial real estate? Everybody is very convinced right now that we're seeing a recovery. In commercial real estate, we can be specific in defining what that actually means. Recovery means one or more of three things are happening: either your rents are going up, your expenses are going down, or your vacancies are going down. That's it. In order for commercial real estate to be in recovery, one or more of those factors have to be present. That is a recovery. If you measure each section of the United States, if you look at all the various product types within those states, those fundamental factors are not improving, meaning there is no recovery happening. In fact, I would argue that they're eroding. DG: What about the banks? Recently money manager Chris Whalen made the case that despite being given essentially free money by the Fed, and lots of it, the big banks are still in deep trouble over their mortgage portfolios. Andy Miller: The banks have been very fortunate because they've managed to squirrel away a lot of money into their reserves, at least those institutions that focus on the commercial side. This is not true on residential. On the commercial side, I think they are very heavily reserved for a lot of what they see as their problems. Most of the banks that I come into contact with feel very comfortable that they have adequate reserves, so that no matter what happens to commercial real estate, they believe they're covered. DG: I guess we'll find out in time if they are. Andy Miller: Yes, we will. Even so, I don't think commercial is the big Achilles heel for these institutions right now because of the manipulations the federal government has undertaken. I think the real Achilles heel for all these banks, and for bond markets, is going to be the residential markets. Not to be overly dramatic, but this is a huge ticking time bomb. Things are getting worse, not better. In fact, what we see now is that the distress is moving up the scale. The single-family home markets under $350,000 in a lot of the country are fairly sound. There is a pick-up in sales activity and lending. But when you get to the mid and the upper ends of the marketplace, there's no upward mobility. In other words, people aren't selling less expensive houses in order to trade up, which was very much going on in the housing bubble. In fact, people are having a very difficult time in the mid and upper ranges selling their homes. For one reason: it is now very difficult to finance these homes without a large down payment. We've watched that situation closely and think that's going to really exacerbate the problems in the market. DG: How serious do you think the problems in loan origination documents are? Andy Miller: It's certainly problematic, and there was a lot of sloppiness when these loans were securitized and sold off. Who knows where the original documents are or what shape they are in? I can tell you, however, that if you lose an original note and you have to file a foreclosure, it's not the end of the world. You can have that addressed by a title company, but it's expensive and it's time consuming. But at this point we don't know the extent to which documents are lost, poorly executed, or don't exist. For the time being, Bank of America has put a national moratorium on foreclosures. In order to understand how big a problem this really is, I think we have to wait and see who else follows suit, and how long this will last. If you take this to its nth degree and you assume that the worst case unfolds, it's bad. It's going to look good in the short run, but it's really bad for the market, and it's really bad for homeowners going forward. DG: Obama's refusal to sign the bill regarding electronic notarizations strikes me as being based as much on politics as anything. After all, ahead of an election, it wouldn't do to be seen signing something considered supportive of foreclosures. So the administration has just kicked the can down the road, past the election. Andy Miller: At this point I would judge every event and every news story that you see by just one criterion, and that is that the government is doing everything it can to slow down or impede the foreclosure process. So whether the president signs something or doesn't sign something, or says something or doesn't say something, the intent is to do whatever it takes to impede or slow down this crisis. If there are losses to mortgage holders and investors, the politicians will try to turn this to their advantage by framing it as being that the banks and mortgage lenders deserve the losses because they're the cause of this problem. That's what you're going to see, that's what you're going to hear, and it's all intended to be a feel-good solution that makes everybody believe that our government is really looking out for us. Meanwhile, the SOBs that originated all these mortgages are going to get what they deserve. DG: But ultimately this has to be resolved – that is unless the government is willing to give a bunch of people free houses… Andy Miller: Years ago I said to you that what was happening in real estate was going to culminate in a big crisis, but that if it were to happen in a measured way that let the free market do what it does best, then the crisis would be less intense. But the latest developments are going to create a lot of intensity and only make things worse. Andy Miller: The nice thing about being the federal government is that you can throw Fannie and Freddie under the bus and suffer no real consequences, at least not in the short term. For most people, that will look good. The important thing for your readers to remember is that these aren't solutions that do anything. These are solutions that have optics, that's all. There's an election coming up. The government wants people to feel good. They want everybody to feel like our government is really addressing these problems. They want it to seem to the public like the government cares. And that's what this is, that's what this is all about, in my opinion, and I think you're going to see some really very, very undesirable, unintended consequences. DG: And on that note, thank you very much for your time. Very interesting, as always. Andy Miller: Happy to help out. Let's talk again soon. Got gold? Start with a free gram of physical gold right now at BullionVault…

|

| Posted: 24 Oct 2010 07:49 AM PDT Bullion Vault GREAT NEWS! says Dan Denning in his Daily Reckoning Australia. NASA researchers say there is at least a billion gallons of water on the moon. And that's just in one crater! They published the findings in the journal Science. So raise a glass to la bella luna! This means that if the accelerated depletion of natural resources by the limitless printing of fake money continues – and there's a pretty good chance it will – we'll have to find a new home with new resources to put to good use after this planet has been looted and depleted into a scorched and lifeless husk, like the moon. The other good news is that the moon is pretty close, physically speaking. You just look right up in the sky and it's there! It looks so close you could almost touch it. It was especially beautiful and silvery when we woke up at 3am last night wondering what the Gold Price would do today. But speaking of gold brings us back to sliver. Scientists say there is some silver on the moon as well, but not enough to mine. That's okay, though. There's no need to hop on Virgin Galactic flight to the moon for your silver. You can buy it for US$23.19 per ounce. That's 31% more than you would have paid if you bought a year ago. But it's 5.8% less than sliver was selling for just last week.